Retirement is often framed as a finish line where financial worries vanish, endless free time begins, and everyday life turns into a permanent vacation. The reality is far more complex and interesting. Many Americans spend decades saving for this chapter, only to discover that their long-held assumptions don’t match what actually happens when the regular paychecks stop. Medicare premiums and out-of-pocket costs often exceed estimates, shifting tax brackets can surprise the most diligent savers, and the sudden abundance of unstructured time can feel more overwhelming than liberating. By understanding the gap between expectation and reality, you can adjust your strategy today to build a more secure future free from these nine pervasive myths.

Expectation 1: Medicare Covers All Your Healthcare Costs

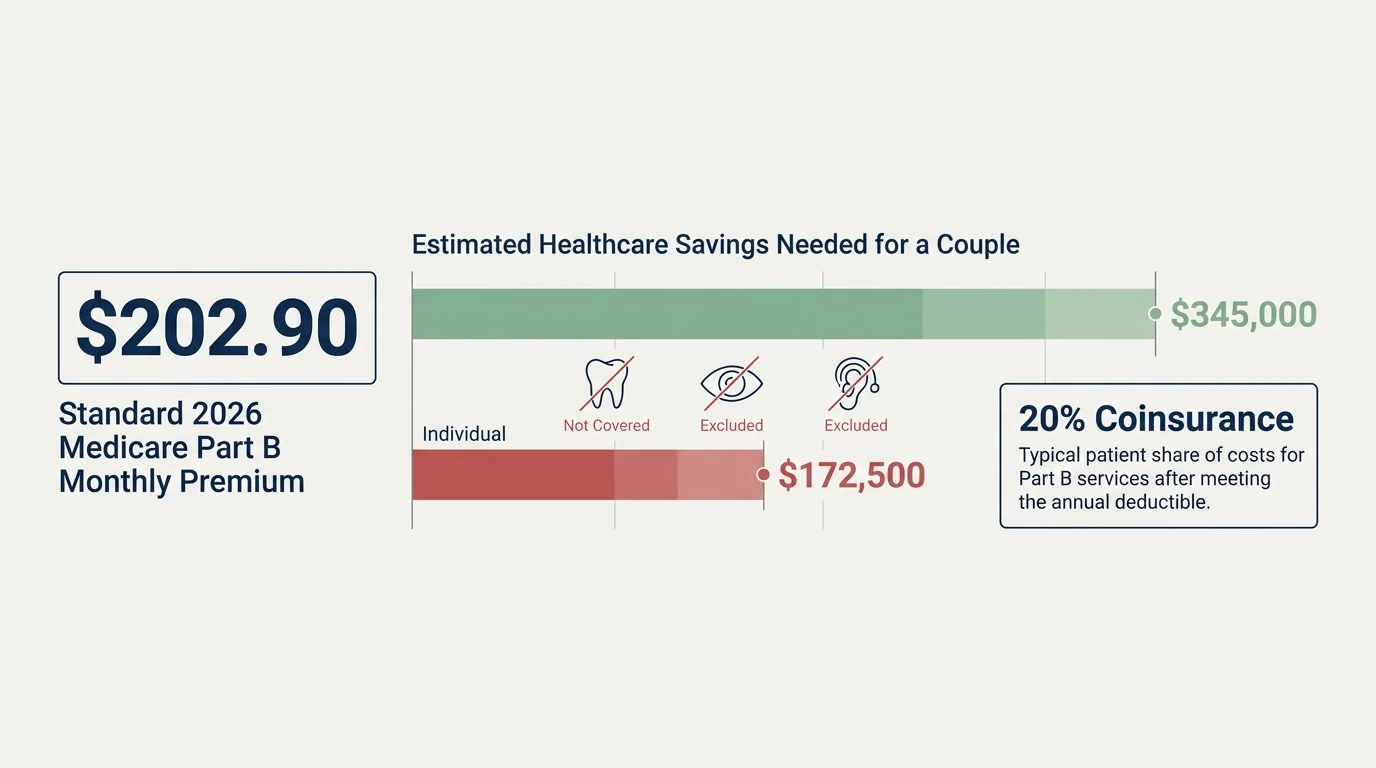

Many pre-retirees assume that turning 65 unlocks a golden ticket to free, comprehensive healthcare. While Medicare provides an essential safety net, it operates more like a subsidized insurance program than a free ride. Original Medicare is split into Part A (hospital insurance), which is typically premium-free, and Part B (medical insurance), which requires a monthly premium. In 2026, the standard Part B premium is $202.90 per month, a cost that is deducted directly from your Social Security check.

