Pitfalls to Watch For

While working in retirement offers incredible benefits, earning a paycheck while claiming senior benefits requires careful navigation. A lack of planning can trigger unexpected tax bills or reductions in your government benefits.

The Social Security Earnings Limit

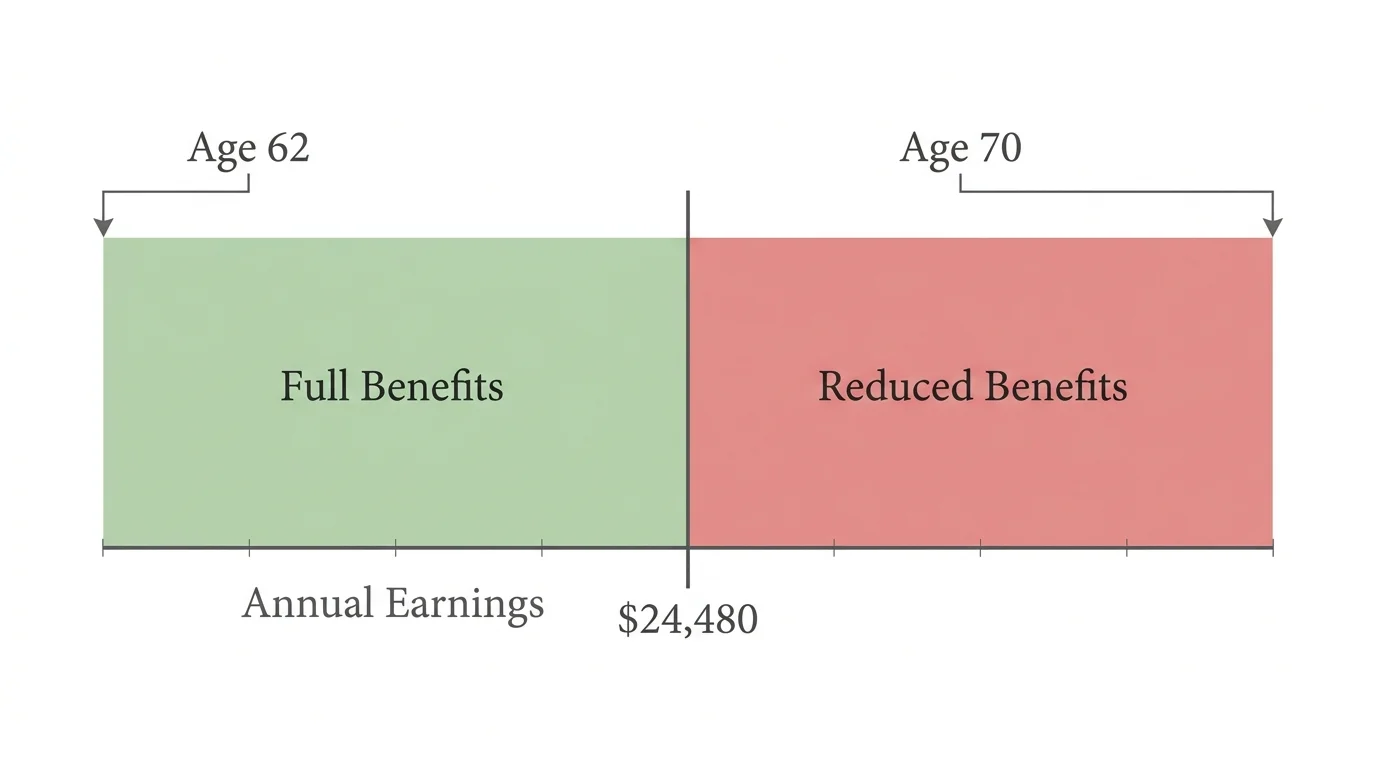

If you claim Social Security before reaching your Full Retirement Age (FRA)—which is 67 for anyone born in 1960 or later—the government limits how much you can earn from working. For 2026, the annual earnings limit is $24,480. If you earn more than that, the Social Security Administration (SSA) will withhold $1 in benefits for every $2 you earn above the threshold.

If you will reach your FRA during 2026, the rules are more lenient. The limit jumps to $65,160 for the months prior to your birth month, and the penalty drops to $1 withheld for every $3 earned. Once you officially hit your Full Retirement Age, the earnings limit disappears entirely, and you can earn millions without facing any benefit deductions.

