Your Social Security benefits are a lifeline in retirement, but the rules and financial realities surrounding them are shifting rapidly. With sweeping changes to Medicare premiums, evolving tax laws, and crucial trust fund deadlines approaching, you need to understand exactly how these shifts will impact your monthly income. Recent reports confirm that the 2026 Cost-of-Living Adjustment (COLA), rising healthcare deductibles, and new legislative tax breaks for seniors are fundamentally altering how you should plan your finances. By staying ahead of these five critical Social Security trends, you can protect your hard-earned benefits, avoid hidden tax traps, and make confident, informed decisions for your retirement years.

Trend 1: The Cost-of-Living Adjustment (COLA) Reality Check

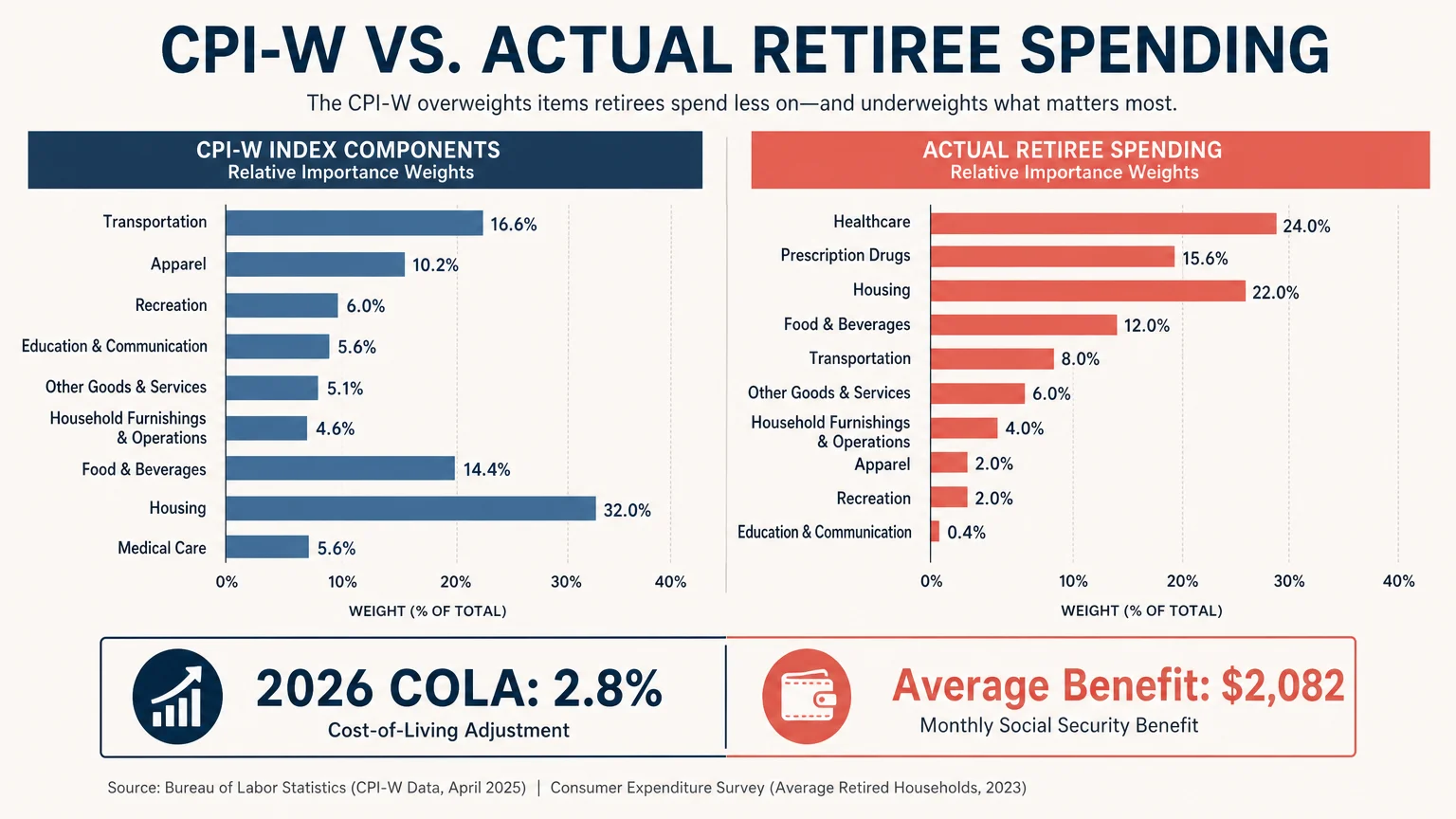

The Social Security Administration approved a 2.8% Cost-of-Living Adjustment for 2026. This moderate adjustment brings the average retired worker’s monthly benefit to approximately $2,082. While a bump in pay is always welcome, many retirees find that the official formula does not capture their actual living expenses.

Social Security calculates your COLA using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index measures the spending habits of working-age Americans, weighing transportation and apparel heavily. Retirees, however, spend a vastly larger portion of their budgets on healthcare, prescription drugs, and housing. Consequently, even when you receive an annual raise, your purchasing power may slowly erode. To counteract this trend, you must build inflation-resistant income streams—such as dividend-paying index funds or Treasury Inflation-Protected Securities—into your broader retirement portfolio.

