The “Big Three” Unexpected Costs: Healthcare, Housing, and Taxes

While life can throw any number of curveballs, three areas consistently surprise new retirees with their true costs. Thinking through them now can save you a world of trouble later.

Healthcare Beyond the Premiums

Most of us know we’ll have Medicare in retirement, and we plan for the monthly premiums. But those premiums are just the beginning of the story. The real costs often lie in the services that Medicare doesn’t fully cover.

Think about deductibles, copayments, and coinsurance. These are the amounts you pay out of your own pocket before your insurance starts paying, or your share of the cost for a doctor’s visit or procedure. These can add up quickly, especially if you have a chronic condition or an unexpected medical event.

Then there are the big three of senior health: dental, vision, and hearing. Original Medicare generally doesn’t cover routine check-ups, fillings, glasses, or hearing aids. These can be significant retirement expenses, with hearing aids alone costing thousands of dollars. Many retirees are surprised to find themselves paying for these entirely out-of-pocket or purchasing separate private insurance plans to cover them.

The largest and most intimidating potential healthcare cost is long-term care. This isn’t medical care, but help with daily activities like dressing, bathing, or eating. It can be provided at home, in an assisted living facility, or in a nursing home. The costs are staggering, and it’s a critical piece of senior financial planning that is too often ignored. You can find more information about your options directly on the official Medicare.gov website.

Action Step: Start by building a “health savings” bucket within your retirement funds. Budget not just for your premiums but also for a reasonable amount of out-of-pocket costs each year. Research Medicare Advantage and Medigap plans long before you enroll to see how they might help cover these gaps.

The Unchanging Cost of “Home”

Congratulations! You’ve paid off your mortgage. It’s a monumental achievement. But that doesn’t mean you’ll be living for free. The costs of homeownership never truly disappear.

Property taxes and homeowner’s insurance are the most obvious ongoing expenses. These rarely go down; in fact, they usually creep up over time. But the real budget-busters are the major repairs. A new roof can cost $10,000 to $20,000. A new HVAC system can be just as expensive. These aren’t small, incidental costs; they are major capital expenditures that you need to plan for.

Furthermore, as we age, our homes may need to change with us. Aging in place is a wonderful goal, but it can come with a price tag. Installing grab bars in the bathroom, building a ramp for the front steps, or even widening doorways for a walker are all modifications that cost money.

Even downsizing has hidden costs. While you might free up equity, you’ll still face moving expenses, potential realtor commissions, closing costs, and the costs of furnishing or modifying your new, smaller space.

Action Step: Create a separate savings account specifically for home maintenance. Think of it as paying yourself a small “mortgage” each month. Putting aside $150 to $300 a month can create a substantial fund over a few years, turning a potential crisis into a manageable expense.

