The 2027 Social Security cost-of-living adjustment (COLA) announcement is fast approaching this October, and recent inflation data suggests a higher increase than previously expected. While a larger check might sound like a relief, it often arrives as a mixed blessing disguised by the rising costs of healthcare and daily living. Understanding how the upcoming COLA affects your overall retirement strategy allows you to protect your purchasing power before the new rates take effect in January. By examining current inflation trends, Medicare premium adjustments, and tax implications, you can make proactive financial moves today rather than reacting to the news later this fall.

Why the 2027 COLA Projection Is Trending Upward

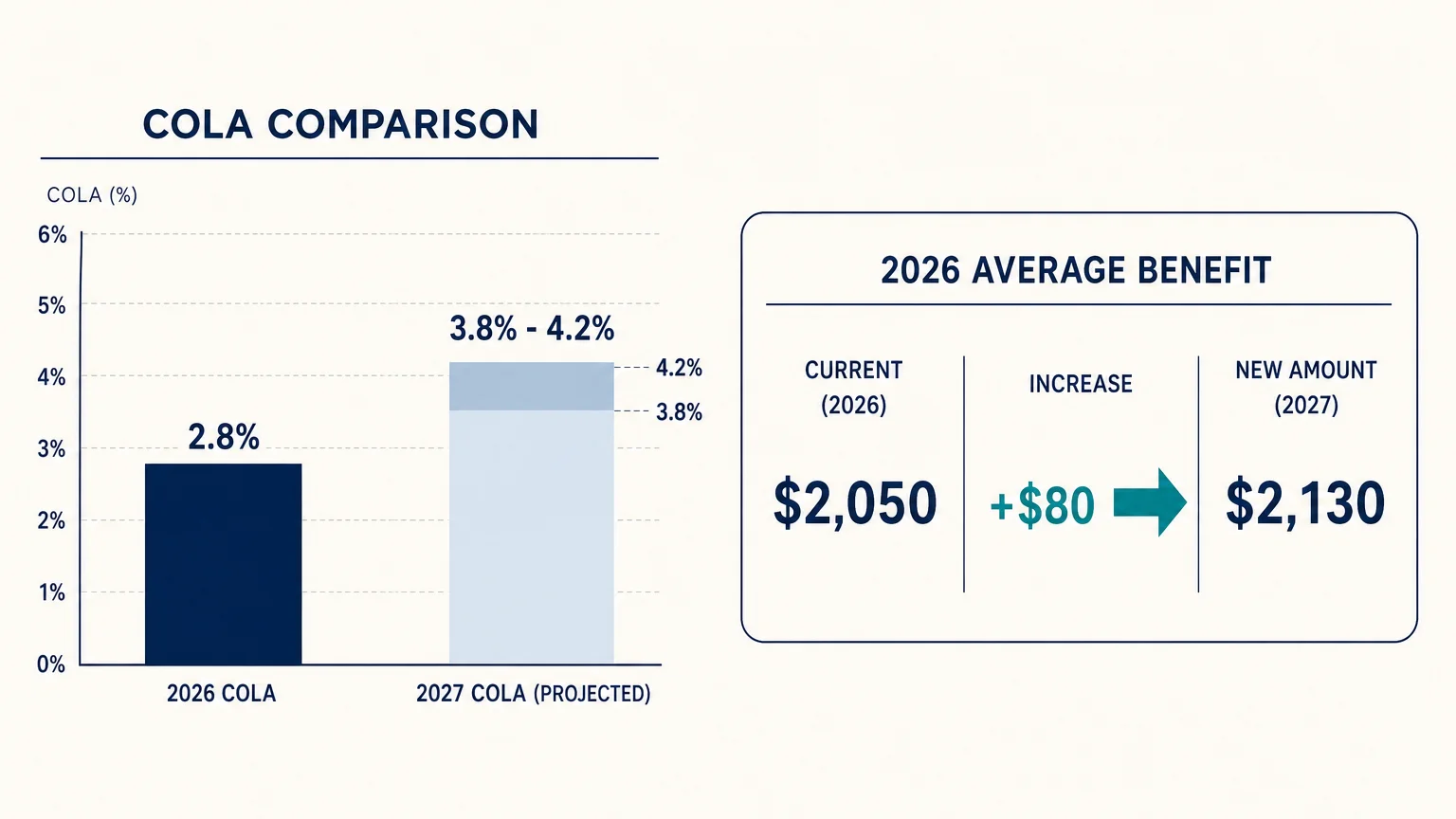

Recent inflation trends have pushed the projected 2027 Social Security COLA higher than the 2.8% adjustment retirees received in 2026. Experts from the Senior Citizens League and independent analysts project the next COLA could land between 3.8% and 4.2%. The Social Security Administration bases its annual adjustment on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) during the third quarter—July, August, and September.

If you currently receive the 2026 average monthly benefit of roughly $2,050, a 3.9% increase would add about $80 to your monthly check. However, a larger payment does not guarantee more financial freedom. The CPI-W measures the spending habits of younger, working-age Americans, placing a heavier weight on transportation and apparel. Seniors typically spend a much larger percentage of their income on healthcare and housing. Consequently, the official COLA rarely matches the actual inflation rate you experience at the pharmacy counter or the grocery store. You must factor in how this extra income interacts with your broader financial plan to avoid unintended consequences.

