Millions of older Americans struggle to stretch their retirement savings while billions of dollars in government assistance go unclaimed every year. If you find yourself rationing essential medications or turning down the thermostat to save money, you might be missing out on programs designed to lower your living costs. Federal and state agencies offer substantial financial relief for healthcare premiums, prescription drugs, groceries, and utility bills, yet complex eligibility rules keep many retirees from applying. Because income guidelines constantly evolve, many seniors who were previously denied now qualify under updated thresholds. By taking the time to understand and claim these commonly overlooked benefits, you can drastically reduce your monthly expenses and protect your long-term financial independence.

1. Medicare Savings Programs (MSPs)

Paying your Medicare Part B premium—which the government automatically deducts from your Social Security check—takes a noticeable bite out of your fixed monthly income. Medicare Savings Programs help lower-income individuals cover these premiums and, in some instances, completely eliminate deductibles and copayments for medical care.

Many seniors assume that having any retirement savings automatically disqualifies them from Medicare assistance. However, not all assets count toward the strict eligibility limits; your primary residence, one vehicle, and your household goods are entirely exempt from the calculation. Furthermore, several states—including California and New York—have recently eliminated the asset test entirely for these programs, opening the door for house-rich but cash-poor retirees.

The Qualified Medicare Beneficiary (QMB) program is the most robust option available. For 2026, the QMB program carries a federal individual monthly income limit of $1,350 and a resource limit of $9,950. If you secure QMB status, federal law strictly prohibits medical providers from billing you for deductibles or copayments for any Medicare-covered services. This means you can visit your doctor or undergo a procedure without fearing a surprise medical bill in the mail.

