Money arguments don’t magically stop the day you stop working; they just change focus. Instead of arguing about saving for a down payment or funding college tuition, retired couples often clash over withdrawal rates, Social Security timing, and whether to financially support adult children. These disagreements are more than just a source of daily friction—they carry severe financial consequences that can permanently alter your retirement trajectory. Unresolved money conflicts can lead to premature portfolio depletion, thousands of dollars lost in tax inefficiencies, or even the devastating wealth destruction of a gray divorce. Understanding the root causes of these late-in-life financial battles is your first step toward protecting your nest egg and preserving your peace of mind.

The Heavy Toll of the Spender Versus Saver Dynamic

Throughout your working years, the tension between a spouse who loves to spend and a spouse who prefers to save is somewhat masked by a continuous stream of incoming paychecks. However, once you retire and transition to living off a finite portfolio, this dynamic often erupts into full-blown conflict. The saver feels an intense need for security, viewing every withdrawal as a threat to their future survival. Conversely, the spender believes they sacrificed for forty years specifically to enjoy this time, viewing excessive frugality as a tragic waste of their golden years.

The financial cost of failing to reconcile these two mindsets can be steep. If the spender acts recklessly and bypasses budgetary agreements, they expose the couple to longevity risk—the very real danger of running out of money at age eighty-five. On the other hand, if the saver completely dominates the finances, the couple may fall victim to cash drag. Holding too much money in low-yield cash equivalents out of a paralyzing fear of the stock market ensures that inflation will steadily erode your purchasing power. Over a twenty-year retirement, inflation is a mathematical certainty that will devastate a cash-heavy portfolio.

To find equilibrium, successful couples often agree on an overarching annual withdrawal rate, such as a modified 4% rule. Once the saver sees that the mathematical framework is secure and sustainable, they can more easily release their grip on the purse strings, allowing the spender to use the allocated “fun money” without triggering feelings of guilt or resentment.

The Social Security Standoff: When to Claim?

