The latest estimates forecast a 3.8% Social Security cost-of-living adjustment (COLA) for 2027, driven by unexpectedly stubborn inflation. If this projection holds, you will see your monthly payments increase by about $79 on average starting in January. Preparing for this change requires understanding how higher prices impact both your benefits and your broader retirement budget. Because the official announcement does not happen until October, you have a crucial window right now to assess your financial plan. Knowing how the upcoming adjustment interacts with your Medicare premiums, taxes, and daily expenses empowers you to make proactive spending and investing decisions. Rather than waiting for an official notice in the mail, you can take control of your financial future today.

The Numbers Behind the 2027 COLA Forecast

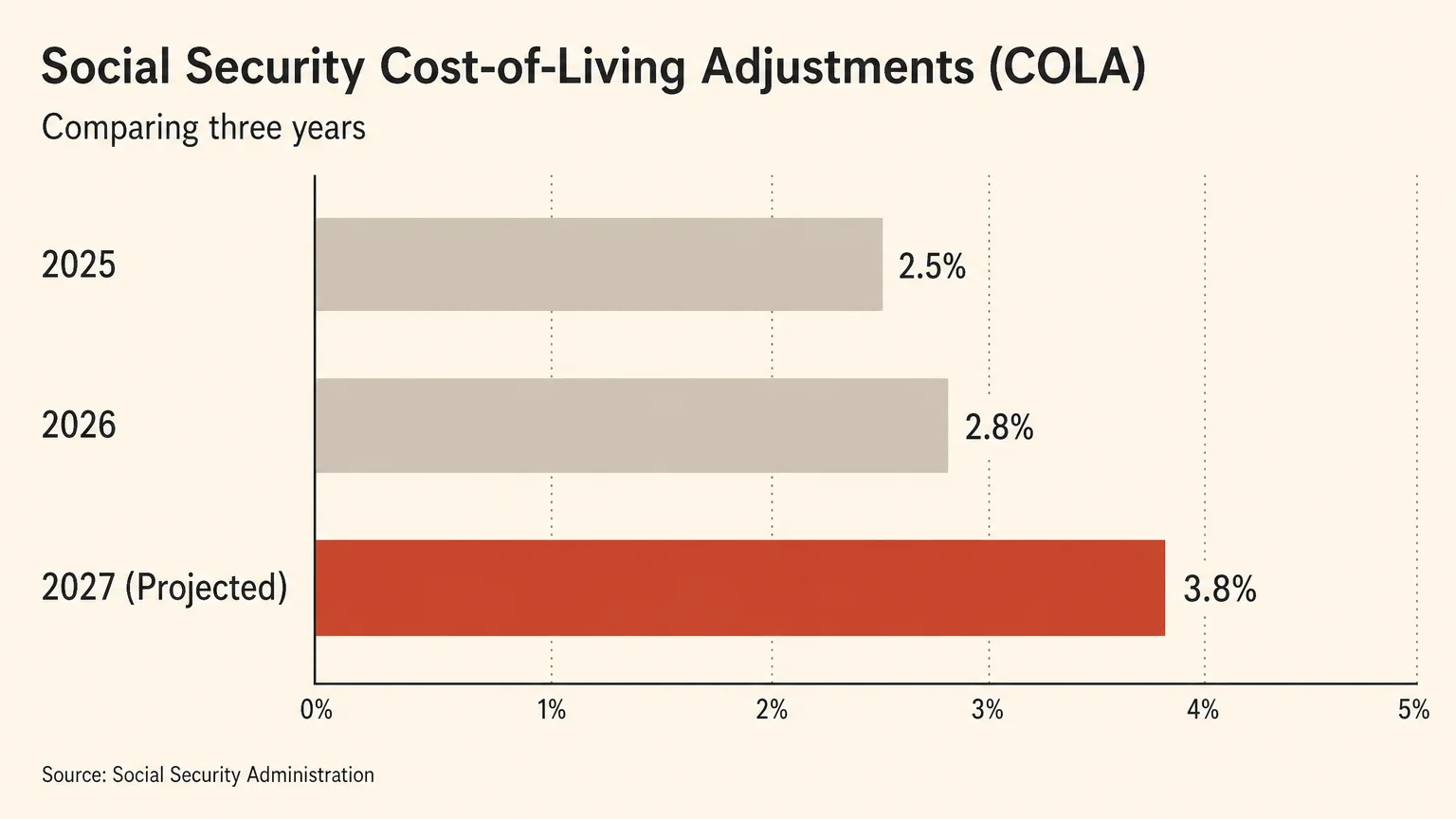

Tracking the upcoming cost-of-living adjustment allows you to forecast your baseline retirement income months before the official declaration. According to June 2026 data from the Senior Citizens League (TSCL)—a prominent nonpartisan senior advocacy group—the 2027 COLA is currently projected at 3.8 percent. This represents a significant upward shift from their earlier estimates of 2.8 percent, largely fueled by recent consumer price index reports showing inflation running hotter than economists anticipated.

To put this projection into perspective, you need to look at the current benefit landscape. According to the Social Security Administration (2026), the average monthly benefit for retired workers reached $2,081.16 in the spring of 2026. A 3.8 percent increase on that average amount translates to a monthly boost of roughly $79.08, or nearly $950 in additional income over the course of the year. If you delay claiming until your full retirement age and qualify for the maximum benefit—which stands at $4,152 per month in 2026—a 3.8 percent adjustment would add over $157 to your monthly check.

This projected rate marks a noticeable increase from the adjustments seen in the past two years. Retirees received a 2.5 percent COLA for 2025 and a 2.8 percent adjustment for 2026. A 3.8 percent bump for 2027 would provide the largest benefit boost in four years. However, an increased gross benefit does not automatically equal a proportionately larger deposit in your bank account. The actual amount you take home depends entirely on your specific deductions, your tax liabilities, and your Medicare enrollment status.

