Your Social Security check is not a static number, and you can expect your monthly payout to look different when 2027 arrives. Whether your benefit grows or shrinks depends on a complex mix of economic shifts, tax laws, and your personal financial decisions over the next twelve months.

While annual cost-of-living adjustments naturally push your gross benefit higher, rising Medicare premiums and rigid tax thresholds often offset those gains before the money ever hits your bank account.

By understanding the specific triggers that alter your benefit amount, you can adjust your retirement income strategy now and avoid unexpected cash flow shortages in the year ahead.

1. The 2027 Cost-of-Living Adjustment (COLA)

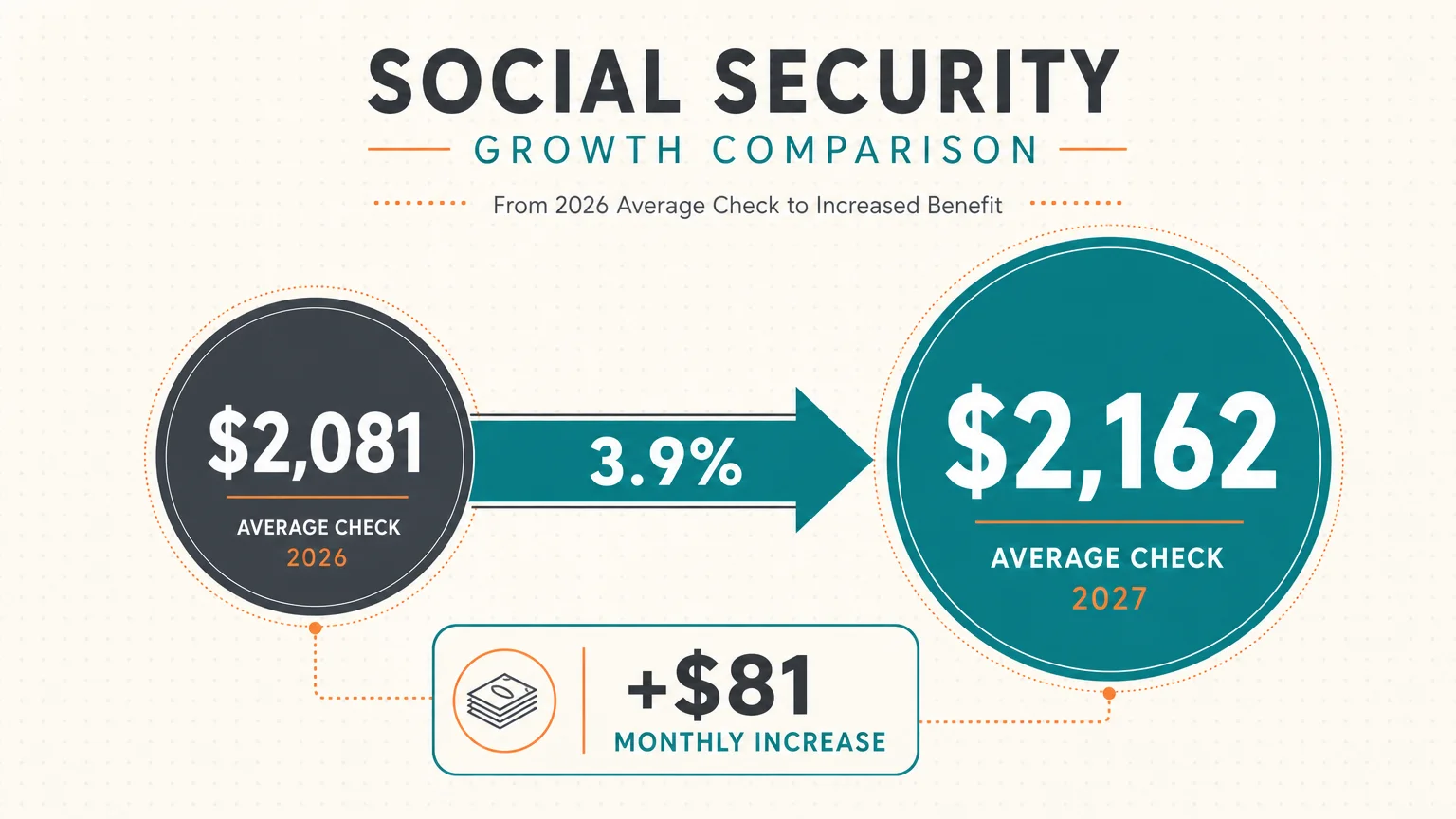

The most common reason your Social Security payment will change in 2027 is the annual Cost-of-Living Adjustment (COLA). The Social Security Administration (SSA) implements this adjustment to ensure your purchasing power keeps pace with inflation. In 2026, beneficiaries received a 2.8 percent increase, which raised the average retirement check to approximately $2,081 per month by the spring of that year.

For 2027, the adjustment is already shaping up to be higher than previous estimates. Due to stubborn inflation rates—particularly driven by energy, gasoline, and housing costs—recent projections indicate the 2027 COLA could reach 3.9 percent. If this projection holds true, the average retired worker could see a monthly increase of around $81.

Keep in mind that the official COLA for 2027 will not be locked in until October 2026. The SSA calculates the exact percentage by comparing the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the current year against the third quarter of the previous year. While a larger gross check feels like a win, it is vital to remember that this extra income is intended to cover the higher prices you are already paying for daily essentials.