Taking on a seasonal retail job before the holiday rush offers a practical way to boost your retirement income while securing valuable employee discounts. As stores ramp up hiring for year-end demand, you have the leverage to find flexible, low-stress roles that fit your lifestyle. Retail employers highly value the reliability, patience, and life experience you bring to the sales floor. Whether you want to fund a holiday travel budget, pad your emergency savings, or simply get out of the house, seasonal work provides a temporary commitment with immediate financial rewards. By choosing the right retail environment and understanding how new earnings interact with your Social Security benefits, you can maximize your seasonal paycheck without complicating your tax situation.

Why Seasonal Retail Work Makes Sense for Retirees

The retail industry fundamentally shifts as the holiday season approaches. To manage the surge in foot traffic, big-box retailers, specialty boutiques, and grocery chains actively recruit reliable workers. For retirees, this creates an ideal window to re-enter the workforce on temporary, highly negotiable terms.

Recent data shows that the average hourly pay for a part-time retail sales associate sits between $15.00 and $16.50 nationwide in 2026, with some specialized roles paying significantly higher. Beyond the direct hourly wage, the financial perks of seasonal retail can dramatically reduce your year-end expenses. Most retailers offer employee discounts ranging from 15% to 30%—and sometimes higher during designated employee appreciation weeks. If you plan to purchase gifts, electronics, or home goods during the holidays, these discounts effectively stretch your seasonal paycheck much further.

Financial incentives aside, the social aspects of a part-time job often provide the most profound benefits for retirees. Leaving a full-time career can sometimes result in a sudden loss of structure and daily interaction.

“Many people underestimate how much of their identity and daily routine was tied to their job, and they miss the structure, social interaction and sense of purpose that work provided.” — Laura Mattia, Certified Financial Planner

A seasonal job bridges this gap without asking for a permanent commitment. You secure a reason to get out of the house, interact with your local community, and stay physically active, all while knowing exactly when the commitment will end.

Top Seasonal Retail Jobs for Retirees

Not all retail environments are created equal. Finding the right fit requires matching your physical comfort levels and personal interests with the pace of the store. Here are the most retiree-friendly retail sectors to target before the holiday rush.

Hardware and Home Improvement Stores

Retailers like The Home Depot, Lowe’s, and local Ace Hardware locations constantly seek employees with life experience. If you have spent decades maintaining a home, gardening, or completing DIY projects, you possess a baseline of knowledge that younger applicants often lack. These environments tend to move at a steadier, more consultative pace than fast fashion or electronics stores.

Bookstores and Craft Stores

If you prefer a quieter environment, consider applying at Barnes & Noble, local independent bookstores, Michaels, or Jo-Ann Fabrics. Customers in these stores generally seek advice on specific hobbies, reading material, or craft projects. The physical demands are typically lower, mostly involving light stocking, operating a cash register, and guiding customers to the right aisles.

Premium Grocery and Big-Box Greeters

Specialty grocery stores like Trader Joe’s and Whole Foods often hire seasonal workers to manage holiday food orders and sample stations. These roles emphasize customer service and a positive attitude. Alternatively, big-box retailers like Costco and Walmart utilize receipt checkers and greeters—roles that keep you stationed near the entrance to welcome shoppers and verify purchases, which minimizes heavy lifting.

Comparing Retail Environments

| Retail Sector | Pace & Physical Demand | Typical Roles | Best For Retirees Who… |

|---|---|---|---|

| Hardware & Home Improvement | Moderate; involves walking large aisles and occasional light lifting. | Department specialist, cashier, paint mixer. | Have DIY knowledge and enjoy offering project advice. |

| Craft Stores & Bookstores | Relaxed; standing at a register or arranging displays. | Sales associate, gift wrapper, inventory clerk. | Prefer a quieter environment and share the store’s core hobby. |

| Premium Grocery | Fast-paced during holiday weeks; requires standing. | Sample demonstrator, bagging assistant, order fulfillment. | Enjoy active environments and engaging in quick conversations. |

| Big-Box Retailers | Variable; high foot traffic but distinct role boundaries. | Door greeter, receipt checker, customer service desk. | Want clear, repetitive tasks without heavy physical strain. |