How Your Medicare Premiums Intersect With Your Raise

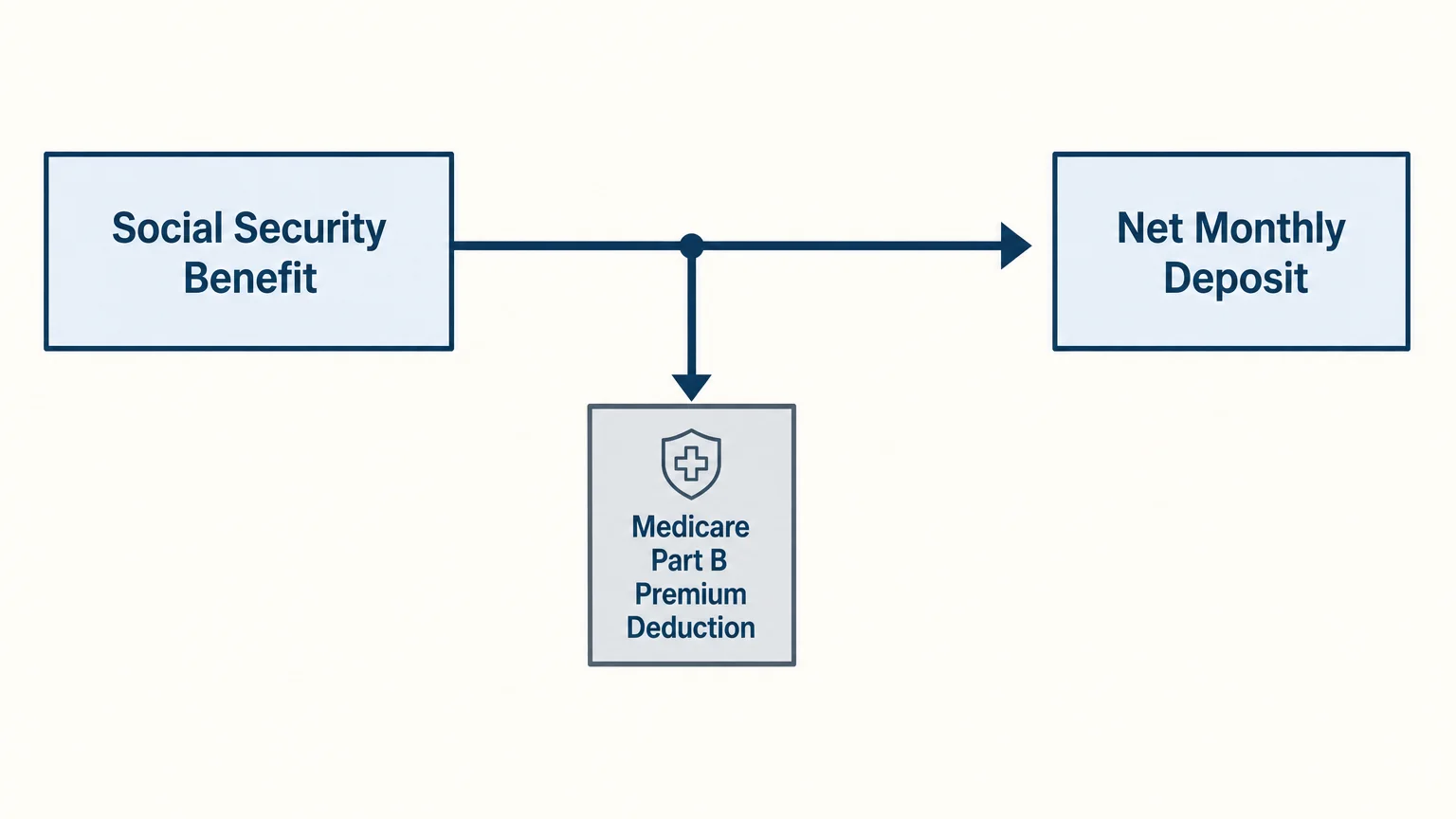

For the vast majority of retirees, Social Security benefits and Medicare Part B premiums are permanently linked. When you enroll in Medicare Part B, the federal government automatically deducts your monthly premium from your Social Security check before the funds ever reach your bank account. Because of this structural connection, any increase in your Social Security benefit must outpace the annual increase in Medicare premiums for you to feel a positive difference in your budget.

In 2026, the standard Medicare Part B premium is $202.90 per month, which represented a nearly $18 increase from the 2025 premium of $185.00. Healthcare inflation traditionally runs higher than general consumer inflation. If the Centers for Medicare and Medicaid Services (CMS) announces another significant premium hike for 2027, that increase will consume a portion—or in some rare cases, the entirety—of your COLA. For instance, if your COLA provides an extra $50 a month, but your Medicare Part B premium rises by $20 a month, your net increase drops to $30.

Fortunately, federal law provides a safety net known as the “hold harmless” provision. This rule guarantees that your Medicare Part B premium increase cannot exceed the dollar amount of your Social Security cost-of-living adjustment. If you receive a very small Social Security benefit, the hold harmless provision prevents a rising Medicare premium from actually reducing your net monthly check. Your benefit will simply remain flat. However, you do not qualify for hold harmless protection if you are a new Medicare enrollee, if you pay your premiums directly rather than having them deducted from Social Security, or if you are subject to high-income surcharges.

