Rising prices can make even a generous pension feel inadequate, especially when the cost of living outpaces your fixed monthly income. As inflation continues to chip away at your purchasing power, relying solely on a fixed pension and Social Security could leave you financially vulnerable. The reality is that your retirement income must grow just to maintain your current lifestyle. By understanding how inflation, Social Security adjustments, and rising healthcare premiums interact, you can take control of your financial future. This guide breaks down the math behind your changing purchasing power and provides actionable strategies to protect your hard-earned money. You will discover how to evaluate your current income streams, offset rising expenses, and ensure your retirement funds stretch across decades.

The Hidden Impact of Inflation on Your Pension

Many Americans enter their golden years celebrating the security of a guaranteed corporate or government pension. A fixed monthly check provides tremendous peace of mind—until you factor in the relentless, compounding nature of inflation. If your pension lacks a built-in Cost-of-Living Adjustment (COLA), every passing year quietly reduces the actual amount of goods and services your check can buy.

Inflation acts as an invisible siphon on your wealth. For example, the U.S. inflation rate reached 3.8% in April 2026. While this sits lower than the historic peaks experienced earlier in the decade, compounding inflation—even at moderate levels—can completely reshape a fixed income over a twenty-year retirement window. When the cost of groceries, utility bills, homeowner’s insurance, and property taxes rises, a $3,000 monthly pension simply stops covering your baseline expenses. You are essentially taking an annual pay cut without ever looking at a smaller number on your bank statement.

“The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures. The inflation tax has a fantastic ability to simply consume capital.” — Warren Buffett, Chairman and CEO of Berkshire Hathaway

