Retiring to the American South looks like a financial slam dunk when you only review state income tax rates and average winter temperatures. Unfortunately, the glossy brochures leave out the soaring property insurance premiums, strained medical infrastructure, and hidden cost-of-living traps that turn many dream relocations into costly regrets. Before you pack up and trade the snow for humidity, you need a realistic look at what it actually costs to live in the most popular Sunbelt retirement destinations today. By digging into current 2026 data on housing markets, insurance realities, and healthcare access, you can avoid the costly mistake of moving to a town that looks perfect on paper but drains your retirement savings in reality.

The Sunbelt Trap: When Tax Savings Hide the Real Costs

State tourism boards spend millions convincing you that relocating South guarantees a low-stress, low-cost retirement. They loudly advertise the lack of state income taxes and the abundance of golf courses. However, state governments must fund their roads, schools, and emergency services somehow. If a state does not tax your income, it will inevitably tax your property, your purchases, or your vehicle registrations.

Furthermore, the physical environment in the South requires specialized, expensive maintenance. Extreme heat, relentless humidity, and severe weather patterns drastically increase your home upkeep costs. When you factor in the skyrocketing costs of coastal property insurance and the uneven quality of rural healthcare, the “cheap” Southern retirement often proves to be an expensive illusion. To protect your nest egg, you must look beyond the initial home purchase price and calculate your true month-to-month carrying costs.

