Major shifts in federal policy are fundamentally rewriting how Americans save for the future, placing powerful new tools—and risks—directly into your hands. President Trump’s recent executive orders and the Department of Labor’s latest rulings have unlocked sweeping changes for both workplace 401(k)s and individual savers. If you lack access to an employer-matched plan, upcoming federally matched accounts could finally bridge your savings gap. Conversely, if you already hold a traditional 401(k), new rules allowing alternative assets like private equity and cryptocurrency mean you must navigate a vastly more complex investment landscape. Understanding exactly how these proposals work ensures you maximize new federal dollars while protecting your hard-earned nest egg.

What the New Retirement Rules Actually Mean

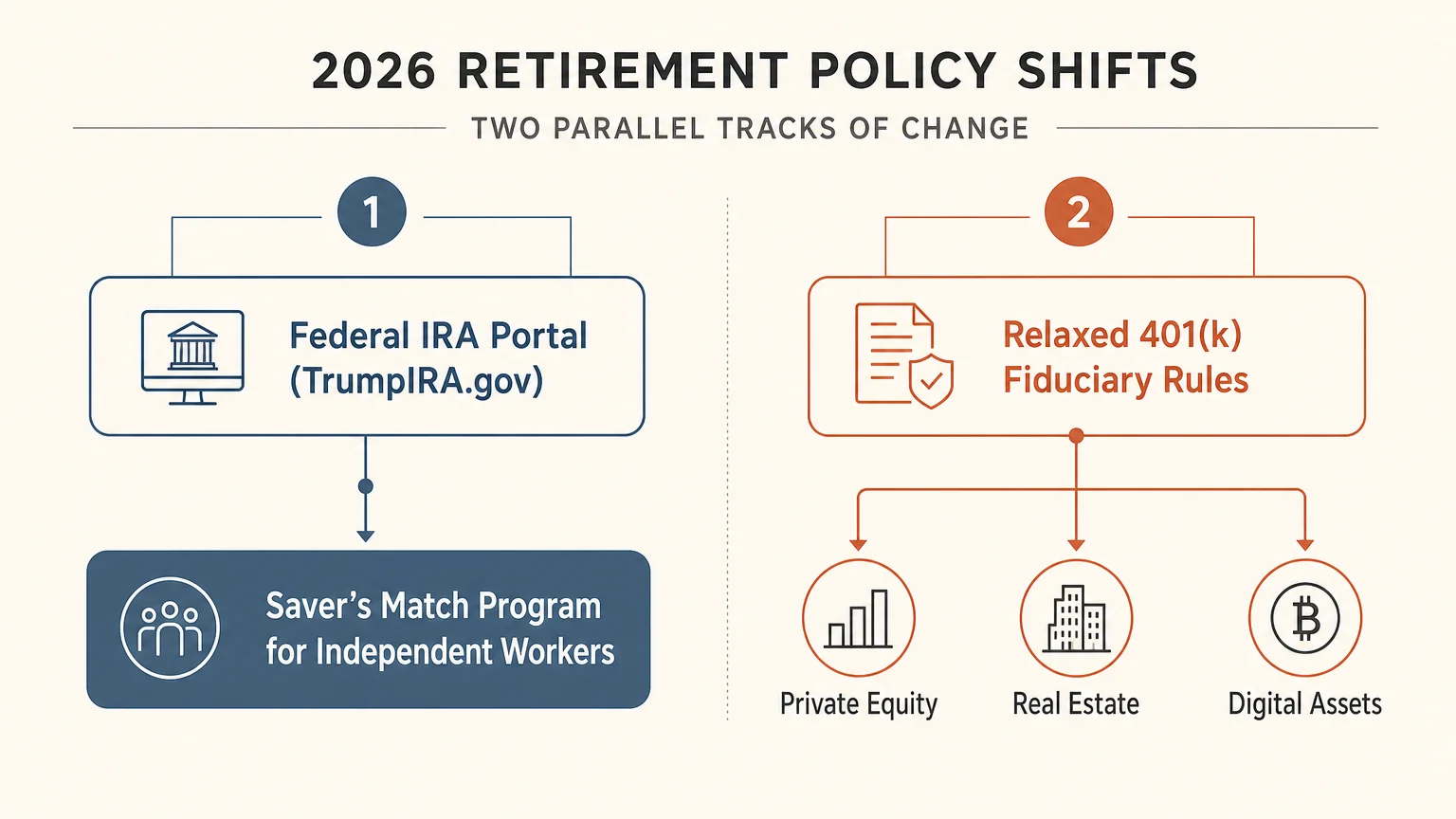

The retirement landscape of 2026 looks significantly different than it did just a few years ago. The central changes stem from two distinct but overlapping policy shifts: the rollout of government-backed IRA platforms for independent workers and the relaxation of investment restrictions inside traditional 401(k) plans.

Recent data suggests that roughly 56 million American workers lack access to an employer-sponsored retirement plan. To address this, the current administration recently signed executive orders establishing a centralized federal portal, slated to launch as TrumpIRA.gov by early 2027. This system connects freelancers, gig workers, and small business employees with low-cost private Individual Retirement Accounts (IRAs). More importantly, it integrates with the incoming Saver’s Match program—a provision originally embedded in the SECURE 2.0 Act—which transforms how the federal government incentivizes lower-income savers.

At the same time, the Department of Labor finalized process-based safe harbors for 401(k) plan fiduciaries. Historically, employer plans stuck to traditional mutual funds and index funds. The new rules democratize access to alternative assets, allowing your 401(k) to potentially invest in private equity, real estate, private credit, and even digital assets. This structural change attempts to give everyday workers the same wealth-building tools previously reserved for institutional investors and high-net-worth individuals.

The Winners: Who Stands to Gain the Most?

Any major shift in tax code or retirement policy inevitably creates a specific class of beneficiaries. Based on the current framework, two very different groups stand to reap the largest rewards.