Those high-income surcharges—officially called the Income-Related Monthly Adjustment Amount (IRMAA)—add another layer of complexity. Medicare uses a two-year lookback period to determine your premium. Therefore, your 2027 Medicare Part B and Part D premiums will be based on the Modified Adjusted Gross Income (MAGI) you report on your 2025 tax return. If selling a home, executing large Roth conversions, or taking substantial required minimum distributions pushed your income into a higher tier in 2025, you will pay significantly more for Medicare in 2027, regardless of your Social Security COLA.

Taxes and Your Increased Benefits

One of the most persistent and frustrating surprises for new retirees is discovering that the federal government taxes Social Security benefits. What makes this taxation particularly aggressive during periods of high inflation is that the income thresholds triggering these taxes are not indexed for inflation. They have remained completely static since they were enacted decades ago.

The Internal Revenue Service uses a formula called “provisional income” (sometimes called combined income) to determine how much of your benefit faces taxation. You calculate your provisional income by taking your Adjusted Gross Income, adding any nontaxable interest (such as municipal bond interest), and then adding exactly 50 percent of your Social Security benefits.

If you file your taxes as an individual, a provisional income between $25,000 and $34,000 means up to 50 percent of your benefit may be taxable. If your provisional income exceeds $34,000, up to 85 percent of your benefit becomes taxable. For married couples filing jointly, the 50 percent threshold sits between $32,000 and $44,000, while incomes above $44,000 trigger the 85 percent taxation bracket.

