Retirement planning in 2026 brings critical updates designed to keep more money in your pocket, from historic Medicare cost caps to brand-new senior tax deductions. Navigating these changes early ensures you maximize your fixed income and protect your savings from inflation. This year, the implementation of recent legislation reaches a crucial milestone, activating benefits that directly lower prescription drug costs and increase tax-advantaged savings limits. Whether you are already enrolled in Medicare or finalizing your timeline for claiming Social Security, understanding these seven government provisions is essential. By taking advantage of expanded standard deductions, negotiated drug prices, and adjusted retirement contribution rules, you can significantly improve your financial stability and confidently enjoy your retirement years.

1. Medicare Part D Maximum Out-of-Pocket Cap Reaches $2,100

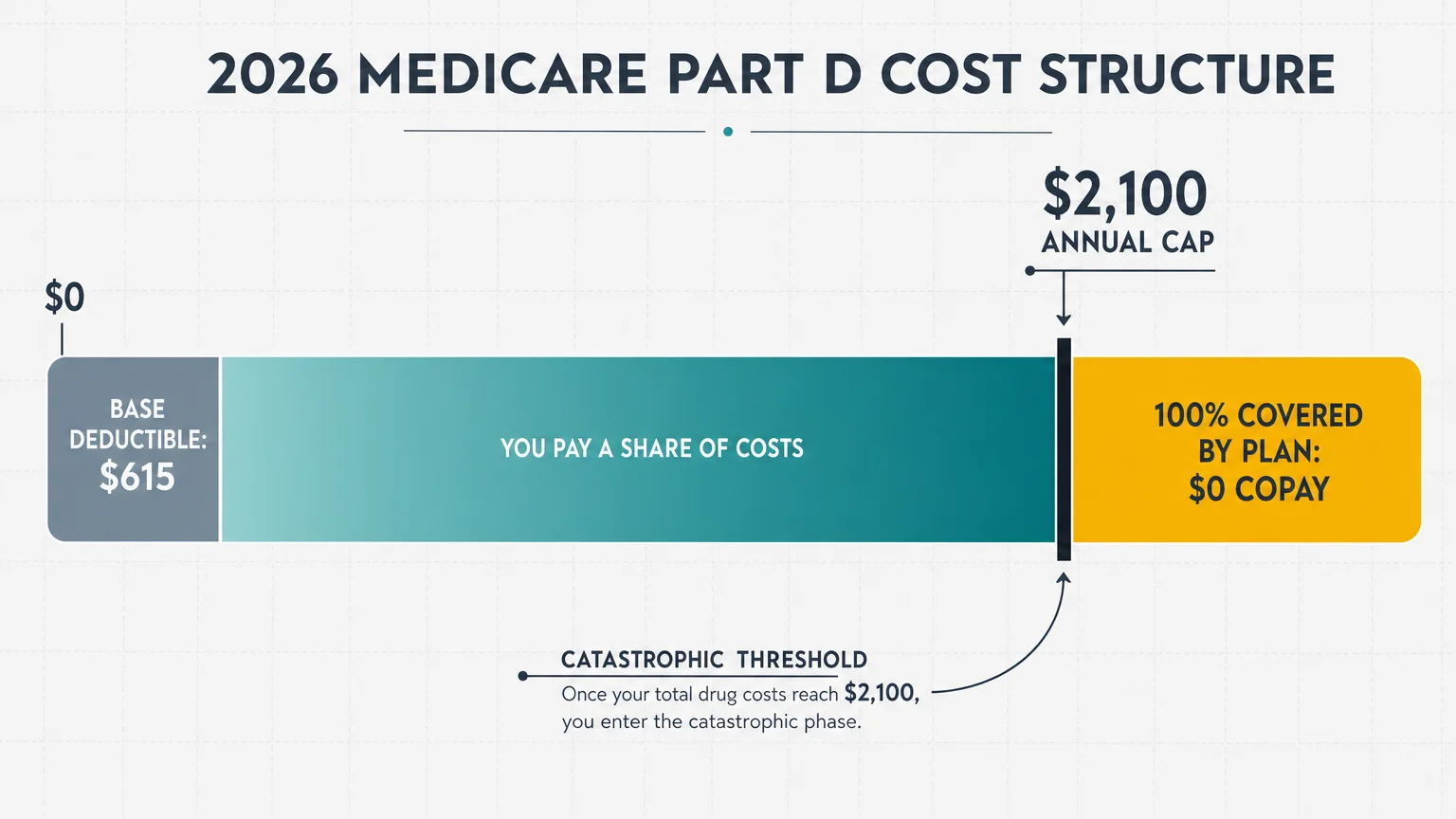

Healthcare costs consistently rank as the top financial concern for retirees. To combat this, the Inflation Reduction Act completely redesigned the Medicare Part D benefit structure. In 2025, the government introduced a hard $2,000 annual cap on out-of-pocket prescription drug costs. For 2026, this cap adjusts slightly for inflation to $2,100.

Once your total out-of-pocket spending on covered formulary drugs hits $2,100, your Part D or Medicare Advantage plan covers 100% of your eligible prescription costs for the rest of the calendar year. You pay $0 in copays or coinsurance for those medications. Keep in mind that the annual Medicare Part D base deductible also increases slightly to $615 in 2026. You