The IRS has finalized significant tax code updates for 2026, delivering larger family tax credits and a brand-new $6,000 bonus deduction for seniors. If you are a grandparent raising a grandchild, still working, or simply managing your retirement income, these changes can dramatically lower your federal tax bill. The Child Tax Credit jumps to $2,200 per qualifying dependent, while the maximum Earned Income Tax Credit expands past $8,200. Older Americans also gain unprecedented standard deduction increases, allowing some married couples to shield nearly $50,000 of income from federal taxes. Navigating these updated thresholds requires proactive planning, so you must understand how the 2026 rules apply to your household before you file.

The 2026 Child Tax Credit: What Grandparents and Parents Need to Know

Many retirees assume family tax credits no longer apply once their own children leave the nest. However, millions of grandparents serve as primary caregivers for their grandchildren. If you fall into this category, the updated 2026 Child Tax Credit offers substantial financial relief.

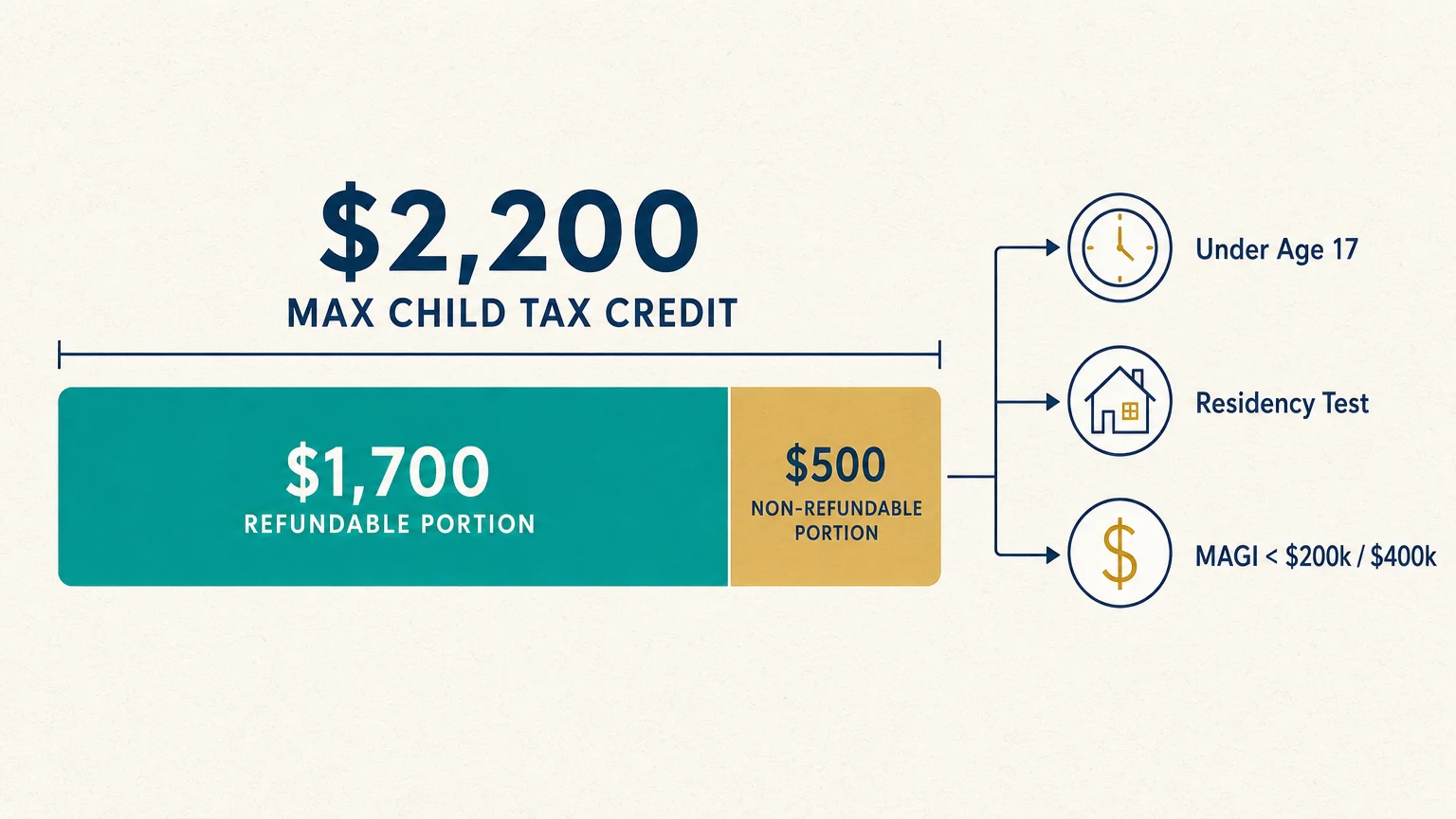

For the 2026 tax year, the IRS increased the maximum Child Tax Credit to $2,200 per qualifying child—up from the previous $2,000 threshold. Furthermore, up to $1,700 of this credit is fully refundable. A refundable tax credit is exceptionally valuable because it does not just reduce your tax liability to zero; the IRS will send you a direct check for the remaining refundable balance.

