Your Social Security check is not a static number, and you can expect your monthly payout to look different when 2027 arrives. Whether your benefit grows or shrinks depends on a complex mix of economic shifts, tax laws, and your personal financial decisions over the next twelve months. While annual cost-of-living adjustments naturally push your gross benefit higher, rising Medicare premiums and rigid tax thresholds often offset those gains before the money ever hits your bank account. By understanding the specific triggers that alter your benefit amount, you can adjust your retirement income strategy now and avoid unexpected cash flow shortages in the year ahead.

1. The 2027 Cost-of-Living Adjustment (COLA)

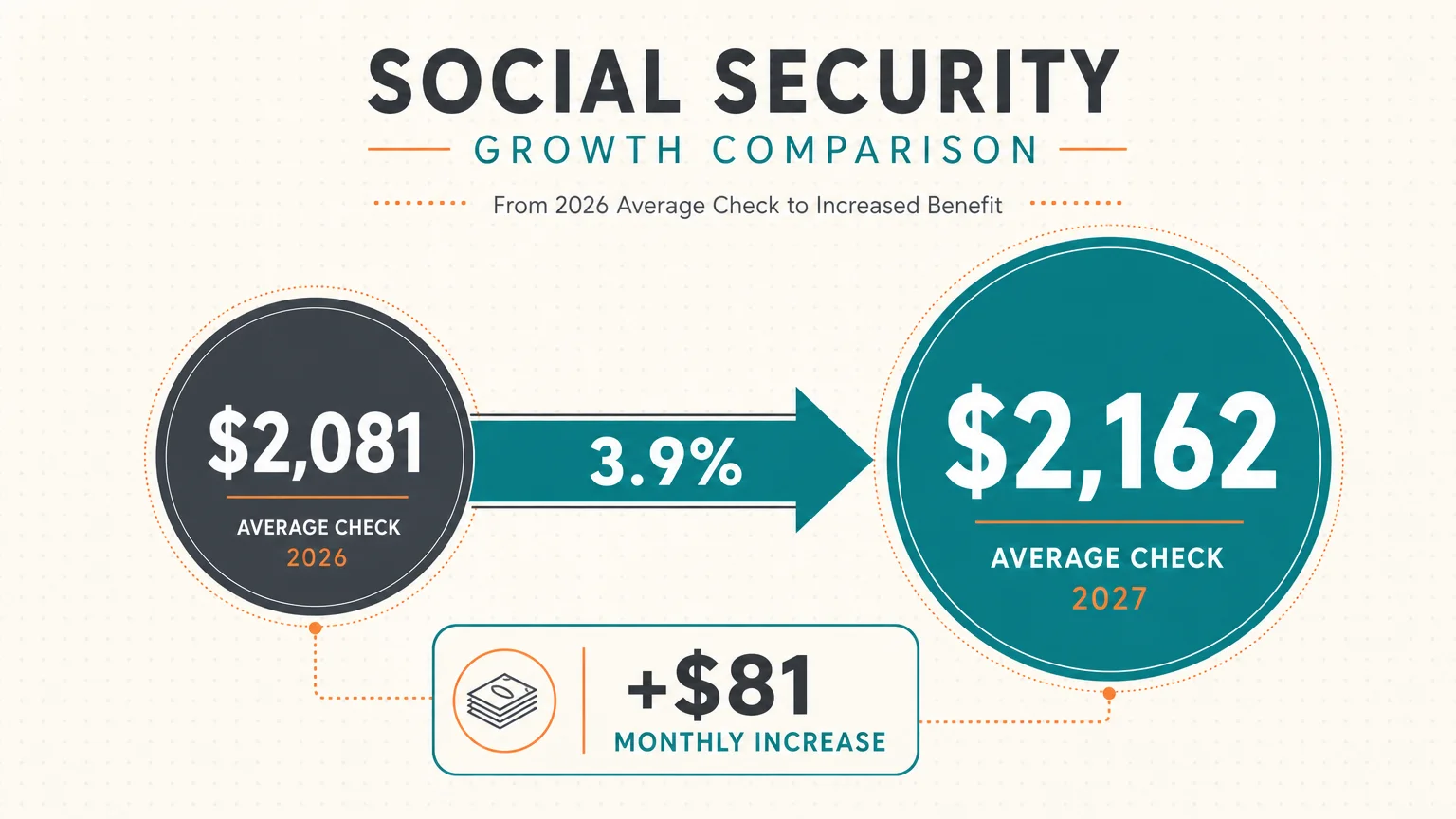

The most common reason your Social Security payment will change in 2027 is the annual Cost-of-Living Adjustment (COLA). The Social Security Administration (SSA) implements this adjustment to ensure your purchasing power keeps pace with inflation. In 2026, beneficiaries received a 2.8 percent increase, which raised the average retirement check to approximately $2,081 per month by the spring of that year.

For 2027, the adjustment is already shaping up to be higher than previous estimates. Due to stubborn inflation rates—particularly driven by energy, gasoline, and housing costs—recent projections indicate the 2027 COLA could reach 3.9 percent. If this projection holds true, the average retired worker could see a monthly increase of around $81.