must still satisfy this deductible and pay your standard copays until your total spending reaches the $2,100 catastrophic threshold. You can compare the latest plan formularies directly at Medicare.gov to ensure your medications remain covered under the new structure.

2. The First Negotiated Medicare Drug Prices Take Effect

January 1, 2026, marks a historic milestone for Medicare: the first round of government-negotiated drug prices officially goes into effect. For decades, Medicare lacked the legal authority to negotiate directly with pharmaceutical manufacturers. Now, the government flexes its purchasing power to secure deep discounts on ten of the most widely used and expensive medications.

These medications cover critical conditions affecting millions of seniors, including heart disease, diabetes, arthritis, and blood clots. The finalized negotiated rates offer discounts ranging from 38% to 79% off the original 2023 list prices. Some of the high-profile drugs benefiting from this program include:

- Eliquis and Xarelto: Widely prescribed blood thinners used to prevent strokes.

- Jardiance and Farxiga: Popular medications treating diabetes, heart failure, and chronic kidney disease.

- Enbrel and Stelara: Treatments for autoimmune conditions like rheumatoid arthritis and psoriasis.

The Centers for Medicare and Medicaid Services (CMS) projects these lower prices will save beneficiaries nearly $1.5 billion in direct out-of-pocket costs this year alone. As an added benefit, insulin costs remain firmly capped at $35 per month, and recommended adult vaccines—including the shingles shot—continue to be completely free under Part D.

