How the 2026 Benefit Math Actually Works

Understanding exactly how much you can expect to receive requires looking at current Social Security limits and the timing of your claim. In 2026, a 2.8% Cost-of-Living Adjustment (COLA) increased base benefits across the board. The absolute maximum you can receive as a divorced spouse is 50% of your ex-spouse’s Primary Insurance Amount (PIA)—which is the benefit they are entitled to collect at their Full Retirement Age (FRA).

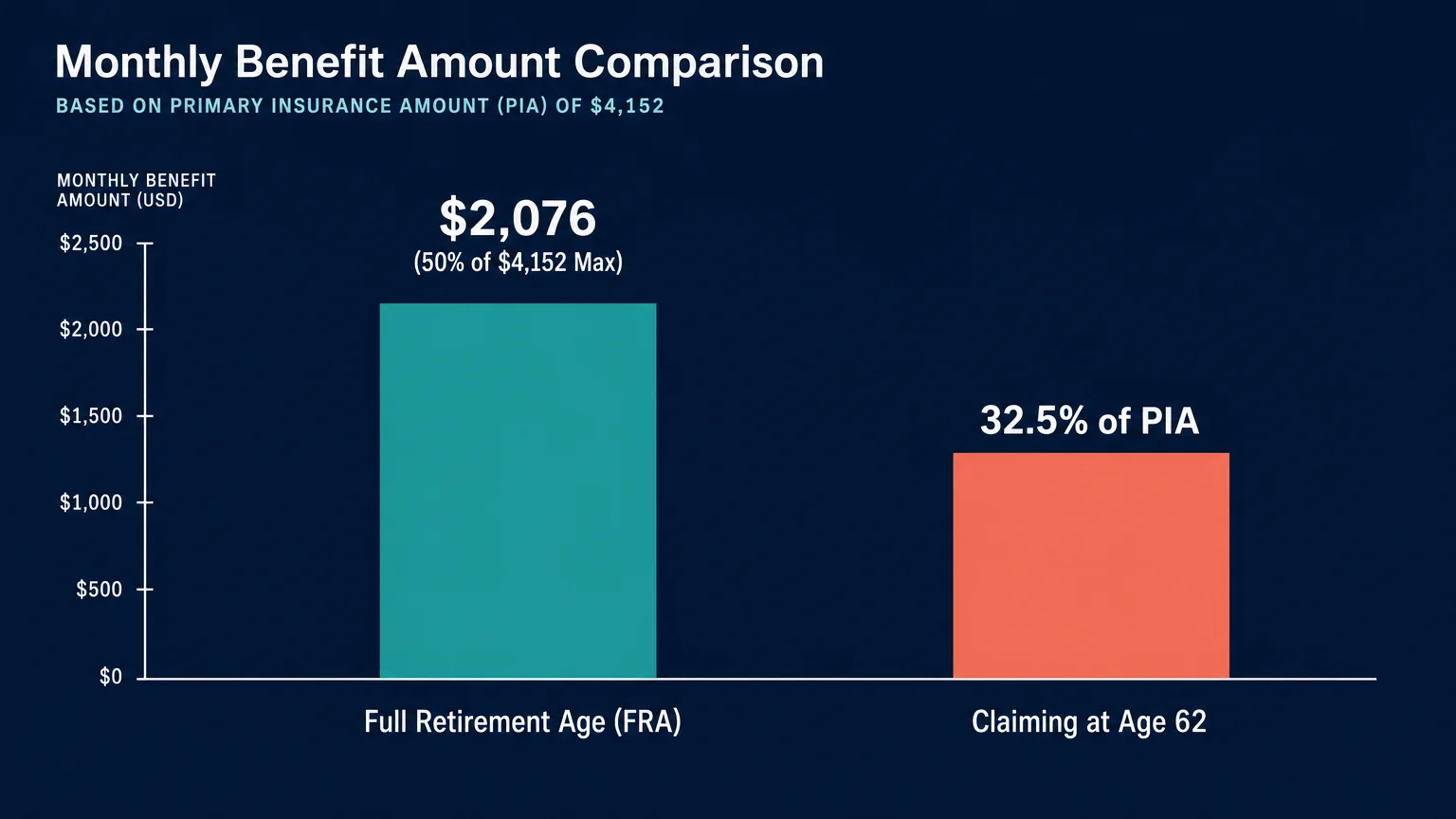

For perspective, the maximum Social Security benefit payable to a worker at Full Retirement Age in 2026 is $4,152 per month. Therefore, the maximum possible divorced spousal benefit this year sits at $2,076 per month. However, the average retired worker currently receives closer to $2,081 per month, meaning the average spousal benefit will likely hover around $1,040 monthly.

Timing your claim dictates the percentage of that maximum you actually take home. If you file at age 62, the Social Security Administration permanently reduces your spousal benefit. Instead of the full 50% of your ex-spouse’s PIA, you will receive approximately 32.5% of their base amount. To receive the maximum 50%, you must wait until your own Full Retirement Age—which is 67 for anyone born in 1960 or later.

Unlike benefits claimed on your own work record, delayed retirement credits do not apply to spousal benefits. While your ex-spouse can increase their own benefit by 8% per year by delaying their claim up to age 70, your spousal benefit maxes out at your Full Retirement Age. There is zero financial incentive for you to wait past your FRA to claim a divorced spouse benefit.