Filing for Social Security is often viewed as the final step in a successful retirement plan, but treating it like a straightforward finish line is a mistake that costs millions of retirees dearly. Once you activate your benefits, an entirely new set of government rules takes over—dictating how much you can earn, how your benefits are taxed, and what your spouse is entitled to receive. Many retirees file their paperwork expecting a predictable monthly paycheck, only to be blindsided by hidden taxes, earnings penalties, and automatic deductions that significantly reduce their actual take-home income. Understanding these regulations before you claim your benefits is the only way to protect your retirement income and ensure you keep every dollar you deserve.

At a Glance: Critical Rules to Know Before You Claim

- Working while claiming has limits: If you collect benefits before your Full Retirement Age (FRA) and continue to work, the government will temporarily withhold a portion of your checks once you exceed the 2026 earnings cap of $24,480.

- Benefits are rarely tax-free: A formula called “provisional income” dictates whether your benefits are taxed. Depending on your other income sources, up to 85% of your Social Security payments may be subject to federal income tax.

- Your net check will be lower at 65: Once you enroll in Medicare, your Part B premiums (and potential high-income surcharges) are automatically deducted from your Social Security payment before the money ever hits your bank account.

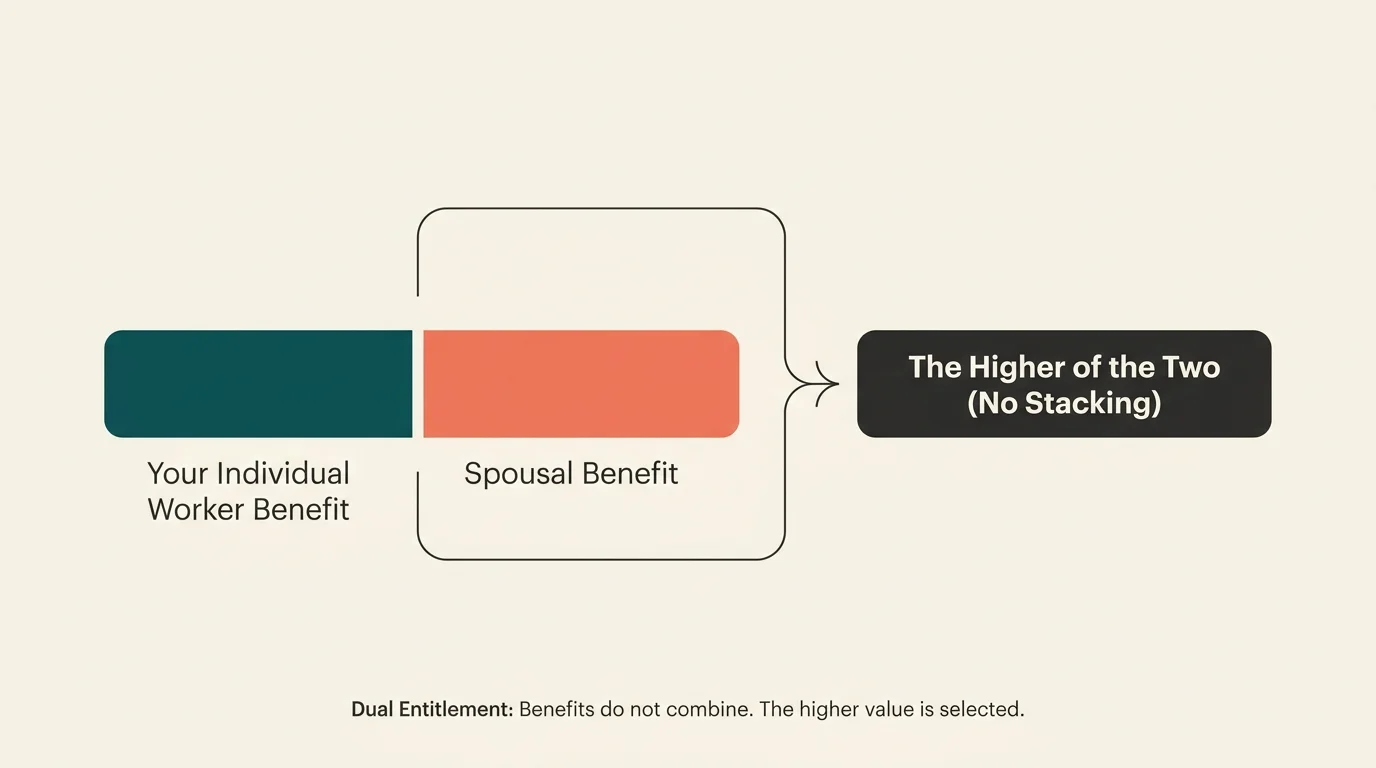

- Spousal benefits do not stack: You cannot collect your full individual worker benefit plus a full spousal benefit; the Social Security Administration pays the higher of the two amounts.

- Payments are handled strictly in arrears: You must live through the entirety of a calendar month to be legally entitled to that month’s benefit check.

1. The Retirement Earnings Test Temporarily Slashes Your Checks