3. A Groundbreaking $6,000 Additional Tax Deduction for Seniors

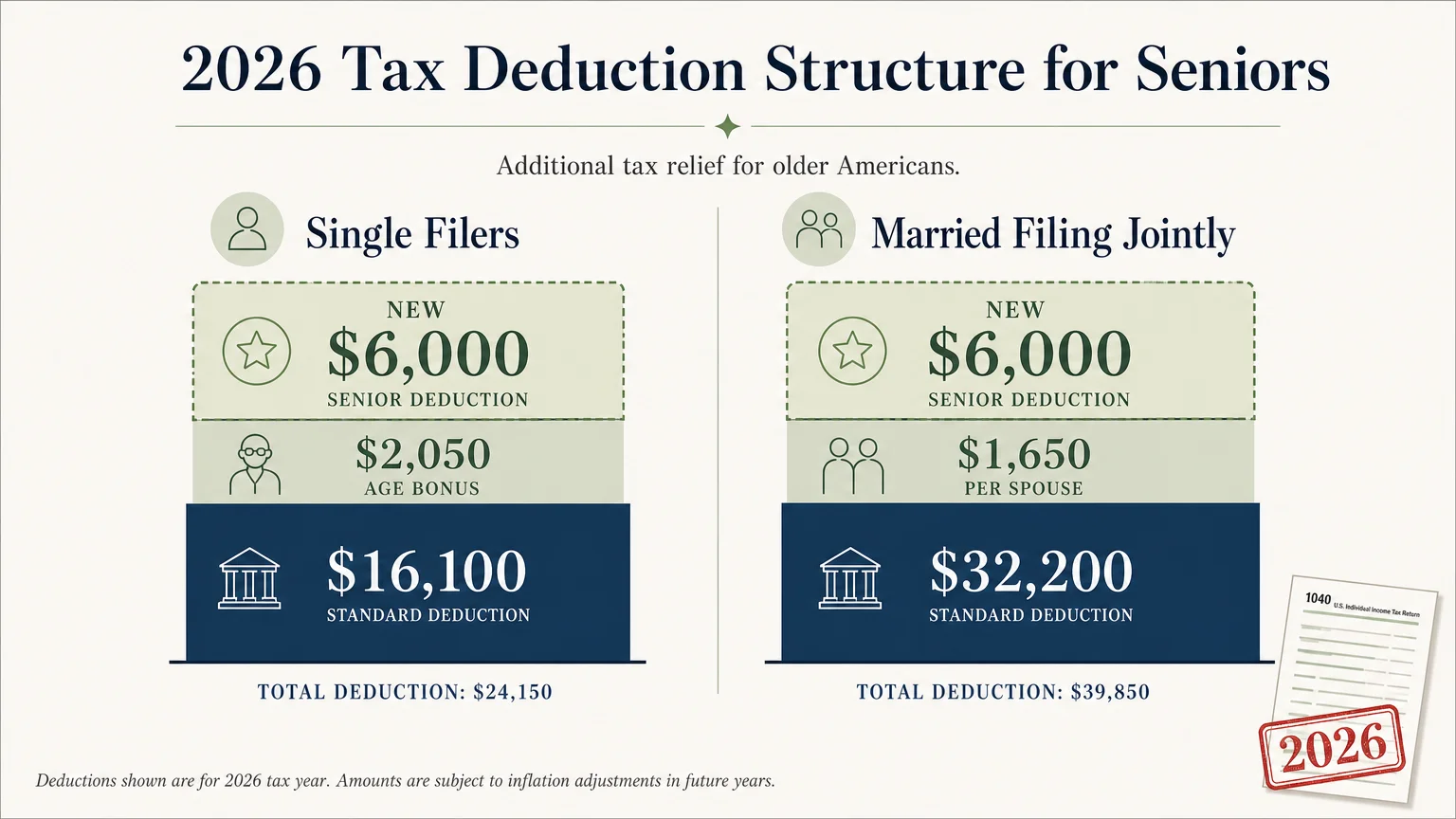

If you are 65 or older in 2026, your tax return will look significantly different. Recent federal tax adjustments provide immense relief for retirees living on fixed incomes. First, the base standard deduction increases to $32,200 for married couples filing jointly and $16,100 for single filers. You also retain the existing age-based bonus deduction—$2,050 for single filers and $1,650 per spouse for joint filers.

However, the most impactful update is a newly implemented senior tax deduction provision applicable through 2028. Qualifying taxpayers aged 65 and older can claim an additional $6,000 deduction per person. This equates to a staggering $12,000 extra deduction for a married couple where both spouses qualify. The government phases out this specific $6,000 benefit at a 6% rate for single filers earning over $75,000 and joint filers earning over $150,000.

