Finding the right balance of purpose, income, and freedom is the ultimate goal when transitioning out of a full-time career. A flexible part-time job allows you to boost cash flow, stay socially engaged, and maintain mental sharpness without sacrificing the leisure time you worked decades to earn. A 2026 AARP survey reveals that many older adults are returning to the workforce to combat high living costs, but they are doing it entirely on their own terms. Setting your own schedule means you can still travel, visit family, and pursue hobbies while generating meaningful income. Whether you want to leverage your professional expertise or try something new, the modern gig economy offers countless opportunities designed for your lifestyle.

The Rise of the Flexible Retiree

Retirement no longer represents a sharp cliff where you immediately drop from working forty hours a week to zero. Instead, a phased approach to retirement has become the new normal. Working a job that lets you dictate your own hours provides a crucial financial buffer against inflation and market volatility, allowing you to withdraw less from your retirement accounts during down years.

Furthermore, the psychological benefits of working on your own terms are profound. Staying engaged in the workforce provides a built-in social network, a structured reason to get out of the house, and a continuous sense of achievement. By focusing exclusively on roles that offer schedule autonomy, you eliminate the stress of asking a boss for time off. If you want to spend the entire month of February in a warmer climate, a flexible job allows you to simply pause your work and resume when you return.

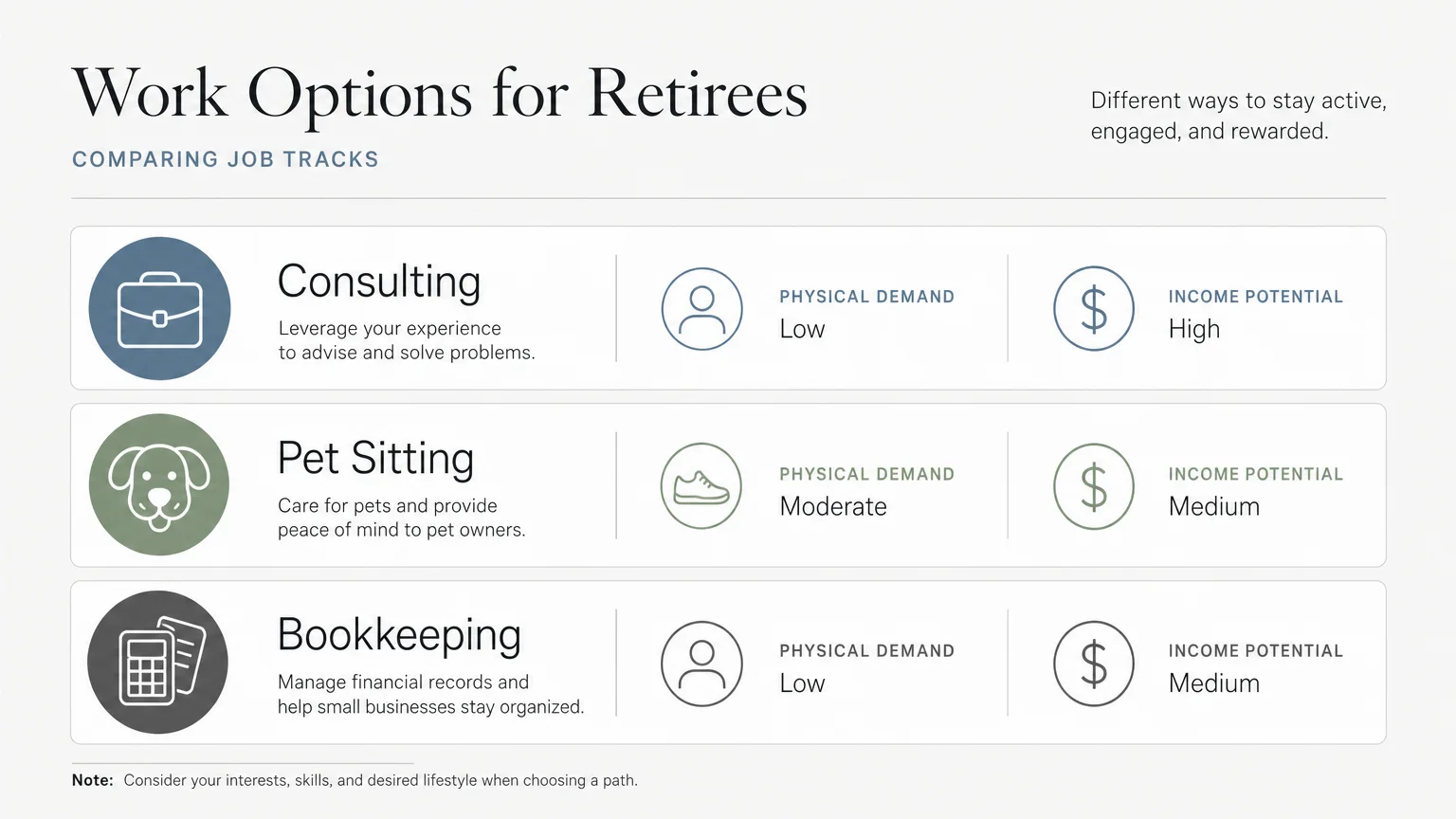

Quick Summary: Comparing Your Options

Before diving into the specifics of each role, review this high-level comparison to see which opportunities align best with your physical preferences and income goals.