Many Americans choose to transition into retirement gradually, claiming their Social Security benefits at age 62 while continuing to work part-time or even full-time. If you follow this path, you will run straight into the Social Security Administration’s retirement earnings test. This rule applies exclusively to those who claim benefits before reaching their Full Retirement Age (FRA), which is 67 for anyone born in 1960 or later.

If you are under your FRA for the entire year of 2026, the government allows you to earn up to $24,480 from a job or self-employment without any penalty. However, for every $2 you earn above that specific threshold, the SSA will withhold $1 from your Social Security benefit. If you earn significantly more than the limit, your monthly checks can be suspended entirely for several months of the year.

The rules soften slightly during the calendar year in which you actually reach your FRA. For 2026, the earnings limit jumps to $65,160 for that transitional year. During this period, the SSA withholds only $1 for every $3 you earn above the limit, and they only count the wages you earn in the months prior to your birth month. Once your birth month arrives and you officially hit Full Retirement Age, the earnings limit disappears completely; you can earn a million dollars a year, and your Social Security checks will not be reduced by a single cent.

The good news is that the money withheld by the earnings test is not confiscated forever. When you reach Full Retirement Age, the SSA automatically recalculates your benefit upward to give you credit for the months your checks were withheld. Over your lifetime, you get the money back in the form of a slightly larger monthly payout. However, the immediate cash flow shock of receiving a letter stating your next three checks are suspended is deeply stressful for retirees relying on that money to pay their daily living expenses.