To claim your grandchild, niece, nephew, or other qualifying relative, you must satisfy several strict IRS dependency requirements:

- Age Test: The dependent child must be under age 17 at the end of the 2026 calendar year.

- Relationship Test: The child can be your son, daughter, stepchild, foster child, grandchild, niece, or nephew.

- Residency Test: The dependent must have lived in your home for more than half of the year.

- Support Test: The child cannot provide more than half of their own financial support.

- Income Limits: The full $2,200 credit is available if your Modified Adjusted Gross Income (MAGI) is under $200,000 as a single filer or $400,000 if married filing jointly. Above these levels, the credit amount begins to phase out.

Earned Income Tax Credit Expansions for Older Workers

Retirement looks vastly different today than it did a generation ago. Many seniors choose to work part-time, consult, or launch small businesses during their retirement years. If you generate income from working, you might qualify for the Earned Income Tax Credit (EITC), which sees significant inflation adjustments for 2026.

For 2026, the maximum EITC payout climbs to $8,231 for taxpayers with three or more qualifying children. Even if you do not have dependents living with you, eligible single workers can still claim a maximum credit of $664.

However, the EITC rules feature strict income limitations that frequently catch retirees off guard. The IRS draws a hard line between “earned” income and “passive” income. Wages, salary, tips, and self-employment earnings count as earned income. Conversely, Social Security benefits, pension payouts, and withdrawals from your 401(k) or IRA do not count toward EITC eligibility.

You must also closely monitor your investment income. For 2026, the IRS disqualifies anyone with more than $12,200 in investment income—such as dividends, interest, and capital gains—from claiming the EITC, regardless of how much earned income they generated. If you plan to realize capital gains in your portfolio, you should weigh the tax consequences against the potential loss of your EITC.

The Adoption Tax Credit: Now Partially Refundable

Expanding your family through adoption involves substantial financial costs, whether you are adopting through the foster care system, stepping in to legally adopt a family member, or pursuing a private adoption. The IRS Adoption Tax Credit exists to offset these heavy financial burdens, and the 2026 rules introduce a massive structural improvement for families.

For 2026, the maximum Adoption Tax Credit reaches $17,280 per eligible child. While this high limit is helpful, the most important update revolves around refundability. Thanks to recent legislative changes, this credit is now partially refundable up to $5,000 per qualifying child.

Previously, the entire adoption credit was strictly nonrefundable, meaning it could only wipe out your existing tax bill. If your tax liability was low—a common scenario for retirees heavily reliant on Social Security—the credit offered little immediate cash benefit. Now, even if you owe zero federal income tax, you can receive up to $5,000 back as a direct refund from the IRS.

Eligible expenses include reasonable and necessary adoption fees, court costs, attorney fees, and travel expenses directly related to the legal adoption process. Keep meticulous records of these expenses, as the IRS frequently requires strict documentation to process this specific credit.

The New 2026 Senior Bonus Deduction (A Total Game Changer)