| Job Role | Primary Benefit | Physical Demand | Income Potential |

|---|---|---|---|

| Freelance Consulting | High hourly rates | Low (Desk work) | High |

| Pet Sitting / Dog Walking | Built-in exercise | Moderate to High | Medium |

| Bookkeeping / Virtual Assistant | Work from anywhere | Low (Computer work) | Medium |

| Substitute Teaching | Say “no” whenever you want | Moderate (Standing/Walking) | Medium |

| Rideshare / Delivery | Instant schedule control | Low (Driving) | Low to Medium |

| Local Tour Guiding | Highly social environment | High (Walking) | Medium |

| Mock Juror / Focus Group | No commitment required | Low (Online/Seated) | Low |

| Real Estate Notary | Professional independent work | Low (Driving to clients) | Medium to High |

1. Freelance Consulting and Coaching

If you spent decades mastering a specific industry, you possess institutional knowledge that businesses desperately need. Consulting allows you to package your expertise and sell it back to your former industry—or to younger professionals—without committing to a grueling corporate schedule.

You dictate how many clients you accept and which months you want to work. Many retirees find success by returning to their former employers as independent contractors, handling specialized projects that require deep experience. Others pivot to executive coaching, helping mid-level managers navigate leadership challenges.

“The best investment you can make is an investment in yourself. The more you learn, the more you’ll earn.” — Warren Buffett

To get started, establish a simple LLC, update your LinkedIn profile, and reach out to your existing professional network. Because you provide high-level strategic value, you can often charge premium hourly rates, meaning you only need a few hours of work a week to generate significant supplemental income.

2. Pet Sitting and Dog Walking

For retirees looking to stay active, pet care represents the perfect blend of physical exercise, companionship, and income. Platforms like Rover and Wag! allow you to create an online profile, set your own rates, and explicitly define your availability calendar.

If you plan to visit your grandchildren for two weeks, you simply block out those dates on your calendar. You also have the power to accept or decline specific breeds and sizes, ensuring you never take on a pet that is too difficult to handle. Many retirees eventually transition off the apps and build a private clientele of neighbors and friends, which eliminates platform fees and fosters deep community trust.

3. Bookkeeping and Virtual Assistance

Small business owners frequently outsource their administrative, scheduling, and financial tasks because they cannot afford full-time employees. If you are detail-oriented, highly organized, and comfortable with basic software, offering virtual support provides exceptional schedule control.

Bookkeeping, in particular, is highly lucrative for retirees. You do not need to be a Certified Public Accountant (CPA) to manage daily ledgers, reconcile bank statements, or run payroll. Getting certified in a program like QuickBooks Online takes only a few weeks. The work is strictly deadline-driven rather than hours-driven; as long as the accounts are reconciled by the end of the month, you can do the actual work at six in the morning or late at night.

4. Substitute Teaching and Tutoring

School districts across the country constantly seek reliable substitute teachers. The greatest advantage of this role is the absolute freedom to accept or decline work on a daily basis. District automated systems allow you to wake up, check available assignments on your phone, and decide if you feel like working.

Requirements vary heavily by state—some require a bachelor’s degree and a teaching license, while others require only a high school diploma and a clean background check. If classroom management sounds unappealing, consider private tutoring. Online tutoring platforms let you set specific available hours to teach subjects you love, from high school algebra to conversational English for international students.

5. Rideshare and Delivery Driving

The app-based driving economy offers the purest form of schedule control available today. You can log into the Uber, Lyft, or DoorDash app precisely when you want to earn money, and log out the second you decide to go home. There are no minimum hour requirements and no shifts to schedule in advance.

While the flexibility is unmatched, you must treat this work like a small business. Track your mileage meticulously for tax deductions, account for accelerated vehicle wear and tear, and contact your auto insurance provider to secure a rideshare endorsement policy. Driving during peak hours—like morning airport runs or weekend dinner rushes—maximizes your hourly earnings while minimizing the time spent behind the wheel.

