The Tax Torpedo: When Extra Income Makes Benefits Taxable

While your gross monthly benefit remains safe, the net amount you keep after taxes is highly vulnerable. This is where the concept of the “tax torpedo” comes into play. The federal government taxes Social Security benefits based on a specific formula known as “combined income.” To find your combined income, you add your adjusted gross income (AGI), any nontaxable interest you earned, and exactly 50 percent of your annual Social Security benefits.

The Internal Revenue Service uses strict, unadjusted thresholds to determine taxation:

- Individual Filers: If your combined income falls between $25,000 and $34,000, you may have to pay income tax on up to 50 percent of your benefits. If your combined income exceeds $34,000, up to 85 percent of your benefits become taxable.

- Joint Filers: If you and your spouse have a combined income between $32,000 and $44,000, up to 50 percent of your benefits are taxable. If your combined income crosses the $44,000 line, up to 85 percent of your benefits are subject to federal income tax.

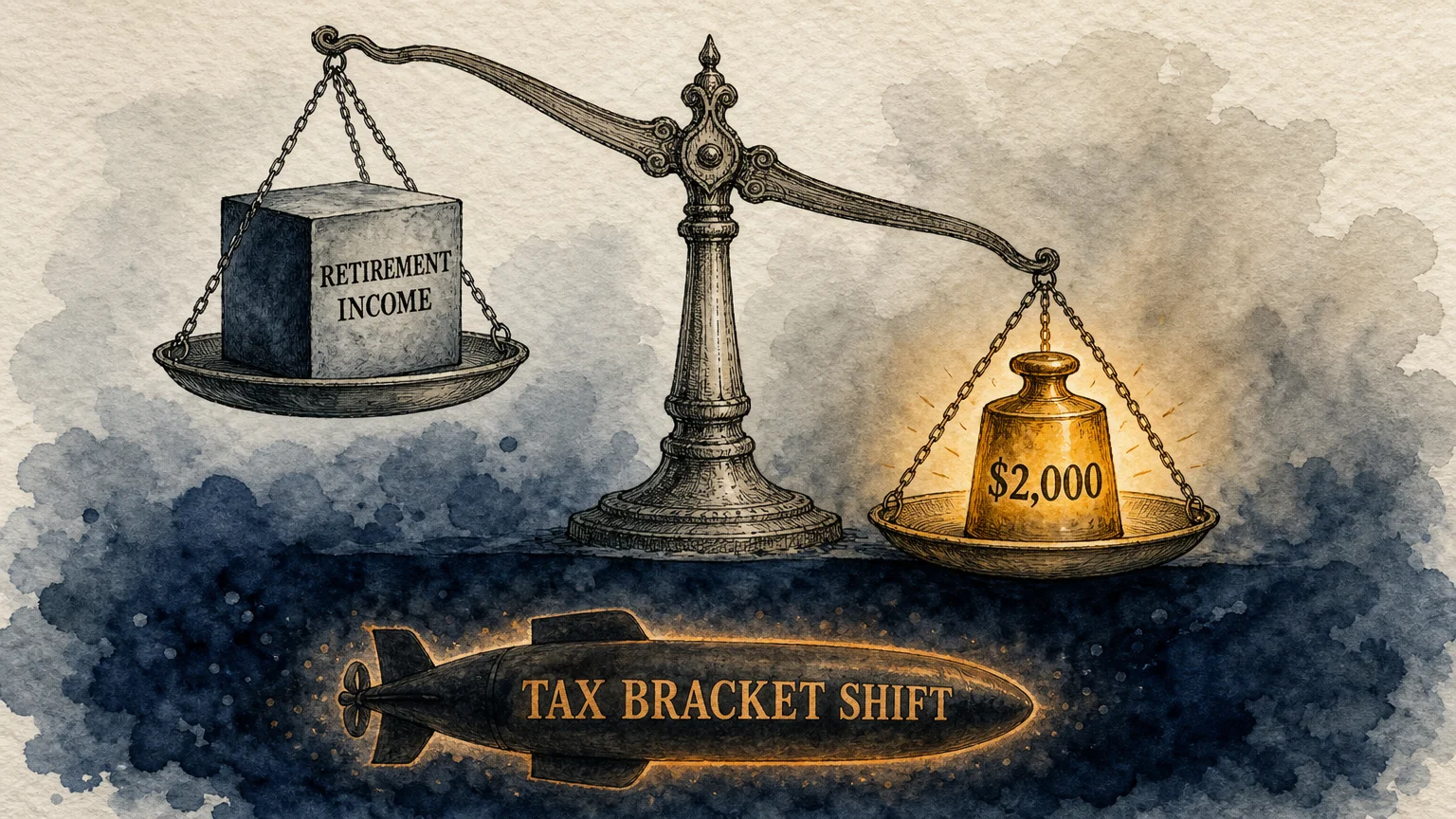

If Congress decides to classify a new proposed $2,000 payment as taxable income, it will immediately increase your adjusted gross income. For retirees hovering right on the edge of these taxation cliffs, that extra $2,000 can push a significant portion of their previously untaxed Social Security benefits into the taxable category.

This creates a compounding effect; the extra income not only brings its own tax burden but also drags your core benefits into the IRS’s reach. Careful monitoring of your total household income ensures you can adjust your IRA withdrawals or charitable giving to offset this potential tax trap.