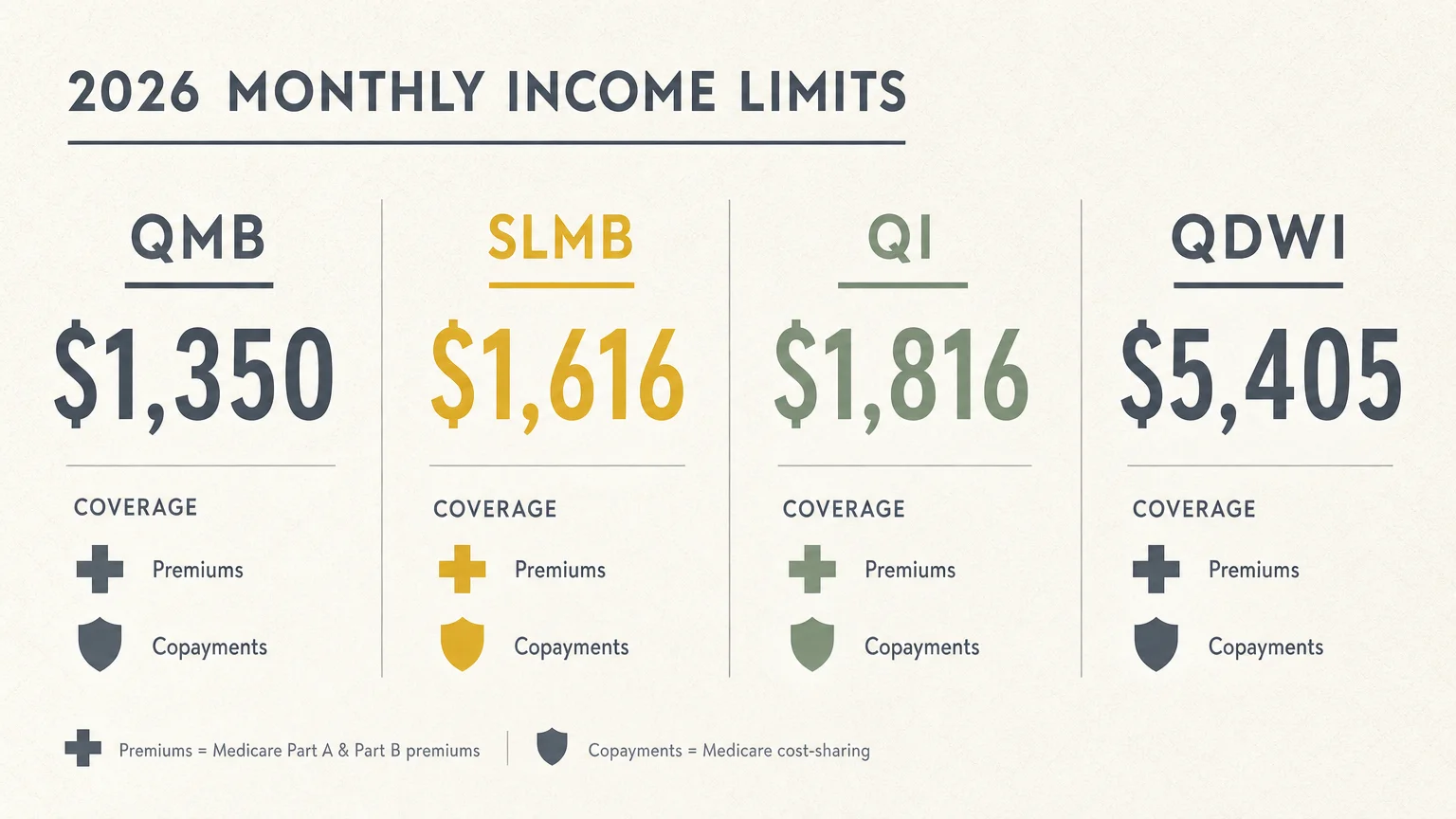

Comparing the Four Medicare Savings Programs

If you need help managing your healthcare costs, your state Medicaid office will determine which specific program you qualify for based on your financial footprint. Here is a breakdown of the 2026 federal monthly income limits for single individuals:

| Program Name | 2026 Individual Income Limit | What the Program Covers |

|---|---|---|

| Qualified Medicare Beneficiary (QMB) | $1,350 per month | Part A and B premiums, deductibles, and copayments |

| Specified Low-Income Medicare Beneficiary (SLMB) | $1,616 per month | Part B premiums only |

| Qualifying Individual (QI) | $1,816 per month | Part B premiums only |

| Qualified Disabled and Working Individuals (QDWI) | $5,405 per month | Part A premiums only |

