Retirement planning often focuses entirely on hitting a magic portfolio number, leaving millions of Americans completely unprepared for the jarring financial and emotional realities that follow their last day of work. You might have your 401(k) dialed in and a rough idea of your Social Security benefits, but the landscape changes the moment you transition from accumulating wealth to living off it. Hidden tax traps, escalating healthcare premiums, and shifting government rules can quickly erode the nest egg you spent decades building. By understanding these ten critical retirement surprises—from Medicare surcharges to unexpected emotional hurdles—you can protect your life savings and navigate your golden years with absolute confidence.

1. Medicare Premiums Eat Your Social Security Raise

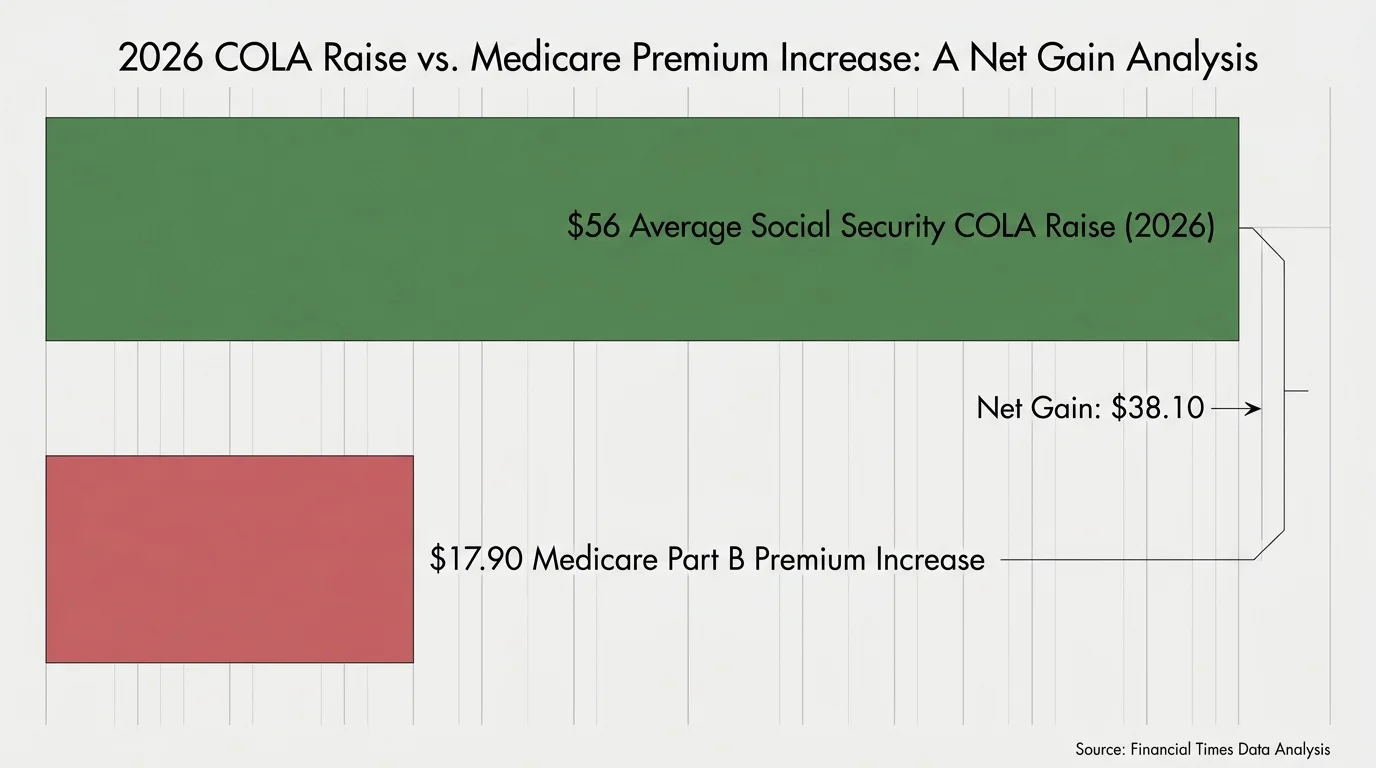

Many retirees assume their annual Social Security cost-of-living adjustment (COLA) provides a pure, uninterrupted boost to their monthly income. The reality on the ground often looks quite different. The Social Security Administration implemented a 2.8% COLA for 2026, which adds roughly $56 a month to the average retirement benefit. However, the vast majority of retirees have their Medicare Part B premiums deducted directly from their Social Security checks.