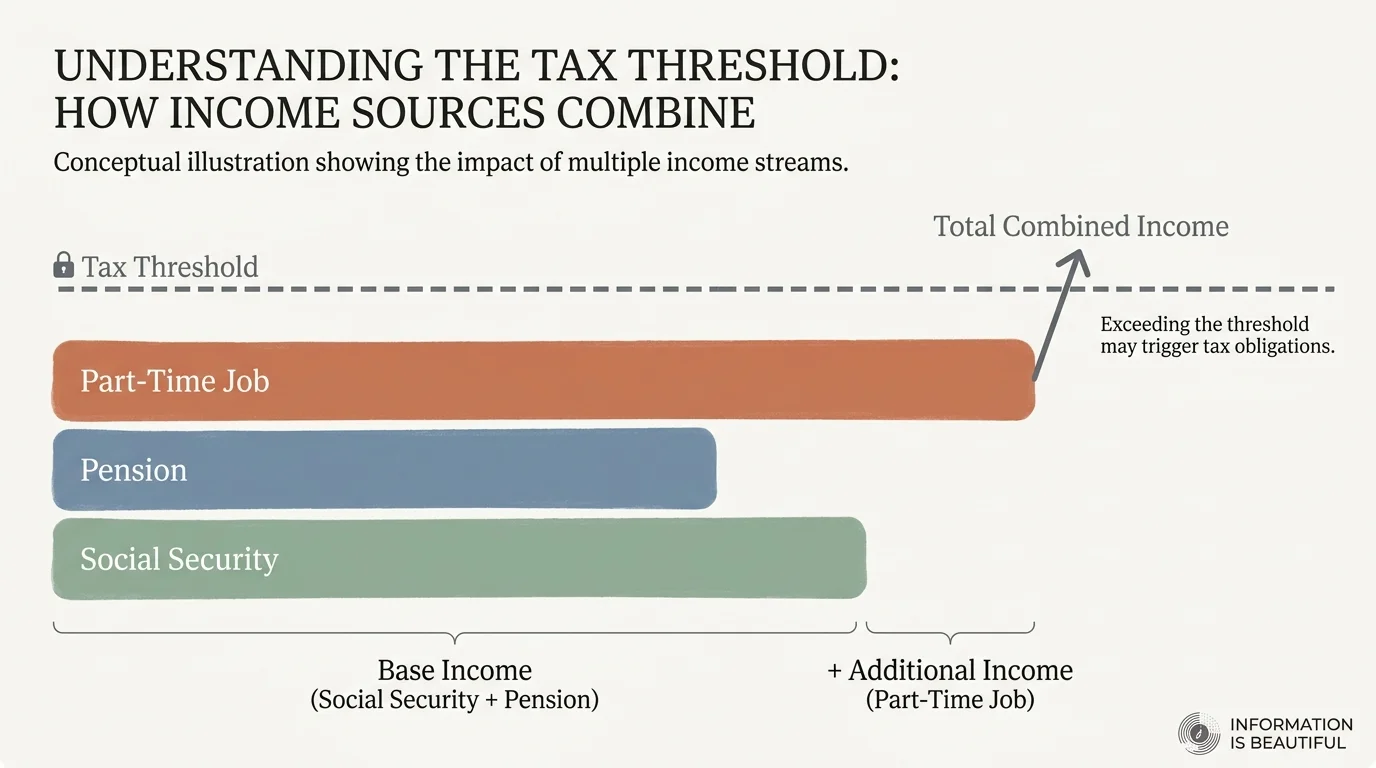

Tax Bracket Creep and Benefit Taxation

Your part-time income might push your total income into a higher tax bracket. More importantly, it can trigger the taxation of your Social Security benefits. If your “combined income” (your Adjusted Gross Income + nontaxable interest + half of your Social Security benefits) exceeds certain thresholds, up to 85% of your Social Security benefits become subject to federal income taxes. You must factor this hidden tax cost into your decision to work.

This is a wonderful acknowledgement and a bright guiding light for many seniors’ futures I’m sure.

please send me jobs part time in the Villages Florida or Leesburg Florida area I am retired would like to find an easy simple job may part time working with animals I love animals just an example of what I like to do Thank you

Please send me a list of part time positions for seniors in the Washington, DC area. I would really

appreciate it. Thank you.

Hello there! My name is A. Atkins. I am a Senior seeking a part time job. I enjoy typing and

data entry. Are there any of those jobs available anymore? I miss typing for a living. The last

position that I held was very enjoyable because I could use those skills. Please let me know how

to apply as I am truly interested. Thank you.

Please send me information on part time jobs for seniors that they will enjoy.