Keep in mind that the official COLA for 2027 will not be locked in until October 2026. The SSA calculates the exact percentage by comparing the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the current year against the third quarter of the previous year. While a larger gross check feels like a win, it is vital to remember that this extra income is intended to cover the higher prices you are already paying for daily essentials.

2. Medicare Part B Premium Hikes

For the vast majority of retirees, Medicare Part B premiums are deducted directly from their Social Security checks. Because of this automatic deduction, your net Social Security payment is heavily dependent on Medicare costs. If Medicare premiums rise faster than your COLA, your effective raise could be entirely wiped out.

In 2026, the standard Medicare Part B premium increased to $202.90 per month. Historically, healthcare costs rise at a faster pace than general inflation. This means Medicare premiums often take a disproportionate bite out of annual Social Security increases. When you view your 2027 Social Security statement, you must factor in the updated Part B premiums to understand your actual cash flow.

There is a protective measure in place called the hold harmless provision. This rule ensures that your Medicare Part B premium increase cannot be larger than the dollar amount of your Social Security COLA. It prevents your actual check amount from dropping from one year to the next strictly due to standard Medicare hikes. However, the hold harmless rule does not protect everyone. If you are subject to high-income surcharges or if you are newly enrolling in Medicare, you will bear the full brunt of 2027 premium increases.