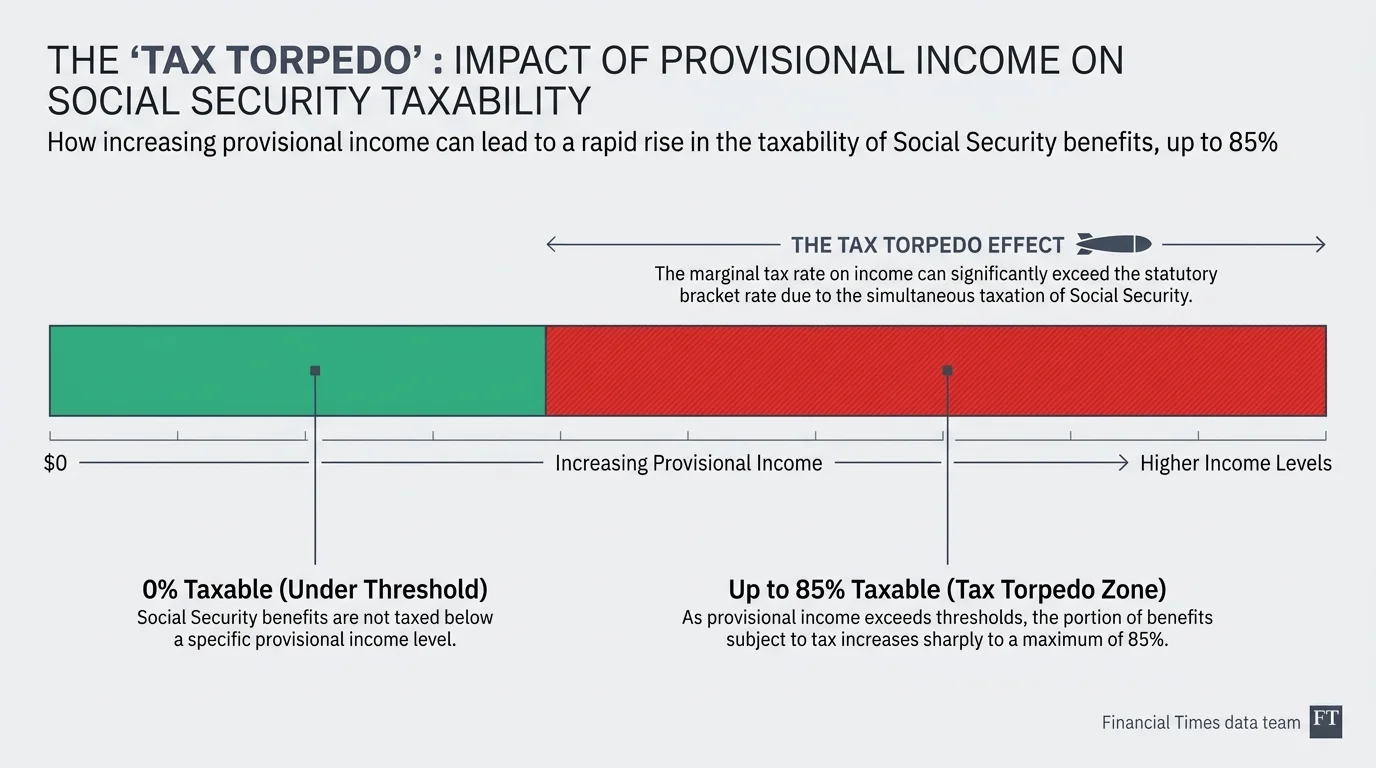

2. The “Tax Torpedo” Can Expose Up to 85% of Your Benefits to the IRS

There is a persistent myth that because you paid taxes on your wages to fund Social Security during your working years, the benefits you receive in retirement are tax-free. Unfortunately, this has not been true since 1984. Today, millions of retirees fall victim to what financial planners call the “tax torpedo”—a sharp spike in marginal tax rates caused by the way the IRS calculates the taxation of Social Security benefits.

The IRS uses a specific formula called “provisional income” (also known as combined income) to determine your tax liability. You calculate provisional income by adding your Adjusted Gross Income (which includes traditional IRA withdrawals, wages, and pensions), any nontaxable municipal bond interest, and 50% of your annual Social Security benefits.

Because the thresholds for this calculation were established decades ago and were never indexed for inflation, more retirees are pushed into taxable territory every single year as standard living costs rise.

| Filing Status | Up to 50% of Benefits Taxable | Up to 85% of Benefits Taxable |

|---|---|---|

| Single / Head of Household | $25,000 to $34,000 | Over $34,000 |

| Married Filing Jointly | $32,000 to $44,000 | Over $44,000 |

If your provisional income crosses the upper threshold, up to 85% of your Social Security benefits must be reported as taxable income on your federal return. This creates a compounding tax problem: taking a $1,000 withdrawal from a traditional 401(k) to fix a leaky roof increases your standard taxable income, but it also increases your provisional income. This can suddenly pull another $850 of your Social Security benefits into the taxable bracket, meaning that single $1,000 withdrawal could increase your taxable income by $1,850. The resulting effective marginal tax rate can easily devastate your net spendable income.

