Finding a retirement haven that balances affordability, lifestyle, and healthcare access feels increasingly impossible as major relocation hubs see their real estate values skyrocket. You do not have to sacrifice financial security to enjoy a fulfilling retirement if you know where to look.

Across the country, smaller communities are quietly offering the amenities of much larger cities, including walkable downtowns, outdoor recreation, and top-tier medical facilities, at a fraction of the cost.

However, the secret is getting out, and housing markets in these hidden gems are steadily heating up. Moving sooner rather than later can lock in your living costs. Here are seven small towns you should consider relocating to before their home prices spike completely out of reach.

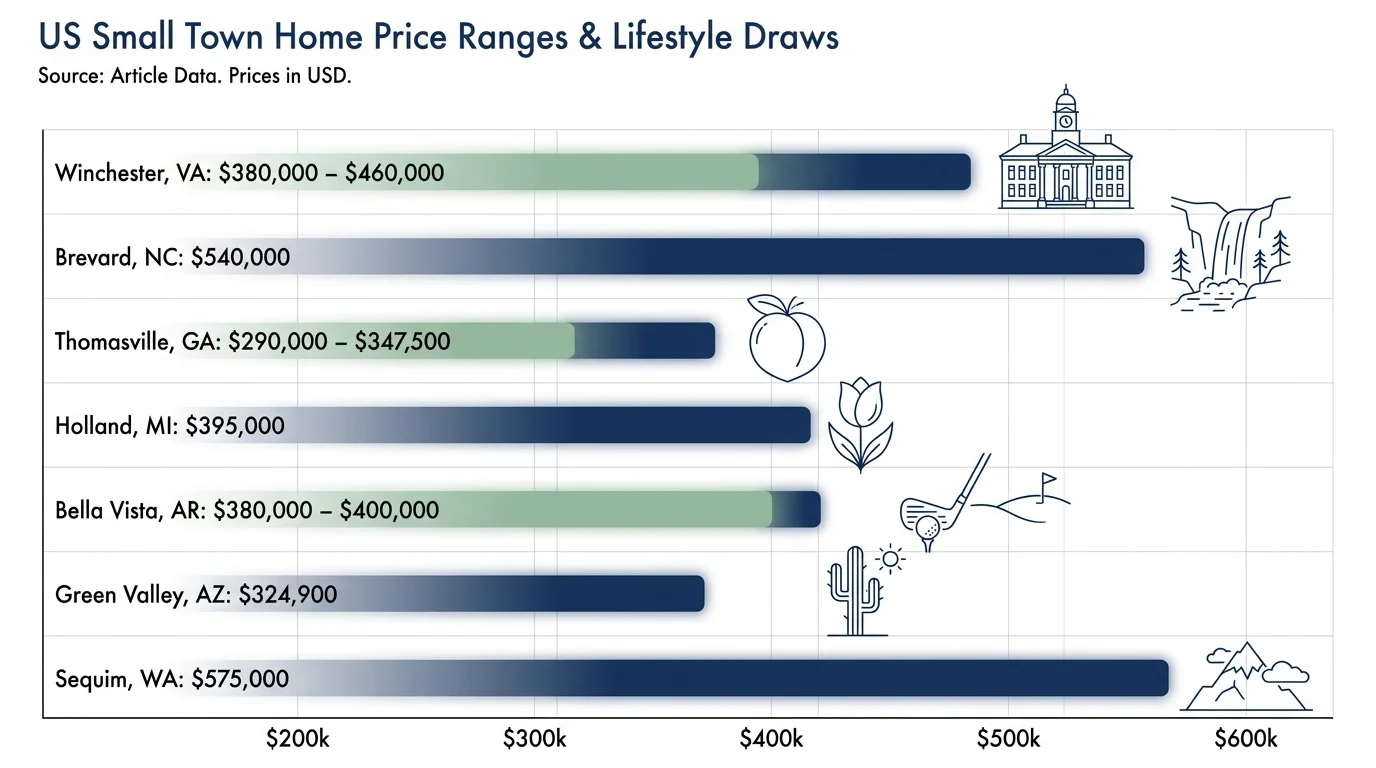

At a Glance: The 7 Rising Retirement Towns

If you want a quick overview of the housing markets across these desirable locations, review this comparison of median home prices and primary lifestyle draws. All housing data reflects market conditions as of early 2026.

| Retirement Town | Median Home Price (2026) | Primary Lifestyle Draw |

|---|---|---|

| Winchester, VA | $380,000 – $460,000 | Historic downtown, commuter-friendly, Shenandoah Valley views |

| Brevard, NC | $540,000 | Mountain trails, hundreds of waterfalls, moderate climate |

| Thomasville, GA | $290,000 – $347,500 | Southern charm, warm winters, extremely tax-friendly |

| Holland, MI | $395,000 | Lake Michigan beaches, local festivals, slower pace |

| Bella Vista, AR | $380,000 – $400,000 | Wooded trails, golf courses, Ozark mountain lakes |

| Green Valley, AZ | $324,900 | Active adult communities, cooler desert elevation, golf |

| Sequim, WA | $575,000 | Coastal mountains, low rainfall, no state income tax |