If you earned a higher income during your working years, you might also face the Income-Related Monthly Adjustment Amount (IRMAA), which can significantly increase your monthly Part B and Part D premiums. Furthermore, Original Medicare does not cap your annual out-of-pocket expenses. You are generally responsible for a 20% coinsurance on medical services, plus separate deductibles.

Crucially, traditional Medicare does not cover routine dental care, vision exams, hearing aids, or long-term nursing home care. When you factor in premiums, deductibles, copays, and out-of-pocket prescription drug costs, the financial burden is substantial. According to Fidelity Investments, a 65-year-old individual retiring in 2025 needs an estimated $172,500 in after-tax savings just to cover healthcare expenses throughout retirement. For a married couple, that number doubles to $345,000—and that figure excludes potential long-term care costs.

Expectation 2: Your Taxes Will Automatically Drop to Zero

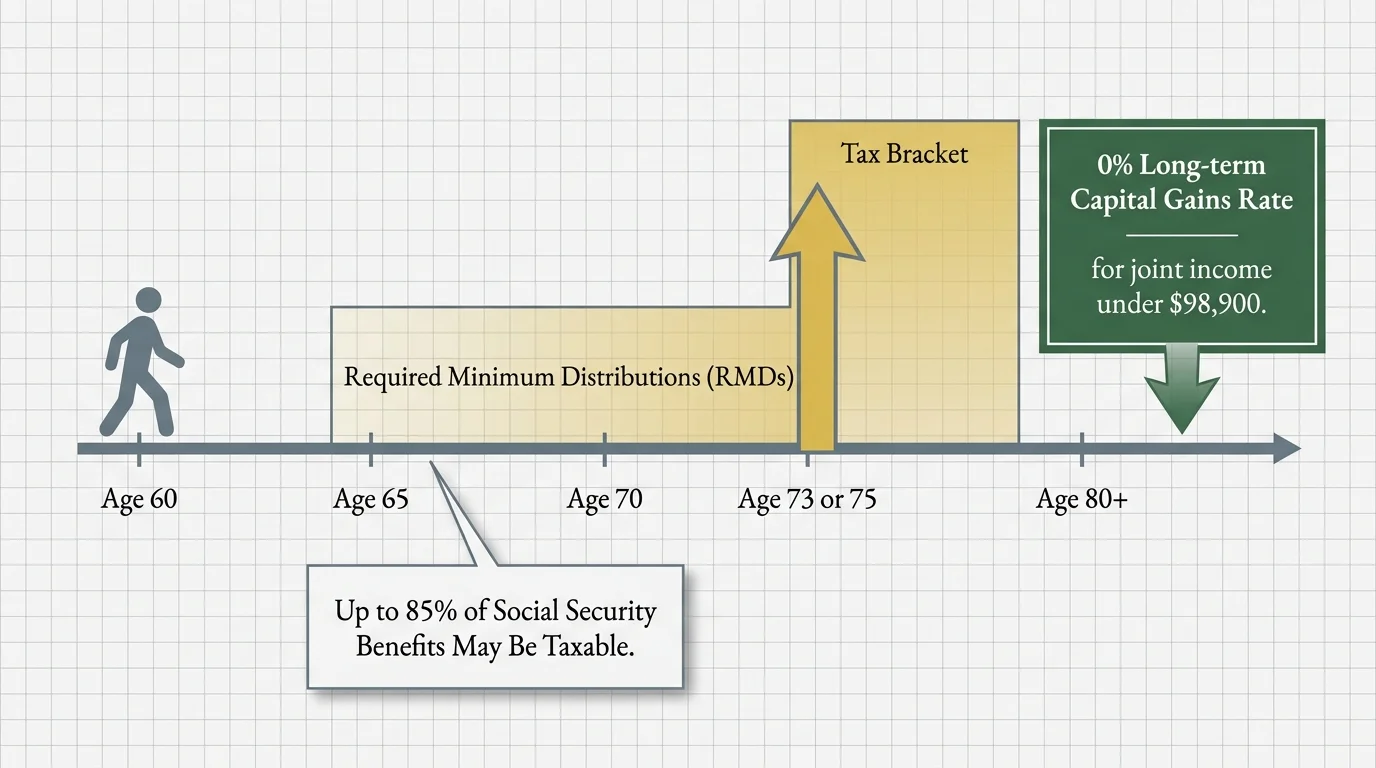

A widespread assumption is that once you stop earning a salary, your tax bill vanishes. In reality, your income sources simply change, and the Internal Revenue Service (IRS) still expects its share. If you spent decades diligently funneling money into traditional 401(k)s and IRAs, every dollar you withdraw is taxed as ordinary income.