1. Naples and the Southwest Florida Coast

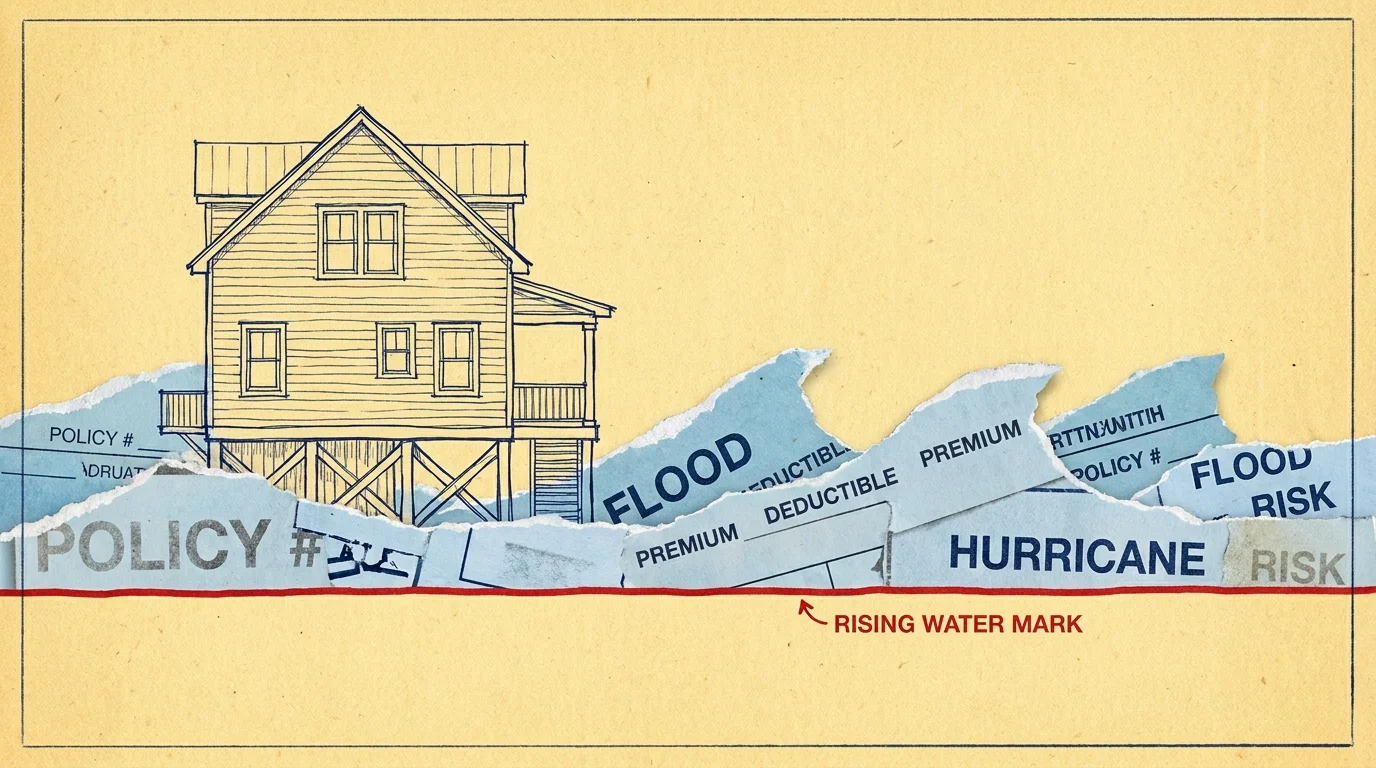

Naples boasts world-class dining, stunning Gulf Coast sunsets, and the financial perk of zero state income tax. On paper, it looks like a financial paradise for affluent retirees. However, the reality of living on the Southwest Florida coast involves navigating a severely stressed property insurance market.

While recent 2026 legislative reforms have finally begun stabilizing rates statewide to an average of roughly $3,800, coastal regions tell a much different story. If you buy a home near the water in Collier County, you can expect annual insurance premiums ranging from $6,500 to over $10,000. Standard homeowners policies in Florida do not cover flood damage from storm surges or heavy rainfall. That requires a separate policy through the National Flood Insurance Program or a private carrier. Once you combine your mortgage, soaring property taxes on newly reassessed homes, luxury HOA fees, and massive windstorm deductibles, your tax savings vanish instantly.

2. Asheville, North Carolina

Tucked into the beautiful Blue Ridge Mountains, Asheville has long been marketed as a quirky, artsy haven with four mild seasons. Many retirees flocked here to escape the severe heat and humidity of the Deep South. The reality is that Asheville is currently experiencing a severe cost-of-living crisis driven by limited space and high demand.

Housing costs in Asheville currently sit 13% higher than the national average, with median home prices exceeding $600,000 in early 2026. The region’s mountainous topography strictly limits new construction, keeping inventory painfully low and prices artificially high. Furthermore, local healthcare costs run about 15% above the national average. If you factor in the recent infrastructure vulnerabilities exposed by late-2024 flooding events, Asheville’s appeal as an insulated “climate haven” requires serious reconsideration. You will pay a massive premium for the mountain views, and you may find yourself navigating congested, winding roads just to reach basic amenities.