2. Medicare Extra Help (Part D Low-Income Subsidy)

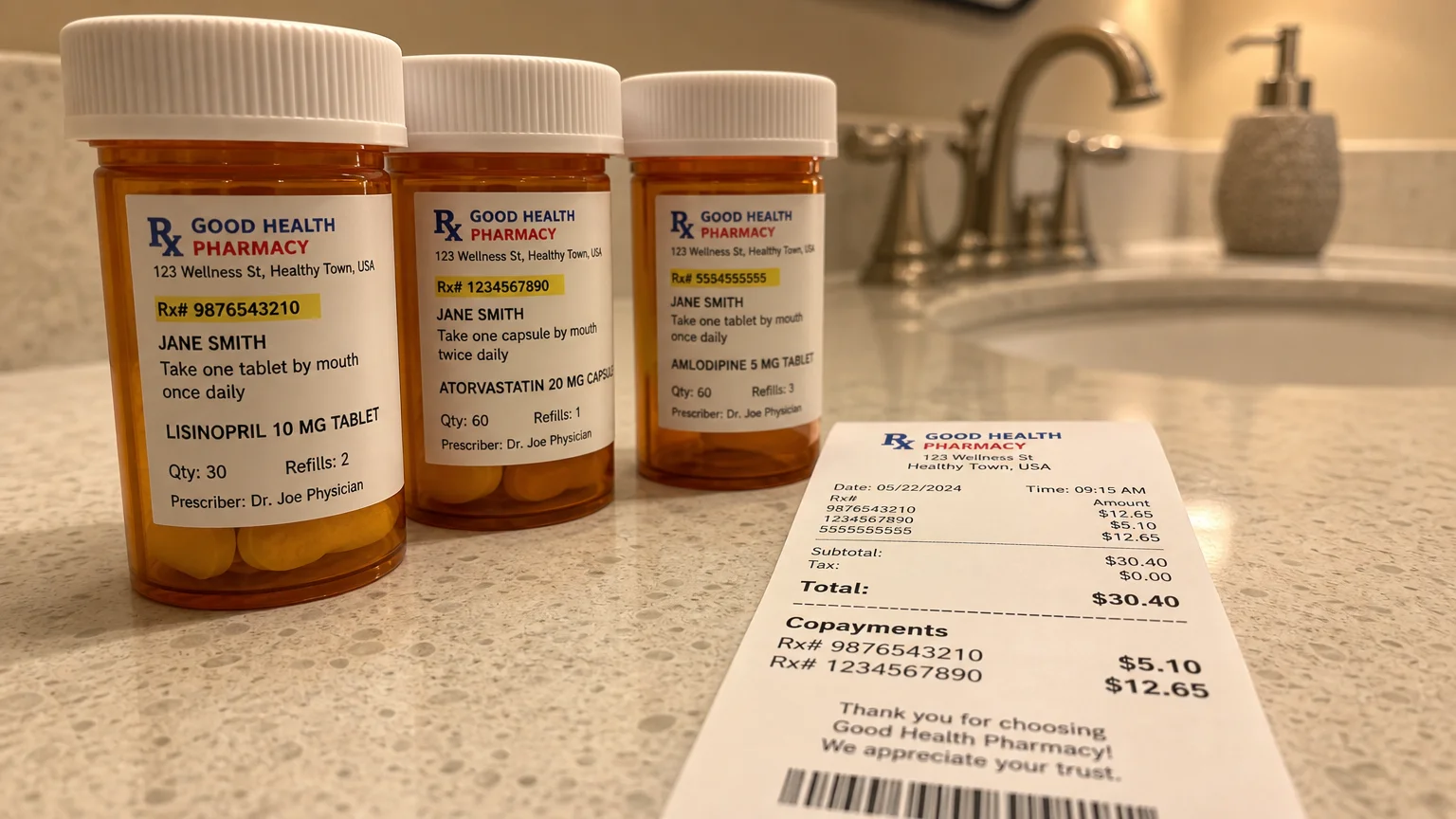

Prescription medication costs can single-handedly devastate a carefully planned retirement budget. Extra Help, officially known as the Part D Low-Income Subsidy, is a federal program that subsidizes Medicare Part D premiums, annual deductibles, and pharmacy copayments. If you qualify for a Medicare Savings Program, you are automatically enrolled in Extra Help; otherwise, you must submit an application directly through the Social Security Administration.

As of 2026, the annual income limit to qualify for Extra Help is $23,940 for a single individual and $31,725 for a married couple living together. The program drastically alters how much you pay at the pharmacy counter. Under current regulations, your copayments are capped at $5.10 for generic drugs and $12.65 for brand-name medications.

More importantly, recent legislative updates have completely transformed the out-of-pocket maximums. Once your total prescription drug spending reaches $2,100 in 2026, you will pay exactly $0 for any covered medication for the remainder of the calendar year. This hard cap provides immense peace of mind for seniors managing expensive chronic conditions like diabetes, heart disease, or rheumatoid arthritis.

3. Supplemental Nutrition Assistance Program (SNAP)

The Supplemental Nutrition Assistance Program remains one of the most misunderstood and underutilized benefits among older adults. A massive percentage of eligible seniors refuse to apply because they mistakenly believe that owning a home disqualifies them or that they will only receive a trivial amount of assistance that is not worth the bureaucratic hassle.

In reality, the maximum SNAP allotment for a single-person household in 2026 is $298 per month. What many retirees miss is the powerful “medical deduction” built into the application process. If you are 60 or older and incur out-of-pocket medical expenses exceeding $35 a month, you can deduct these costs from your gross income when the state calculates your SNAP eligibility. Qualifying expenses include Medicare premiums, prescription copays, hearing aids, dental care, and even transportation to medical appointments. By thoroughly documenting these medical costs, you can lower your net countable income and secure a substantially higher grocery benefit.