Freelancers and Lower-Income Savers

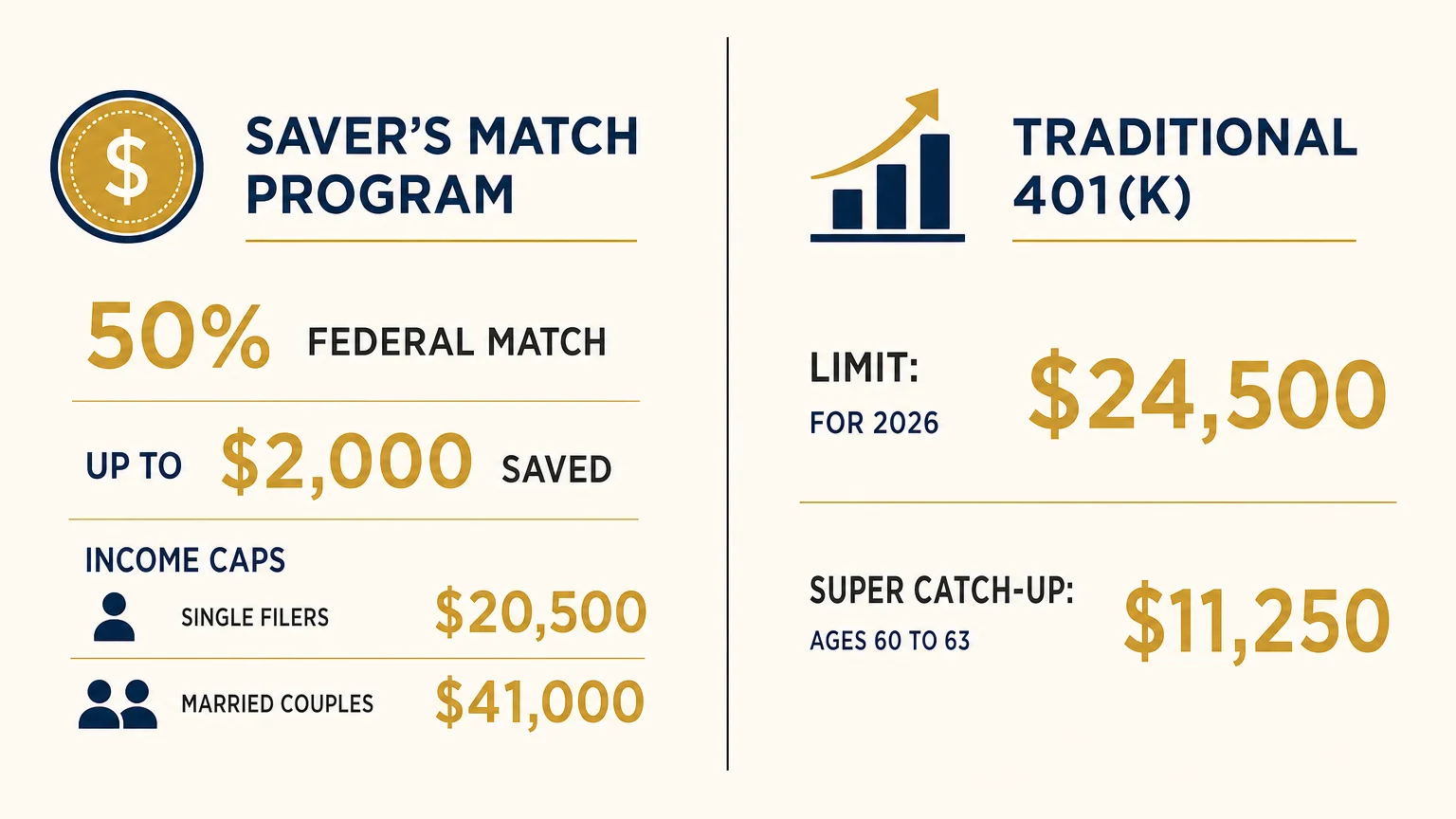

If you fall into the lower-to-middle income bracket and do not receive a 401(k) match from your employer, the upcoming Saver’s Match could prove highly lucrative. Starting in 2027, the federal government provides a 50 percent matching contribution on the first $2,000 you save into a qualifying retirement account. That means you could receive up to $1,000 directly deposited into your retirement account by the Treasury.

To qualify for the full match in 2027, single tax filers must earn $20,500 or less, with the benefit phasing out completely at $35,500. For married couples filing jointly, the full match applies to household incomes up to $41,000, phasing out at $71,000. While the income limits remain strict, earning a guaranteed 50 percent return on a $2,000 investment presents an unprecedented opportunity for a gig worker or part-time employee.

High-Net-Worth Investors and Fund Managers

On the opposite end of the spectrum, high-income earners with established 401(k)s also benefit, albeit in an entirely different way. The IRS increased standard 401(k) contribution limits to $24,500 for 2026. Furthermore, a new “super catch-up” provision allows workers aged 60 to 63 to contribute an extra $11,250. If your employer opts to include alternative assets in their plan under the new Department of Labor guidelines, you will soon have the ability to diversify your tax-advantaged accounts with private equity or real estate—asset classes that historically offer higher potential yields to offset market volatility.

