Are you ready to plan your health care costs?

Because of this inflation, people are a bit panicked, and that’s normal somehow. We’re all concerned, especially the retirees. A recent study shows that 17% of Americans are afraid of the high cost of living, and the ugly truth is that health care costs are even higher. And when you don’t have a fixed income, problems don’t cease to appear.

There are planning considerations to be mindful of because the prices are continuing to rise, especially on this matter.

What can we do? Is there a solution to this problem? Let’s take some notes and see what’s best for us in order to have a happy retirement.

1. Evaluate family history

This is a serious matter, and because your family’s medical history, longevity, and expectations can all have an impact on Medicare coverage, you should learn more about it. The concept of planning for health care is not simple, and it requires a forward-looking approach.

It’s guided by your finances, of course. And you have to keep in mind that it’s going to be a long time until you pass away. The leading conditions that often require long-term care include dementia, stroke, Parkinson’s disease, or even Alzheimer’s.

Before you retire, make sure you understand your family’s history. This can affect your healthcare costs more than you expect.

If you are not ready to do this by yourself, you can always hire a financial advisor or ask one of your family members to help you with the research.

TIP: If you are planning on getting insurance, long-term care insurance allows you to know that you’re protected as you age. It’s mostly for seniors and for people who are physically disabled.

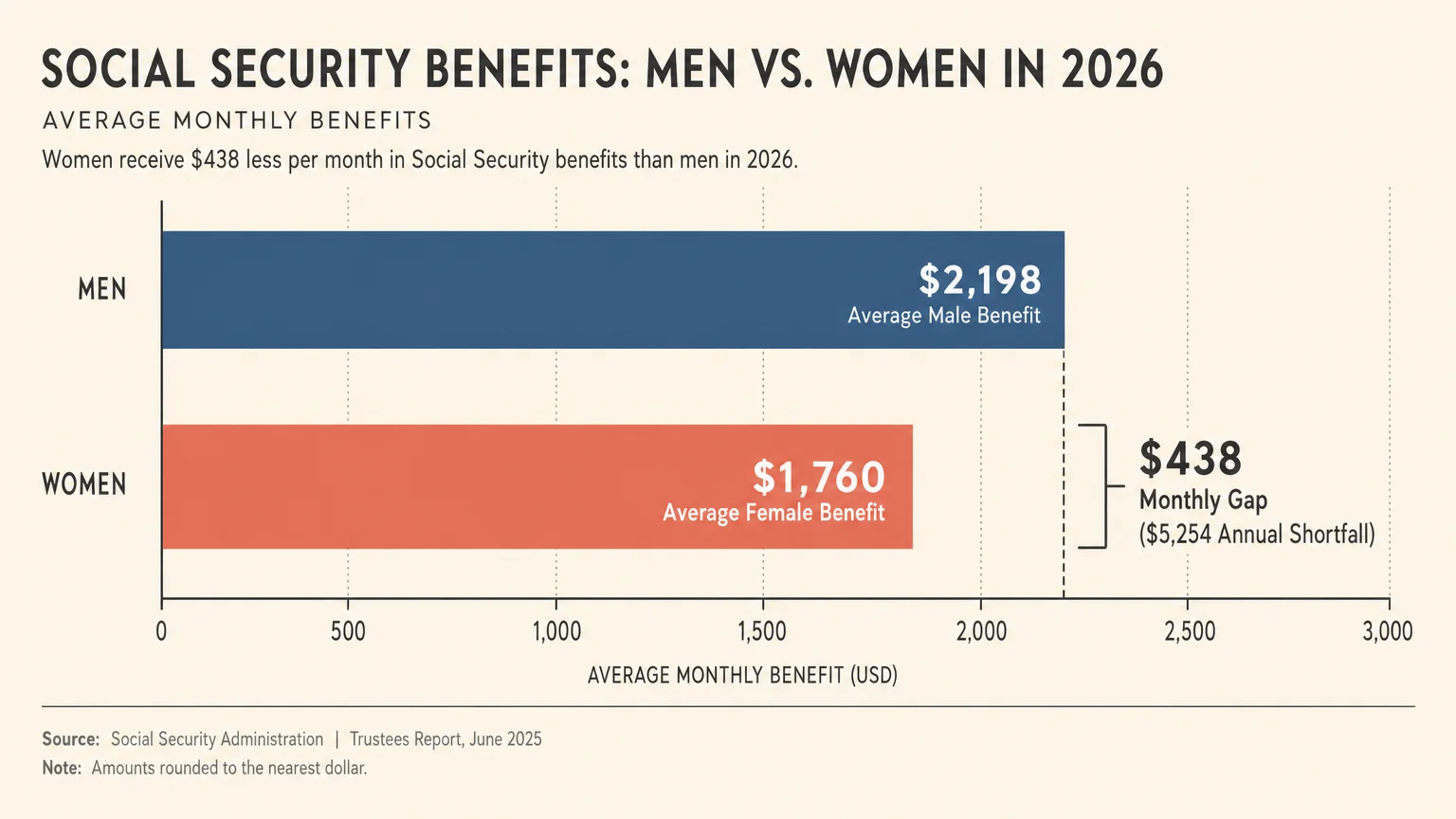

2. Social Security won’t cut it

A lot of us were pleased to hear that the Social Security Administration increased the Cost of Living Adjustment to 5.9% in 2022. This is by far the highest it has been since 1982, and that means a lot of seniors saw a healthy bump in their Social Security benefits. 2022 started out pretty well, right?

But let’s keep this in mind: the raise didn’t go that far, and a lot of statistics can prove it. And Medicare Part B premiums actually increased from last year by almost 15%.

Unfortunately, a good percentage of your Social Security will go to cover healthcare costs. A lot of studies have shown that plenty of people over 65 need at least 71% of their lifetime Social Security benefits to cover their medical expenses. And because of this, inflation can actually be even more expensive.

Because who knows how long it will last? And the bad news won’t stop here. Health expenditures will exceed Social Security income by 56% for those who are planning to retire in 20 years.

Other things that are contributing to higher health care costs are the COVID-19 pandemic, hospital consolidations, and the fact that nurses and other medical staff will have bigger salaries in the near future.

Even if it sounds harsh, don’t get discouraged! Make sure you plan everything in time in order to have a carefree retirement.

3. Turning 65 and still employed

Maybe you are already 65 but you’re still working and get health insurance through your employer or your spouse’s employer, and this is actually great because you have the opportunity to enroll in Medicare when you leave your employer plan through a Special Enrollment Period.

Medicare is an option to consider, but if your spouse continues to work, they will be able to cover you through their health care plan.