3. Navigating the Retirement Earnings Test

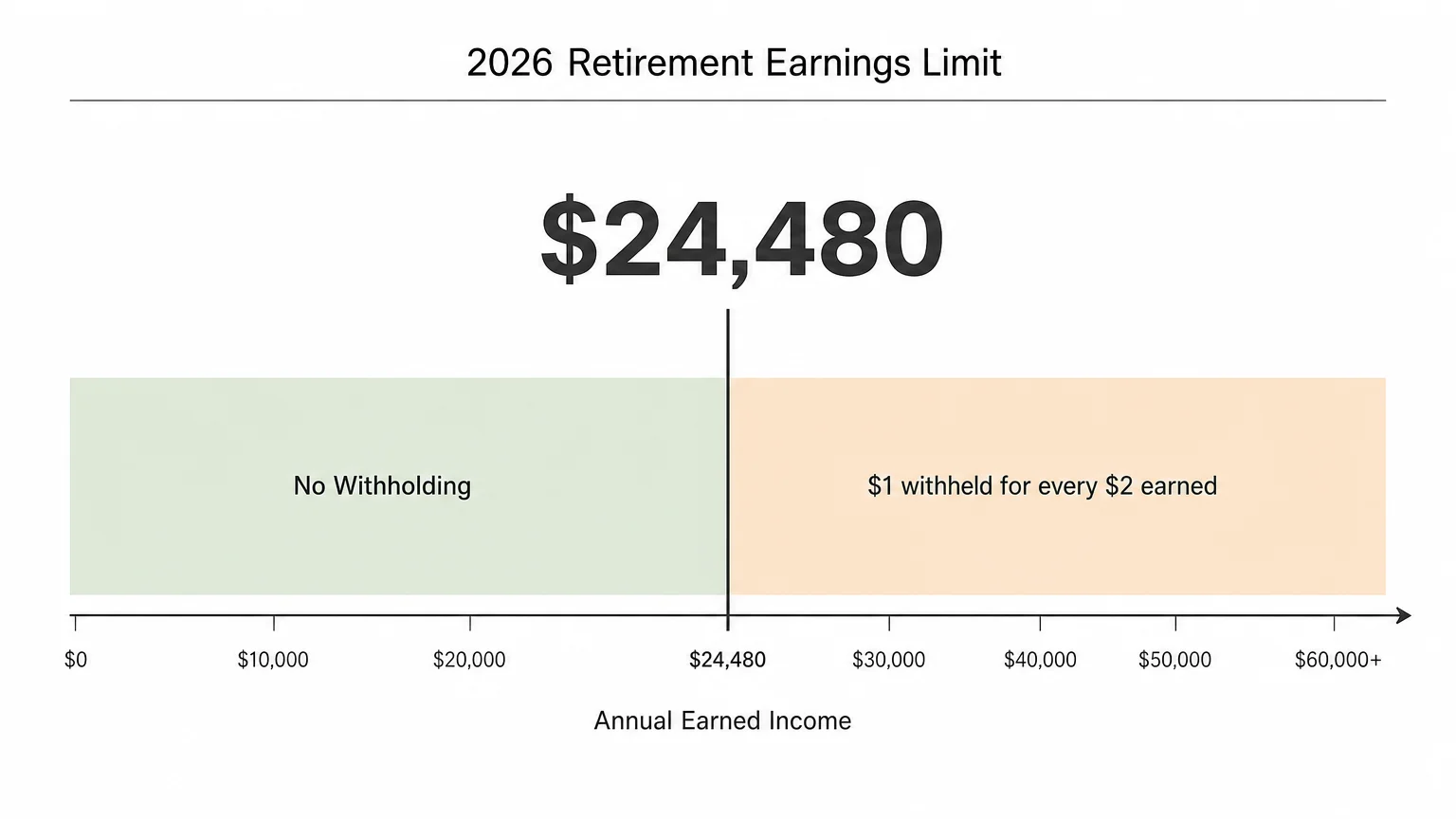

If you claim Social Security before reaching your Full Retirement Age (FRA) and continue to work, your benefits are subject to the Retirement Earnings Test. The SSA caps the amount of money you can earn from a job before they start withholding your benefits.

In 2026, the earnings limit was $24,480 if you were under your FRA for the entire year. For every $2 you earned above that threshold, the SSA withheld $1 from your benefit. The SSA adjusts this earnings limit annually based on national average wage trends. When the 2027 limit is announced, it will likely be higher, giving you more room to earn income without triggering a temporary reduction in your checks.

For example, if the limit rises in 2027 and you maintain the same part-time salary you had in 2026, you might find that less of your benefit is withheld. It is crucial to understand that this limit only applies to earned income from a W-2 job or net self-employment earnings. Investment income, pensions, annuities, and capital gains do not count toward the Retirement Earnings Test. If you plan to work part-time in 2027, monitor your wages closely to anticipate any withholding.

4. Reaching Full Retirement Age (FRA)

Your Social Security payout will change dramatically in the year you reach your Full Retirement Age. Depending on your birth year, your FRA falls between 66 and 67. If 2027 is the year you hit this milestone, two major shifts will occur to your monthly payout.

First, the restrictive earnings test relaxes significantly. In the months leading up to your FRA birthday, the earnings limit is much higher. In 2026, individuals reaching FRA were allowed to earn up to $65,160 in the months prior to their birthday, with only $1 withheld for every $3 earned above the limit. Once your birth month arrives, the earnings test disappears completely. You can earn as much as you want, and the SSA will no longer withhold any portion of your benefit.

Second, if you had benefits withheld in previous years due to the earnings test, the SSA will automatically recalculate your monthly payment. They adjust your payout formula to give you credit for the months you did not receive a full check. This recalculation results in a higher monthly payout going forward, meaning your 2027 checks could see a substantial and permanent boost.