Healthcare inflation rarely mirrors general economic inflation. In 2026, the standard Medicare Part B premium increased by $17.90 to reach $202.90 per month. Additionally, the annual deductible for Part B beneficiaries rose to $283. Because these fundamental healthcare costs climb relentlessly, your net Social Security raise often feels significantly smaller than the headline percentage suggests. Fortunately, a “hold harmless” provision protects most beneficiaries from seeing their actual Social Security check decrease if the Medicare premium hike exceeds their COLA amount. But for many, the raise essentially amounts to a net zero gain.

2. The IRMAA Cliff Penalizes Your Past Income

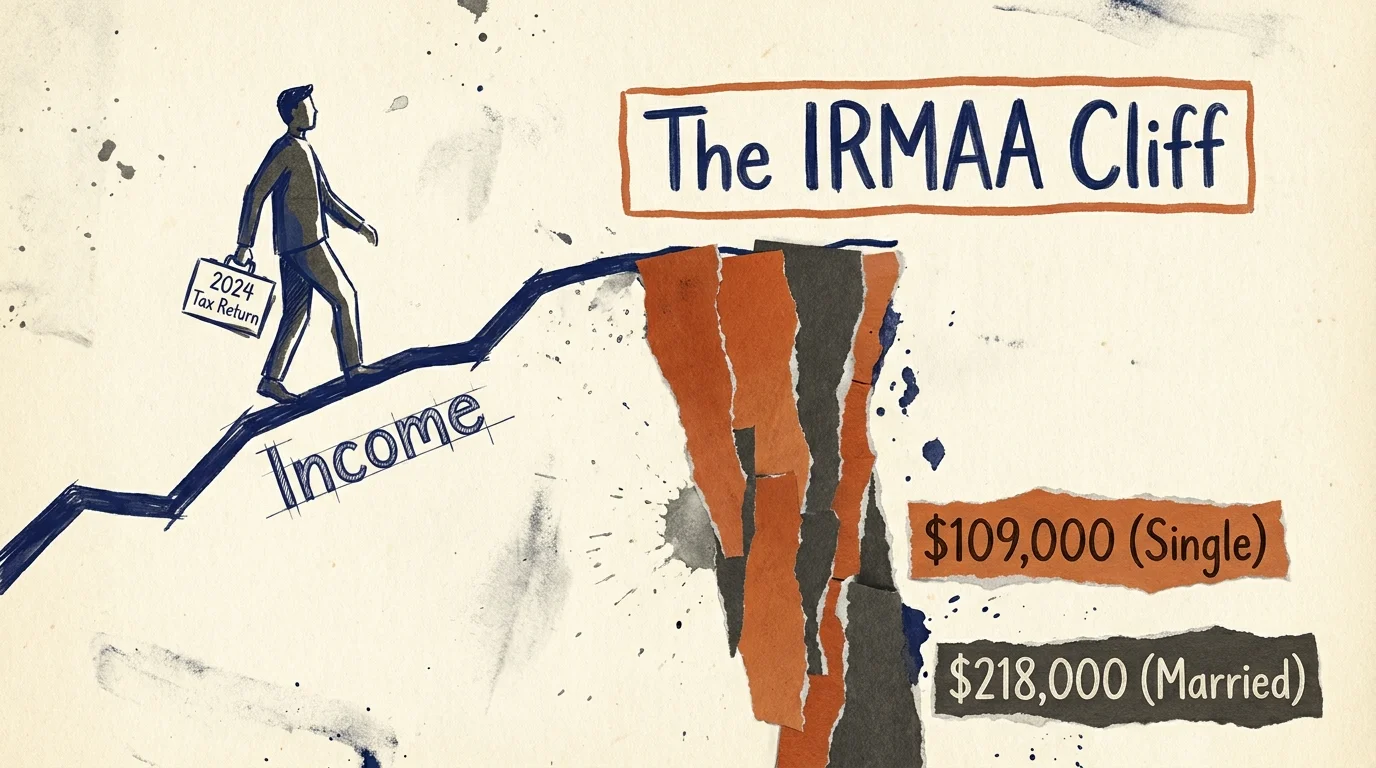

If you generated substantial income in the years leading up to your retirement date, Medicare will charge you extra for the exact same coverage your peers receive. The Income-Related Monthly Adjustment Amount (IRMAA) acts as a surcharge on your Part B and Part D premiums. The government looks at your modified adjusted gross income (MAGI) from two years prior to determine your IRMAA status; this means your 2026 premiums are based on your 2024 tax returns.