6. Local Tour Guiding

If you live in a city with historical significance, a vibrant food scene, or cultural landmarks, working as a local tour guide is a highly engaging way to earn extra money. Tour companies frequently hire part-time guides to manage overflow during peak tourist seasons or to work exclusively on weekends.

This job keeps you physically active and allows you to share your passion for your hometown with visitors from around the world. Because the work is often seasonal or strictly scheduled around specific tour times, you can easily mold it around your personal life. Keep in mind that some major cities require tour guides to pass a local history exam and carry a municipal license.

“A (1) diverse (2) group (3) of (4) participants (5) sits (6) around (7) a (8) table, (9) deliberating (10) during (11) a (12) mock (13) jury (14) session. (15)” – 1

7. Mock Juror and Focus Group Participant

Trial attorneys frequently test their case strategies on mock juries before stepping into a real courtroom. They need diverse demographic groups to read case summaries, view evidence, and provide feedback on their arguments. Similarly, market research firms constantly pay for consumer opinions on new products, website designs, and advertising campaigns.

Platforms like eJury or specialized focus group agencies allow you to participate in these panels from your living room. The work is entirely ad-hoc. You receive an email invitation, review the compensation and time requirement, and decide if you want to participate. While it will not replace a full-time salary, it provides an interesting, low-effort stream of extra cash.

8. Real Estate Notary and Signing Agent

Becoming a commissioned notary public and a certified loan signing agent requires a small upfront investment in state licensing, background checks, and training. However, it pays off by providing extreme flexibility and professional-level compensation.

Title companies, escrow officers, and real estate agencies rely on mobile notaries to guide buyers and sellers through massive stacks of mortgage documents. As an independent signing agent, you receive text messages or emails offering a specific signing at a specific time and location. If the appointment fits your schedule, you accept it. If you are busy, you simply decline.

How Part-Time Work Impacts Social Security and Taxes

Generating income during retirement requires careful coordination with your existing benefits and tax strategies. Earning money from a gig does not exist in a vacuum; it directly impacts how the federal government views your total financial picture.