Eventually, the IRS forces you to take Required Minimum Distributions (RMDs) from these tax-deferred accounts. Depending on your birth year, RMDs currently begin at age 73 or 75. These forced withdrawals can push you into a higher tax bracket, trigger higher Medicare premiums (IRMAA), and even cause a larger portion of your Social Security benefits to become taxable.

If your combined income (your adjusted gross income plus nontaxable interest and half of your Social Security benefits) exceeds certain thresholds, up to 85% of your Social Security benefits may be subject to federal income tax. Capital gains taxes also play a role if you sell off taxable investments to generate cash flow. Fortunately, proactive planning helps; for instance, in 2026, married couples filing jointly can realize long-term capital gains at a 0% federal tax rate if their taxable income remains under $98,900.

Expectation 3: Social Security Will Fully Fund Your Lifestyle

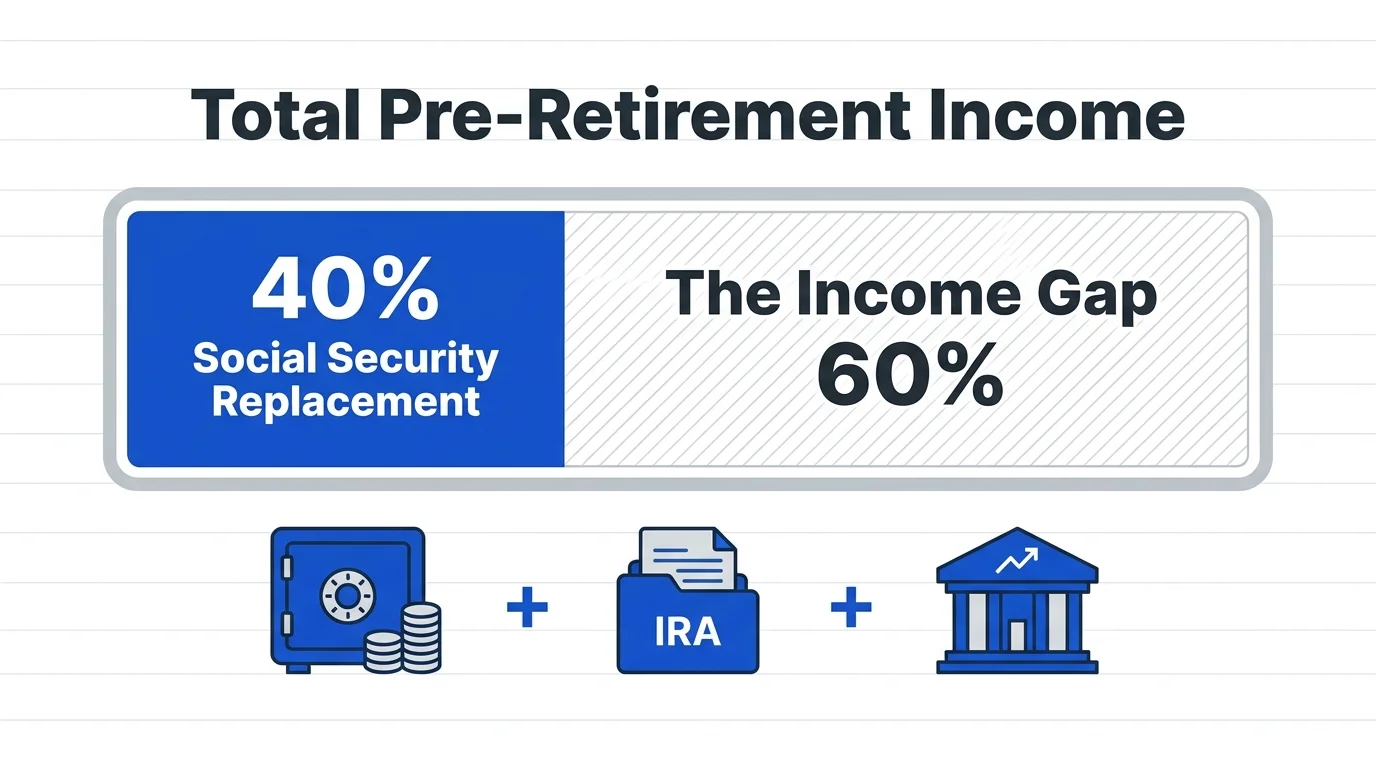

Social Security was designed to replace roughly 40% of the average worker’s pre-retirement income, yet many Americans mistakenly view it as a primary pension. Relying entirely on this benefit often leads to a severe lifestyle downgrade. Recent data from the Social Security Administration (SSA) shows that the average monthly retirement benefit in 2026 is approximately $2,076. That translates to just under $25,000 a year—hardly enough to cover housing, food, transportation, and healthcare in most parts of the country.