For 2026, single filers who reported more than $109,000 and married couples reporting over $218,000 face these steep surcharges. The most brutal aspect of IRMAA is its cliff structure. Surpassing the income threshold by just a single dollar bumps you entirely into the higher premium bracket, adding thousands of dollars to your annual healthcare bill. A strategic Roth conversion, the sale of a vacation home, or an unexpected mutual fund capital gain distribution can easily trigger this penalty, catching newly retired individuals completely off guard. If you experienced a life-changing event—such as retiring and losing your primary income—you can file Form SSA-44 to request a reduction in your IRMAA surcharge.

3. Up to 85% of Your Social Security Can Be Taxed

Millions of Americans enter retirement assuming their Social Security benefits operate as entirely tax-free income. Unfortunately, the Internal Revenue Service taxes up to 85% of your benefits if your combined income exceeds specific thresholds. To calculate your combined income, you add your adjusted gross income, your nontaxable interest (such as municipal bond yields), and half of your Social Security benefits.

If you file as an individual and your combined income exceeds $25,000, up to 50% of your benefits become taxable. Once your combined income pushes past $34,000, up to 85% of your benefits are subject to federal income tax. For married couples filing jointly, the 50% taxation bracket begins at $32,000, and the 85% bracket begins at $44,000. These thresholds have remained unchanged since they were established decades ago. Because Congress never indexed these figures for inflation, routine cost-of-living adjustments naturally push more retirees into this tax trap every single year.

4. The “Super” Catch-Up Opportunity for Ages 60 to 63

The SECURE 2.0 Act introduced a powerful—yet widely misunderstood—tool for late-career savers who need to accelerate their retirement funding. While standard catch-up contributions have existed for years, the IRS now allows a “super” catch-up specifically targeted at workers aged 60 to 63.

For 2026, the base 401(k) and 403(b) contribution limit stands at $24,500. If you fall between the ages of 60 and 63, you can add an extra $11,250 as a super catch-up, bringing your total allowable workplace contribution to a massive $35,750 for the year. Once you turn 64, your limit drops back down to the standard age 50+ catch-up rate of $8,000. Taking advantage of this narrow three-year window can significantly bolster your tax-advantaged savings right before you leave the workforce.

| 2026 Retirement Account Type | Base Limit (Under Age 50) | Standard Catch-Up (Age 50-59 & 64+) | “Super” Catch-Up (Age 60-63) |

|---|---|---|---|

| 401(k) / 403(b) | $24,500 | $32,500 total | $35,750 total |

| Traditional / Roth IRA | $7,500 | $8,600 total | $8,600 total |

5. Medicare Does Not Cover Long-Term Care

A devastating misconception involves the actual scope of Medicare coverage. Medicare pays for acute medical needs—surgeries, specialist doctor visits, hospital stays, and short-term rehabilitative care. It categorically does not cover custodial care, which includes daily assistance with bathing, dressing, eating, or moving around your home.

If you develop a cognitive impairment like Alzheimer’s or a chronic physical condition that requires long-term care in an assisted living facility or nursing home, you must pay out of pocket, rely on family members, or utilize long-term care insurance. With the national average cost of a private room in a nursing home exceeding six figures annually, this expense can drain a lifetime of savings in just a few years. Medicaid eventually steps in to cover these costs, but only after you have exhausted nearly all of your personal assets down to poverty levels. Planning for long-term care remains one of the most critical elements of a secure retirement strategy.