Additionally, participating in SNAP often serves as a gateway to other financial relief. Being an active SNAP recipient typically qualifies you for discounted utility rates, specialized senior delivery services, and reduced-cost internet programs.

4. Veterans Aid and Attendance Pension

If you or your spouse served during a recognized period of war, you might be eligible for a massive financial boost designed to help cover the exorbitant costs of long-term care. The Aid and Attendance pension provides monthly, tax-free payments on top of the standard VA pension for veterans who need physical assistance with activities of daily living—such as bathing, dressing, or eating—or who are bedridden or suffer from severe visual impairment.

For 2026, the maximum monthly Aid and Attendance benefit rate is an impressive $2,424 for a single veteran and $1,558 for a surviving spouse. Married veterans can receive up to $2,874 per month. You can use these funds to pay for private in-home care, assisted living facility fees, or nursing home care.

To qualify, you must meet specific military service, clinical, and financial parameters. The VA applies a strict net worth limit—set at $163,699 for 2026—which includes your countable assets and annual income combined. However, the calculation is highly favorable to those already paying for care; the VA allows you to subtract your unreimbursed medical expenses from your income, making it significantly easier to meet the financial threshold.

5. Supplemental Security Income (SSI)

Not to be confused with standard Social Security retirement benefits—which are based on your lifetime earnings record—Supplemental Security Income (SSI) is a strict, needs-based welfare program. Administered by the Social Security Administration, SSI provides monthly cash assistance to adults aged 65 and older, as well as disabled individuals, who have minimal income and practically zero financial safety net.

For 2026, the maximum federal SSI payment stands at $994 a month for an eligible individual and $1,491 for an eligible couple. While the federal asset limit is notoriously rigid, many states proactively step in to offer supplemental cash payments on top of this federal base rate to help combat local living costs.

Your actual benefit amount depends heavily on your living arrangement. For instance, if you live in someone else’s household and do not pay your fair share of food and shelter expenses, the government will automatically reduce your SSI benefit by one-third. Understanding these complex living arrangement rules is essential before you submit your application.

6. Low-Income Home Energy Assistance Program (LIHEAP)

Utility bills are highly volatile, making them a significant stressor for retirees trying to balance a fixed monthly budget. LIHEAP is a federally funded block grant program designed to help vulnerable, low-income households manage their energy costs. Depending on where you live, the program assists with heating bills during brutal winters and cooling bills during dangerous summer heatwaves.

Unlike monthly cash assistance, LIHEAP grants are typically paid directly to your utility provider to offset your balance. For 2026, many states set their LIHEAP income eligibility threshold at 150 percent of the federal poverty guidelines, which equates to an annual income limit of $23,940 for a single person.

Beyond simply paying your monthly electric or gas bill, LIHEAP can fund emergency weatherization projects. If you have a broken furnace in December or a failing air conditioning unit in July, the program can provide emergency crisis grants to repair or replace your HVAC equipment, ensuring your home remains safe and habitable.