“Retirement is not an age; it’s a financial number.” — Dave Ramsey, Personal Finance Expert

While the maximum possible benefit for someone retiring at age 70 in 2026 is an impressive $5,181 per month, very few retirees qualify for this amount. Hitting the maximum requires you to earn at or above the Social Security wage base limit for 35 years and delay claiming until age 70. The reality is that a comfortable retirement requires a robust mix of Social Security, personal savings, investment portfolios, and potentially part-time income.

| Claiming Age Strategy | Percentage of Full Benefit | 2026 Maximum Monthly Benefit |

|---|---|---|

| Age 62 (Earliest Eligibility) | ~70% | $2,969 |

| Full Retirement Age (67) | 100% | $4,152 |

| Age 70 (Maximum Delay) | 124% | $5,181 |

Expectation 4: Your Spending Will Drop Dramatically on Day One

Financial planners often use a rule of thumb stating that you will need 70% to 80% of your pre-retirement income to maintain your lifestyle. Many future retirees look forward to shedding commuting costs, professional wardrobes, and payroll taxes. While those specific expenses do disappear, new ones quickly take their place.

Retirement spending generally follows a “smile” curve. During the early “Go-Go” years, spending often increases as you finally have the time to travel, renovate your home, spoil grandchildren, and pursue expensive hobbies. Your daily entertainment budget swells when you suddenly have seven Saturdays a week. During the middle “Slow-Go” years, spending tends to dip as you settle into a quieter routine. Finally, in the “No-Go” years of late retirement, spending spikes again—this time driven by out-of-pocket healthcare and assisted living costs. If you budget for a flat, drastically reduced spending line from day one, you may quickly deplete your liquid savings.

Expectation 5: Transitioning to Endless Free Time Is Effortless

We spend our working years daydreaming about doing absolutely nothing. Yet, when the alarm clock stops ringing permanently, the reality of unstructured time hits hard. Your career provides more than just a paycheck; it offers a built-in social network, a daily routine, intellectual challenges, and a sense of purpose and identity.

Losing that structure overnight can lead to feelings of isolation, boredom, and even depression. You can only play so much golf, read so many books, or organize the garage so many times before a profound sense of aimlessness sets in. Successful retirees plan their “time portfolio” just as carefully as their financial portfolio. They proactively schedule volunteer work, part-time consulting, continuing education, and community group involvement to maintain a strong sense of purpose.

Expectation 6: You Can Work as Long as You Want

Many Americans plan to make up for a lack of retirement savings by simply working longer. The assumption is that you are fully in control of your retirement date. The data tells a very different story. According to the 2026 Employee Benefit Research Institute (EBRI) Retirement Confidence Survey, active workers expect to retire at a median age of 65. However, the actual median retirement age among current retirees is 62.

Why the discrepancy? Nearly half of retirees report leaving the workforce earlier than they had planned. The most common catalysts are completely out of their control: unexpected health problems or disabilities (cited by 41% of early retirees in 2026), company downsizing, corporate restructuring, or the sudden need to care for an ailing spouse or aging parent. Banking on those final few years of peak earnings to fund your nest egg is a highly risky strategy.

Expectation 7: Downsizing Is Always a Massive Financial Windfall

Trading the four-bedroom family home for a cozy condo sounds like an easy way to slash expenses and unlock hundreds of thousands of dollars in home equity. While downsizing can be an effective strategy, the financial windfall is rarely as large as expected on paper.

When you sell, you must account for real estate agent commissions, staging costs, and capital gains taxes if your profit exceeds the primary residence exclusion limits. When you buy, you face closing costs, moving expenses, and potentially the need to purchase new furniture that fits a smaller floor plan. Furthermore, many retirees downsize into desirable, active-adult communities or move closer to city centers and grandchildren. These areas often carry premium real estate prices, high property taxes, and steep monthly Homeowner Association (HOA) fees. In today’s interest rate environment, giving up a paid-off home or a low-rate mortgage for a new purchase can quickly eat into your expected profits.

