The latest estimates forecast a 3.8% Social Security cost-of-living adjustment (COLA) for 2027, driven by unexpectedly stubborn inflation. If this projection holds, you will see your monthly payments increase by about $79 on average starting in January.

Preparing for this change requires understanding how higher prices impact both your benefits and your broader retirement budget. Because the official announcement does not happen until October, you have a crucial window right now to assess your financial plan.

Knowing how the upcoming adjustment interacts with your Medicare premiums, taxes, and daily expenses empowers you to make proactive spending and investing decisions. Rather than waiting for an official notice in the mail, you can take control of your financial future today.

The Numbers Behind the 2027 COLA Forecast

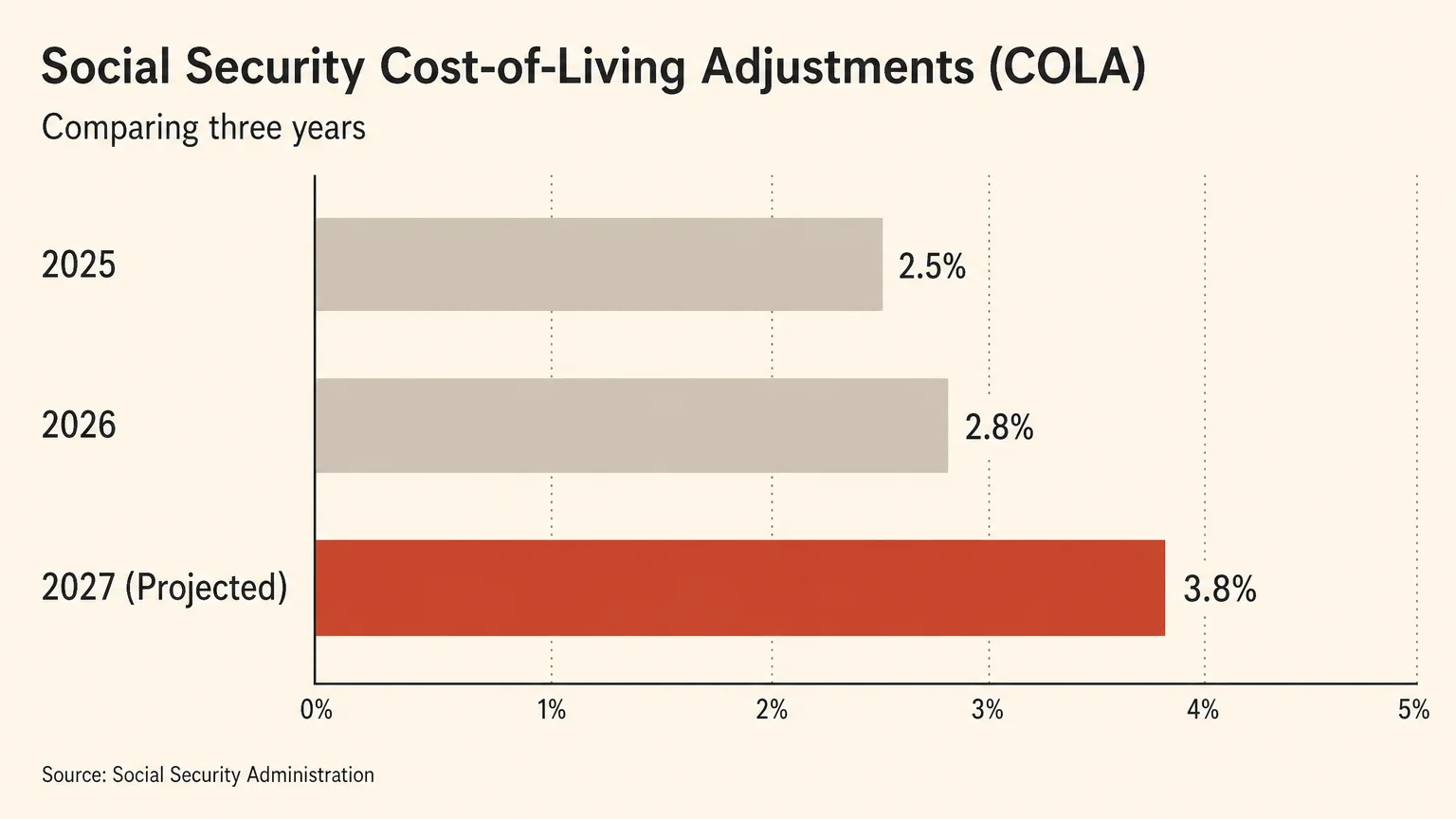

Tracking the upcoming cost-of-living adjustment allows you to forecast your baseline retirement income months before the official declaration. According to June 2026 data from the Senior Citizens League (TSCL)—a prominent nonpartisan senior advocacy group—the 2027 COLA is currently projected at 3.8 percent.

This represents a significant upward shift from their earlier estimates of 2.8 percent, largely fueled by recent consumer price index reports showing inflation running hotter than economists anticipated.

To put this projection into perspective, you need to look at the current benefit landscape. According to the Social Security Administration (2026), the average monthly benefit for retired workers reached $2,081.16 in the spring of 2026. A 3.8 percent increase on that average amount translates to a monthly boost of roughly $79.08, or nearly $950 in additional income over the course of the year.

If you delay claiming until your full retirement age and qualify for the maximum benefit—which stands at $4,152 per month in 2026—a 3.8 percent adjustment would add over $157 to your monthly check.

This projected rate marks a noticeable increase from the adjustments seen in the past two years. Retirees received a 2.5 percent COLA for 2025 and a 2.8 percent adjustment for 2026.

A 3.8 percent bump for 2027 would provide the largest benefit boost in four years. However, an increased gross benefit does not automatically equal a proportionately larger deposit in your bank account. The actual amount you take home depends entirely on your specific deductions, your tax liabilities, and your Medicare enrollment status.