How Part-Time Work Impacts Social Security and Taxes

Generating income during retirement requires careful coordination with your existing benefits and tax strategies. Earning money from a gig does not exist in a vacuum; it directly impacts how the federal government views your total financial picture.

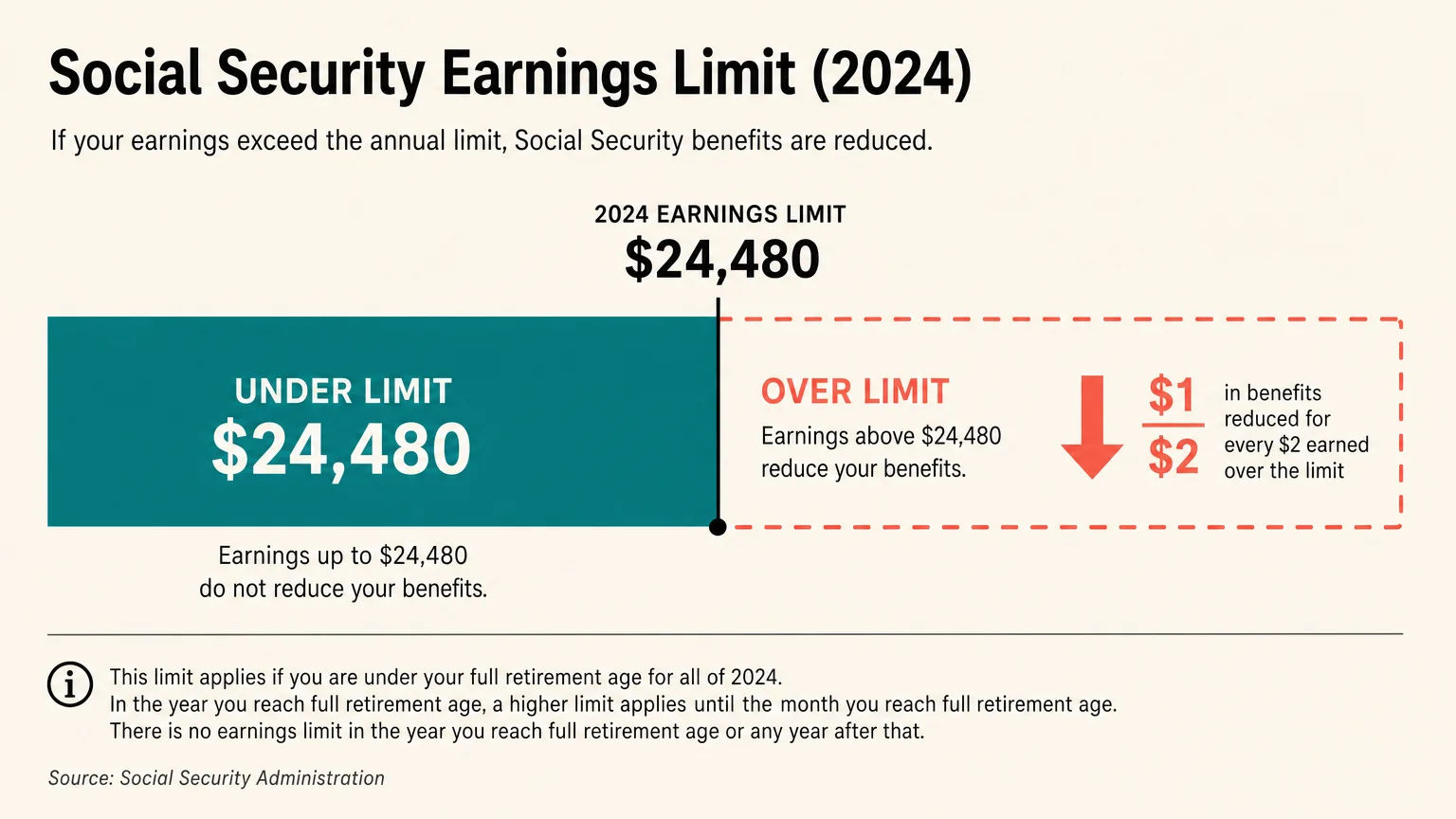

Social Security Earnings Limits

If you claim Social Security benefits before reaching your Full Retirement Age (FRA) and continue to work, you are subject to the annual earnings test. According to the Social Security Administration, the earnings limit for 2026 is $24,480. If you earn more than this amount, the SSA will withhold $1 in benefits for every $2 you earn over the limit.

There is a special rule for the specific year you reach your FRA. In 2026, the limit jumps to $65,160 for the months prior to your birth month, and the withholding penalty softens to $1 for every $3 over the limit. The moment you reach your Full Retirement Age, the earnings limit disappears completely. From that month forward, you can earn as much gig income as you desire without any reduction to your Social Security checks.

The 2026 Tax Landscape for Retirees

Adding part-time income to your Social Security, pensions, and required minimum distributions (RMDs) could push you into a higher tax bracket. However, older adults benefit from generous deductions that shield a significant portion of this income.

For the 2026 tax year, the IRS set the baseline standard deduction for a single filer at $16,100, plus an additional $2,050 for being age 65 or older, bringing your total standard deduction to $18,150. Married couples filing jointly where both spouses are 65 or older enjoy a robust standard deduction of $35,500 ($32,200 base plus $3,300 in senior allowances). If your total taxable income falls below these thresholds, your federal income tax burden remains remarkably low.