Expectation 8: Your Investment Portfolio Will Manage Itself

During your working years, investing is relatively straightforward: you regularly buy broad index funds, reinvest the dividends, and ignore market volatility. You are in the accumulation phase. Once you retire, you shift into the decumulation phase, and the math changes entirely.

You can no longer afford to simply let your portfolio coast on autopilot. You must now navigate “Sequence of Returns Risk”—the danger of experiencing a major market downturn early in your retirement while simultaneously withdrawing funds to live on. Selling stocks while they are down permanently locks in losses and drastically reduces the capital available to catch the eventual market rebound.

To combat this, retirees must actively manage their asset allocation. This often means maintaining a “cash bucket” with one to two years of living expenses to ride out bear markets, while keeping the rest of the portfolio invested to outpace inflation. If you haven’t maximized your savings yet, take advantage of the IRS contribution limits while still working. In 2026, the 401(k) contribution limit is $24,500, with an $8,000 catch-up allowed for those 50 and older, and a new “super catch-up” of $11,250 for those aged 60 to 63.

Expectation 9: You Will Travel Non-Stop

The vision of spending your entire retirement jet-setting across Europe, cruising the Caribbean, and living out of a luxury RV is a staple of financial commercials. It is an appealing dream, but relentless travel is both financially draining and physically exhausting.

Many retirees discover that after a few months of constant movement, they miss the comfort of their own bed, their local community, and their daily routines. Health issues, mobility constraints, and the desire to be physically present for grandchildren’s milestones often curb the appetite for endless globetrotting. Instead of permanent vagabonding, most fulfilled retirees settle into a rhythm of taking one or two meaningful, well-planned trips a year, while finding deep satisfaction in local, low-cost activities closer to home.

What Can Go Wrong When Reality Bites

Failing to bridge the gap between expectation and reality can lead to severe consequences in your later years. The most critical risk is outliving your money. If you drastically underestimate healthcare costs or pull too much from your portfolio during an early market downturn, you could find yourself entirely dependent on Social Security in your 80s.

Another common pitfall is marital strain. Spouses often have wildly different, unspoken expectations about what retirement looks like. If one expects to travel the world while the other wants to putter in the garden, the resulting friction can be intense. Furthermore, “gray divorce” can instantly halve a couple’s assets while doubling their living expenses.

When to Consult a Professional

Navigating the transition into retirement involves irreversible decisions. You should seek guidance from a fee-only fiduciary financial planner or tax professional in the following scenarios:

- Five years before retirement: To stress-test your portfolio, determine a safe withdrawal rate, and decide if you need to work a few extra years.

- Before claiming Social Security: To run an analysis on optimal claiming strategies, especially if you are married and need to coordinate spousal and survivor benefits.

- When navigating Medicare enrollment: Missing your Initial Enrollment Period can result in permanent lifetime penalties on your Part B and Part D premiums.

- For tax-efficient withdrawal strategies: A professional can help you decide when to pull from taxable, tax-deferred, and tax-free (Roth) accounts to minimize your lifetime tax burden and manage future RMDs.

Frequently Asked Questions

Does my Social Security benefit increase with inflation?

Yes. The Social Security Administration applies an annual Cost-of-Living Adjustment (COLA) to help your benefits keep pace with inflation. However, this adjustment is often quickly absorbed by rising Medicare premiums.

At what age do I have to start taking money out of my retirement accounts?

Required Minimum Distributions (RMDs) currently begin at age 73 for those born between 1951 and 1959, and age 75 for those born in 1960 or later, according to IRS regulations.

Can I work while receiving Social Security benefits?

Yes, you can work while collecting Social Security. However, if you have not yet reached your Full Retirement Age (FRA), your benefits may be temporarily reduced if your earnings exceed the annual limit set by the SSA. Once you reach FRA, the earnings limit disappears entirely.

Will I get a bigger tax deduction when I turn 65?

Yes. The IRS offers an additional standard deduction for taxpayers age 65 and older. For 2026, the base standard deduction for a married couple filing jointly is $32,200, and seniors can add the extra age-based deduction on top of that, provided they do not itemize.

Building a Retirement Rooted in Reality

Shifting your mindset from what you hope will happen to what is statistically likely gives you a distinct advantage. You gain the power to adjust your asset allocation, rethink your healthcare safety net, and redefine your daily purpose while you still have the time and income to maneuver. Retirement is a dynamic transition rather than a static finish line. By aligning your expectations with reality, you protect your hard-earned wealth and give yourself the freedom to enjoy this chapter exactly as it unfolds.

Last updated: May 2026. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.