“Taxes are the biggest challenge for investors approaching retirement. As an advisor, if you can help people keep more of the money they’ve made and make it last through retirement, that’s where the value is.” — Ed Slott, CPA and Retirement Tax Expert

To navigate the tax torpedo, retirees must look to IRS Publication 915 and proactively plan their income streams. Drawing from Roth accounts—which do not count toward your provisional income—can help you maintain the cash flow you need without triggering higher taxes on your Social Security benefits.

3. Medicare Part B Premiums Are Automatically Deducted from Your Payout

When you map out your retirement budget, you might estimate that your Social Security check will be exactly $2,500. You plan your mortgage, groceries, and utility bills around that gross figure. But when the first deposit arrives in your bank account, it is surprisingly light. The culprit? Medicare.

If you are receiving Social Security benefits when you turn 65 and enroll in Medicare, your monthly Part B premiums are automatically deducted from your Social Security payment. You do not get a bill in the mail; the government simply intercepts the money before it reaches you. In 2026, the standard Medicare Part B premium is $202.90 per month. If you and your spouse both collect benefits and are both on Medicare, that is over $400 removed from your household cash flow every single month.

The situation escalates if you have been a diligent saver or had a high-earning career. Medicare enforces an Income-Related Monthly Adjustment Amount (IRMAA) for retirees whose Modified Adjusted Gross Income (MAGI) exceeds certain limits. In 2026, if you are single with a MAGI over $109,000, or married filing jointly with a MAGI over $218,000, you will be forced to pay a surcharge on top of the standard Part B premium. Those in the highest brackets can see hundreds of additional dollars deducted from their checks.

The most frustrating aspect of IRMAA for new retirees is the two-year lookback rule. Your 2026 Medicare premiums are based on the tax return you filed for the 2024 tax year. If 2024 was your final year of full-time employment, Medicare treats you as a high-income earner, severely reducing your current Social Security check. You can fight this by filing Form SSA-44 with the Social Security Administration, requesting a new assessment due to a “life-changing event” such as work stoppage or retirement. If approved, your premiums will be adjusted to reflect your new, lower retirement income.

4. Spousal and Survivor Benefits Follow the Strict “Dual Entitlement” Rule

The Social Security system offers a valuable safety net for households where one spouse earned significantly more than the other. A lower-earning spouse is entitled to claim a spousal benefit equal to 50% of the primary earner’s Full Retirement Age benefit amount. However, the mechanics of how this money is paid out consistently confuse retirees.

Under the dual entitlement rule, you do not receive your own work benefit stacked on top of a spousal benefit. The SSA will always pay your own earned worker benefit first. If your spousal benefit is larger than your worker benefit, the government simply adds a supplemental payment to bring your total check up to the higher spousal amount. You ultimately receive the higher of the two figures, never both.

This dynamic shifts drastically when a spouse passes away. Survivor benefit rules dictate that a widow or widower is entitled to 100% of the deceased spouse’s benefit amount—but again, they do not get to keep both checks. The surviving spouse assumes the larger of the two Social Security payments coming into the household, and the smaller payment disappears permanently.

This reality creates a massive structural flaw in many retirement plans, often referred to as the “widow’s penalty.” When the first spouse dies, the household loses 30% to 50% of its Social Security income overnight. Meanwhile, living expenses—such as property taxes, home maintenance, and utilities—rarely drop by the same proportion. Furthermore, the surviving spouse must now file taxes as a single individual, pushing them into tighter tax brackets and potentially exacerbating the tax torpedo discussed earlier. Couples must aggressively plan for this inevitable drop in household income by securing life insurance, optimizing pensions, or maintaining robust Roth IRA balances.

5. You Must Survive an Entire Calendar Month to Keep That Month’s Payment

One of the most rigid—and emotionally distressing—rules in the Social Security playbook involves the final payment made to a beneficiary. Social Security operates on an arrears system, meaning the payment you receive in July is actually your benefit for the month of June. To be legally entitled to that June benefit, you must live through every single day of June.