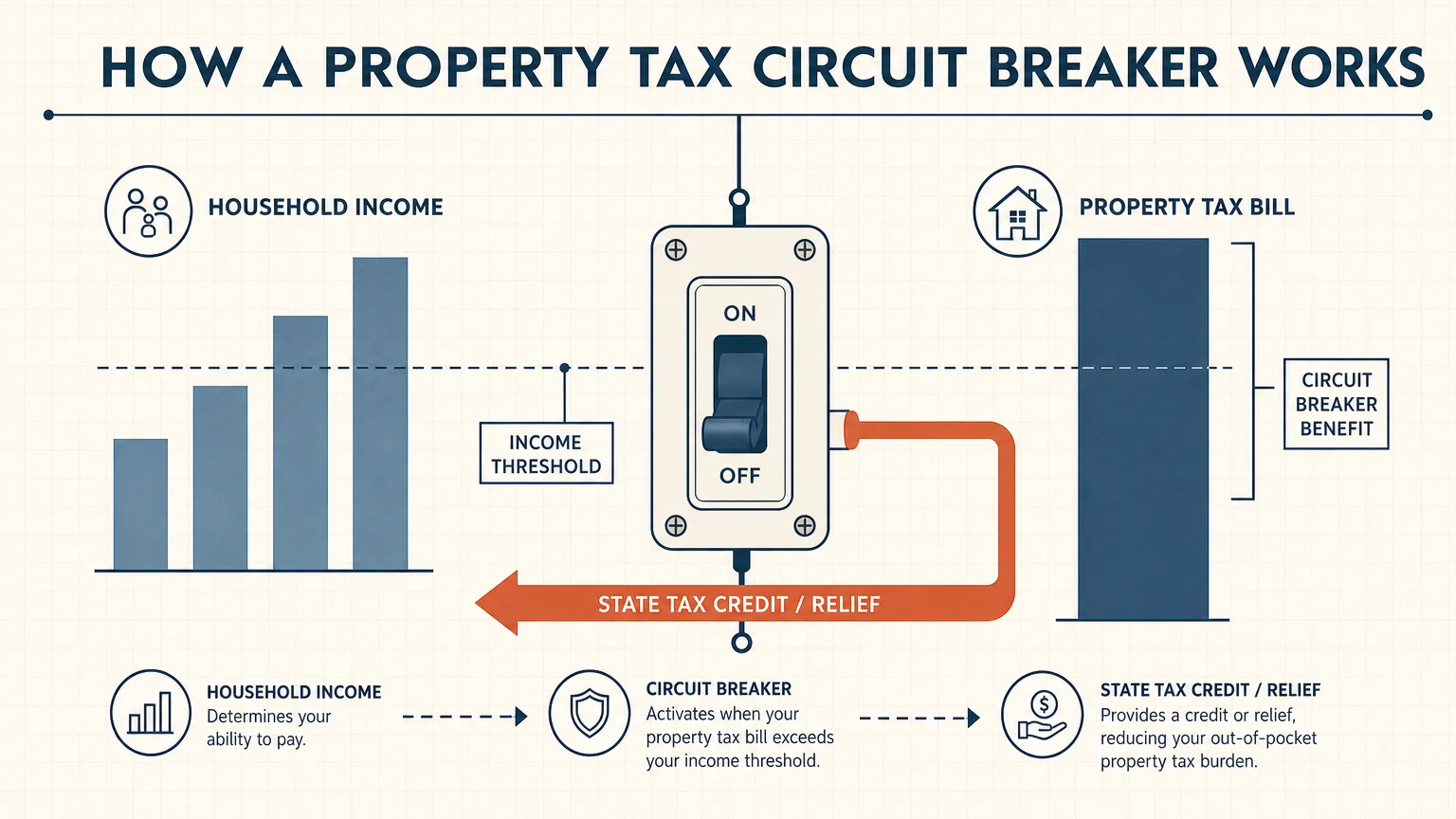

7. Property Tax Relief and Circuit Breaker Programs

While not managed at the federal level, state and local property tax relief programs represent some of the most valuable—and frequently ignored—benefits for senior homeowners. As real estate values surge across the country, property taxes skyrocket alongside them, threatening to price long-time residents out of their family homes.

To combat this, many states offer “circuit breaker” programs. Much like an electrical circuit breaker prevents a power overload, a property tax circuit breaker kicks in when your tax bill exceeds a certain percentage of your annual income, providing you with a direct rebate or tax credit. Other municipalities offer senior property tax freezes, which lock in your home’s assessed value the year you turn 65, ensuring your tax burden never increases regardless of the housing market.

Because these programs operate entirely at the county or municipal level, the eligibility rules vary wildly from one town to the next. You usually have to take the initiative and apply directly with your local county tax assessor’s office, as this relief is rarely applied automatically.

