How Your Medicare Premiums Intersect With Your Raise

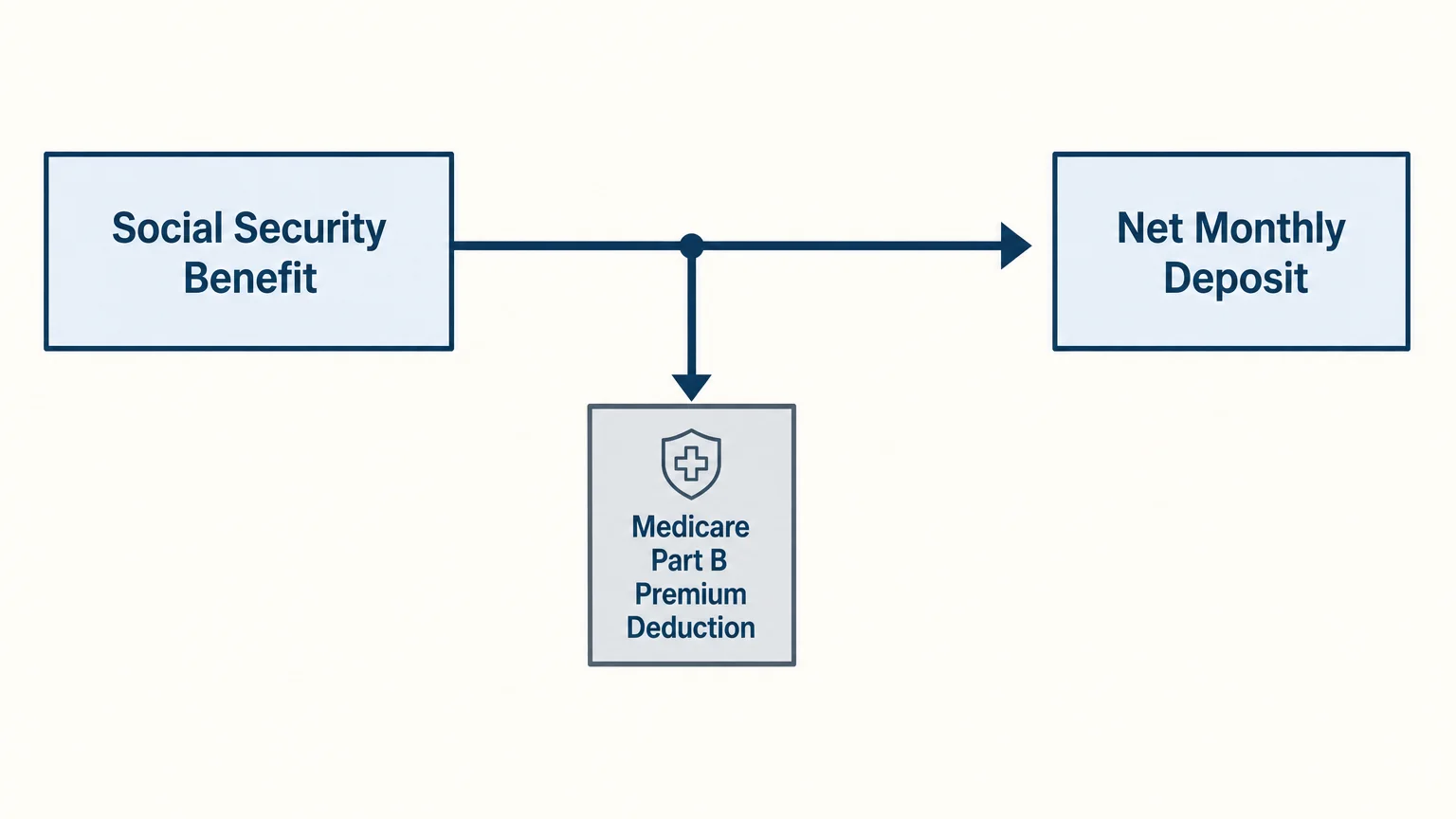

For the vast majority of retirees, Social Security benefits and Medicare Part B premiums are permanently linked. When you enroll in Medicare Part B, the federal government automatically deducts your monthly premium from your Social Security check before the funds ever reach your bank account. Because of this structural connection, any increase in your Social Security benefit must outpace the annual increase in Medicare premiums for you to feel a positive difference in your budget.

In 2026, the standard Medicare Part B premium is $202.90 per month, which represented a nearly $18 increase from the 2025 premium of $185.00. Healthcare inflation traditionally runs higher than general consumer inflation. If the Centers for Medicare and Medicaid Services (CMS) announces another significant premium hike for 2027, that increase will consume a portion—or in some rare cases, the entirety—of your COLA. For instance, if your COLA provides an extra $50 a month, but your Medicare Part B premium rises by $20 a month, your net increase drops to $30.

Fortunately, federal law provides a safety net known as the “hold harmless” provision. This rule guarantees that your Medicare Part B premium increase cannot exceed the dollar amount of your Social Security cost-of-living adjustment.

If you receive a very small Social Security benefit, the hold harmless provision prevents a rising Medicare premium from actually reducing your net monthly check. Your benefit will simply remain flat. However, you do not qualify for hold harmless protection if you are a new Medicare enrollee, if you pay your premiums directly rather than having them deducted from Social Security, or if you are subject to high-income surcharges.

Those high-income surcharges—officially called the Income-Related Monthly Adjustment Amount (IRMAA)—add another layer of complexity. Medicare uses a two-year lookback period to determine your premium.

Therefore, your 2027 Medicare Part B and Part D premiums will be based on the Modified Adjusted Gross Income (MAGI) you report on your 2025 tax return. If selling a home, executing large Roth conversions, or taking substantial required minimum distributions pushed your income into a higher tier in 2025, you will pay significantly more for Medicare in 2027, regardless of your Social Security COLA.