Understanding the Social Security Earnings Limit in 2026

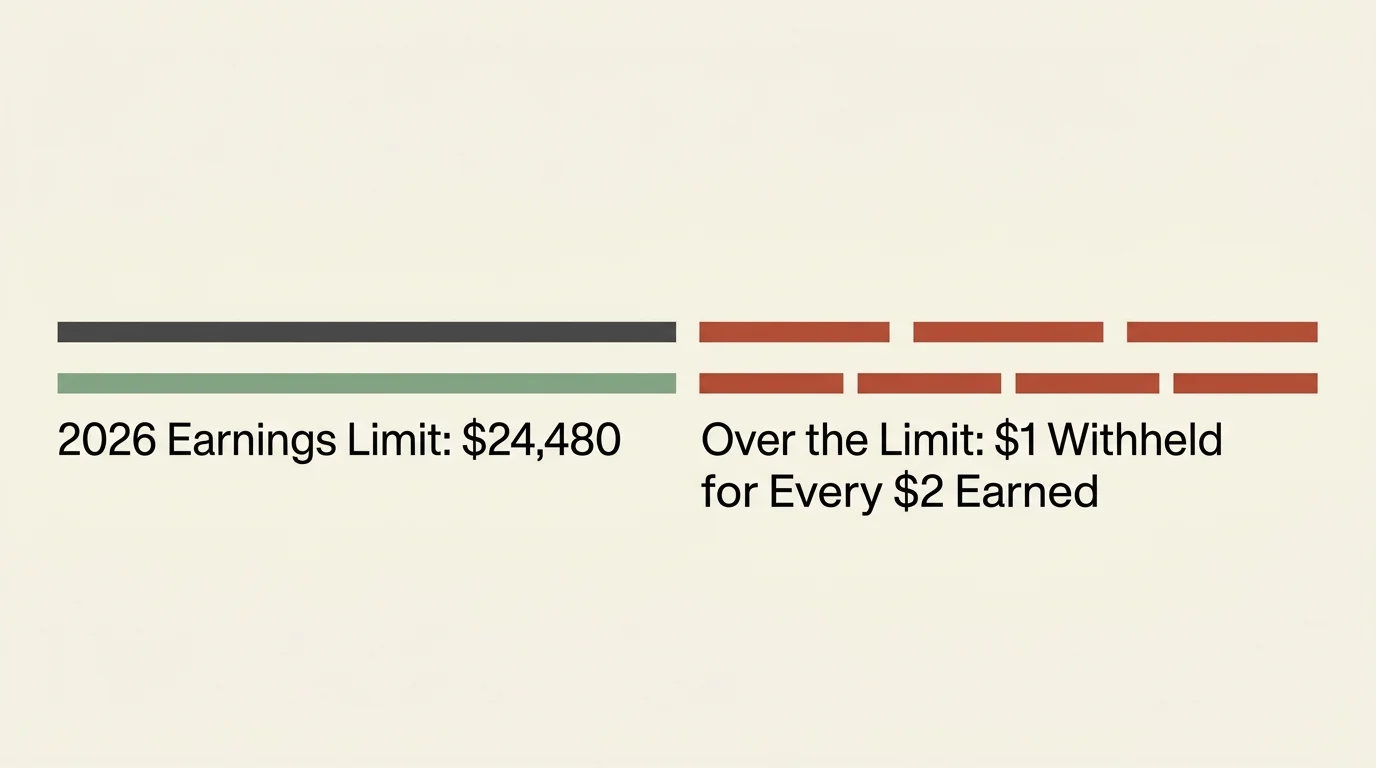

If you have already claimed Social Security but have not yet reached your Full Retirement Age (FRA), you must monitor your seasonal earnings carefully. The Social Security Administration imposes an earnings limit on beneficiaries who work while receiving benefits early.

For 2026, the standard earnings limit is $24,480 for anyone who will be under their Full Retirement Age for the entire year. If your total job earnings for the year exceed this amount, Social Security will deduct $1 from your benefit payments for every $2 you earn above the limit.

If 2026 is the year you actually reach your Full Retirement Age, the rules become much more generous. The earnings limit jumps to $65,160, and it only applies to money earned in the months prior to your birthday month. Furthermore, the penalty drops; the SSA will only deduct $1 for every $3 you earn above the threshold. Once you hit your FRA, the earnings limit vanishes completely—you can earn an unlimited amount of money without facing any benefit deductions.

It is important to remember that the earnings test only looks at wages from a job or net earnings from self-employment. The SSA does not count pensions, investment income, interest, or capital gains toward this limit. Additionally, if a seasonal job pushes you over the limit and triggers a withholding, that money is not permanently lost. When you reach Full Retirement Age, the SSA recalculates your monthly benefit upward to account for the months your benefits were withheld, effectively paying you back over your remaining lifetime.

Tax Implications: Keep More of Your Seasonal Paycheck

A common worry among retirees is that a seasonal job will thrust them into a higher tax bracket or trigger massive federal income tax liabilities. Fortunately, recent adjustments to the tax code heavily favor older adults, allowing you to shield a significant portion of your income.

For the 2026 tax year, the Internal Revenue Service has set the standard deduction for single filers at $16,100, and $32,200 for married couples filing jointly. However, if you are 65 or older, you get an additional standard deduction. For 2026, a single filer age 65 or older can claim an extra $2,050, bringing their total standard deduction to $18,150.

On top of this, a temporary provision in effect from 2025 through 2028 introduced a new “senior bonus deduction.” This allows eligible individuals age 65 and older to claim an additional $6,000 deduction—or $12,000 for a married couple where both spouses qualify.