Trend 2: Medicare Premium Creep Eating Into Benefits

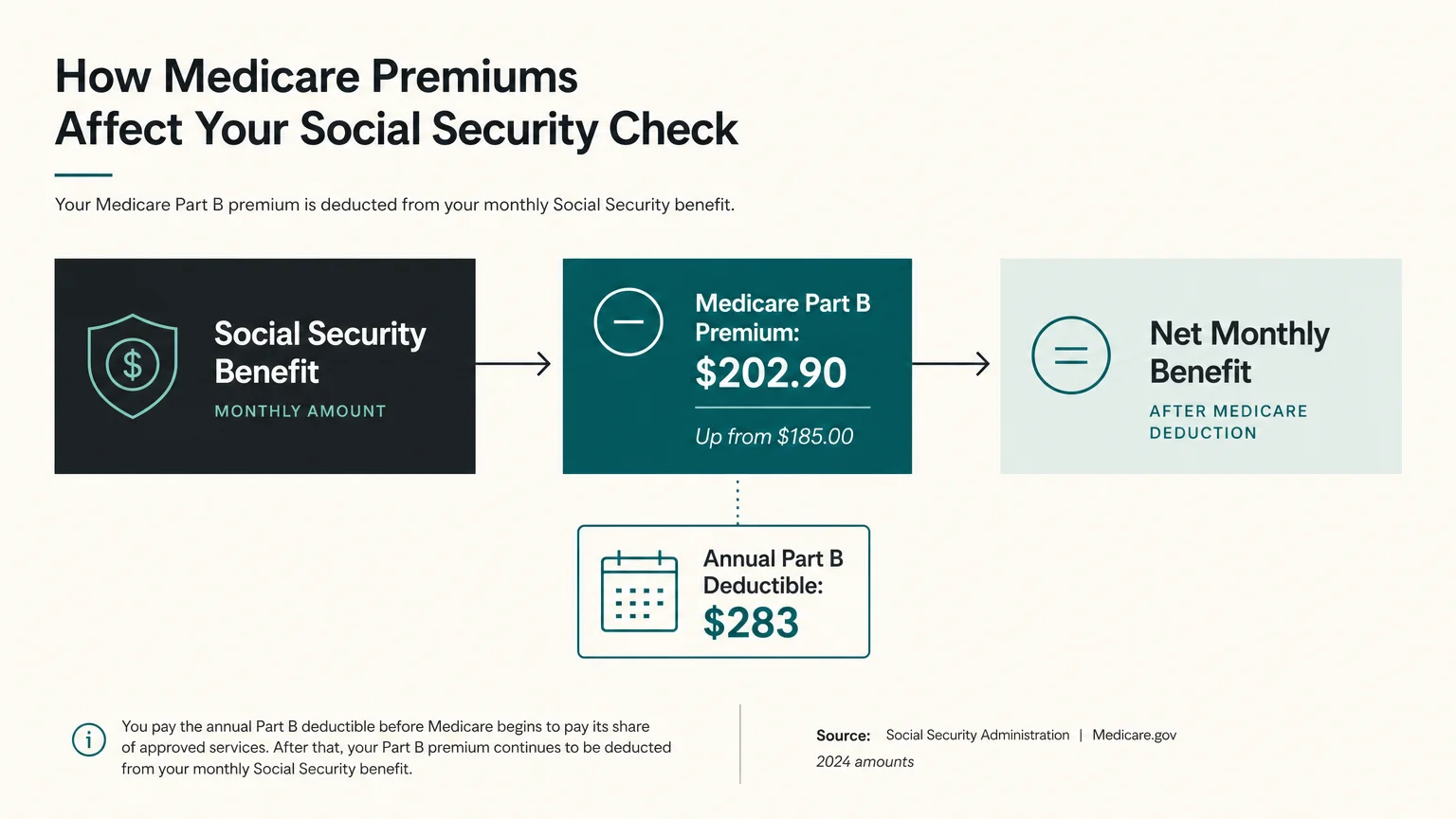

Your Social Security check and your Medicare costs are inextricably linked, and healthcare expenses are consuming a larger piece of the pie. Most retirees have their Medicare Part B premiums deducted directly from their Social Security payments before the money ever hits their bank accounts.

In 2026, the standard Medicare Part B premium increased significantly to $202.90 per month, up from $185.00 the previous year. Simultaneously, the annual Part B deductible rose to $283. If your Social Security benefit goes up by $50 due to COLA, but your Medicare premium jumps by $17.90, your net increase shrinks considerably.

Higher-income retirees face an even steeper climb due to the Income-Related Monthly Adjustment Amount (IRMAA). If your modified adjusted gross income from two years prior exceeds designated brackets, the government tacks a surcharge onto your standard premium. Monitoring your income carefully—especially when making large retirement account withdrawals or executing Roth conversions—is critical to preventing premium spikes.

Trend 3: The Approaching 2032 Trust Fund Deadline

Retirees often worry that Social Security is going bankrupt. While the program will not disappear, it does face a genuine mathematical shortfall that will force congressional action. The 2026 Social Security Trustees Report projects that the Old-Age and Survivors Insurance (OASI) Trust Fund will be depleted in 2032.