Because these thresholds never change, a generous COLA acts as a double-edged sword. As your Social Security payments increase to keep pace with inflation, that extra income automatically drives up your provisional income. This phenomenon frequently pushes retirees over the $34,000 or $44,000 limits, subjecting a larger portion of their benefits to federal income tax. Managing this dynamic requires intentional tax planning.

“Always pay taxes at the lowest rates, even if it means paying taxes when they’re not required.” — Ed Slott, CPA and Retirement Tax Expert

As Ed Slott advises, proactive tax planning allows you to control your tax brackets. Many retirees execute strategic Roth conversions during years when their income dips, moving funds from tax-deferred IRAs into tax-free Roth IRAs. While you pay taxes on the converted amount today, any future withdrawals from that Roth IRA will not increase your provisional income. This strategy helps shield your future Social Security benefits from taxation, allowing you to keep more of your COLA.

Navigating the Purchasing Power Gap

The core purpose of the cost-of-living adjustment is to preserve your purchasing power. It is not a raise or a bonus; it is a defensive mechanism designed to prevent inflation from eroding your standard of living. However, many retirees find that their personal rate of inflation runs much higher than the official national average.

This discrepancy happens because retirees spend their money differently than the general population. While younger workers might allocate a large percentage of their income to transportation, apparel, and electronics, older adults spend a disproportionate amount of their budget on healthcare, prescription drugs, housing, and groceries. When the prices for these specific categories surge, a standard COLA often feels inadequate.

“We’ve spent so much time thinking about accumulation that we haven’t thought about a plan to take what we have accumulated and stretch it over however long we live.” — Jean Chatzky, Personal Finance Expert

Bridging this purchasing power gap requires you to re-evaluate your withdrawal strategy. If your Social Security COLA fails to cover the rising cost of your specific expenses, you must pull more from your investment portfolio to maintain your lifestyle. Relying on a rigid “4 percent rule” withdrawal strategy can be dangerous during high-inflation years. Instead, you need a flexible approach that allows you to trim discretionary spending while ensuring your essential needs remain fully funded.