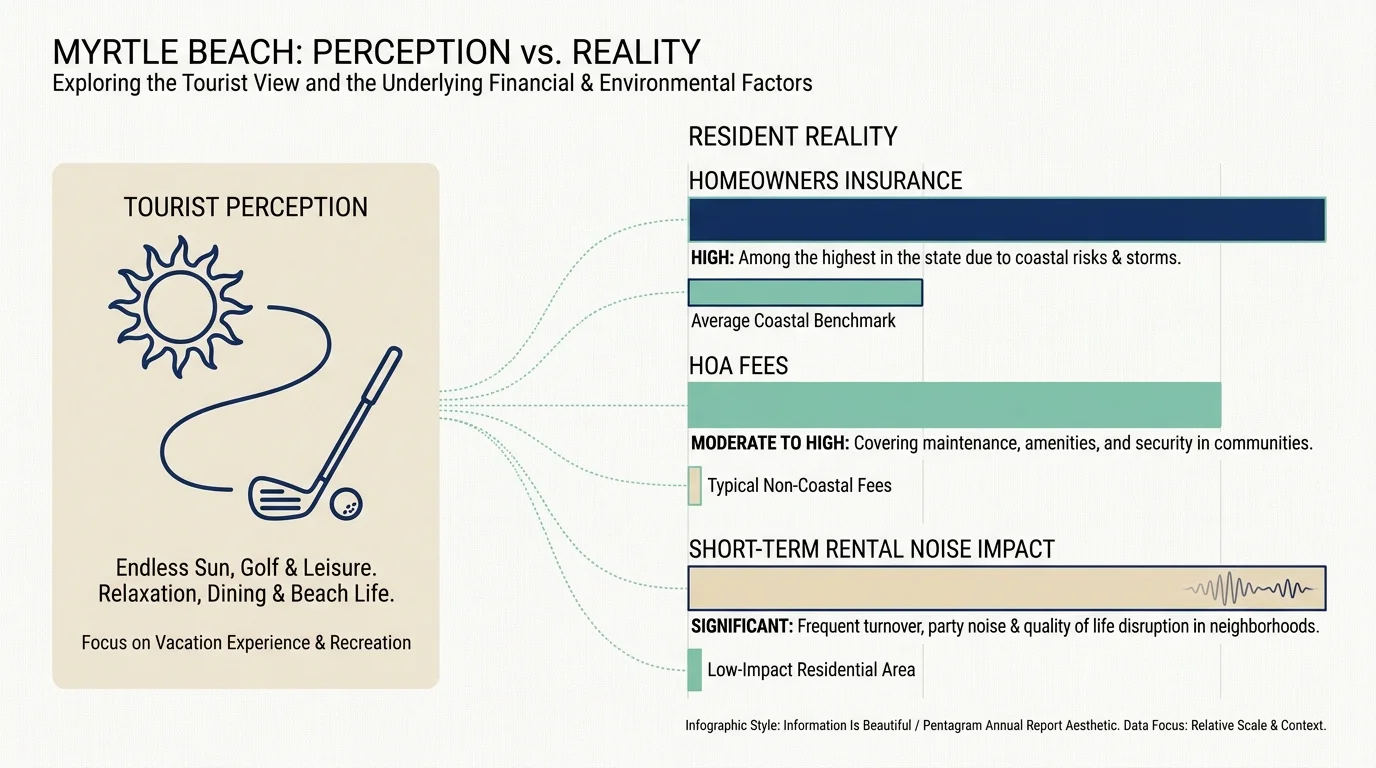

3. Myrtle Beach, South Carolina

Myrtle Beach frequently tops lists of the most affordable beach towns in America. Property taxes in South Carolina are quite low, and the sheer volume of accessible golf courses is staggering. But relocating to a massive, highly commercialized tourist hub comes with significant daily downsides.

During peak summer months, the local population swells, turning quick trips to the grocery store into frustrating traffic nightmares. Beyond the seasonal congestion, Myrtle Beach struggles with stubbornly high property crime rates. According to NeighborhoodScout data, residents face a 1 in 17 chance of becoming a victim of property crime. Furthermore, while routine medical care is accessible, the massive influx of summer visitors routinely strains local emergency rooms and urgent care centers. If you value year-round peace, quiet, and rapid access to specialized medical facilities, a heavily trafficked resort town may leave you highly frustrated.

4. Bella Vista and the Arkansas Ozarks

Bella Vista was quite literally designed as a retirement resort. Situated in the scenic Ozark Mountains, it offers stunning lakes, nature trails, and an incredibly low cost of living. Your retirement dollars stretch exceptionally far in Northwest Arkansas. The fundamental flaw with deeply rural Southern retirement towns, however, is healthcare infrastructure.

“Healthcare is the biggest wild card in retirement.” — Jean Chatzky, Financial Expert

As you age, proximity to high-quality, specialized medical care becomes your most critical asset. Consistently, national evaluations like the 2026 Senior Report by America’s Health Rankings place Arkansas in the bottom tier for clinical care and overall health outcomes. While you might save hundreds of thousands of dollars on a beautiful lakefront property, you may find yourself driving hours to reach top-tier cardiologists, neurologists, or oncology specialists. A cheap cost of living loses its appeal quickly if you cannot access the medical care you need.

5. Gulf Shores, Alabama

Alabama exempts Social Security benefits from state income taxes and features some of the lowest property tax rates in the nation. Gulf Shores, with its white-sand beaches, looks like a perfect, budget-friendly alternative to the crowded Florida coast. The major catch involves severe weather exposure and hidden daily costs.

Just like Florida, Alabama’s Gulf Coast faces an insurance crisis driven by hurricane risks. Premiums are climbing rapidly as regional carriers limit their exposure to windstorms. Additionally, Alabama is one of the few states that still taxes groceries at the local level. While the state reduced its portion of the grocery tax in recent years, county and city taxes can still push the sales tax on your basic food items near 10% in some municipalities. Over a twenty-year retirement, these daily taxes quietly erode the savings you initially gained from the state’s low property taxes.