If a retiree passes away on June 30th at 11:45 PM, they did not survive the entire month. As a result, they are not entitled to the June benefit payment that is normally scheduled to arrive in July. Because the SSA system is automated, that July payment will likely still be deposited into the deceased’s bank account. However, once the SSA processes the death certificate, they will automatically claw that money back from the account.

Surviving spouses who do not know this rule often use that final deposit to pay for immediate expenses, funeral arrangements, or utility bills. Weeks later, the bank account is suddenly overdrawn when the government reverses the deposit. To prevent this financial shock during a period of grieving, families should immediately freeze the use of the deceased’s final Social Security deposit until they confirm with their bank and the SSA that the funds are clear to keep.

Avoiding Common Errors

Knowledge is your best defense against the strict rules of the Social Security system. As you approach your claiming age, be hyper-aware of these frequent missteps:

- Ignoring state taxes: While we have thoroughly covered federal taxation, remember that your physical location matters. A minority of states still tax Social Security benefits at the state level. Always verify your state’s current tax code before finalizing your retirement budget.

- Claiming early to “break even” without considering your spouse: Taking benefits at 62 permanently locks in a lower payout. If you are the higher earner, claiming at 62 doesn’t just reduce your check; it permanently reduces the survivor benefit your spouse will rely on if you pass away first.

- Missing the 12-month withdrawal window: If you claim your benefits and quickly realize you made a mathematical error (such as triggering the earnings limit or a massive tax bill), you have a one-time opportunity to hit the reset button. By filing Form SSA-521 within 12 months of your initial claim, you can withdraw your application, repay the benefits you received, and restart your claim at a later date for a higher monthly payout.

When DIY Isn’t Enough

While basic retirement budgeting can be handled at the kitchen table, the intersection of Social Security rules, tax code, and Medicare surcharges often requires professional intervention. You should strongly consider hiring a fiduciary financial planner or a tax professional if you find yourself in the following scenarios:

- Executing large Roth conversions: If you are strategically converting traditional IRA funds to a Roth IRA to defuse the tax torpedo, the conversions will spike your current-year income. A professional can help you sequence these conversions over several years to avoid inadvertently triggering massive Medicare IRMAA surcharges.

- Selling a business or real estate: A massive one-time capital gain in the years immediately preceding your retirement will trigger maximum Medicare premiums and subject 85% of your Social Security to taxation. Planners can use charitable trusts, installment sales, or donor-advised funds to mitigate the damage.

- Navigating complex family dynamics: If you are divorced but your marriage lasted 10 years or longer, you may be eligible to claim benefits on your ex-spouse’s earnings record. Coordinating these benefits—especially if your ex-spouse has remarried or if there are disabled dependents involved—requires precise timing and deep knowledge of SSA policies.

Frequently Asked Questions

Does claiming Social Security early affect my spouse’s survivor benefit?

Yes. If you are the higher-earning spouse and you choose to claim your benefits before reaching your Full Retirement Age, you permanently reduce the maximum survivor benefit your spouse will receive if you pass away first. Delaying your claim protects your surviving spouse’s future income.

Is the Social Security earnings limit a permanent loss of money?

No. The benefits withheld due to the earnings test are not lost forever. Once you reach Full Retirement Age, the Social Security Administration recalculates your monthly benefit upward to account for the exact number of months your checks were withheld, paying you back gradually over your lifetime.

How can I avoid the Social Security tax torpedo?

You can manage the tax torpedo by keeping your provisional income below the IRS thresholds. Strategies include executing Roth conversions in your early 60s before claiming benefits, withdrawing living expenses from taxable brokerage accounts instead of pre-tax IRAs, and working with a financial planner to carefully sequence your withdrawals.

Making a mistake with your Social Security claiming strategy can cost your household tens of thousands of dollars over the course of a 20- or 30-year retirement. Take the time to map out your other income sources, anticipate your tax brackets, and coordinate with your spouse before signing your application. A proactive approach today guarantees a more comfortable, secure lifestyle tomorrow.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.