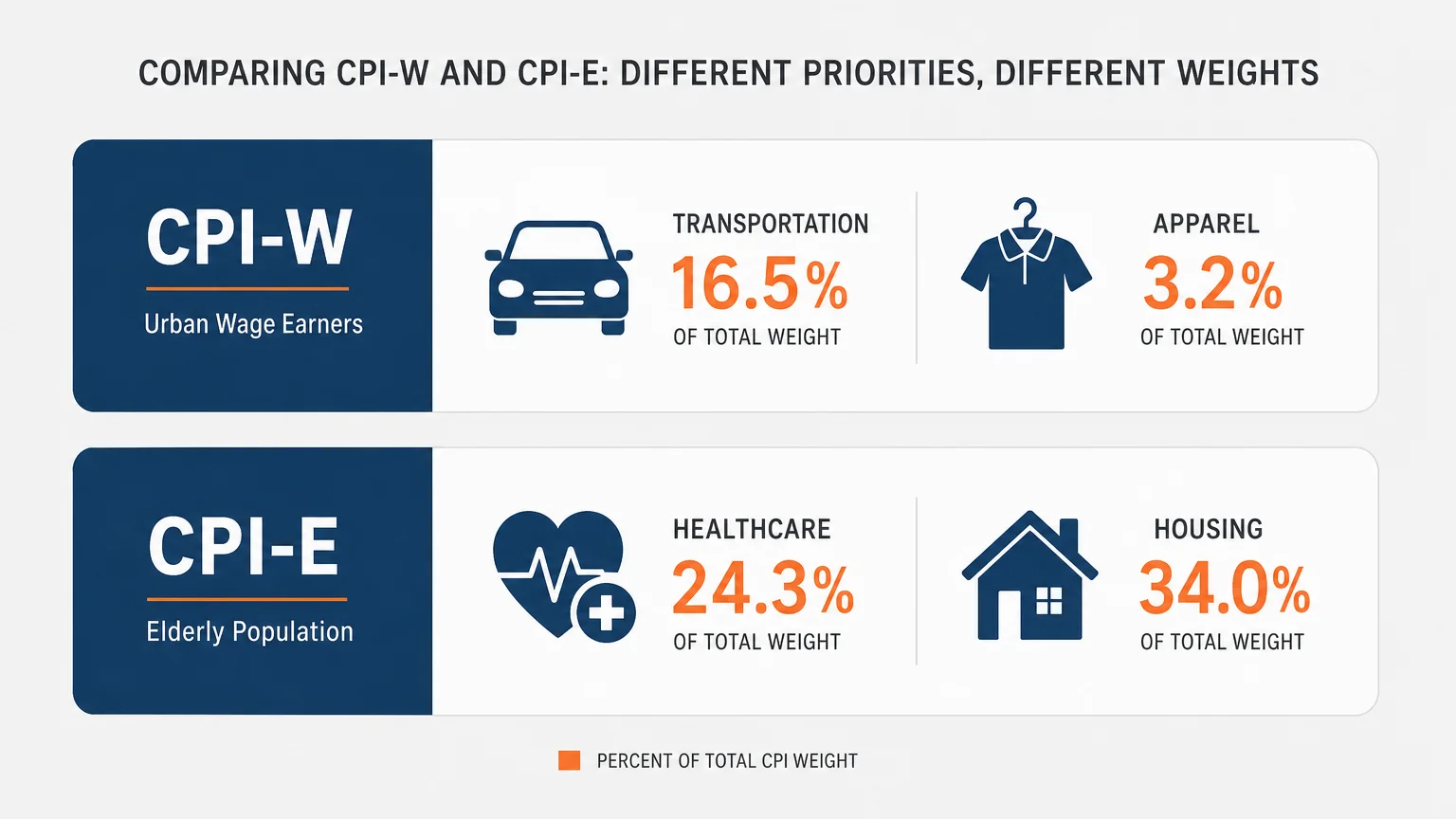

Comparing Inflation Metrics: CPI-W vs. CPI-E

The feeling that the COLA does not accurately reflect senior spending is not just an illusion; it is a structural reality of how the government calculates the adjustment. By law, the Social Security Administration must use the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Senior advocacy groups have lobbied for years to switch the calculation to the Consumer Price Index for the Elderly (CPI-E), which tracks the spending habits of Americans aged 62 and older.

Understanding the difference between these two metrics helps clarify why your cost of living may feel disconnected from your annual adjustment.

| Feature | CPI-W (Current Standard) | CPI-E (Proposed Standard) |

|---|---|---|

| Target Demographic | Urban workers and clerical staff (typically younger). | Americans aged 62 and older. |

| Healthcare Weighting | Lower. Younger workers spend less on medical care. | Significantly higher. Accurately reflects rising Medicare and out-of-pocket costs. |

| Housing Weighting | Moderate. | Higher. Seniors spend a larger percentage of fixed incomes on housing and utilities. |

| Transportation Weighting | Higher. Factors in daily commuting, gas, and vehicle purchases. | Lower. Retirees commute less frequently. |

| Resulting COLA | Often lags behind the actual inflation experienced by retirees. | Historically results in a slightly higher, more accurate benefit increase (typically 0.2% to 0.3% higher). |

Until Congress passes legislation changing the formula, the CPI-W remains the law of the land. You must plan your budget expecting the official adjustment to slightly underrepresent your actual healthcare and housing inflation.

Actionable Strategies to Protect Your Income

You cannot control the inflation rate or the official government formula, but you can control how you structure your retirement income. Taking proactive steps today ensures that inflation does not derail your long-term security.

- Optimize Your Claiming Strategy: If you have not yet claimed Social Security, strongly consider delaying your benefits. Every year you wait past your full retirement age until age 70 increases your base benefit by 8 percent. Because the annual COLA is a percentage multiplier, applying that percentage to a larger base benefit yields significantly more total dollars over your lifetime.

- Re-shop Your Medicare Coverage: Medicare Advantage and Part D prescription drug plans change their formularies and pricing every single year. Use the Medicare Open Enrollment period (October 15 through December 7) to compare plans on Medicare.gov. Switching to a plan that covers your specific medications at a lower cost can save you hundreds of dollars, effectively putting the COLA back in your pocket.

- Implement Tax Diversification: Build buckets of money with different tax treatments. Keep funds in taxable brokerage accounts, tax-deferred accounts (Traditional IRAs), and tax-free accounts (Roth IRAs). When inflation spikes and you need extra cash, pulling from a Roth IRA prevents you from increasing your provisional income and triggering the Social Security tax torpedo.