The True Cost of Southern Relocation

When planning a cross-country move, you must look beyond the initial purchase price of a home. Relocation requires a holistic view of your monthly cash flow. Evaluate the trifecta of Southern living costs: taxes, insurance, and healthcare quality. Below is a realistic look at how these factors interact across popular Southern destinations in 2026.

| Destination | Primary Financial Draw | The Major “But…” | 2026 Reality Check |

|---|---|---|---|

| Naples, FL | No state income tax | Exploding homeowners insurance | Coastal average premiums routinely exceed $6,500/year |

| Asheville, NC | Moderate mountain climate | Severe housing shortages & costs | Housing costs sit 13% above the national average |

| Myrtle Beach, SC | Cheap property taxes | Strained infrastructure & crime | 1 in 17 chance of experiencing property crime |

| Bella Vista, AR | Extremely low cost of living | Poor healthcare access | State ranks in the bottom tier for clinical care |

| Gulf Shores, AL | Social Security tax exemption | High local sales/grocery taxes | Local taxes can push grocery sales tax near 10% |

Professional vs. Self-Guided Relocation Planning

Moving across the country in retirement is a major financial transaction that touches your taxes, your investments, and your estate plan. Deciding whether to handle the logistics yourself or hire professionals depends entirely on the complexity of your financial situation.

“Risk comes from not knowing what you’re doing.” — Warren Buffett, Investor

- When to plan it yourself: If you are simply selling your primary residence, moving to a state where you already have a strong support network, and renting a modest apartment for the first year, a self-guided approach works well. You have time to learn the area without tying up massive amounts of capital.

- When to hire a Certified Financial Planner (CFP): If your retirement income relies heavily on taxable brokerage accounts, rental properties, and pensions, moving across state lines triggers complex tax consequences. A professional can help you navigate domicile laws to ensure you actually qualify for the tax benefits of your new state.

- When to hire a specialized real estate agent: If you are buying property in a coastal or mountainous region, you need an agent who understands hyper-local zoning laws, flood plain maps, and wind-mitigation requirements. A standard home inspection is not enough; you need experts who know how to identify structural risks specific to the Southern climate.

Common Mistakes to Avoid When Moving South

Even meticulous planners can fall into predictable traps when relocating to the Sunbelt. Protect your retirement timeline by avoiding these frequent missteps.

- Buying before renting: It takes a full calendar year to understand a town’s true character. You need to experience the peak summer heat, the tourist traffic, and the off-season closures before committing hundreds of thousands of dollars to a mortgage. Rent a property for twelve months to ensure the reality matches the brochure.