How Rising Medicare Premiums Consume Your Benefit Changes

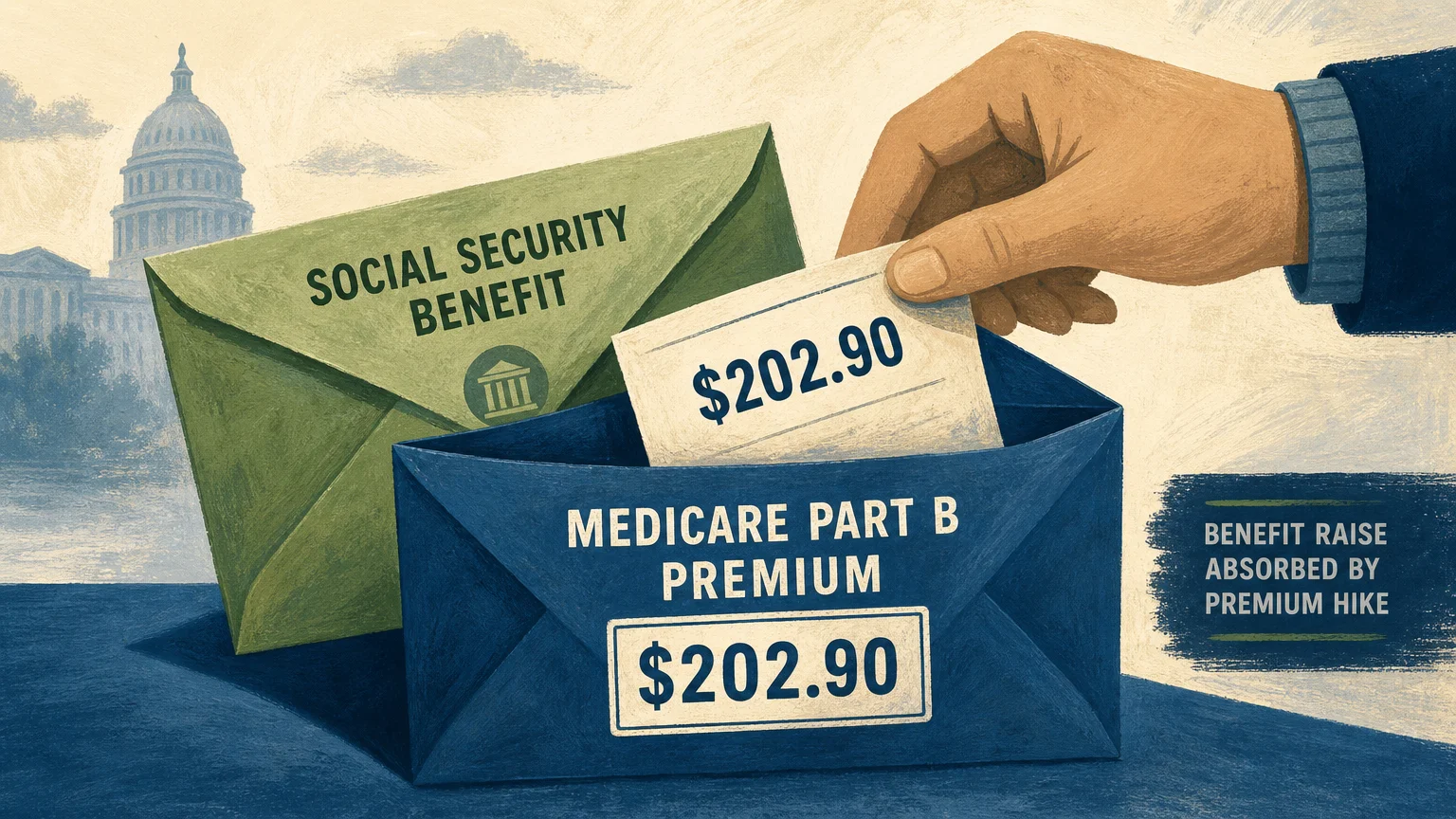

A common frustration among retirees is seeing their retirement benefits update in January, only to find the net increase swallowed by higher healthcare costs. While the Social Security Administration handles your monthly benefit, the Centers for Medicare & Medicaid Services sets your Part B premiums, which are deducted directly from your check.

The standard Medicare Part B premium for 2026 is $202.90 per month, alongside an annual deductible of $283. History shows that when the COLA rises, Medicare premiums often follow suit. A “hold harmless” provision protects most beneficiaries from having their net Social Security check decrease due to Part B premium hikes. However, if the upcoming COLA is substantial, the premium increase will consume a significant portion of your raise before the money ever hits your bank account.