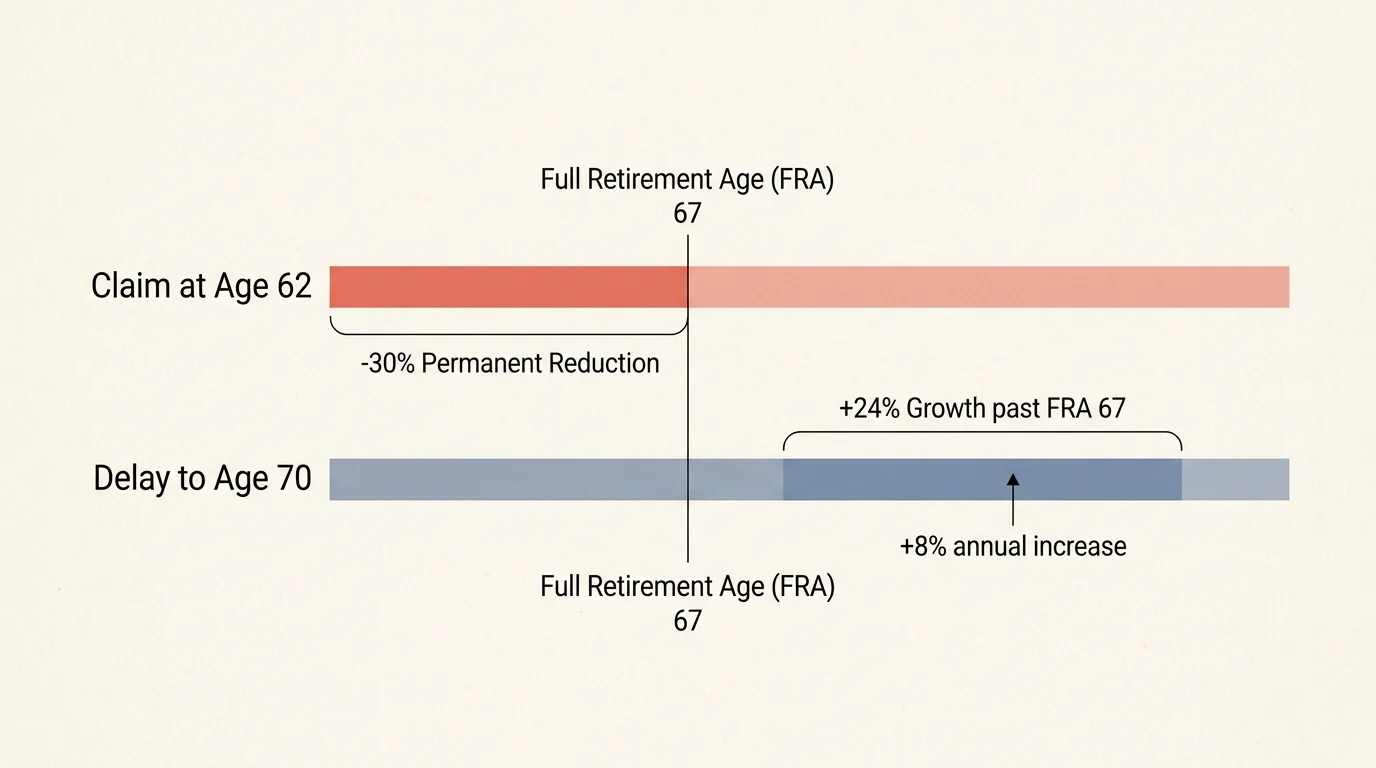

Deciding when to file for benefits with the Social Security Administration (SSA) is one of the most mathematically consequential choices you will make in retirement. It is also a primary battleground for married couples. One spouse may demand to claim as early as possible at age 62 to grab the cash while they are young and healthy. The other spouse may insist on waiting until age 70 to lock in the highest possible guaranteed monthly payout.

The stakes of this argument are incredibly high. For individuals born in 1960 or later, full retirement age (FRA) is 67. If you claim at age 62, you accept a permanent 30% reduction in your monthly benefit. However, if you delay claiming past your FRA, your benefit grows by 8% for every year you wait, up to age 70. This means a benefit taken at 70 is substantially larger than one taken at 62.

The most overlooked cost in this argument is the impact on survivor benefits. When one spouse passes away, the surviving spouse inherits the higher of the two Social Security payments and the smaller one disappears. If the higher-earning spouse forces the decision to claim at 62, they permanently handicap the survivor benefit. Should that higher earner pass away first, the surviving widow or widower is locked into that heavily reduced monthly check for the rest of their life—a mistake that can easily cost a surviving spouse hundreds of thousands of dollars in lost lifetime income.

| Claiming Age | Impact on Monthly Benefit (Assuming FRA of 67) | Strategic Consideration |

|---|---|---|

| Age 62 | 30% permanent reduction | Provides immediate cash flow; suitable if facing severe health issues or depleted savings. |

| Age 67 (FRA) | 100% of Primary Insurance Amount | Offers the standard baseline benefit; a balanced approach for those stopping work entirely. |

| Age 70 | 124% of Primary Insurance Amount (8% increase per year delayed) | Maximizes lifetime payout and secures the highest possible survivor benefit for a spouse. |

The Invisible Drain of Supporting Adult Children

Many couples find themselves bitterly divided over how much financial assistance to provide their adult children. One parent may feel a deep emotional obligation to help fund a grandchild’s education, cover a grown child’s rent, or offer a down payment for a house. The other parent may watch the retirement accounts shrink and urge for financial boundaries to be drawn.

The financial toll of keeping the “Bank of Mom and Dad” open is staggering. A 2026 study by Standard Life revealed that 27% of parents providing financial support to adult children were forced to dip into their own savings, while 15% ended up delaying their retirement or accepting a diminished lifestyle to afford the subsidies. Furthermore, recent survey data shows that simply housing an adult child costs parents an average of $459 per month.

When you subsidize an adult child, you are not just losing the cash you hand over; you are losing the compounding interest that money could have earned in a retirement account. For example, if you withdraw $10,000 from a traditional IRA to bail out a child’s credit card debt, you must actually withdraw significantly more to cover the taxes on that distribution. Protecting your own financial stability must come first. A unified front is essential; couples must agree on hard limits regarding familial support to prevent their generosity from dismantling their own financial security.

Healthcare Surprises and Medicare Premium Traps

Medical expenses represent one of the largest outflows in retirement, and couples frequently argue over how to manage them. Disagreements usually center on whether to purchase comprehensive supplemental coverage or risk going without it to save on monthly premiums. However, the most expensive fights occur when couples mismanage their income and accidentally trigger Medicare surcharges.

For 2026, Medicare.gov outlines that the standard Part B premium is $202.90 per month, with an annual deductible of $283. What many couples fail to realize is that Medicare premiums are tied to your modified adjusted gross income (MAGI) from two years prior. If you and your spouse argue over making a large, uncoordinated withdrawal from a traditional IRA to buy a boat or pay off a mortgage, that massive influx of taxable income can easily push you over specific thresholds.

Crossing these lines triggers the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA is a stealth surcharge that can more than double your Medicare Part B and Part D premiums for an entire year. A single disagreement over a lump-sum withdrawal can quietly siphon thousands of dollars out of your fixed income down the road. Coordinating major purchases and strategically pulling from different tax buckets is vital to keeping healthcare expenses predictable.

