Choosing where to spend your retirement years requires more than picking a spot with pleasant weather and beautiful scenery. You must carefully evaluate the local cost of living, property taxes, and the availability of specialized healthcare. Relocating to the wrong area can rapidly drain your savings and leave you isolated from essential services. In 2026, soaring insurance premiums and shifting tax laws have transformed several destinations into financial traps. By examining the unique challenges of specific states, coastal regions, and community layouts, you can make a highly informed decision about your future. This guide explores twelve places where daily retired life proves more difficult than expected.

1. Coastal Florida: The Insurance Crisis Zone

Many retirees picture their golden years playing out on a sun-drenched Florida beach; however, the financial reality of coastal living has shifted drastically. Driven by severe weather events, rampant litigation, and high rebuilding costs, property insurance in the Sunshine State has become a massive liability. Recent data indicates that the average homeowners insurance premium in Florida ranges from $8,292 to over $11,700 annually for standard dwelling coverage in 2026. Compare that to a national average that hovers around $2,900, and you can see how quickly this single line item can devour a fixed retirement income.

If you are determined to move to Florida, look inland. Communities located further from the coast—such as those in Lake County or Ocala—often feature significantly lower insurance premiums and reduced windstorm risks. Before committing to any property, you must secure firm insurance quotes. Buying a home only to discover it is virtually uninsurable is a disastrous way to begin your retirement.

2. Hawaii: The Unforgiving Paradise Premium

Hawaii offers unmatched natural beauty and a relaxed lifestyle, but it also carries the highest cost of living in the United States. Everything from milk and eggs to prescription medications must be shipped across the Pacific Ocean, resulting in a daily premium on basic necessities. Your grocery bill will likely be substantially higher than on the mainland, and housing costs remain notoriously steep.

Beyond the checkout counter, the isolation of island living presents unique challenges. Flying back to the mainland to visit grandchildren or attend family events requires long, expensive flights. Furthermore, while Oahu boasts excellent medical centers, the neighboring islands have limited specialized healthcare facilities. If you develop a complex medical condition, you may be forced to fly to Honolulu—or even back to the mainland—for treatment.