If you are not sure about what Medicare implies, you should talk to your HR department in order to find answers to your questions. Is it more expensive to stay in your employer’s plan or simply join Medicare? Which one is the best plan for your health needs?

4. Learn about your needs

When you are close to 60 years old, you need to spend some time looking for the best Medicare plan that suits you. When you become eligible at the age of 65, you will sign up during your 7-month initial enrollment period that begins 3 months before the month you turn 65. And there is a lot to know about Medicare. You have to know which plan is OK for you, if it’s an A, B, or D. What is your budget? How many people are in your family?

If you’re thinking about getting part A, it will cover the hospital costs after you meet your deductible. On the other hand, part B is optional coverage for medical expenses and requires an annual premium pack. Part D is for drug prescriptions and coverage.

Compare the overall costs and see the number of visits and co-pays or co-insurance per visit that you anticipate for the next year. And if you want to change your mind after that, it’s perfectly fine too. You can change the Medicare plan whenever you feel it doesn’t suit you anymore.

It’s pretty common for people to choose Medicare Parts A, B, and D when they are first eligible simply because the late enrollment penalty for doing so later is expensive.

5. Estimate costs

In order to have a good plan, first of all, you really need to estimate the costs. At this moment, even if you have Medicare, the average health care cost can reach up to $5,000 per year. And some advance planning is recommended. because you will prepare yourself for the years to come.

Start thinking about the timeline logistics a few years before your retirement. For example, someone plans on retiring at 62, but that’s a bit rushed because they won’t be eligible for Medicare until 65. And they have to determine how they will cover the healthcare expenses for three years.

If you are married, then you can rely on your partner’s health insurance plan if they are not planning the exact same date of retirement as you. Another solution might be to find yourself a short-term insurance plan to cover all the expenses.

If you are not fully prepared for these years, you might need to dig into your savings, and that will be unfortunate. How often do you think about this?

6. The time to plan is now

Studies have shown that a couple that is 47 years old and earns a 6% annual rate of return will actually need to invest an additional $27,000 to make up for their projected $215,000 in additional health care expenses, taking into consideration inflation. And it’s pretty expensive, right? Imagine how awful it would be if this inflation brought the current 45-year-old medical expenses to around $1,803,526. That’s why it’s the perfect time to start saving as soon as possible.

If your employer offers this, it’s time to think about a 401(k) or IRA. This will actually help you keep the money in one place regardless of your age. If you already have a health plan, you may be able to pair it with an HSA. Don’t forget to read more about this subject to find out the details that matter to you and your choices.

You have to understand how paying for future health care fits into your overall budget and what your retirement income will be. If you are 50, you will be able to make up for the savings shortfall with additional catch-up contributions that rely on your 401(k) or IRA.

What are your plans regarding retirement? Do you feel fully prepared?

In case you need some more financial advice, you are more than welcome to read about the Finances in Retirement: 7 Honest Things Nobody Tells You.