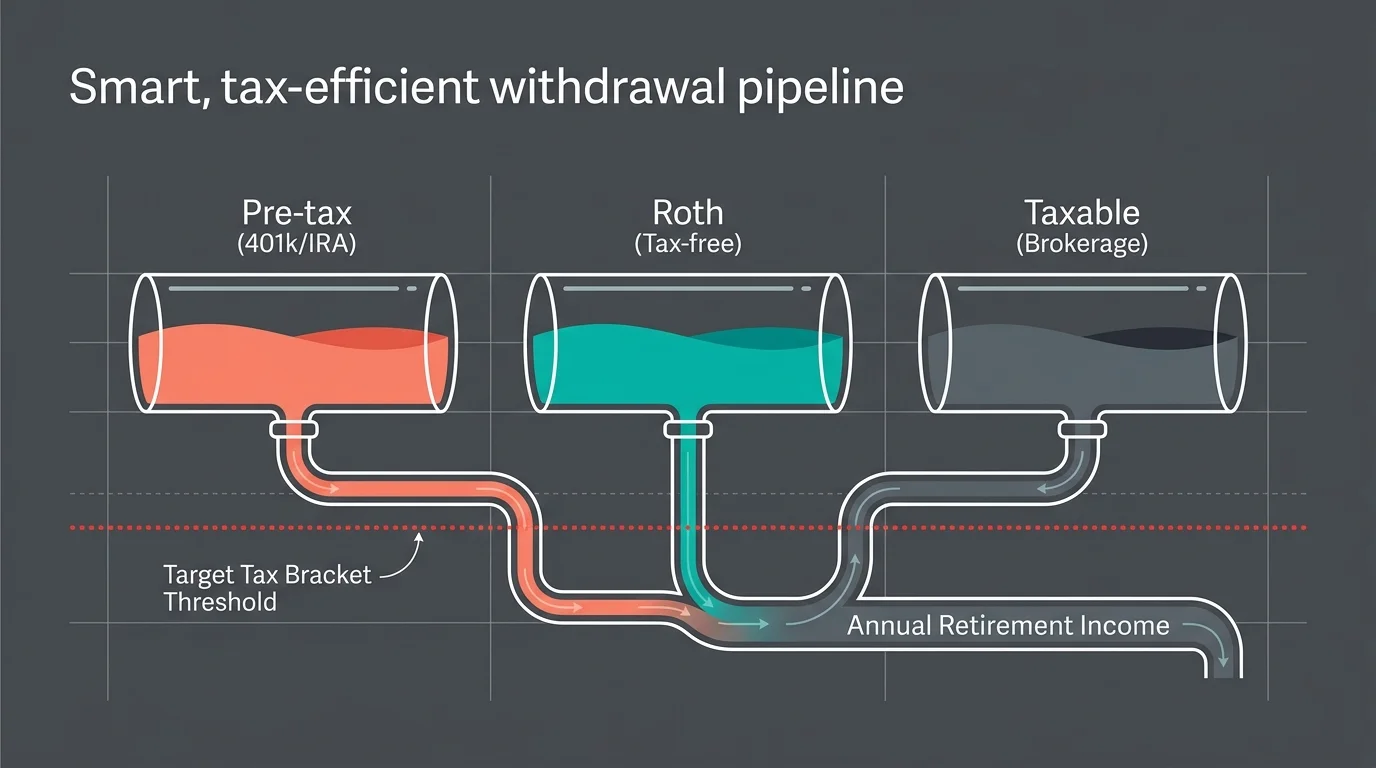

Tax Bracket Mismanagement and Withdrawal Strategies

Without the structure of an employer’s payroll department withholding taxes, retirees are fully responsible for their own tax planning. Couples often clash over where to pull cash from—a traditional IRA, a Roth IRA, or a taxable brokerage account. When spouses act independently and fail to communicate their withdrawal strategies, they invite the Internal Revenue Service (IRS) to take a much larger slice of their wealth.

Understanding current tax laws provides a major advantage. For tax year 2026, the standard deduction for married couples filing jointly is $32,200. Additionally, Congress implemented a temporary Senior Bonus Deduction spanning 2025 through 2028, which offers an extra $6,000 deduction per person for those 65 and older. Consequently, a married couple where both spouses are over 65 can shield up to $44,200 of income from federal taxes before paying a single dime.

If couples argue and fail to utilize this massive deduction efficiently, they leave money on the table. For instance, withdrawing $80,000 entirely from a tax-deferred IRA might push you into a higher tax bracket and cause up to 85% of your Social Security benefits to become taxable. A coordinated strategy—where you withdraw just enough from the traditional IRA to fill the 0% and lower tax brackets, and then pull the remainder from a tax-free Roth account—requires teamwork but saves thousands of dollars annually.