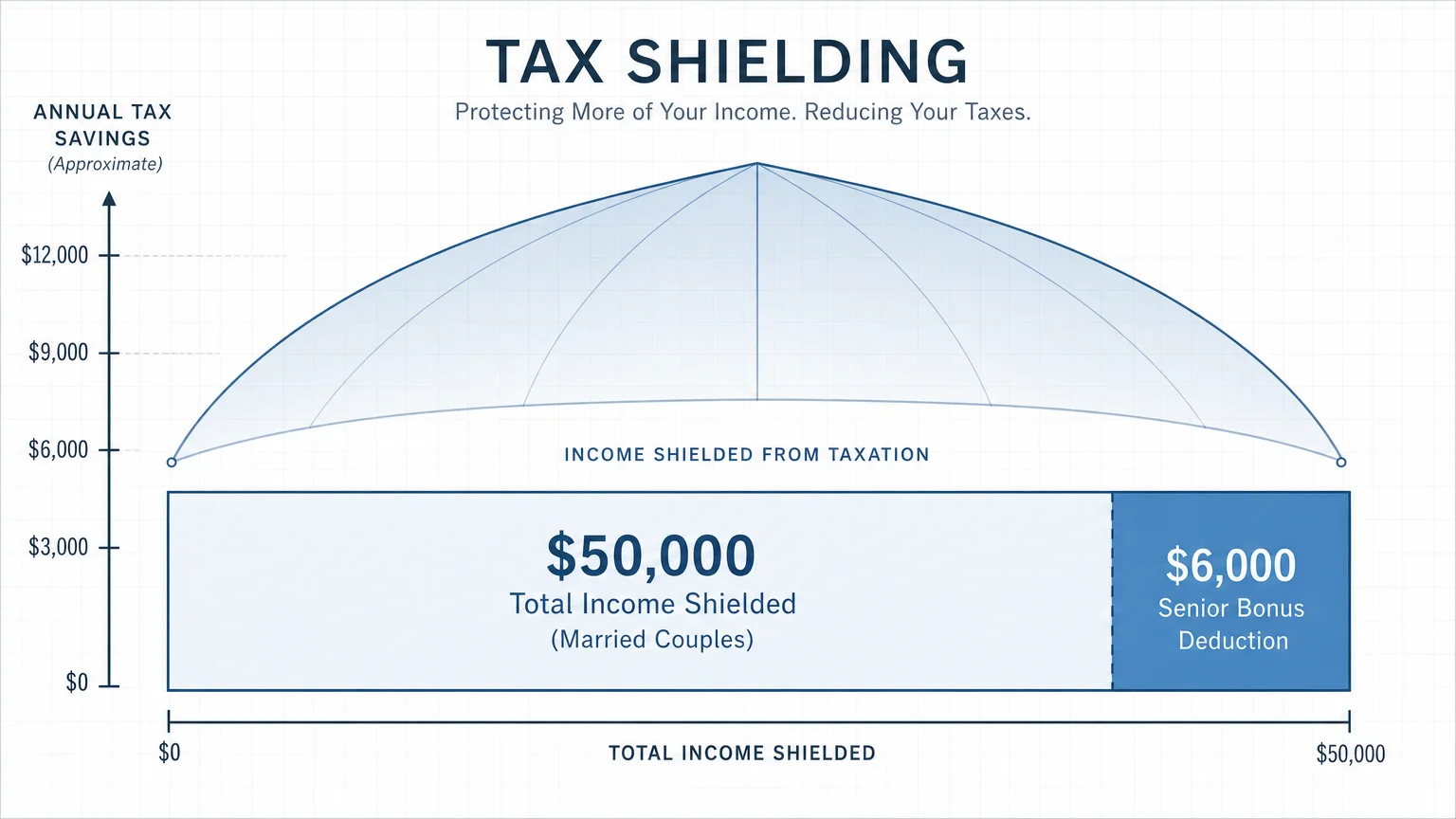

While family credits provide targeted relief, the most sweeping change for retirees in 2026 is the introduction of a massive standard deduction enhancement for seniors. Enacted under recent tax legislation, this new deduction layers on top of the traditional standard deduction, creating unprecedented tax-shielding opportunities for older Americans.

To understand the magnitude of this change, you have to look at how the IRS deductions stack up. In 2026, the base standard deduction rises to $16,100 for single filers and $32,200 for married couples filing jointly. On top of that base, the IRS continues to offer the traditional age 65+ standard deduction bump, which adds $2,050 for singles and $1,650 per qualifying spouse for joint filers.

The true game changer is the brand-new $6,000 “senior bonus” deduction for individuals age 65 and older. If you are married and both spouses are 65 or older, you receive a $12,000 combined bonus deduction.

Let us look at exactly how much income you can shield from federal taxes in 2026 without needing to itemize a single receipt:

| Filing Status (Age 65+) | Base 2026 Standard Deduction | Standard Age 65+ Add-On | New 2026 Senior Bonus | Total 2026 Deduction Amount |

|---|---|---|---|---|

| Single Filer | $16,100 | $2,050 | $6,000 | $24,150 |

| Married Filing Jointly (One Spouse 65+) | $32,200 | $1,650 | $6,000 | $39,850 |

| Married Filing Jointly (Both 65+) | $32,200 | $3,300 | $12,000 | $47,500 |

This stacking effect means a married couple over 65 can earn up to $47,500 completely tax-free at the federal level. This massive deduction can drastically reduce the taxes you owe on required minimum distributions (RMDs) or pension income.

However, the IRS imposes strict income phase-outs on the new $6,000 bonus deduction. The bonus begins to phase out at a rate of 6 percent for taxpayers with a Modified Adjusted Gross Income over $75,000 for singles and $150,000 for joint filers. Strategic income timing—such as carefully choosing when to take IRA withdrawals—becomes vital to keep your MAGI below these thresholds.