5. Triggering Medicare IRMAA Surcharges

High-income retirees face an additional reduction to their Social Security checks through the Income-Related Monthly Adjustment Amount, commonly known as IRMAA. If your income crosses specific thresholds, Medicare charges you a surcharge on both your Part B and Part D premiums. You can review detailed Medicare surcharge information directly at Medicare.gov.

IRMAA operates on a two-year lookback period. This means your 2027 Medicare premiums—and subsequently, your 2027 net Social Security check—will be determined by the income you reported on your 2025 tax return. The IRMAA system uses a cliff bracket structure. If your Modified Adjusted Gross Income (MAGI) exceeds a threshold by even one single dollar, you are pushed into the higher premium tier for the entire year.

To understand how these cliffs function, consider the verified brackets used for 2026 (which were based on 2024 income):

| Individual Filer MAGI | Joint Filer MAGI | Monthly Part B Premium (2026) |

|---|---|---|

| $109,000 or less | $218,000 or less | $202.90 |

| $109,001 to $137,000 | $218,001 to $274,000 | $284.10 |

| $137,001 to $171,000 | $274,001 to $342,000 | $405.80 |

| $171,001 to $205,000 | $342,001 to $410,000 | $527.50 |

| $205,001 to $499,999 | $410,001 to $749,999 | $649.20 |

| $500,000 or more | $750,000 or more | $689.80 |

If you sold real estate, executed large Roth conversions, or took substantial Required Minimum Distributions (RMDs) in 2025, that income spike could trigger IRMAA surcharges in 2027. This will automatically shrink your net Social Security deposit.

6. Crossing Taxation Thresholds

Your Social Security benefits are not entirely tax-free. Depending on your “combined income” (your adjusted gross income plus nontaxable interest plus half of your Social Security benefits), you could owe federal income tax on up to 85 percent of your payout.

The federal thresholds that trigger these taxes have not been adjusted for inflation since they were introduced decades ago. Familiarize yourself with these fixed guidelines available through the IRS:

- Single Filers: Combined income between $25,000 and $34,000 makes up to 50 percent of benefits taxable. Income over $34,000 makes up to 85 percent taxable.

- Joint Filers: Combined income between $32,000 and $44,000 makes up to 50 percent of benefits taxable. Income over $44,000 makes up to 85 percent taxable.

Because these thresholds do not rise with inflation, the annual COLA organically pushes more retirees into these taxable brackets every single year. A projected 3.9 percent COLA in 2027 might be exactly what pushes your combined income over the $32,000 or $44,000 mark. When this happens, you may need to adjust your Form W-4V to have federal taxes withheld directly from your Social Security check, which lowers your net monthly payment.

“Taxes will be the single biggest factor that separates people from their retirement dreams.” — Ed Slott, CPA and IRA Distribution Expert