- Audit Your Discretionary Spending: Track your actual expenses over a three-month period. Separate your essential bills (housing, food, healthcare, utilities) from your discretionary spending (travel, dining out, hobbies). When inflation drives up your essential costs, knowing exactly where to temporarily trim discretionary spending provides immediate financial relief.

- Build a Robust Cash Buffer: Maintain one to two years of living expenses in a high-yield savings account or short-term Treasury bills. This cash buffer ensures you do not have to sell stocks at a loss during a market downturn just to keep up with rising daily living costs.

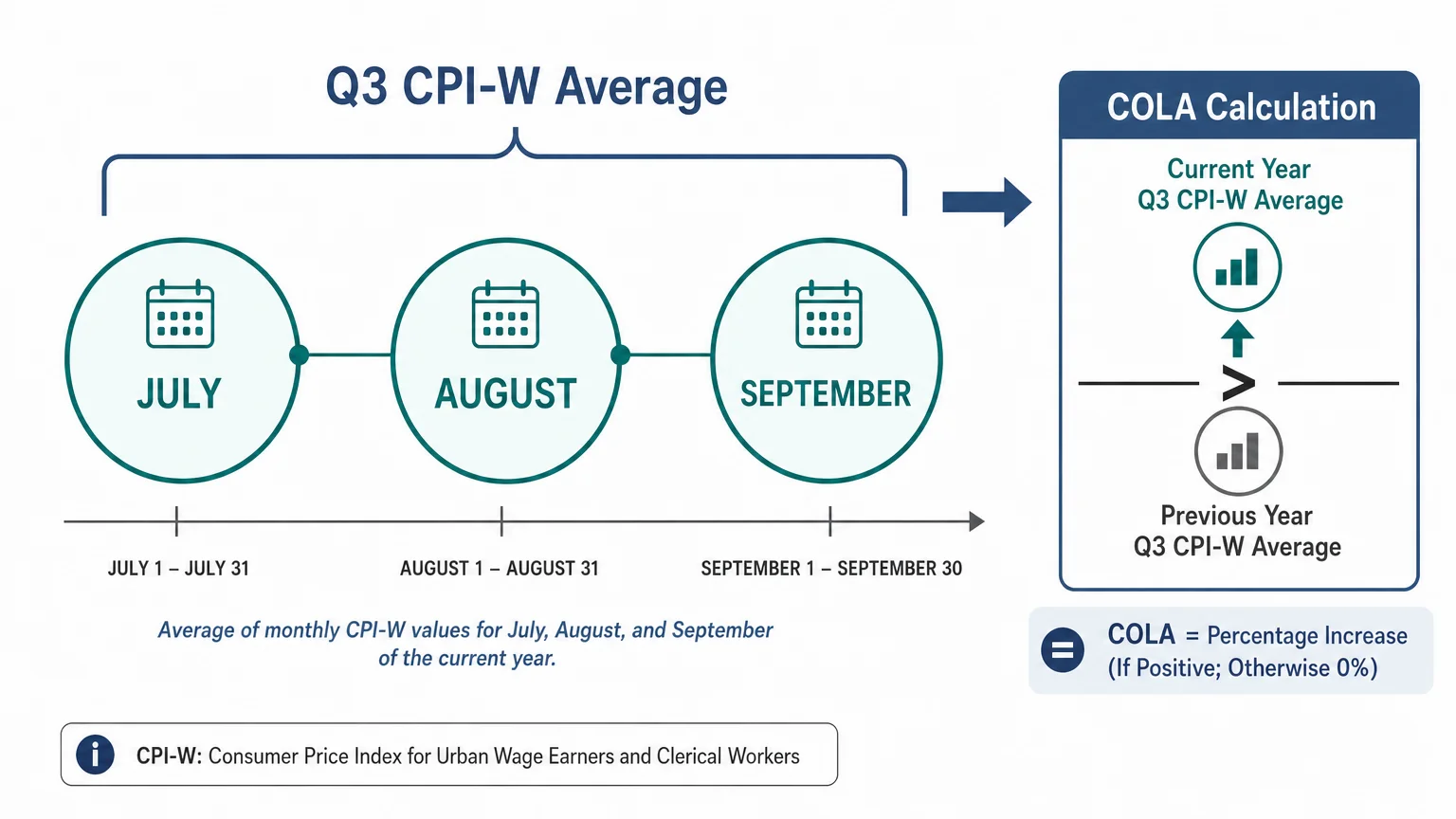

The Calculation: How Social Security Determines the Official Rate

While advocacy groups release monthly predictions, the official adjustment relies on a strict, legally mandated timeline. The Social Security Administration does not look at inflation across the entire calendar year. Instead, they focus exclusively on the third quarter.