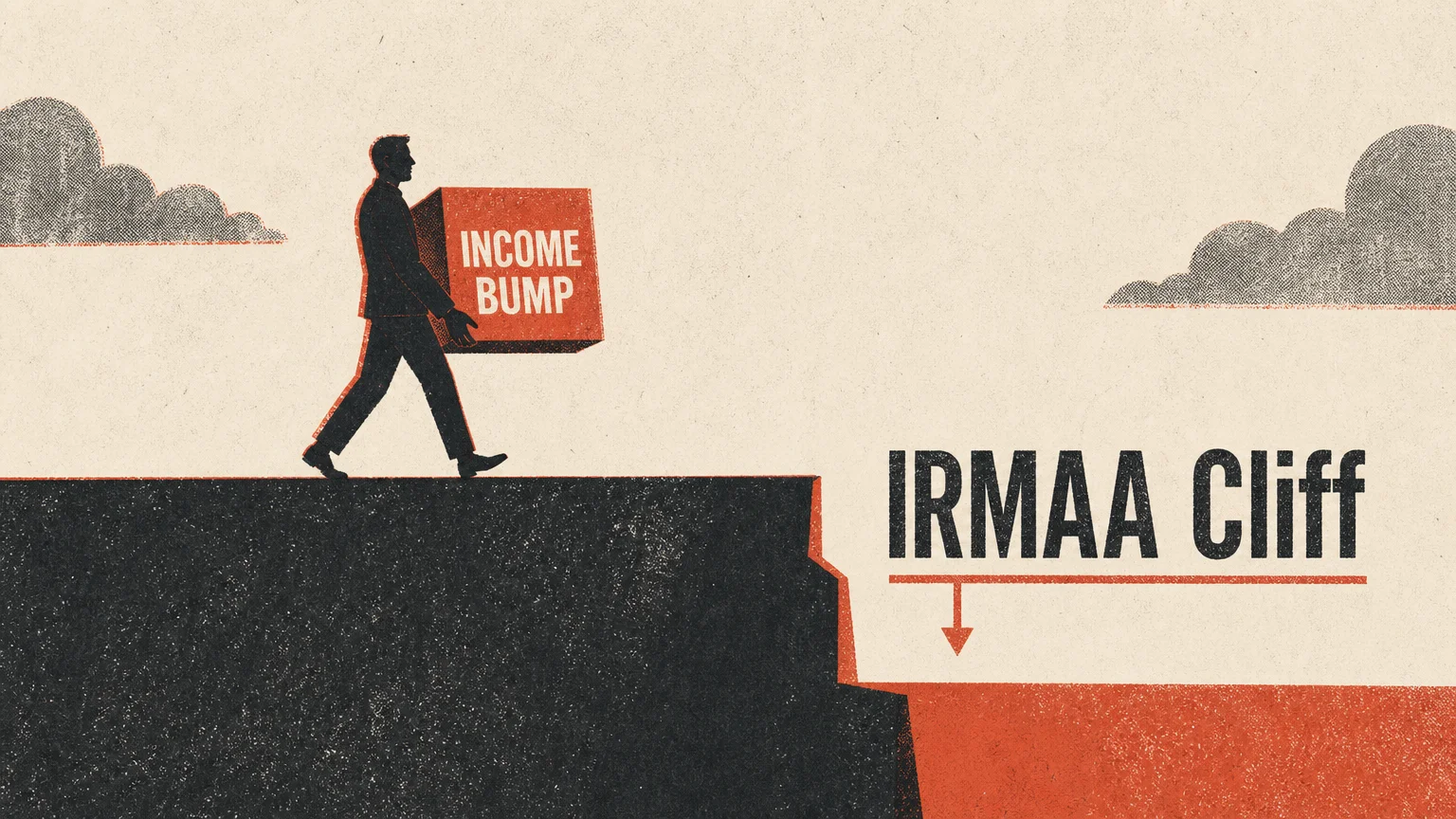

Furthermore, a larger COLA increases your modified adjusted gross income (MAGI). Medicare uses the Income-Related Monthly Adjustment Amount (IRMAA) to determine if you owe a surcharge on your Part B and Part D premiums. Because IRMAA relies on a two-year lookback period, your 2026 premiums are based on your 2024 tax return. A sudden bump in your income can inadvertently push you over the IRMAA cliff in future years, forcing you to pay hundreds of dollars more each month for the exact same health coverage.

Tax Traps to Watch For When Benefits Increase

While a bump in your monthly benefit is welcome, it can aggressively complicate your tax situation. The Internal Revenue Service taxes Social Security benefits based on your “provisional income.” You calculate this figure by adding your adjusted gross income, your non-taxable interest, and exactly half of your annual Social Security benefits.

The thresholds for taxing these benefits have not been adjusted for inflation in decades. As a result, each new COLA announcement pushes more retirees into higher taxation brackets. Depending on your filing status and provisional income, up to 85% of your Social Security benefits could become taxable.

| Filing Status | Up to 50% Taxable | Up to 85% Taxable |

|---|---|---|

| Single, Head of Household, or Qualifying Widow(er) | $25,000 — $34,000 | Over $34,000 |

| Married Filing Jointly | $32,000 — $44,000 | Over $44,000 |

Fortunately, the current tax landscape offers some robust relief mechanisms. For the 2026 tax year, the standard deduction has increased to $16,100 for single filers and $32,200 for married couples filing jointly. Taxpayers aged 65 and older can claim an extra standard deduction of $2,050 (single) or $1,650 (per qualifying married spouse). Furthermore, recent tax updates introduced a temporary senior bonus deduction of $6,000 for singles and $12,000 for married couples filing jointly. Leveraging these expanded deductions is crucial for shielding your adjusted benefit from the IRS.

Practical Steps to Protect Your Purchasing Power

You do not have to sit back and watch taxes and premiums erode your wealth. Take control of your senior planning by implementing these proactive strategies before the official COLA announcement.