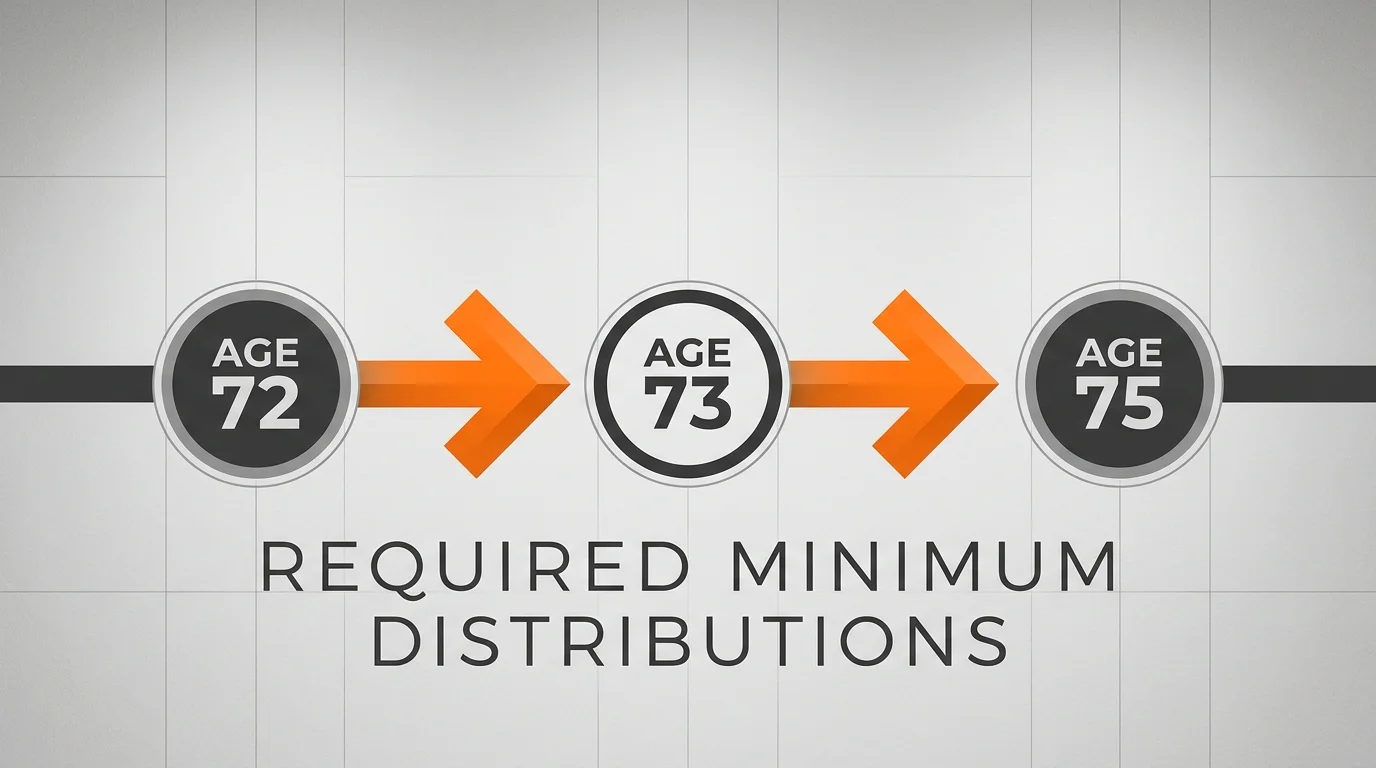

6. The RMD Age Keeps Moving

Required Minimum Distributions (RMDs) force you to pull money out of your tax-deferred accounts—like Traditional IRAs and 401(k)s—and pay ordinary income tax on those withdrawals. Recent legislative changes have created widespread confusion regarding exactly when these withdrawals must begin.

The original SECURE Act pushed the starting age from 70½ to 72. SECURE 2.0 pushed it further to age 73 for those born between 1951 and 1959. Eventually, the RMD age will increase to 75 for those born in 1960 or later. Failing to take the correct distribution on time results in a severe IRS penalty—up to 25% of the amount you should have withdrawn, though it can sometimes be reduced to 10% if corrected quickly. Keeping track of your exact RMD timeline requires constant vigilance, especially if you hold multiple retirement accounts across different financial institutions.