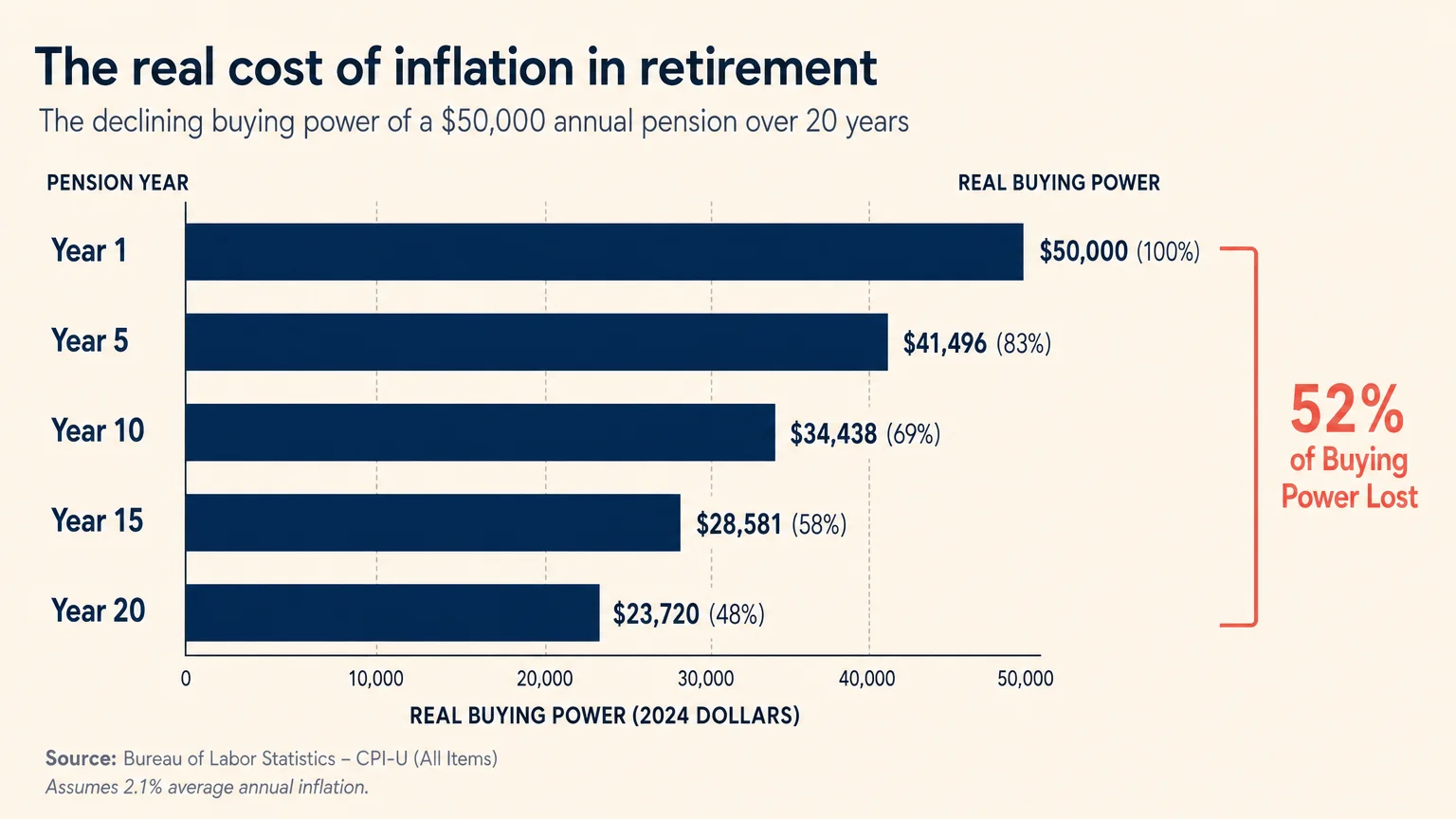

To grasp the true danger of relying heavily on fixed income, you must look at the arithmetic of purchasing power decay over an extended timeline. Consider a scenario where you retire with a fixed pension of $50,000 per year. If inflation averages an ongoing 3.8% annually, the real-world value of that income drops dramatically. The table below illustrates how much purchasing power you lose over various intervals.

| Years in Retirement | Nominal Pension Income | Real Purchasing Power (at 3.8% Annual Inflation) | Percentage of Buying Power Lost |

|---|---|---|---|

| Year 1 | $50,000 | $50,000 | 0% |

| Year 5 | $50,000 | $41,496 | 17% |

| Year 10 | $50,000 | $34,438 | 31% |

| Year 15 | $50,000 | $28,581 | 42% |

| Year 20 | $50,000 | $23,720 | 52% |

By year twenty, your $50,000 pension buys less than half of what it did on your first day of retirement. This loss of purchasing power forces you to draw much more heavily from your personal savings, 401(k)s, and IRAs to bridge the financial gap. If you underestimate this drain, you risk depleting your liquid nest egg much faster than anticipated.

How Social Security Attempts to Fill the Gap

Unlike a fixed corporate pension, your federal retirement benefits are designed to adapt to a changing economy. The Social Security Administration provides an annual Cost-of-Living Adjustment to preserve the buying power of your monthly benefit. In 2025, the COLA delivered a 2.5% increase, and projections for the 2026 adjustment hover around 2.6% to 2.8%,.

While any increase is welcome, the mechanism used to calculate the Social Security COLA frequently fails to reflect the true financial reality experienced by seniors. The adjustment is tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This specific index measures the spending habits of younger, working-age Americans who allocate a larger portion of their budgets to commuting, apparel, and consumer electronics. Retirees, by contrast, spend a disproportionate share of their fixed incomes on healthcare and housing—two sectors that historically inflate much faster than the broader consumer market.

Because the government measures inflation using a basket of goods you likely do not purchase in high volumes, your Social Security raise will almost always feel a step behind your actual cost of living. When property taxes surge and out-of-pocket medical expenses climb, an extra $50 a month from Social Security does little to ease the strain on your budget. The purchasing power of Social Security benefits has been slowly eroding for decades because the mandated adjustments simply do not keep pace with the specific, unavoidable costs retirees face.