The Bureau of Labor Statistics gathers CPI-W data for the months of July, August, and September. In mid-October, the government averages the data from these three months and compares it to the third-quarter average from the previous year. If the current year’s average is higher, the percentage difference becomes the official COLA for the upcoming year. If prices remain flat or decrease (deflation), benefits stay exactly the same—the law prohibits Social Security from reducing benefits due to deflation.

Once the government announces the official rate in October, the Social Security Administration applies the adjustment to benefits payable in January. Because Social Security pays benefits a month in arrears, the increase officially takes effect in December but shows up in the payment you receive in January 2027.

What Can Go Wrong

Relying too heavily on early predictions can lead to financial missteps. While a 3.8 percent forecast sounds promising, several factors can disrupt your expectations.

First, economic conditions change rapidly. If the Federal Reserve successfully cools the economy and inflation drops sharply during the summer months, the third-quarter data will come in lower than current projections. The final COLA announced in October could easily land closer to 2.5 or 3.0 percent. If you budget based on the higher prediction, you will face a shortfall come January.

Second, retirees frequently overestimate their net income by ignoring state taxes. While the federal government taxes Social Security based on provisional income, roughly ten states still tax Social Security benefits to varying degrees. Kiplinger regularly updates its state-by-state tax guides, which provide essential reading if you plan to relocate. Failing to factor state tax liabilities into your budget will leave you with less disposable income than you planned.

Finally, underestimating personal healthcare inflation remains a critical danger. Even if the COLA is robust, a new diagnosis requiring expensive tier-3 or tier-4 prescription drugs can decimate your monthly budget. You must plan for out-of-pocket medical maximums, not just baseline premiums.

When to Consult a Professional

While you can manage basic budgeting independently, the interaction between Social Security, Medicare, and the IRS creates a highly complex web. You should seek guidance from a fee-only fiduciary financial planner or a certified public accountant (CPA) when you encounter specific trigger events.

Consult a professional if you are nearing age 63 and plan to transition into Medicare soon. Because of the two-year IRMAA lookback, the income you earn at age 63 dictates your Medicare premiums at age 65. A professional can help you structure your income to avoid unnecessary surcharges.

You also need expert guidance when you face Required Minimum Distributions (RMDs). Once you reach your early 70s, the IRS forces you to withdraw money from your tax-deferred accounts. These mandatory withdrawals can drastically alter your tax bracket and subject a maximum 85 percent of your Social Security to taxation. A tax professional can help you execute strategic charitable distributions or Roth conversions to mitigate this impact before the RMDs begin.

Finally, consult a professional if you experience a major life transition, such as divorce or the death of a spouse. The “widow’s penalty” forces the surviving spouse to file taxes as an individual, drastically lowering the threshold for Social Security taxation and Medicare surcharges, even though the household only lost one Social Security check.

Final Steps to Take Before October

You do not need to wait for the October announcement to prepare your finances. Start by logging into your my Social Security account to verify your current benefit amount and review your earnings record. If you have not yet claimed, use the site’s calculators to see how delaying your claim impacts your future monthly payouts.

Next, perform a comprehensive review of your household spending. Pull your bank statements from the last three months and categorize your expenses. Identify exactly where inflation hits your budget the hardest. Having an accurate picture of your baseline expenses allows you to plug the official COLA number into your budget immediately upon its release.

Lastly, prepare for the Medicare Open Enrollment period. Create a list of your current medical providers and prescription dosages. When October arrives, you will have the information you need to swiftly compare plans, ensuring that a rising Part B or Part D premium does not unfairly consume your cost-of-living adjustment. Taking these proactive steps today positions you to navigate 2027 with financial confidence and clarity.

Last updated: June 2026. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.