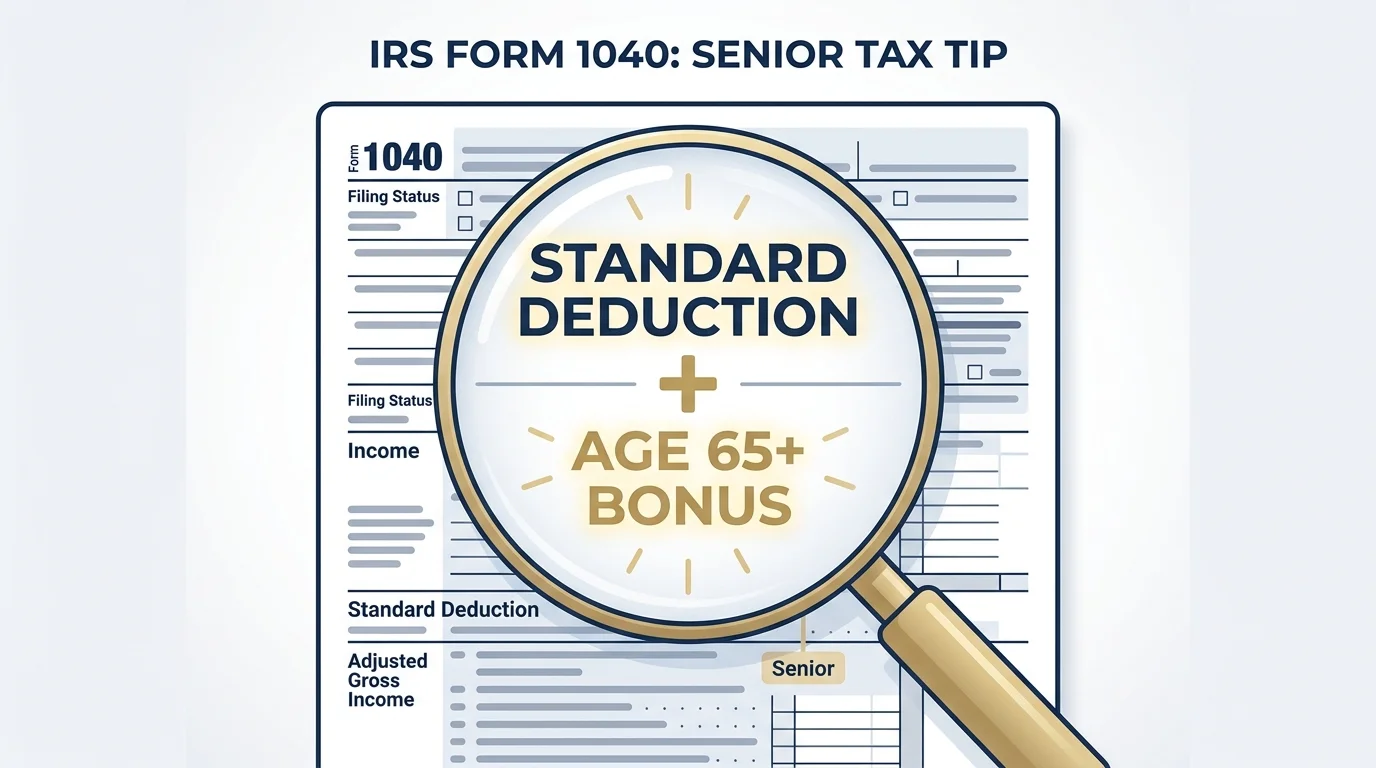

7. The Hidden “Senior” Standard Deduction

When calculating your taxes in retirement, you should never overlook the additional standard deduction available specifically to older Americans. The IRS grants taxpayers who are 65 or older—or those who are legally blind—a higher standard deduction amount.

This extra buffer reduces your taxable income directly from the top, potentially keeping you in a lower tax bracket or helping you avoid crossing the threshold for Social Security taxation altogether. If you are married and both you and your spouse are 65 or older, you both receive the additional amount. Many retirees who prepare their own taxes blindly default to the standard deduction they used throughout their working years, inadvertently paying more tax than legally necessary. Always verify your tax software applies this extra credit on the return for the year you turn 65.