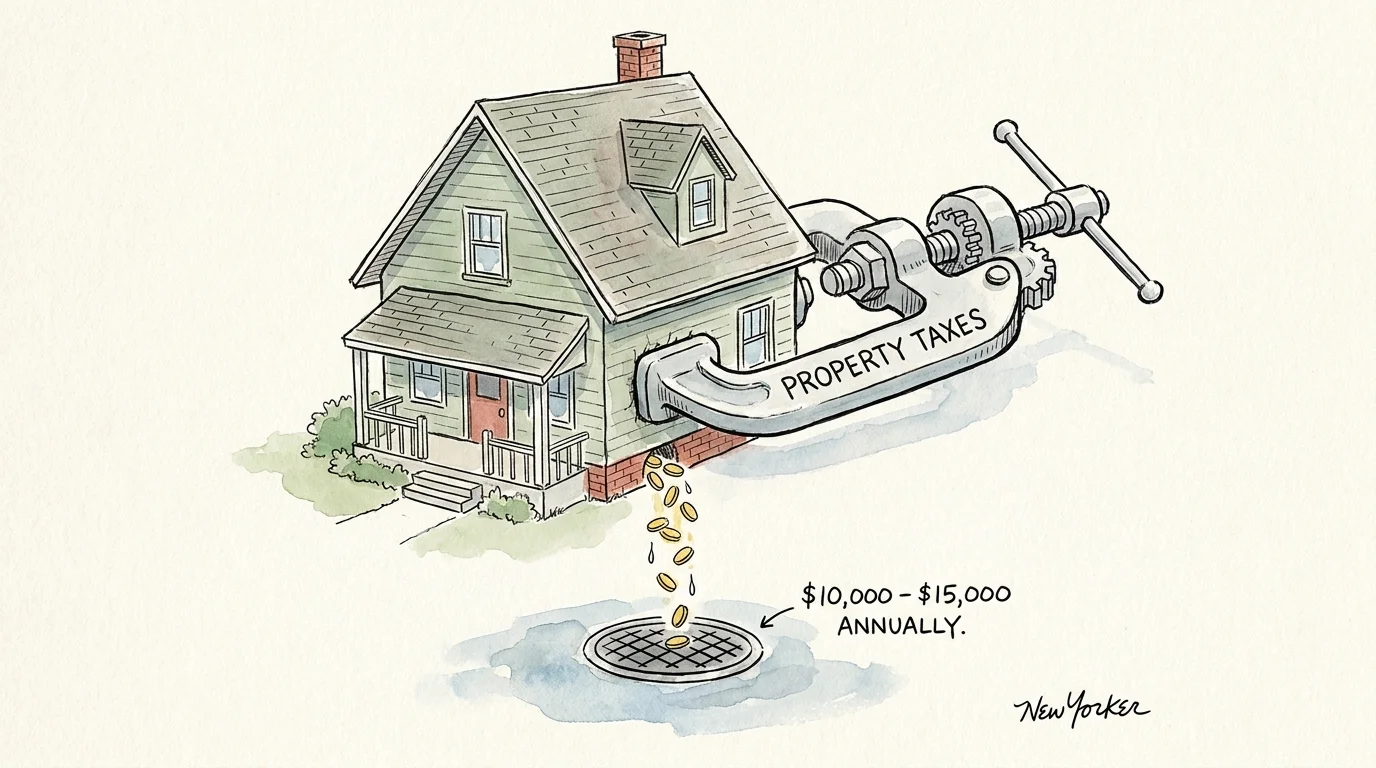

3. New Jersey: The Property Tax Pinch

New Jersey frequently lands at the bottom of retirement destination rankings, primarily due to its crushing property tax burden. While the state does offer some exclusions for pension and retirement account income, those savings are aggressively offset by local municipal taxes. The average effective property tax rate in New Jersey is the highest in the nation.

When you live on a fixed income, an ever-increasing property tax bill acts as a permanent wealth drain. A home that is fully paid off can still cost you upwards of $10,000 to $15,000 a year simply in taxes. If you want to remain in the Northeast to be close to family, bordering states like Pennsylvania—which completely exempts retirement income and Social Security from state taxes—often provide a far more hospitable financial environment.