When you combine the base standard deduction, the over-65 additional deduction, and the new $6,000 senior bonus deduction, a single retiree in 2026 could potentially shield up to $24,150 from federal income tax before owing a single dime. Because most seasonal retail jobs yield only a few thousand dollars over a two-month period, the vast majority of retirees will not see a drastic shift in their federal tax burden. Just be mindful of your state’s specific income tax laws, which operate separately from the IRS.

What to Look for During the Interview Process

When you sit down with a hiring manager for a seasonal retail position, remember that you are interviewing them just as much as they are interviewing you. Retailers are desperate for dependable help during the holidays; use this leverage to establish clear boundaries.

- Precise Schedule Parameters: Retail managers often assume seasonal hires want as many hours as possible. If you only want to work Tuesday and Thursday mornings, state this explicitly during the interview. Ask if the store uses rigid block scheduling or if they can accommodate flexible shifts.

- Physical Expectations: Ask direct questions about the day-to-day physical requirements. Will you be standing on a concrete floor for six hours? Are you expected to climb ladders or lift boxes over twenty pounds? Ensure the tasks align with your comfort level.

- Exact Duration of Employment: Seasonal roles usually end in early January after the rush of holiday returns. Clarify the exact end date. If you plan to travel south for the winter on January 5th, the employer needs to know upfront.

- Discount Activation Dates: If you are taking the job primarily for the employee discount, ask when it activates. Some retailers require you to complete a 30-day probationary period before you can use your discount, which could defeat the purpose of holiday shopping.

What Can Go Wrong

While seasonal work offers great benefits, a few common pitfalls can turn a pleasant side hustle into a source of stress.

Schedule Creep

As Black Friday and the weeks leading up to Christmas arrive, store managers inevitably deal with call-outs and overwhelmed sales floors. You may face pressure to pick up extra shifts or stay late. If you agreed to 15 hours a week, hold firm to that boundary. “Schedule creep” is the fastest way to burn out in a job that is supposed to be low-stress.

Physical Toll

Retail environments are physically demanding. Standing on hard floors for consecutive hours can aggravate joint pain or plantar fasciitis. Invest in high-quality, supportive footwear before your first shift, and do not hesitate to ask for a fatigue mat if you are stationed at a cash register.

Medicare IRMAA Thresholds

For high-net-worth retirees, any additional income requires careful monitoring due to Medicare’s Income-Related Monthly Adjustment Amount (IRMAA). Medicare bases your Part B and Part D premiums on your Modified Adjusted Gross Income (MAGI) from two years prior. While a few thousand dollars from a seasonal job rarely pushes an average retiree over an IRMAA cliff, if you are already sitting right on the edge of a surcharge bracket, that extra retail paycheck could inadvertently trigger higher Medicare premiums down the road.

When to Consult a Professional

For most retirees, picking up a seasonal retail job is straightforward. However, you should consult a financial advisor or tax professional before accepting a role if you fall into specific categories.

Seek professional guidance if you are currently claiming Social Security prior to your Full Retirement Age and your combined income from other part-time work or self-employment puts you close to the $24,480 limit for 2026. A professional can help you calculate the exact break-even point where working more hours actually results in less take-home money due to the earnings test.

Additionally, if you are executing complex tax strategies—such as substantial Roth conversions or managing required minimum distributions (RMDs)—a tax planner can ensure your new retail income does not push you into a higher marginal tax bracket or trigger the taxation of a larger percentage of your Social Security benefits.

Frequently Asked Questions

Will a seasonal job affect my Medicare premiums?

Generally, no. Seasonal retail work typically generates modest income. However, Medicare premiums are tied to your Modified Adjusted Gross Income (MAGI). If your seasonal earnings push your MAGI over specific IRMAA thresholds, you could see a surcharge on your Part B and Part D premiums two years later. Monitor your total income if you are near a bracket limit.

Do seasonal retail jobs offer health or retirement benefits?

Most seasonal, part-time roles do not offer comprehensive health insurance or 401(k) matching. They are classified as temporary employment. The primary perks are hourly wages, employee discounts, and occasionally holiday bonus pay.

Are retail employee discounts considered taxable income?

In most cases, the IRS does not consider employee merchandise discounts to be taxable income as long as the discount does not exceed the employer’s gross profit percentage. Standard retail discounts of 15% to 30% are entirely tax-free perks.

Can I pause my Social Security benefits if I decide to keep working full-time?

If you have reached your Full Retirement Age but are not yet 70, you can voluntarily suspend your retirement benefit payments. During the suspension, you will earn delayed retirement credits, which will permanently increase your future monthly benefits.

Stepping back into the workforce for a few months out of the year is a powerful way to stay engaged and financially nimble. Establish your boundaries during the interview, choose a store environment that matches your pace, and enjoy the extra holiday cash. Retailers need your experience, and you deserve a role that respects your time.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.