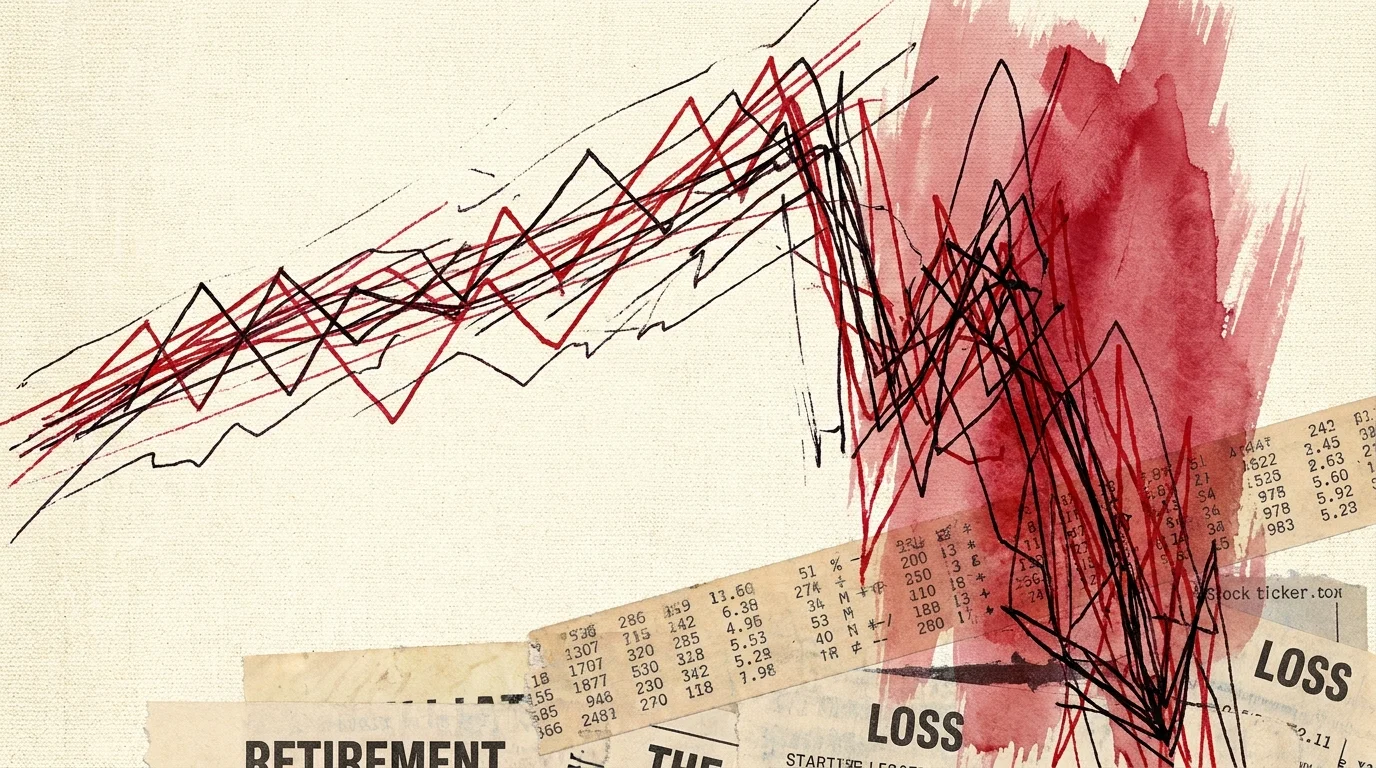

8. Sequence of Returns Risk Can Halve Your Portfolio

The order in which you experience investment returns matters infinitely more during retirement than it did during your working years. When you are accumulating wealth, a market crash simply allows you to buy shares at a discount. In retirement, the math flips entirely.

If the stock market drops 20% early in your retirement and you must sell assets to cover your groceries and utility bills, you lock in those losses permanently. Your portfolio has fewer shares remaining to capture the eventual market rebound. This concept, known as sequence of returns risk, can decimate a portfolio that would have otherwise survived a lifetime.

“Retirement is not an age; it’s a financial number.” — Dave Ramsey, Personal Finance Expert

To mitigate this immense risk, successful retirees often keep a cash buffer of one to three years of living expenses in high-yield savings accounts or short-term certificates of deposit. This cash runway allows them to draw from reserves during a market downturn, giving their broader investment portfolio time to recover without suffering forced liquidations at market bottoms.