What happens if lawmakers do absolutely nothing? By law, the program can only pay out what it collects in payroll taxes. Starting in 2032, ongoing tax revenues would only be sufficient to cover 78% of scheduled benefits. This would effectively mean an immediate 22% benefit cut for all retirees.

Historically, Congress waits until the eleventh hour to pass bipartisan fixes, much like they did in 1983. Potential solutions include raising the Full Retirement Age, increasing the payroll tax rate, or adjusting the maximum taxable earnings limit—which currently sits at $184,500 for 2026. Rather than panicking, you should run your long-term financial projections with a conservative buffer, assuming a potential 10% to 20% reduction in future benefits just to be safe.

Trend 4: Shifting Tax Dynamics and the Provisional Income Trap

More retirees than ever are paying federal income tax on their Social Security benefits. The Internal Revenue Service determines the taxability of your benefits using a formula called “provisional income.” You calculate this by adding your adjusted gross income, any non-taxable interest, and 50% of your Social Security benefit.

If your provisional income falls between $25,000 and $34,000 as a single filer, up to 50% of your benefit is taxable. Above $34,000, up to 85% becomes taxable. For married couples filing jointly, the brackets are $32,000 to $44,000 (up to 50% taxed) and anything above $44,000 (up to 85% taxed). Because Congress set these thresholds in the 1980s and never indexed them for inflation, nearly every middle-class retiree now falls into the taxation trap.