- Reassess your tax withholding: If a higher COLA pushes you into a new tax bracket, you can file an updated Form W-4V with the Social Security Administration. You can elect to have 7%, 10%, 12%, or 22% of your benefit withheld for federal taxes. Adjusting this now prevents a massive surprise tax bill next April.

- Track your personal inflation rate: Since the government index measures urban wage earners, it fails to capture your unique reality. Track your specific spending on prescription drugs, utility bills, and property taxes to understand your actual cost of living and adjust your withdrawal strategy accordingly.

- Explore Roth conversions early: Shifting funds from a traditional IRA to a Roth IRA requires paying taxes upfront, but it eliminates your future Required Minimum Distributions (RMDs). Lower RMDs help keep your provisional income below the threshold that triggers taxation on your Social Security benefits.

- File Form SSA-44 for life events: If your income dropped recently due to full retirement, a reduction in work hours, or the loss of a spouse, you can appeal a Medicare IRMAA surcharge. Filing Form SSA-44 alerts the government to your life-changing event and requests an immediate premium reduction.

- Utilize Qualified Charitable Distributions (QCDs): If you are over age 70½ and donate to charity, you can transfer up to $111,000 in 2026 directly from your IRA to an eligible organization. This satisfies your RMD without adding a single dollar to your adjusted gross income.

“Taxes will be the single biggest drain on your retirement savings. You must have a plan to minimize them.” — Ed Slott, CPA and Retirement Tax Expert

Pitfalls to Watch For

Retirement planning requires anticipating how one financial decision triggers a chain reaction across your entire portfolio. Avoid these common missteps when preparing for the upcoming benefit changes.

First, do not assume the COLA equates to real wealth growth. Treat the increase as an inflation buffer rather than a bonus. Increasing your discretionary spending simply because your monthly check went up often leads to cash flow shortages later in the year.

Second, be highly aware of the “Widow’s Penalty.” When a spouse passes away, the surviving spouse loses the smaller of the two Social Security checks but is immediately forced to file taxes as a single individual. Even though their total household income drops, their tax brackets shrink by half. This frequently pushes the surviving spouse into much higher tax rates and triggers steep Medicare IRMAA surcharges just when they are most financially vulnerable.

Finally, never wait until tax season to address your income strategy. If you wait until April to deal with the impact of a January benefit increase, it is already too late to execute strategies like Roth conversions or QCDs for that tax year. Tax planning must happen in the fall.

Getting Expert Help

Navigating the complex intersection of Social Security, Medicare premiums, and tax law is rarely a do-it-yourself endeavor. Working with a fee-only financial planner or a certified public accountant can pay massive dividends over the course of your retirement.

Seek professional guidance if your provisional income is hovering near the $34,000 (single) or $44,000 (married) taxation thresholds. An expert can determine the exact withdrawal sequence from your taxable, tax-deferred, and tax-free accounts to keep you below those limits. You should also consult an advisor if you plan to sell a large asset, such as a home or a business. These massive capital gains trigger severe Medicare IRMAA penalties unless you structure the sale strategically across multiple tax years.

Frequently Asked Questions

When is the official Social Security COLA announced?

The Social Security Administration officially announces the next year’s Cost-of-Living Adjustment in mid-October. The updated benefit amounts take effect for payments issued in January.

Does the COLA apply to my Medicare Part B premiums?

No. The Centers for Medicare & Medicaid Services determines Medicare Part B premiums independently of the Social Security COLA. However, Medicare premiums typically rise each year and are deducted directly from your Social Security benefit, which can offset your net income increase.

Can a higher Social Security payment affect my eligibility for other benefits?

Yes. Federal and state support programs like Medicaid, SNAP, and housing assistance enforce strict income limits. A COLA increase can push your income past these thresholds and reduce or eliminate your eligibility.

You have the tools to prepare for the upcoming COLA before the headlines hit in October. Take a close look at your expected income for the year, evaluate your current tax withholding, and project how a higher benefit might interact with your Medicare premiums. Staying proactive protects your hard-earned retirement savings from creeping taxes and inflation.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.