7. Replacing a Low-Earning Year on Your Record

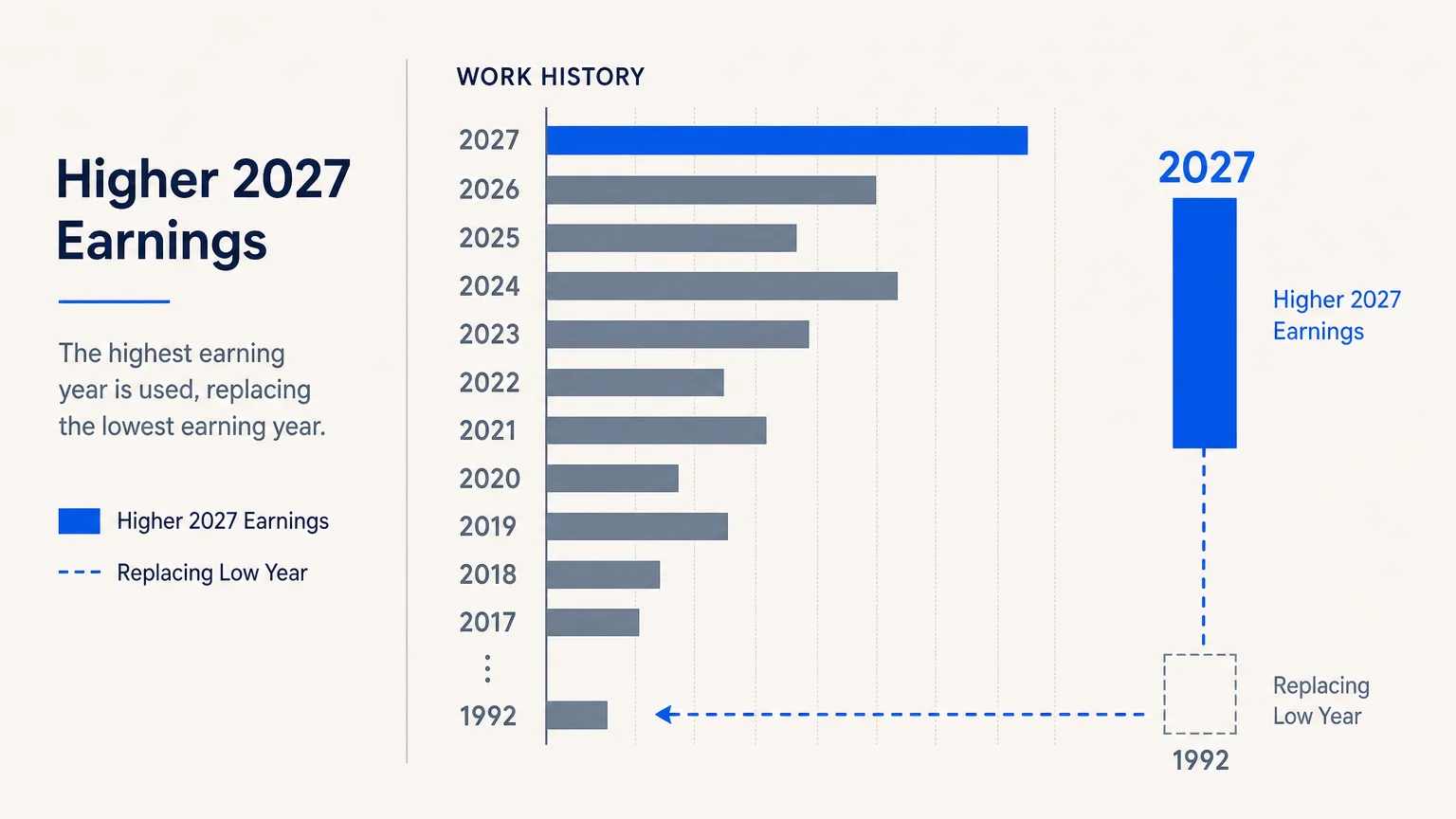

The SSA calculates your primary insurance amount based on your Average Indexed Monthly Earnings (AIME) over your 35 highest-earning years. If you do not have a full 35 years of work history, the SSA fills the missing years with zeros, which drags down your lifetime average.

If you continue to work while collecting benefits in 2026 or 2027, you are still paying Social Security payroll taxes. The SSA reviews your earnings record every year. If your current earnings are higher than one of the lowest years currently used in your calculation—or if your current earnings replace a zero year entirely—the SSA automatically recalculates your benefit.

This recalculation always works in your favor. If your recent work history boosts your 35-year average, you will see a permanent, automatic increase in your Social Security check. You do not need to file any special paperwork to receive this bump; the SSA processes it automatically when your earnings are reported.

8. Navigating Life Events: Spousal and Survivor Benefits

Major life events directly impact how the SSA calculates and distributes your benefits. If your marital status changes in late 2026 or 2027, your payment will likely change as well.

If a spouse passes away, the surviving spouse is eligible to inherit the deceased partner’s benefit, provided it is larger than their own. You cannot collect both your own retirement benefit and a survivor benefit simultaneously; the SSA pays the higher of the two amounts. Stepping up to a higher survivor benefit can significantly increase your monthly check.