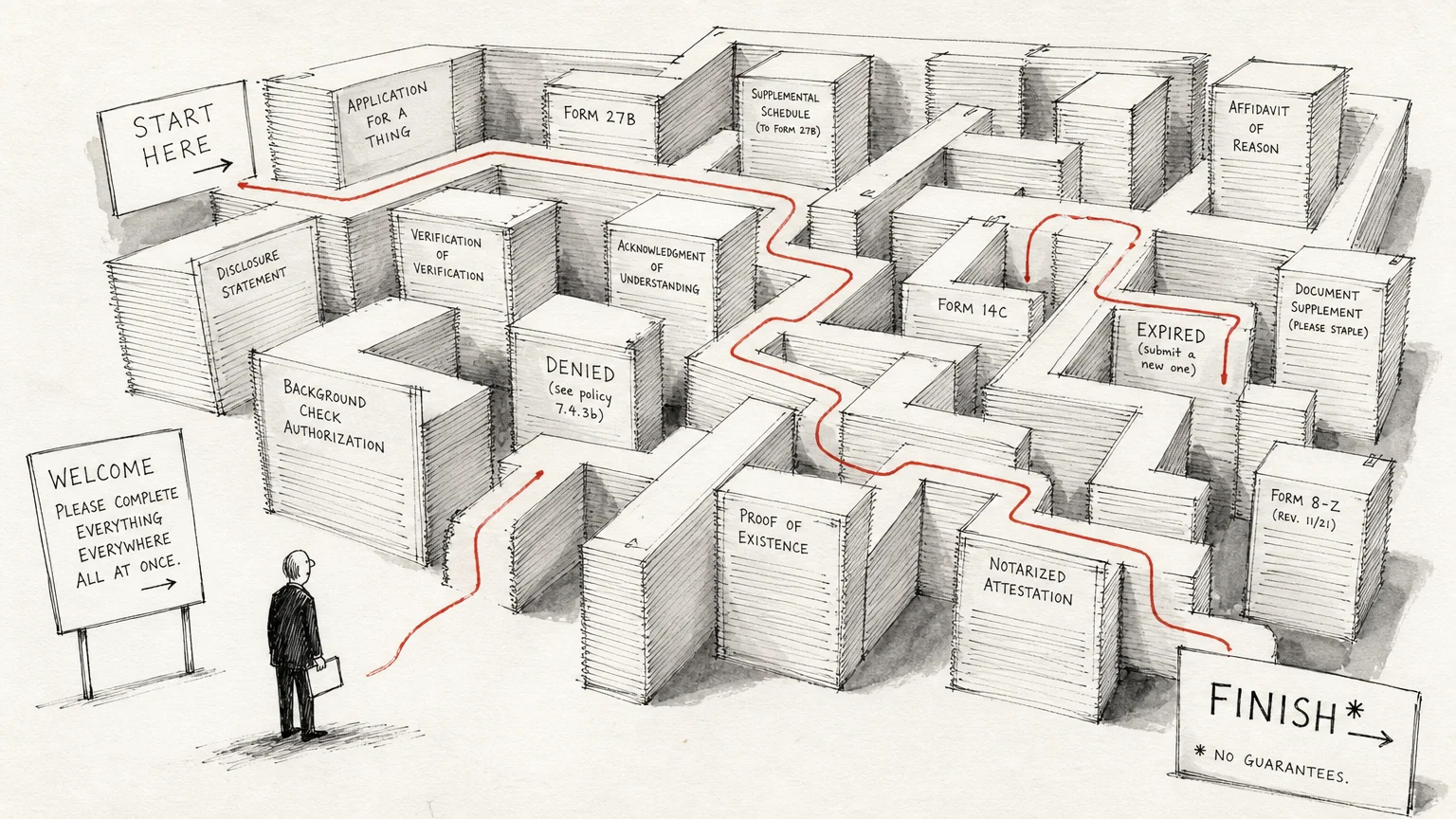

What Can Go Wrong

The landscape of government benefits is littered with bureaucratic hurdles. Many seniors accidentally disqualify themselves by making simple paperwork errors or misunderstanding the complex terminology used by state agencies.