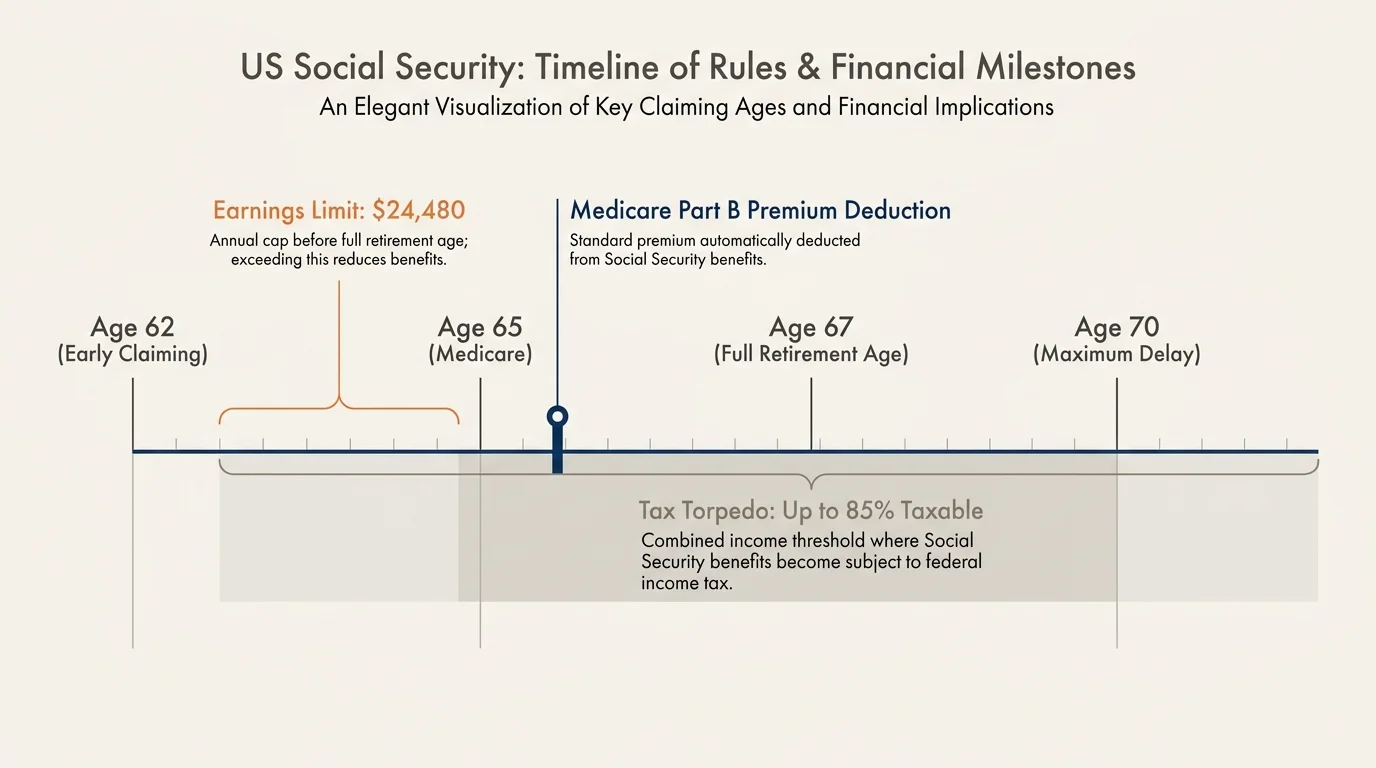

The Surprise Tax Bill

One of the biggest financial surprises for seniors is discovering that retirement doesn’t mean you stop paying taxes. Most of the income you rely on in retirement is likely taxable.

Withdrawals from traditional 401(k)s, 403(b)s, and traditional IRAs are taxed as ordinary income. So are payments from most pensions. But the real shock for many is that a portion of their Social Security benefits can be taxable, too.

Whether your benefits are taxed depends on your “provisional income.” Provisional income is a measure used by the IRS to determine taxability. It’s calculated by taking your adjusted gross income (AGI), adding any non-taxable interest (like from municipal bonds), and then adding half of your annual Social Security benefits.

If that total is above a certain threshold, you’ll owe taxes on up to 85% of your benefits. The rules and thresholds can be found on the official IRS website, and it’s a good idea to check them as they can change.

Mini-Math Example: A Look at Provisional Income

Let’s imagine a married couple, Sarah and Tom, filing their taxes jointly.

– They withdraw $40,000 from their traditional IRA.

– They receive a total of $30,000 in Social Security benefits for the year.

– They have no other income or tax-exempt interest.

First, we find half of their Social Security: $30,000 / 2 = $15,000.

Next, we add that to their other income: $40,000 (from the IRA) + $15,000 = $55,000.

Their provisional income is $55,000. Because this amount is well above the IRS threshold for married couples (which was $32,000 for the 2023 tax year), a significant portion of their Social Security benefits will be subject to federal income tax.

Action Step: Don’t let taxes be a year-end surprise. You can ask the Social Security Administration to withhold federal taxes from your benefit checks. You can do this by completing an IRS Form W-4V (Voluntary Withholding Request) and sending it to your local Social Security office. You can choose to have 7%, 10%, 12%, or 22% withheld, giving you more control over your tax situation.