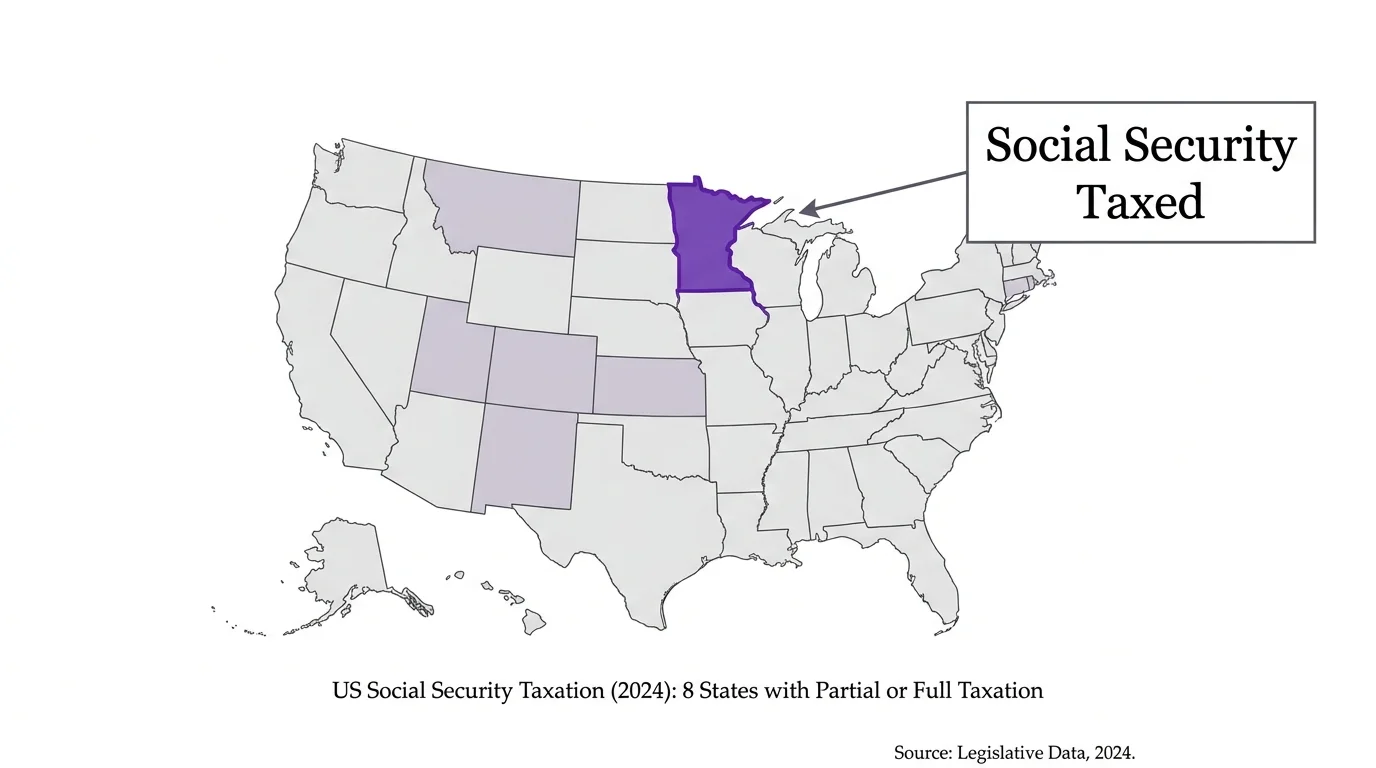

4. Minnesota: The Retirement Income Tax Hit

Minnesota boasts beautiful lakes, excellent healthcare networks, and vibrant communities, but it remains one of the few jurisdictions that aggressively tax retirees. As of 2026, Minnesota is one of only eight states that still tax Social Security benefits. While the state legislature has expanded subtraction rules to offer some relief, higher-income households are still left footing a substantial bill.

Combine the taxation of Social Security with a progressive state income tax system that reaches up to 9.85 percent, and Minnesota quickly becomes a difficult place to stretch your retirement savings. Before settling here, you should run a detailed tax projection to understand exactly how much of your nest egg will go to the state.

State Taxation of Social Security in 2026

To put Minnesota’s tax laws into perspective, it helps to look at the broader national landscape. If avoiding taxes on your benefits is a priority, you need to know which states still target this income.

| State | Social Security Tax Policy Detail (2026) |

|---|---|

| Colorado | Fully exempt for ages 65 and older; limited exclusions for ages 55–64. |

| Connecticut | Exempt for incomes below $75,000 (single) or $100,000 (joint); higher earners pay partial tax. |

| Minnesota | Partial deductions available, but taxes remain high for upper-income households. |

| Montana | Taxes are based on income thresholds, largely mirroring federal taxation rules. |

| New Mexico | Exempts lower and middle-income retirees; only taxes higher earners. |

| Rhode Island | Provides an income-based exemption; upper brackets are subject to state tax. |

| Utah | Offers a non-refundable tax credit, but base benefits remain taxable. |

| Vermont | Exemptions phase out entirely for single filers earning over $50,000. |

5. Rural Healthcare Deserts: The Accessibility Trap

The idea of buying a quiet cabin in the woods or a remote farmhouse is appealing. You get peace, quiet, and plenty of space. However, rural areas across America are currently facing an unprecedented healthcare crisis. Hundreds of rural hospitals have closed over the last decade, creating massive geographic gaps in emergency medical services.