- Assuming you make too much money: Government programs rarely look at your gross income in a vacuum. Instead, they evaluate your net countable income. A significant portion of your income may be entirely disregarded if you demonstrate high out-of-pocket medical expenses, pay steep health insurance premiums, or support a dependent.

- Missing strict funding deadlines: Programs like LIHEAP operate on a strict first-come, first-served basis. Once your specific state runs out of allocated funds for the heating or cooling season, they will immediately stop accepting applications. Applying on the very first day the portal opens is crucial.

- Failing to update your status: If your financial picture changes—perhaps a working spouse fully retired, you lost a part-time job, or a new medical condition developed—you must reapply. A harsh denial letter last year could easily become a fast-tracked approval letter under your new circumstances.

- Misunderstanding the VA look-back period: The VA enforces a 36-month look-back period for asset transfers. If you gift money to your children or transfer a home into an irrevocable trust right before applying for Aid and Attendance, you will face severe penalty periods that delay your monthly payouts.

When to Consult a Professional

While you can successfully navigate simple applications like SNAP or LIHEAP on your own, other benefits require a sophisticated strategy to secure. Consider consulting a professional in these specific scenarios:

- Applying for VA Aid and Attendance: Because of the rigorous financial look-back periods and the highly specific medical documentation required to prove your need for daily assistance, working with a VA-accredited claims agent can prevent devastating application delays.

- Structuring Medicaid for Nursing Home Care: If you or your spouse must transition to a nursing facility and need Medicaid to cover the exorbitant costs, an elder law attorney can legally structure your assets to ensure the healthy spouse is not left completely impoverished.

- Managing Denied Disability Claims: If your application for SSI or Social Security Disability is denied, a disability advocate can skillfully guide you through the appeals process, ensuring you meet strict procedural deadlines and present the proper medical evidence to an administrative law judge.

Frequently Asked Questions

Do I have to pay back government benefits when I pass away?

Most common senior assistance programs—including SNAP, Medicare Extra Help, and LIHEAP—are pure grants or subsidies that never need to be repaid. However, if you rely on Medicaid to pay for long-term nursing home care, the state is federally mandated to seek reimbursement from your estate after you pass away through the Medicaid Estate Recovery Program. Proper estate planning can help mitigate this risk.

Can I receive both VA Aid and Attendance and Medicaid at the same time?

Yes, but the two programs interact aggressively. If you secure Medicaid to pay for your nursing home stay, the VA will typically reduce your Aid and Attendance pension to a maximum of just $90 per month. Coordinating these two benefits requires precise financial planning to avoid overpayments.

How can I easily check my eligibility for all these different programs?

Instead of visiting dozens of separate government websites, you can use the free online tool called BenefitsCheckUp, managed by the National Council on Aging. By answering a few anonymous questions regarding your zip code, monthly income, and specific health conditions, the database will instantly screen you for thousands of federal, state, and local assistance programs.

“The most important number in retirement is not what you earn, but what you get to keep.” — Ed Slott, CPA and Retirement Expert

Authoritative Resources to Help You Apply

Ready to take the next step? Use these official portals to verify the current rules in your specific state and begin your application process:

- Medicare.gov: Official hub for Medicare Savings Programs and Extra Help details.

- Social Security Administration: Apply for SSI and navigate Extra Help applications.

- Department of Veterans Affairs: Download the exact forms needed for the Aid and Attendance pension.

- National Council on Aging: Access the comprehensive BenefitsCheckUp screening tool.

- USA.gov Benefits: The federal government’s official directory for housing, utility, and food assistance programs.

Taking the time to investigate and apply for these benefits can fundamentally alter your retirement trajectory. Whether it secures a few hundred dollars a month in food assistance or thousands in long-term care subsidies, this is money you spent your entire working life paying into the system—you absolutely deserve to utilize it.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.