“The greatest enemy of a good plan is the dream of a perfect plan. Stick to the basics of low-cost diversification, but remain open to structural advantages when the tax code shifts in your favor.” — John Bogle, Founder of Vanguard

The New Rules on Alternative Assets in Your 401(k)

You may soon notice new investment options appearing on your workplace 401(k) dashboard. Executive orders aimed at reducing regulatory red tape have given plan administrators a “safe harbor” to include private market funds.

Private equity and private credit operate outside public stock exchanges. They involve directly investing in private companies or lending money to corporations. Because these assets lack liquidity—meaning you cannot buy and sell them as easily as shares of public companies—they often demand a premium return. Proponents argue that locking everyday investors out of these markets restricts their ability to grow wealth, especially as companies stay private longer before holding an initial public offering.

However, this access arrives with substantial caveats. Alternative assets typically carry much higher management fees than traditional mutual funds or exchange-traded funds (ETFs). The Securities and Exchange Commission (SEC) frequently reminds investors that complex products require a deep understanding of the underlying risks. A private real estate fund might freeze withdrawals during an economic downturn, leaving you unable to access your money when you need it most.

Who Could Be Left Out—or Left Behind

Despite the optimistic framing of the new rules, millions of Americans sit in a precarious middle ground where they receive little to no benefit from the proposals.

