Taxation and Medicare Implications

Claiming a divorced spouse benefit increases your overall household income, which triggers secondary financial effects. Chief among these is the taxation of your Social Security benefits. The IRS determines the taxability of your benefits based on your “provisional income,” calculated by adding half of your annual Social Security benefits to your adjusted gross income and any non-taxable interest.

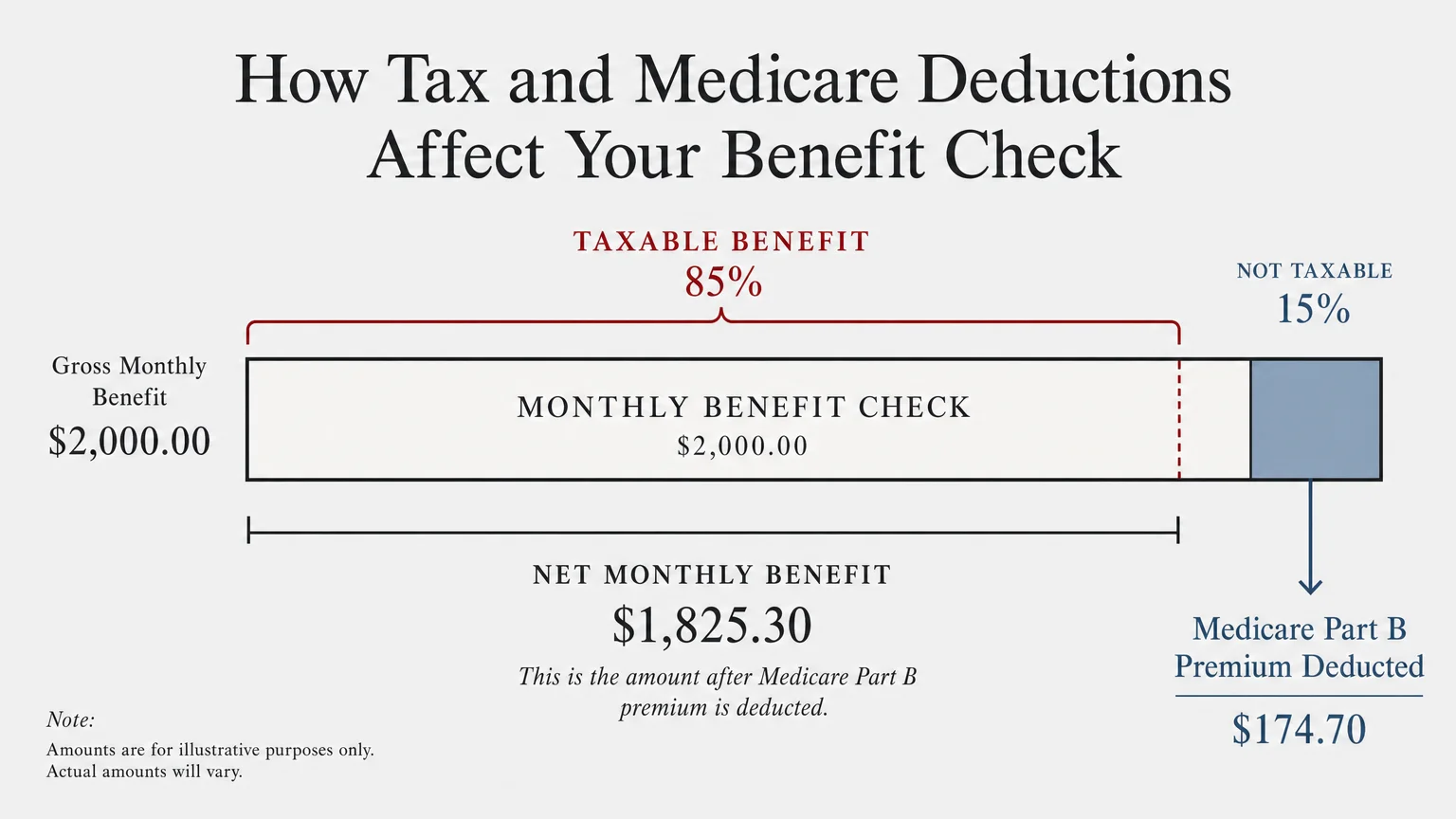

If you file your taxes as a single individual and your provisional income falls between $25,000 and $34,000, up to 50% of your benefits may be taxable. If your provisional income exceeds $34,000, up to 85% of your benefits become subject to federal income tax. Proper withdrawal strategies from your standard retirement accounts can help mitigate this tax burden.

Higher income also affects your healthcare costs. For those enrolled in Medicare, an increase in your adjusted gross income could trigger an Income-Related Monthly Adjustment Amount (IRMAA). For 2026, the standard Medicare Part B base premium is $201.96; exceeding specific income thresholds will force you to pay surcharges on both your Part B and Part D premiums. Review current thresholds at Medicare.gov when projecting your net retirement income.