In a medical emergency—such as a stroke or a heart attack—the time it takes to reach a Level 1 Trauma Center is often the difference between full recovery and permanent disability. Furthermore, managing chronic conditions becomes exhausting when you have to drive two hours just to see a specialist. Always use resources like Medicare.gov to locate and evaluate the quality of hospitals within a thirty-minute radius of any home you consider purchasing.

6. Alaska: The Climate and Healthcare Challenge

Alaska rewards its residents with the Permanent Fund Dividend, and it does not levy a state income tax. Unfortunately, the financial benefits end there. The state has the coldest average temperatures in the country, and maintaining a home through the long, dark winters is both physically demanding and incredibly expensive.

The true dealbreaker for many retirees, however, is healthcare access. Alaska has a severe shortage of medical specialists. Retirees facing complex medical diagnoses often find themselves booking frequent, expensive flights to Seattle just to receive adequate care. Unless you plan to adopt a “snowbird” lifestyle—living in Alaska only during the brief summer months—the Last Frontier is an intensely difficult place to age comfortably.

7. California: The Housing and Cost of Living Wall

California continues to hemorrhage retirees, and the reasons are strictly mathematical. The state suffers from a severe housing affordability crisis, high gas taxes, and a top marginal income tax rate that punishes withdrawals from traditional IRAs and 401(k)s. While Proposition 13 helps long-time residents keep their property taxes manageable, newcomers buying real estate at today’s inflated prices will face staggering tax assessments.

Additionally, California is facing an insurance crisis similar to Florida’s, albeit driven by wildfires rather than hurricanes. Many major insurance carriers have halted new policies in the state, leaving homebuyers scrambling for expensive, last-resort coverage options. If your family ties keep you tethered to California, consider extreme downsizing or exploring accessory dwelling units (ADUs) to minimize your financial footprint.

8. Car-Dependent Exurbs: The Mobility Dead End

Moving far outside city limits into sprawling, newly built subdivisions might buy you a larger house for less money. Yet, these car-dependent exurbs present a hidden danger that reveals itself slowly over time. These neighborhoods are built entirely around the automobile; they lack sidewalks, nearby grocery stores, and robust public transit.

As you advance in age, your vision, reaction times, or simple desire to drive on busy highways may decline. In a community devoid of walkable amenities or specialized senior transit, surrendering your driver’s license means surrendering your independence. You can quickly become isolated in your own home, entirely dependent on delivery services or family members for basic survival.

9. Mississippi: The Healthcare Quality Divide

If you look strictly at affordability metrics, Mississippi appears to be a retirement haven. Housing is incredibly cheap, and the state exempts all qualified retirement income from taxation. However, a successful retirement requires more than just low expenses—it requires a system that keeps you healthy and active.

Mississippi frequently ranks at the very bottom of national assessments for healthcare access, elder care quality, and overall life expectancy. When estimating your monthly budget, remember that the standard Medicare Part B premium has risen to $202.90 in 2026. You pay this exact same federal premium regardless of where you live, meaning you receive far less value for your Medicare dollar in an area plagued by physician shortages and poorly rated medical facilities.

10. New York: The Overwhelming Tax Burden

New York spares Social Security benefits from state taxation, but that is where the leniency ends. The Empire State levies heavy taxes on nearly everything else. Property taxes in areas like Westchester County and Long Island are astronomical, and the daily cost of living in urban centers quickly exhausts fixed incomes.

Even if you retreat to the more affordable upstate regions, you trade financial stress for brutal winter weather and heavy snowfall, which brings its own physical and maintenance challenges. Retirees who love the culture of the Northeast often find that living in a more tax-friendly neighboring state allows them to visit New York frequently without suffering its daily economic penalties.

11. Connecticut: The Costly Northeast Corridor

Connecticut shares many of the same drawbacks as New York and New Jersey, combining high property taxes with an overall expensive cost of living. Crucially, Connecticut is also one of the eight states that still tax Social Security benefits, though the state does provide exemptions for individuals earning below $75,000 and joint filers earning below $100,000.