- The Middle-Class Donut Hole: If you are a single filer making $45,000 a year, you earn too much to qualify for the new federal Saver’s Match. If your employer does not offer a 401(k) match, you must still rely entirely on your own contributions to build your nest egg, gaining no leverage from the new policies.

- Conservative Retirees: If you are already retired and taking distributions, changes to accumulation rules offer you no immediate value. You remain subject to standard Required Minimum Distribution (RMD) rules and current tax brackets.

- Uninformed Investors: The democratization of alternative assets poses a genuine risk to workers who simply choose the default investments in their 401(k). If a target-date fund incorporates private equity or cryptocurrency without the worker fully grasping the fee structure or volatility, a market correction could severely impact their retirement timeline.

Comparing Your Options

To help visualize how the current landscape might apply to your specific situation, review how standard workplace accounts compare to the incoming federally matched options.

| Feature | Traditional Workplace 401(k) | Incoming Federal Accounts (TrumpIRA.gov) |

|---|---|---|

| Eligibility | Must be offered by your employer. | Open to freelancers, self-employed, and those without workplace plans. |

| 2026 Contribution Limit | $24,500 (plus catch-ups if 50 or older). | Tied to standard IRA limits (typically lower than 401(k) limits). |

| Matching Funds | Varies entirely by employer generosity. | Up to $1,000 federal match on a $2,000 contribution, strictly income-dependent. |

| Investment Choices | Chosen by the plan administrator; now potentially including alternative assets. | Standard private-sector IRA options (stocks, bonds, ETFs) curated for low fees. |

| Tax Treatment | Pre-tax or Roth options available. | Subject to standard IRA taxation rules upon withdrawal. |

Avoiding Common Errors With Your Retirement Plan

The introduction of new investment vehicles and tax incentives often leads to confusion. Avoid these frequent missteps as you adjust your strategy.

First, never abandon a guaranteed employer match in favor of a government-backed IRA. If your company matches your 401(k) contributions up to 5 percent of your salary, that represents free money without the strict income phase-outs of the federal Saver’s Match. Always capture your employer’s full match before directing dollars elsewhere.

Second, scrutinize the fee disclosures on any new alternative asset funds offered in your 401(k). You can use resources from the Employee Benefits Security Administration (EBSA) to understand your rights regarding fee transparency. While a private credit fund might advertise an 8 percent return, a 2 percent management fee severely dampens the actual growth of your portfolio over two decades. Compare the net returns against a standard, low-cost S&P 500 index fund before allocating a portion of your paycheck.

Finally, do not confuse the launch dates of these programs. While the new alternative asset safe harbors actively influence 401(k) administrators now, the actual Saver’s Match and the TrumpIRA.gov portal launch in 2027. You must plan your current cash flow according to the 2026 tax code, relying on the existing IRA contribution frameworks maintained by the IRS.

When DIY Isn’t Enough

Managing a straightforward portfolio of index funds serves as a reasonable do-it-yourself task for many savers. However, the introduction of alternative assets and new account structures complicates the picture. Seek out a fiduciary financial advisor if you encounter the following scenarios:

- You run a small business or freelance full-time: Structuring a Solo 401(k) or determining whether you qualify for the federal Saver’s Match requires precise income management. A tax professional can optimize your deductions to ensure you hit the exact Modified Adjusted Gross Income (MAGI) targets.

- Your 401(k) introduces complex private equity funds: Assessing the liquidity constraints and fee structures of alternative investments proves notoriously difficult. An advisor evaluates whether these assets genuinely fit your risk tolerance and time horizon.

- You are coordinating multiple retirement incomes: Balancing an employer 401(k), an IRA, and Social Security benefits requires strategic drawdown planning. You can verify current benefit rules directly at SSA.gov, but an expert minimizes your lifetime tax burden.

The evolving retirement landscape offers powerful new tools to accelerate your savings, provided you understand the mechanics. Take a careful look at your current income trajectory, verify your workplace plan’s newest investment options, and position yourself to capture every matching dollar available to you. By staying informed, you transform policy changes from a source of confusion into a structured advantage for your financial future.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.