Investment Risk: Playing It Safe Versus Seeking Growth

Transitioning from wealth accumulation to wealth preservation is jarring. It is incredibly common for one partner to suddenly want to liquidate all equity positions and hold only cash or certificates of deposit (CDs), terrified of a stock market crash. Meanwhile, the other partner, perhaps having spent time reading resources from Fidelity Retirement or Vanguard, understands the absolute necessity of keeping money invested to outpace inflation.

This tug-of-war is exhausting and financially hazardous. If the conservative spouse wins and liquidates the portfolio during a market dip, they lock in losses that the portfolio may never recover from. If the aggressive spouse insists on remaining 100% in stocks at age seventy, the couple faces immense sequence of returns risk—where a poorly timed bear market early in retirement can permanently cripple the nest egg.

Couples must find a mathematical middle ground. Utilizing a bucket strategy is highly effective here. By placing one to three years of living expenses in guaranteed, safe assets like cash and short-term bonds, the conservative spouse gains peace of mind. The remaining assets can then be invested in a globally diversified portfolio of equities to ensure long-term growth for the decades ahead.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

The Ultimate Cost: The Financial Reality of Gray Divorce

When financial arguments fester for years without resolution, they can ultimately destroy the marriage. The phenomenon known as “gray divorce”—couples splitting up after age 50—has doubled since 1990 and now accounts for over a third of all divorces. The economic consequences of divorcing near or during retirement are absolutely devastating.

According to longitudinal data from the Health and Retirement Study, women experience a shocking 45% decline in their standard of living following a gray divorce, while men experience a 21% drop. Both spouses typically suffer roughly a 50% loss in their total wealth. The mechanics behind this wealth destruction are straightforward: you are taking a single retirement portfolio meant to support one household and splitting it in half to support two entirely separate households in a high-inflation environment.

Divorcing late in life means you lose all economies of scale. You now have two housing payments, two sets of utility bills, and two property tax bills, all funded by a fractured nest egg. While repartnering can reverse some of these economic costs, relying on finding a new partner to achieve financial stability is a highly risky retirement plan. Resolving money conflicts through counseling or mediation is almost always cheaper than funding a gray divorce.

Professional vs. Self-Guided: Resolving Money Conflicts

When you hit an absolute standstill on how to handle your retirement assets, you face a choice: continue trying to hash it out at the kitchen table or bring in an objective third party.

Managing your finances yourselves works beautifully when both partners have a solid grasp of retirement mechanics, communicate without hostility, and share similar lifestyle goals. If your only disagreements are minor—such as whether to spend $3,000 or $5,000 on an annual vacation—you can likely resolve them through routine budgeting check-ins.

However, you should seek professional guidance when:

- Emotions override math: If conversations about money consistently devolve into bitter arguments about past mistakes, a financial advisor can act as an impartial mediator who focuses solely on the numbers.

- Tax strategies become complex: Navigating Roth conversions, managing IRMAA thresholds, and optimizing standard deductions requires precise calculations. A certified professional can execute these moves efficiently.

- Estate planning is contested: If you are a blended family arguing over inheritance distributions and trust structures, relying on a professional estate attorney and a financial planner is essential to prevent costly legal battles for your heirs.

Bringing in a fiduciary shifts the dynamic entirely. Instead of one spouse dictating financial rules to the other, an expert evaluates the data and recommends the safest, most logical path forward.

Common Mistakes to Avoid When Managing Joint Finances

Retirement amplifies the impact of everyday financial errors. To protect your marriage and your life savings, make sure you and your spouse avoid these frequent pitfalls:

- Operating in financial silos: Keeping secret credit cards or hiding purchases—often referred to as financial infidelity—destroys trust. You must maintain complete transparency regarding all debts, assets, and spending habits. If you cannot look at the statements together, you have a structural problem in your plan.

- Ignoring the survivor’s lifestyle: Spouses often argue about buying life insurance or taking a single-life pension payout just to get a slightly larger monthly check today. If the higher-earning spouse passes away, the surviving spouse could be left with a drastically reduced income. Always model what the household finances will look like for the surviving partner.

- Failing to update legal documents: If you constantly fight about estate planning and simply decide to ignore it, you leave your assets vulnerable to probate courts. According to AARP and legal experts, beneficiary designations, wills, and powers of attorney must be updated regularly and fully agreed upon by both partners.

The Bottom Line

Your retirement years should be a time to reap the rewards of a lifetime of hard work, not a period defined by financial anxiety and marital strife. By addressing the root causes of your money arguments—whether they stem from Social Security claiming strategies, supporting adult children, or investment risk—you can build a unified financial plan that protects both your wealth and your relationship.

Open communication, a willingness to compromise, and a shared vision are your best tools for a successful retirement. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: July 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.