If your retirement income pushes you over those thresholds, you will lose a portion of your benefits to the state. When combined with steep utility costs and expensive local services, Connecticut makes it remarkably difficult to maintain the lifestyle you enjoyed during your working years.

12. High-Altitude Mountain Towns: The Physical Toll

Retiring to a picturesque cabin in the Rocky Mountains of Colorado or the Wasatch Range of Utah sounds idyllic. But living at an elevation above 6,000 feet places serious demands on the human body. The thin air forces your heart and lungs to work much harder, which can severely exacerbate pre-existing conditions like COPD, asthma, or hypertension.

Beyond the physiological impacts, high-altitude towns experience long, brutal winters. Shoveling heavy snow becomes a dangerous cardiac risk for older adults, and navigating steep, icy driveways increases the likelihood of debilitating falls. Before committing to a mountain town, rent a property during the dead of winter. You must ensure you can handle the physical strain when the romanticism of the scenery fades.

“A good financial plan is a road map that shows us exactly how the choices we make today will affect our future.” — Jean Chatzky, Financial Editor

Pitfalls to Watch For

When selecting your retirement destination, avoiding obvious mistakes is just as important as finding the perfect community. Keep an eye out for these common missteps:

- Ignoring the total tax picture: Focusing solely on a state’s lack of income tax can blind you to exorbitant property or sales taxes. Texas and Washington have no state income tax, but their property and sales taxes, respectively, are quite high.

- Underestimating travel costs: Moving to a remote paradise saves money on paper, but if you have to spend $5,000 a year on airfare to visit your children, those savings evaporate quickly.

- Assuming Medicare covers everything everywhere: If you use a Medicare Advantage plan, your coverage is highly localized. Moving across state lines—or even just across the county—can force you out of your network, requiring you to find entirely new doctors.

Getting Expert Help

You do not have to navigate the complexities of relocation alone. Seeking professional guidance before you pack your bags can save you from making a six-figure mistake.

- Consult a Certified Financial Planner (CFP): A fiduciary advisor can run multi-state tax projections, showing you exactly how your IRA withdrawals and pensions will be taxed in different locations. You can find qualified professionals through the Certified Financial Planner Board.

- Work with an elder law attorney: Estate laws, probate rules, and Medicaid recovery regulations vary wildly by state. An attorney can ensure your existing trusts and advanced directives remain valid in your new home.

- Speak with a local Medicare broker: Before finalizing a move, have a broker verify that top-rated hospitals and your required specialists are actually accepting new Medicare patients in that specific zip code.

Frequently Asked Questions

Which states completely exempt retirement income from taxes?

Several states, including Illinois, Iowa, Mississippi, and Pennsylvania, completely exempt qualified retirement income—such as 401(k) distributions, pensions, and Social Security—from state income taxes. Additionally, states with no broad income tax (like Florida, Nevada, and Wyoming) naturally do not tax retirement income.

Does my Medicare coverage change if I move to a different state?

If you have Original Medicare (Parts A and B), your coverage travels with you anywhere in the United States. However, if you are enrolled in a Medicare Advantage (Part C) plan or a standalone Part D prescription drug plan, you will likely need to enroll in a new plan specific to your new zip code to maintain in-network coverage. Always update your address with the Social Security Administration immediately after moving.

How can I find out if a home is in an uninsurable area?

Before making an offer on a home, request an insurance claims history report (often called a CLUE report) from the seller. Additionally, contact an independent insurance agent local to the area; they can tell you immediately if carriers are issuing new policies or if the property sits in a high-risk flood or wildfire zone.

Relocating in retirement is a permanent decision that impacts your daily comfort and your financial security. Take your time, verify your assumptions with hard data, and prioritize locations that support both your wealth and your health.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.

Good information and article!!!!!! Gives me a lot to think about. Somethings I would not have thought of.