3. Navigating the Retirement Earnings Test

If you claim Social Security before reaching your Full Retirement Age (FRA) and continue to work, your benefits are subject to the Retirement Earnings Test. The SSA caps the amount of money you can earn from a job before they start withholding your benefits.

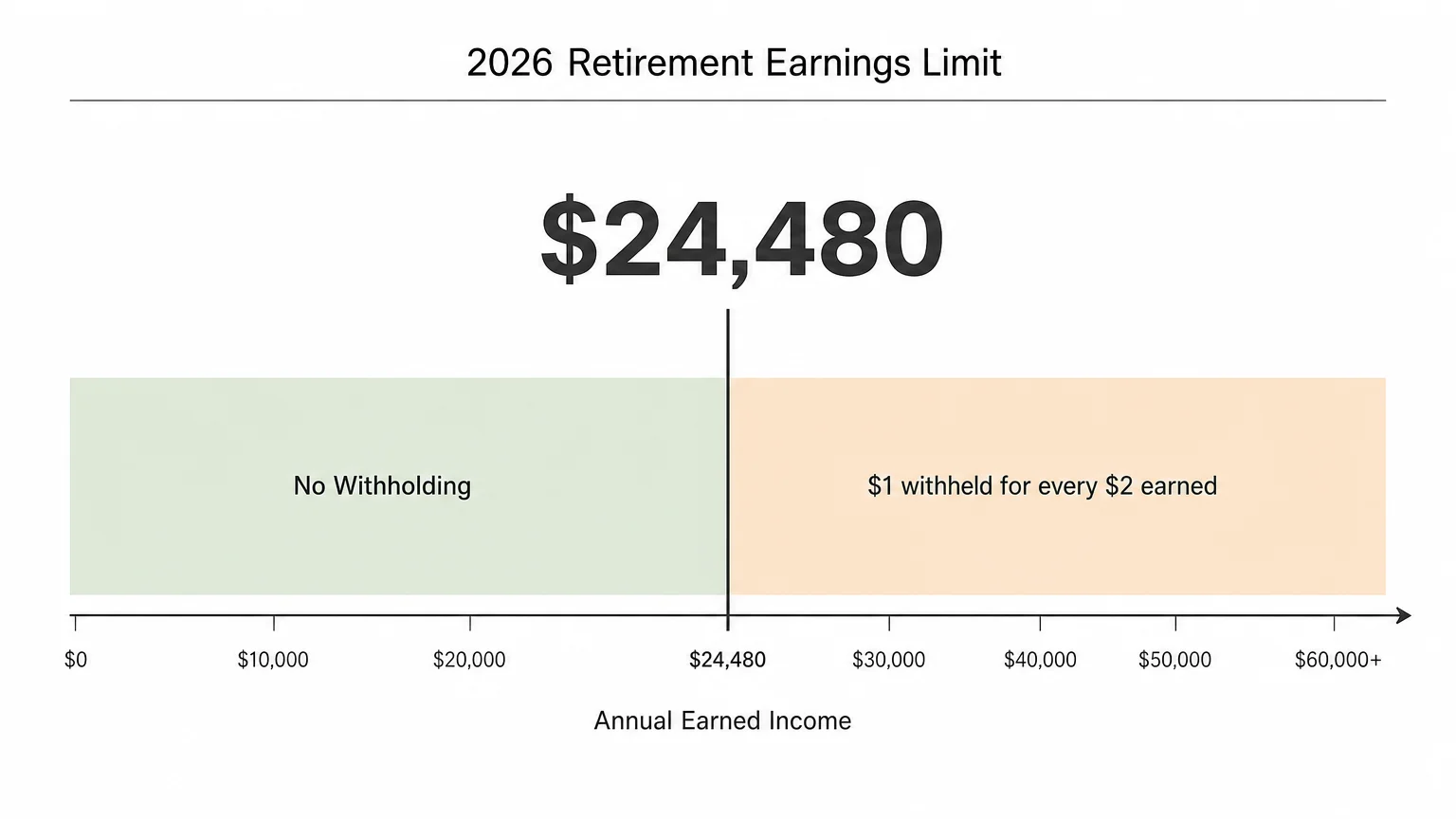

In 2026, the earnings limit was $24,480 if you were under your FRA for the entire year. For every $2 you earned above that threshold, the SSA withheld $1 from your benefit. The SSA adjusts this earnings limit annually based on national average wage trends. When the 2027 limit is announced, it will likely be higher, giving you more room to earn income without triggering a temporary reduction in your checks.

For example, if the limit rises in 2027 and you maintain the same part-time salary you had in 2026, you might find that less of your benefit is withheld. It is crucial to understand that this limit only applies to earned income from a W-2 job or net self-employment earnings. Investment income, pensions, annuities, and capital gains do not count toward the Retirement Earnings Test. If you plan to work part-time in 2027, monitor your wages closely to anticipate any withholding.