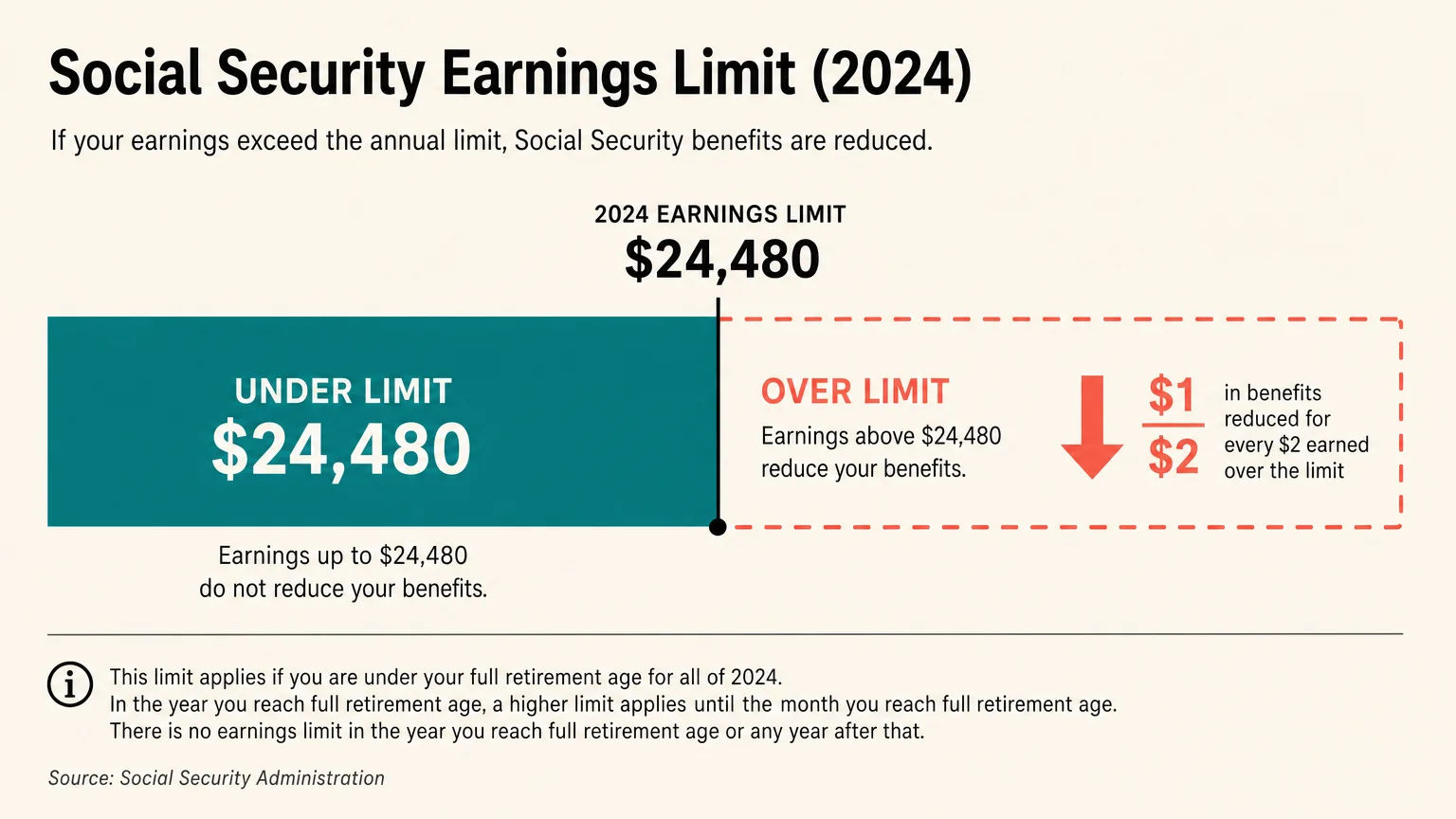

Social Security Earnings Limits

If you claim Social Security benefits before reaching your Full Retirement Age (FRA) and continue to work, you are subject to the annual earnings test. According to the Social Security Administration, the earnings limit for 2026 is $24,480. If you earn more than this amount, the SSA will withhold $1 in benefits for every $2 you earn over the limit.

There is a special rule for the specific year you reach your FRA. In 2026, the limit jumps to $65,160 for the months prior to your birth month, and the withholding penalty softens to $1 for every $3 over the limit. The moment you reach your Full Retirement Age, the earnings limit disappears completely. From that month forward, you can earn as much gig income as you desire without any reduction to your Social Security checks.

The 2026 Tax Landscape for Retirees

Adding part-time income to your Social Security, pensions, and required minimum distributions (RMDs) could push you into a higher tax bracket. However, older adults benefit from generous deductions that shield a significant portion of this income.

For the 2026 tax year, the IRS set the baseline standard deduction for a single filer at $16,100, plus an additional $2,050 for being age 65 or older, bringing your total standard deduction to $18,150. Married couples filing jointly where both spouses are 65 or older enjoy a robust standard deduction of $35,500 ($32,200 base plus $3,300 in senior allowances). If your total taxable income falls below these thresholds, your federal income tax burden remains remarkably low.

What Can Go Wrong

Working flexible jobs almost always means working as an independent contractor (a 1099 worker) rather than a traditional W-2 employee. This classification brings unique responsibilities and risks.

- 1099 Tax Surprises: Because you are an independent contractor, clients and apps do not withhold taxes from your pay. You are responsible for both income tax and self-employment tax (Medicare and Social Security contributions). Failing to set aside 20 to 30 percent of your earnings for quarterly estimated taxes will result in a painful tax bill and potential underpayment penalties in April.

- Medicare Premium Surcharges: Medicare Part B and Part D premiums are tied to your Modified Adjusted Gross Income (MAGI) from two years prior. Earning a sudden spike of part-time income could push you over an Income-Related Monthly Adjustment Amount (IRMAA) threshold. If this happens, your monthly healthcare premiums will increase significantly. You can find current IRMAA brackets at Medicare.gov.

- Employment Scams: Fraudsters prey on older adults seeking flexible, work-from-home income. Be deeply skeptical of any opportunity that requires you to pay upfront fees for training, specialized software, or inventory. Legitimate clients pay you; you do not pay them. Resources from AARP and the National Council on Aging provide excellent tools for verifying legitimate remote work.

When to Consult a Professional

Even moderate amounts of gig income can create ripple effects throughout your broader retirement plan. Consider speaking with a fee-only fiduciary financial planner or a certified tax professional under these specific scenarios:

- You are trying to optimize your Social Security claiming strategy while balancing part-time income before your Full Retirement Age.

- You want to aggressively shelter your gig income from taxes by opening a Solo 401(k) or a Simplified Employee Pension (SEP) IRA.

- Your combined household income is approaching the threshold for Medicare IRMAA surcharges, and you need strategies to manage your MAGI.

Making Your Next Move

Choosing to work during retirement is a deeply personal decision that should enhance your lifestyle, not hinder it. Start small by dedicating just five to ten hours a week to a new endeavor. Test the waters, evaluate how the work impacts your physical energy, and adjust your schedule accordingly. The beauty of the modern gig economy is that you hold the power to pivot instantly if an opportunity no longer serves your needs.

As you explore these avenues, keep strict records of your earnings and business expenses. Treating your flexible job like a proper small business ensures you reap the maximum financial reward. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.