“Taxes will be the single biggest factor that separates people who keep their retirement money from those who lose it to the government.” — Ed Slott, CPA and Retirement Tax Expert

Fortunately, the broader tax code offers some relief. For the 2026 tax year, the standard deduction for married couples filing jointly increased to $32,200. Furthermore, seniors aged 65 and older may qualify for an enhanced deduction of $6,000 per person, provided they meet specific income limitations. Strategic tax planning—such as managing traditional IRA distributions alongside tax-free Roth withdrawals—is essential to keeping your provisional income below the taxation thresholds.

Trend 5: Maximizing Benefits Through Delayed Claiming

With longer life expectancies and rising healthcare costs, a distinct trend has emerged: knowledgeable retirees are delaying their claims to maximize guaranteed lifetime income. You can claim benefits as early as age 62, but doing so locks in a permanent reduction of up to 30%. Conversely, if you wait past your Full Retirement Age (FRA)—which is 67 for anyone born in 1960 or later—you earn delayed retirement credits of 8% per year up until age 70.

To illustrate the sheer power of patience, consider a worker whose Full Retirement Age benefit is exactly $2,000 per month. Here is how their age at claiming dictates their lifelong monthly income in 2026:

| Claiming Age | Percentage of Full Benefit | Monthly Payment |

|---|---|---|

| Age 62 (Earliest) | 70% | $1,400 |

| Age 64 | 80% | $1,600 |

| Age 67 (Full Retirement Age) | 100% | $2,000 |

| Age 70 (Maximum) | 124% | $2,480 |

For high earners who consistently paid the maximum Social Security tax over a 35-year career, delaying until age 70 in 2026 unlocks the absolute maximum monthly benefit of $5,181. Waiting also provides a massive advantage for married couples; when one spouse passes away, the surviving spouse inherits the higher of the two benefits. Delaying the primary earner’s claim is the most effective way to protect a widow or widower from poverty later in life.

Pitfalls to Watch For

Even with careful planning, simple administrative mistakes can cost you thousands. Watch out for these common Social Security pitfalls:

- The Earnings Test Penalty: If you claim Social Security before your Full Retirement Age and continue to work, your benefits will be reduced. In 2026, the annual earnings limit is $24,480. The SSA withholds $1 for every $2 you earn above that threshold. This money is not permanently lost—it is added back to your benefit calculation once you reach FRA—but it causes severe cash flow disruptions for the unprepared.

- Assuming Medicare is Automatic at 62: You can claim Social Security at age 62, but Medicare eligibility does not begin until age 65. If you retire early, you must secure private health insurance, which can cost upwards of $1,000 per month, eating away at your early Social Security benefits.

- Failing to Coordinate Spousal Benefits: Married couples often file independently without looking at the broader picture. You must evaluate whether claiming a spousal benefit (up to 50% of the primary earner’s full benefit) yields a higher payout than claiming on your own work record.

Getting Expert Help

Social Security rules are complex, and reversing a bad decision is incredibly difficult once the initial 12-month withdrawal window closes. Consider seeking guidance from a Certified Financial Planner (CFP) or CPA if you fall into any of the following scenarios:

- You own a business or real estate: A tax professional can help you structure your income to avoid triggering IRMAA Medicare surcharges.

- You have a large traditional IRA or 401(k): An advisor can build a withdrawal sequence that minimizes taxes on your Social Security benefits using the provisional income formula.

- You are divorced or widowed: The rules for ex-spousal and survivor benefits are heavily nuanced. An expert can calculate the exact month you should switch from a survivor benefit to your own benefit for maximum payout.

Social Security is the cornerstone of American retirement, but it is not a set-it-and-forget-it program. By understanding how COLA calculations, Medicare premiums, and tax laws intersect, you can optimize your claiming strategy and keep more money in your pocket.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.