Consider a married couple, both age 67, drawing income from Social Security and traditional IRA withdrawals. For the 2026 tax year, they start with a base standard deduction of $32,200. They add their age-based bonuses of $1,650 each, bringing their deduction to $35,500. Then, they apply the new $6,000 senior deduction per spouse. This couple now commands a $47,500 standard deduction. If their combined taxable income remains below this threshold, they effectively owe zero federal income tax. Always check the Internal Revenue Service (IRS) website for the most current tax bracket publications and worksheet instructions.

“The biggest risk retirees face is failing to adjust their strategy when the rules change. You have to aggressively manage your tax brackets and Medicare thresholds every single year.” — Ed Slott, CPA and Retirement Tax Expert

4. Increased “Super Catch-Up” Contributions for Ages 60 to 63

The SECURE 2.0 Act heavily rewards Americans in the final sprint toward retirement. If you are 60, 61, 62, or 63 years old in 2026, you qualify for a “super catch-up” contribution to your workplace retirement plan. While the standard catch-up allowance for workers 50 and older is $8,000, those in this specific four-year age bracket can contribute an extra $11,250 to their 401(k), 403(b), or Thrift Savings Plan (TSP).

With the 2026 base contribution limit set at $24,500, a 62-year-old employee can stash away up to $35,750 in a single year. Major brokerages like Fidelity Investments offer calculators to help you model how these super catch-ups impact your long-term compounding.

| Age Group in 2026 | Base 401(k) Limit | Catch-Up Limit | Total Potential Contribution |

|---|---|---|---|

| Under 50 | $24,500 | $0 | $24,500 |

| 50 to 59 | $24,500 | $8,000 | $32,500 |

| 60 to 63 | $24,500 | $11,250 | $35,750 |

| 64 and Older | $24,500 | $8,000 | $32,500 |

High-income earners face a critical new mandate regarding these limits. Starting in 2026, if you earned more than $150,000 from your employer in the previous calendar year, the IRS requires you to make all catch-up contributions using after-tax Roth dollars. You lose the immediate pre-tax deduction, but your future withdrawals from those specific contributions will be entirely tax-free. If you fall into this income bracket, coordinate with your human resources department early to ensure your payroll deductions route correctly.

5. Lower Penalties for Missed Required Minimum Distributions

Navigating Required Minimum Distributions (RMDs) from your traditional IRAs and 401(k)s often induces unnecessary anxiety. Historically, forgetting to take your RMD triggered a devastating 50% excise tax on the exact amount you failed to withdraw. The government recognized this penalty was overly punitive and significantly softened the blow under the SECURE 2.0 Act.

The base penalty for a missed RMD now sits at 25%; more importantly, if you realize your mistake and correct the missed withdrawal within a two-year correction window, the IRS further reduces the penalty to just 10%. Additionally, the government officially eliminated RMD requirements for employer-sponsored Roth 401(k) accounts. This aligns workplace Roth rules with existing Roth IRA regulations, granting you complete control over how long you let your tax-free investments grow without forced distributions.