“The biggest mistake retirees make is assuming their tax situation is set in stone. With major shifts in the standard deduction and family credits, proactive income planning is the only way to protect your wealth.” — Ed Slott, CPA and Retirement Tax Expert

Common Mistakes to Avoid

Tax laws are notoriously rigid. A simple misinterpretation of the 2026 rules can trigger IRS letters, delayed refunds, or lost financial benefits. Protect your household by avoiding these common missteps.

Assuming Dependency Without the Residency Test

Grandparents frequently provide substantial financial support to their grandchildren without the child actually living in their home. The IRS strictly enforces the residency rule for the Child Tax Credit. To claim the credit, the dependent must live in your home for more than half of the year. Financial support alone does not grant you the right to claim the tax credit.

Ignoring the EITC Investment Income Limit

You might assume your part-time job easily qualifies you for the Earned Income Tax Credit. However, if you sell a large chunk of stock, take a sizable capital gain, or collect significant dividends, you could accidentally cross the $12,200 investment income limit. Once you exceed that limit by even one dollar, you forfeit the entire EITC.

Failing to Monitor the Senior Deduction Phase-Outs

The new $6,000 senior bonus deduction is a powerful tool, but high-income retirees will lose it if they ignore their MAGI. Because the phase-out starts at $150,000 for married couples, taking an unnecessarily large IRA withdrawal to buy a new car or fund a home renovation could push your income past the limit, simultaneously increasing your tax bracket and stripping away your bonus deduction.

Professional vs. Self-Guided Tax Planning

Deciding how to file your 2026 taxes depends heavily on your income complexity and household dynamic. While basic returns are easy to handle at home, the new credits and deductions add layers of strategic planning.

Scenario 1: You have straightforward retirement income

If your only income sources are Social Security and a modest standard pension, and your MAGI easily falls below the $75,000 single or $150,000 joint phase-out limits, self-guided filing is highly effective. You will naturally claim the full $47,500 joint standard deduction without needing complex tax software or professional intervention. Free resources like the AARP Foundation Tax-Aide program provide excellent guidance for these straightforward scenarios.

Scenario 2: You are claiming dependents for the first time in decades

If your adult child recently moved back home with their children, determining who has the legal right to claim the Child Tax Credit and the Earned Income Tax Credit becomes complicated. The IRS “tie-breaker” rules dictate who gets the credit when multiple people live in the same house. Consulting a certified public accountant (CPA) prevents duplicate filing errors and ensures your family maximizes the available refund.

Scenario 3: You are managing heavy capital gains and part-time income

If you work a part-time job to qualify for the EITC but also manage a taxable brokerage account, you need professional guidance. A tax planner can help you perform tax-loss harvesting to keep your investment income below the $12,200 EITC disqualification threshold, ensuring you get the best of both worlds.

Scenario 4: You finalized a family adoption

The Adoption Tax Credit requires precise record-keeping and involves complex carry-forward rules for nonrefundable portions. Because the 2026 updates introduce a partially refundable $5,000 tier, you want a professional to correctly fill out Form 8839 to ensure you receive the cash refund you are owed without triggering an audit.

Frequently Asked Questions

How much is the Child Tax Credit for 2026?

For the 2026 tax year, the maximum Child Tax Credit is $2,200 per qualifying child under age 17. Up to $1,700 of this credit is refundable through the Additional Child Tax Credit.

Can I claim the Child Tax Credit if I am retired and only receive Social Security?

While you can technically claim the credit, the Child Tax Credit is generally designed to offset earned income tax liabilities. To access the refundable portion (the Additional Child Tax Credit), you generally need a certain amount of earned income. If your only income is Social Security, you may not see a direct cash benefit.

What is the new standard deduction for seniors in 2026?

The base standard deduction is $16,100 for singles and $32,200 for joint filers. Seniors age 65 and older receive an additional age-based add-on ($2,050 single / $1,650 joint). Additionally, new tax rules for 2026 provide a $6,000 bonus deduction per senior, bringing the total potential standard deduction for a qualifying married couple (both over 65) to $47,500.

Does Medicare IRMAA affect my family tax credits?

The Medicare Income-Related Monthly Adjustment Amount (IRMAA) does not directly change your tax credits. However, both IRMAA surcharges and family tax credits rely heavily on your Modified Adjusted Gross Income (MAGI). If your MAGI spikes due to investment sales or IRA withdrawals, you could simultaneously lose your tax credits, lose your new senior bonus deduction, and trigger a steep Medicare premium surcharge.

As the IRS implements these massive 2026 tax updates, you have a brief window to optimize your income strategy. Whether you are claiming a grandchild for the new $2,200 Child Tax Credit, tracking your earned income for the EITC, or shielding your retirement savings behind the new $47,500 joint senior standard deduction, the rules demand your attention. Review your projected 2026 income now, adjust your withholding or estimated payments, and take full advantage of the most generous tax code older Americans have seen in decades.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.