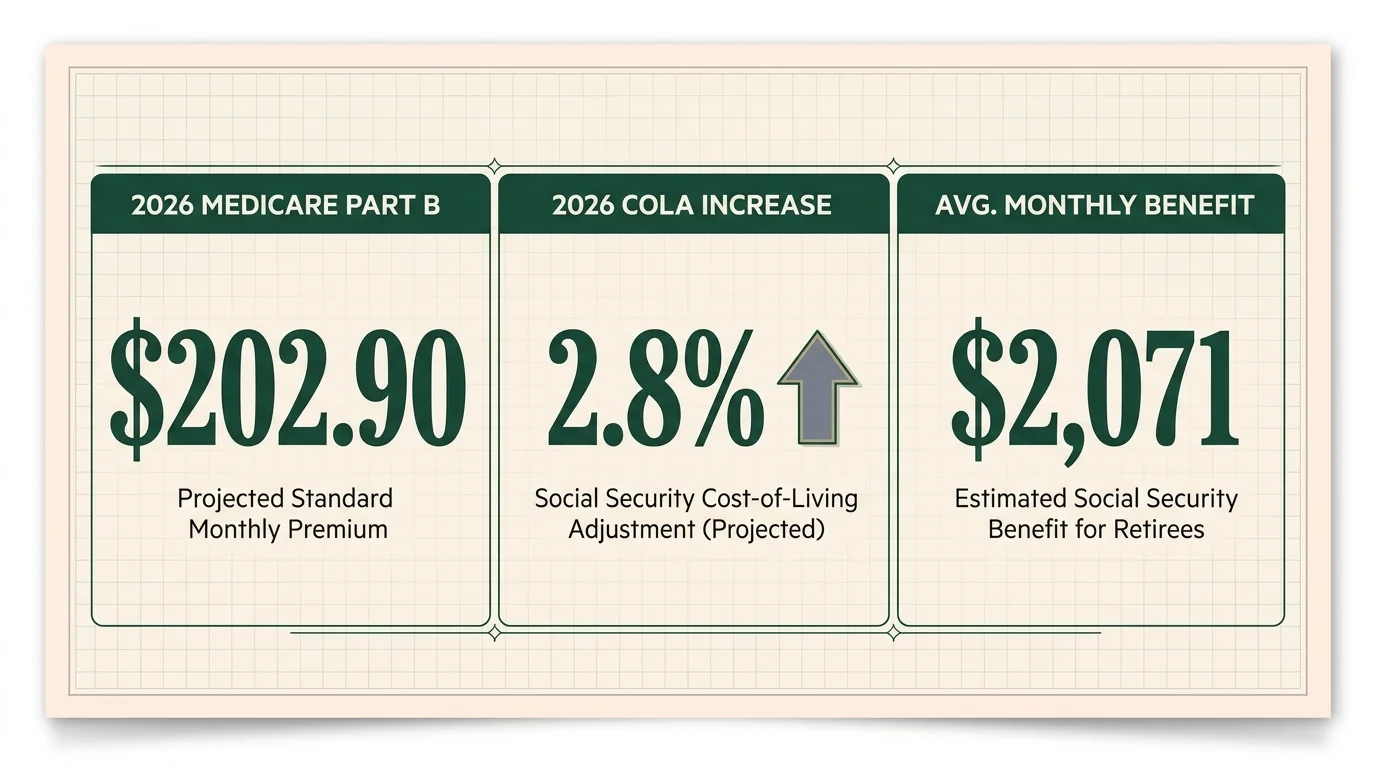

- Ignoring localized Medicare networks: The federal government manages standard Medicare, but private companies manage Medicare Advantage plans. For 2026, the standard Medicare Part B premium is $202.90. If you rely on a localized Medicare Advantage plan, moving out of state might mean losing your preferred doctor network entirely. Always verify coverage at Medicare.gov before finalizing a move.

- Forgetting the “Sunshine Tax”: Warm weather requires constant maintenance. You must budget for continuous air conditioning, professional pest control, pool maintenance, lawn care that grows year-round, and higher depreciation on vehicles due to intense sun and salt air.

- Misunderstanding Social Security taxes: While your new state may not tax your benefits, the federal government still might. Furthermore, your benefits must keep pace with local inflation. The 2026 Social Security Cost-of-Living Adjustment (COLA) is 2.8%, which raises the average monthly benefit to roughly $2,071. Ensure your new town’s cost of living aligns with your projected income at SSA.gov.

Frequently Asked Questions

What is the 2026 Medicare Part B premium?

In 2026, the standard Medicare Part B monthly premium is $202.90. Keep in mind that high earners may pay more due to Income-Related Monthly Adjustment Amounts (IRMAA). You can review current brackets via the official Medicare website.

How much did Social Security increase in 2026?

The Social Security Cost-of-Living Adjustment (COLA) for 2026 is 2.8%. This adjustment brings the average retired worker’s monthly benefit up by about $56, reaching approximately $2,071 per month.

Why is Florida homeowners insurance so high right now?

Florida property owners face a “perfect storm” of insurance challenges. The state deals with severe hurricane risks, coastal flooding vulnerability, and historically high rates of property insurance litigation. While recent legal reforms are helping to stabilize the market, many major carriers have already limited their exposure in the state, driving up costs for the remaining policies.

A Quick Word Before You Pack

Relocating to the South can still provide a wonderful, fulfilling retirement experience, provided you enter the process with your eyes wide open. Do not let the allure of mild winters blind you to the realities of insurance premiums, healthcare access, and hidden taxes. Take your time, rent before you buy, and build a localized budget that accounts for the unique challenges of Sunbelt living.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.