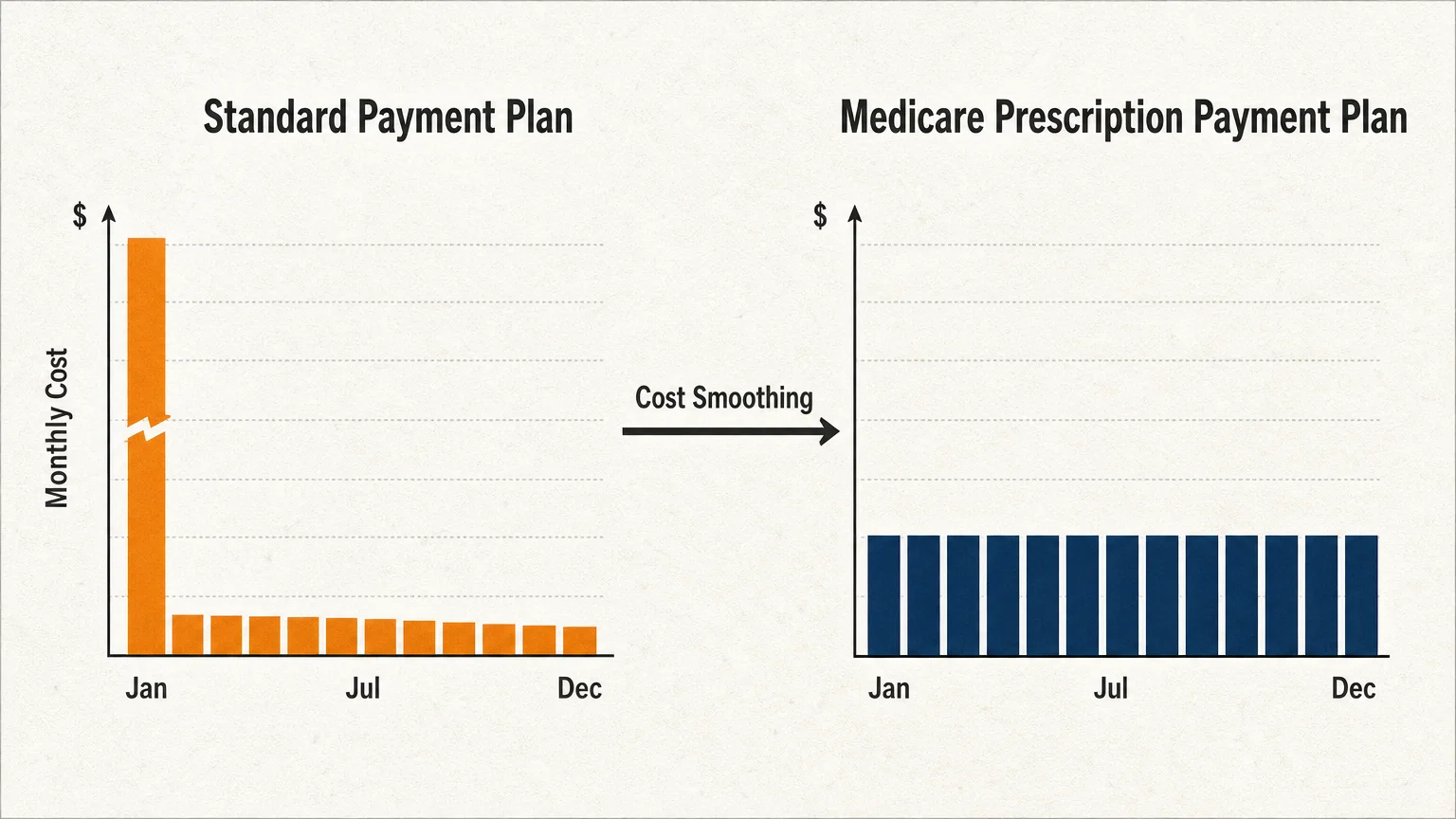

6. The Medicare Prescription Payment Plan Smooths Out Costs

The $2,100 out-of-pocket maximum provides excellent annual protection, but it does not prevent a massive pharmacy bill in January or February from derailing your monthly cash flow. To solve this specific problem, Medicare implemented the Prescription Payment Plan.

This completely free, opt-in program allows you to spread your out-of-pocket prescription drug costs across the entire calendar year. Instead of paying a $615 lump sum to satisfy your deductible during a single pharmacy visit, your Part D sponsor breaks your anticipated costs into manageable, interest-free monthly installments. Your pharmacy will simply process your prescription for $0 at the counter, and your insurance company will send you a monthly bill for your portion. You must actively opt into this program by contacting your specific Medicare Part D or Medicare Advantage provider directly.

7. The 2026 Social Security COLA Boost

The Social Security Administration adjusts benefits annually to ensure your purchasing power survives inflation. The SSA calculates this Cost-of-Living Adjustment (COLA) by comparing the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the previous year to the same period in the current year. For 2026, the finalized COLA provides a moderate raise in the 2.7% to 2.8% range.