9. Healthcare Out-of-Pocket Costs Average Six Figures

Even with comprehensive Medicare Part A, Part B, and prescription drug coverage, out-of-pocket medical expenses continually surprise new retirees. Original Medicare does not place a hard cap on your out-of-pocket spending. Routine dental care, hearing aids, eye exams, glasses, and specific prescription drugs all carry substantial costs that fall squarely on your shoulders.

Industry estimates consistently show that an average couple retiring today should anticipate spending hundreds of thousands of dollars on healthcare premiums, deductibles, and co-pays throughout their retirement years. Budgeting specifically for these inevitable expenses ensures a medical emergency or a high-tier prescription drug does not force you to drain your primary investment accounts.

10. The Sudden Loss of Identity and Routine

Financial preparedness only solves half the retirement equation. The emotional and psychological impact of leaving the workforce catches millions of capable professionals completely off guard. For decades, your career dictated your schedule, your social circle, your daily goals, and often your fundamental sense of purpose.

Waking up on a Monday morning with a completely blank calendar sounds luxurious while you are grinding through your fifties, but it often leads to depression, anxiety, and a profound sense of isolation once the “honeymoon phase” of retirement fades. Building a fulfilling post-career life requires deliberate, proactive effort. You must forge new social connections outside of the office, pursue engaging hobbies that challenge your mind, and establish a meaningful daily routine to thrive in this new chapter.

Pitfalls to Watch For

- Ignoring the slow burn of inflation: A fixed corporate pension feels fantastic on day one, but assuming an average inflation rate, it will lose a massive percentage of its purchasing power over a twenty-year retirement.

- Underestimating your lifespan: Modern medicine and lifestyle improvements extend life expectancies rapidly. You must structure your portfolio to generate stable income well into your late 80s or 90s to avoid outliving your money.

- Overspending in the early years: The “go-go” phase of early retirement often features excessive spending on global travel, home renovations, and luxury purchases, putting your long-term financial security at severe risk.

- Filing for Social Security out of fear: Claiming benefits at age 62 permanently reduces your monthly payout by up to 30%. While claiming early makes sense for those with poor health or immediate cash needs, doing it purely out of fear that the system will go bankrupt locks in a lower income for the rest of your life.

Getting Expert Help

Navigating the intersection of tax law, Medicare regulations, and investment withdrawal strategies rarely happens by accident. Consider consulting a licensed professional in these specific scenarios:

- Before claiming Social Security: A fee-only financial planner can calculate the exact break-even age for your specific health history, life expectancy, and marital status.

- When organizing Roth conversions: A tax professional or CPA can help you shift tax-deferred money into Roth accounts surgically, ensuring you do not inadvertently trigger the IRMAA surcharge or jump into a punitive tax bracket.

- Navigating Medicare enrollment: Independent insurance brokers can compare Medigap and Medicare Advantage plans based on your specific prescription medication needs and your preferred network of local doctors.

- Planning a comprehensive estate: An estate planning attorney can structure irrevocable trusts and medical directives to protect your assets from the devastating costs of long-term care.

Frequently Asked Questions

At what age is Social Security no longer taxed?

The taxation of Social Security benefits depends entirely on your income, not your age. As long as your combined income exceeds the IRS thresholds, a portion of your benefits remains taxable for the rest of your life, even if you live well past 100.

Does Medicare Part B cover dental and vision?

Original Medicare Part B does not cover routine dental exams, cleanings, extractions, dentures, or routine eye exams for glasses. Retirees must purchase separate supplemental insurance or enroll in a Medicare Advantage plan that specifically includes these auxiliary benefits.

Can I contribute to an IRA if I am retired?

You must have earned income—such as W-2 wages from a part-time job or 1099 income from consulting—to contribute to a Traditional or Roth IRA. Passive income sources like pensions, Social Security benefits, rental income, and investment dividends do not qualify as earned income for the purpose of making IRA contributions.

Retirement represents a fundamental shift in how you manage your time, your money, and your health. Understanding these hidden surprises allows you to pivot from simply hoping things work out to knowing your plan can withstand sudden changes. Build your cash reserves, optimize your tax strategy, and prioritize your emotional well-being to create the retirement lifestyle you actually envisioned.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.