Divorce can also trigger benefit changes. If your marriage lasted at least 10 years and you are currently unmarried, you may be eligible to claim benefits based on your ex-spouse’s earnings record. If your ex-spouse’s record yields a higher payout than your own work history, coordinating this transition will alter your 2027 payments.

Avoiding Common Errors with Your Social Security Check

Many retirees leave money on the table or face unexpected cash flow issues due to simple misunderstandings of the Social Security system. To protect your income in 2027, avoid these common missteps:

- Assuming the Earnings Test is a Permanent Tax: When the SSA withholds benefits because you earned too much before your FRA, that money is not lost forever. It is credited back to you through higher monthly payments once you reach Full Retirement Age. Do not turn down a lucrative work opportunity simply because you fear the earnings test.

- Ignoring State Taxes: While federal tax rules apply universally, state taxation of Social Security varies wildly. Several states still tax Social Security benefits based on varying income brackets. Verify your state’s current tax laws, as relocating or crossing a state income threshold can change your net benefit.

- Forgetting to Appeal IRMAA: If you receive an IRMAA notice for 2027 based on your 2025 income, you do not always have to accept the premium hike. If you experienced a qualifying life-changing event—such as retiring, losing a pension, or divorce—you can file Form SSA-44 to request a reduction in your Medicare premiums based on your current, lower income.

When DIY Isn’t Enough

While basic Social Security claims are straightforward, certain situations require the expertise of a qualified financial planner or tax advisor. According to the National Council on Aging (NCOA), integrating Social Security with other income streams is a major hurdle for older adults. Consider seeking professional guidance if you fall into any of the following categories:

You Are Coordinating Spousal Benefits with a Large Age Gap: Maximizing lifetime income for a married couple often requires strategic timing. An advisor can run break-even analyses to determine exactly when the higher earner should claim benefits to maximize the surviving spouse’s future income.

You Receive a Pension from Non-Covered Work: If you receive a pension from a job that did not withhold Social Security taxes—such as certain teaching, railroad, or government positions—your Social Security benefits may be heavily reduced by the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO). Calculating these reductions accurately is complex and requires specialized planning.

You Are Managing Large IRA Withdrawals: Coordinating your Social Security claiming strategy with your Required Minimum Distributions (RMDs) is critical. A tax professional can help you sequence your withdrawals, implement Roth conversions, and manage your tax brackets to prevent your Social Security benefits from being needlessly taxed.

“With fewer pensions, Social Security uncertainty and people living longer, it’s time to rethink how retirees transition from saving to spending. The new paradigm calls for a greater focus on guaranteed lifetime income.” — Jean Chatzky, Personal Finance Expert

Frequently Asked Questions

Can my Social Security benefit ever go down?

Your gross Social Security benefit will not decrease. However, your net payment—the amount actually deposited into your bank account—can go down if your Medicare Part B or Part D premiums increase significantly, or if you request a higher percentage of federal tax withholding.

What is the hold harmless rule?

The hold harmless provision is a federal rule ensuring that standard Medicare Part B premium increases do not reduce your net Social Security check. If the Medicare premium increase is larger than your annual COLA, your Part B premium hike is capped so your Social Security payment remains flat. Keep in mind, this rule does not apply to IRMAA surcharges.

Will the Windfall Elimination Provision (WEP) affect my 2027 check?

The WEP only affects your benefit if you worked in a job where you did not pay Social Security taxes and you also qualified for Social Security through other employment. If you are already receiving a reduced benefit due to WEP, that reduction will continue in 2027, though your remaining benefit will still receive the annual COLA.

How do I prepare for the 2027 COLA announcement?

The SSA typically announces the official COLA in mid-October. You can monitor inflation trends through the summer, but the best preparation is to review your current budget, anticipate potential Medicare increases, and consult with a tax professional regarding your federal withholding strategy.

Every year brings subtle shifts to retirement income, and 2027 will be no exception. By actively monitoring your earnings, adjusting for inflation, and planning for Medicare premiums, you can take control of your cash flow and secure a more comfortable lifestyle. Take the time now to review your online Social Security statement, verify your earnings record, and coordinate your broader retirement strategy.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.