While any increase helps stabilize your household budget, you must meticulously evaluate your net raise. The government deducts your Medicare Part B premiums directly from your Social Security check before the money hits your bank account. Because Part B premiums typically rise each year alongside general healthcare costs, your actual take-home increase may feel smaller than the headline COLA percentage. You can verify your specific earnings limit and net benefit amount securely at the Social Security Administration (SSA) portal.

“Retirement is a shifting landscape. The most successful retirees are those who stay engaged with their finances and adapt to new tax laws and benefits as they arise.” — Jean Chatzky, Financial Editor

Pitfalls to Watch For

Even with highly favorable new regulations, costly mistakes lurk in the fine print. Protect your income by avoiding these common traps:

- Medicare IRMAA Surcharges: The Income-Related Monthly Adjustment Amount (IRMAA) uses a strict two-year lookback period. A massive spike in your taxable income during 2024—perhaps from a home sale or a large Roth conversion—will artificially inflate your Medicare Part B and Part D premiums in 2026. If your income has since dropped due to a life-changing event like retirement, file Form SSA-44 immediately to appeal the surcharge.

- Misunderstanding the Roth Mandate: High earners who fail to switch their catch-up contributions to Roth could face administrative headaches. Ensure your payroll system reflects the $150,000 threshold rule so you do not accidentally overcontribute pre-tax dollars.

- Ignoring Plan Formularies: Even with the new $2,100 cap and historic negotiated drug prices, your specific medication must remain on your plan’s approved list (formulary) for the cap to apply. Part D providers change their formularies every single year. Always review your Annual Notice of Change letter during Open Enrollment. The National Council on Aging (NCOA) provides excellent resources for understanding these annual shifts.

Getting Expert Help

Navigating these sweeping 2026 changes requires precision. Consider working with a credentialed fiduciary professional in these specific scenarios:

- Strategic Tax Planning: A Certified Public Accountant (CPA) can help you stack the new $6,000 senior deduction with your standard age-based deductions. They can also optimize your IRA withdrawal sequence to keep your Social Security benefits tax-free.

- Healthcare Choices: Utilize the State Health Insurance Assistance Program (SHIP). They provide free, unbiased, one-on-one counseling to help you compare Part D plans, verify your formulary coverage, and opt into the payment smoothing program.

- Wealth Management: A fee-only financial planner can optimize your super catch-up contributions, build a tax-efficient RMD strategy, and run projections to help you avoid future IRMAA cliffs.

Frequently Asked Questions

Does the $2,100 Medicare out-of-pocket cap apply to all prescriptions?

No. The $2,100 out-of-pocket limit applies exclusively to covered Part D formulary drugs. It does not apply to Part B drugs administered in an outpatient hospital setting, over-the-counter supplements, or any medications specifically excluded from your insurance plan’s formulary list.

How do I claim the new $6,000 senior tax deduction?

You claim this deduction when filing your 2026 federal income tax return in early 2027. You must meet the age requirement of 65 or older by the end of the tax year and fall below the income phase-out thresholds—$75,000 for single filers and $150,000 for joint filers.

Do I have to pay taxes on my Social Security in 2026?

It depends entirely on your combined income. The IRS taxes up to 85% of your Social Security benefits if your combined income exceeds certain thresholds. However, the significantly higher standard deductions implemented for seniors in 2026 allow many middle-income retirees to offset this taxable portion entirely, resulting in a net-zero federal tax bill.

Take Control of Your 2026 Benefits

The rules governing your retirement income underwent a massive overhaul this year. By proactively adapting your strategy to leverage the $2,100 Medicare cap, the new senior tax deductions, and the expanded contribution limits, you establish a fortified financial foundation. Review your tax withholding, double-check your Medicare formulary, and consult with your advisory team to ensure you extract maximum value from these newly implemented government programs.

Last updated: February 2026. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.