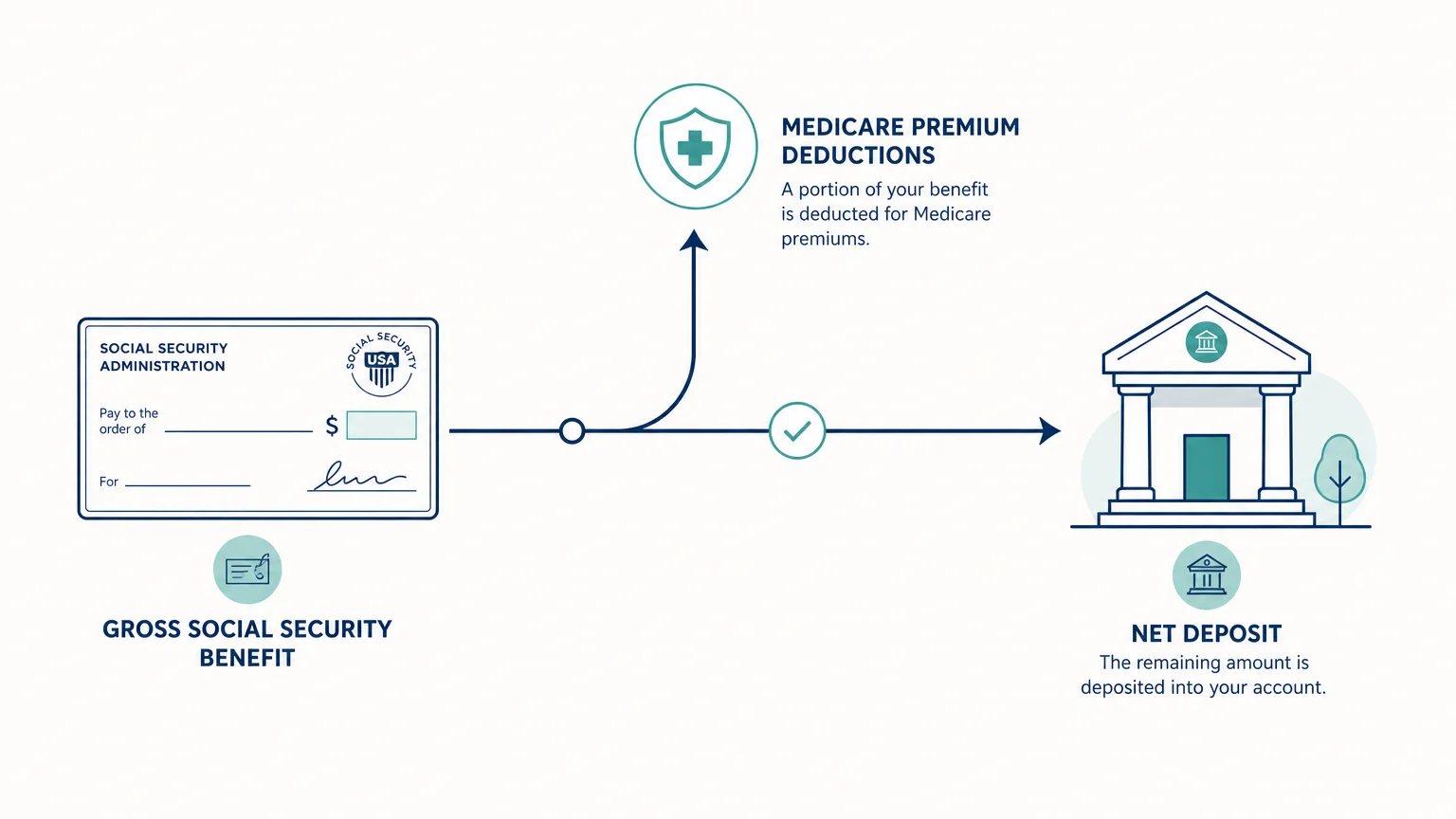

The Medicare Factor: A Silent Siphon

Your gross Social Security benefit is not the amount deposited into your checking account. For the vast majority of retirees, Medicare premiums are deducted directly from Social Security before the money ever clears the bank. This administrative setup creates a frustrating scenario where a large portion of your hard-earned COLA is instantly swallowed by rising healthcare costs.

For 2026, the standard Medicare Part B premium sits at $202.90 per month, alongside an annual deductible of $283,. When Medicare premiums rise at a faster percentage rate than your Social Security COLA, your net monthly increase shrinks significantly. In some years, a moderate Social Security raise is entirely consumed by a simultaneous spike in Medicare costs. While a “hold harmless” provision generally protects most retirees from seeing their actual Social Security checks decrease due to standard Part B premium hikes, this rule effectively wipes out the COLA for millions of Americans.

Furthermore, if you have been diligent in saving and generate a higher income in retirement, you face an additional financial hurdle: the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge is added to your Part B and Part D premiums based on your Modified Adjusted Gross Income (MAGI) from two years prior. The 2026 IRMAA brackets dictate that if you are a single filer with a MAGI over $109,000 (or $218,000 for joint filers) in 2024, your Part B premium jumps from the standard $202.90 to $284.10 per month. Higher income tiers push the monthly premium even further, maxing out at over $680 per month per person.

A strategic financial move—such as executing a large Roth conversion, selling a vacation home, or taking substantial capital gains from your portfolio—can easily push your MAGI over the established thresholds. Surpassing an IRMAA bracket by even one dollar triggers the higher premium tier for the entire calendar year. Because these premiums cut directly into your cash flow, verifying current brackets on Medicare.gov before making large withdrawals is absolutely vital for preserving your income.

Evaluating Your Personal Purchasing Power

Because national inflation metrics do not accurately reflect the senior lifestyle, you need to calculate your personal inflation rate. Understanding exactly where your money goes allows you to build a defensive financial strategy that protects your pension and investment income.

Conduct a thorough expense audit every twelve months. Break down your outgoing cash flow into precise categories to identify which sectors are draining your purchasing power.

- Isolate Healthcare Costs: Separate your Medicare premiums, supplemental insurance premiums, prescription copays, and out-of-pocket dental or vision expenses. Healthcare inflation routinely outpaces general inflation, meaning this sector requires the most aggressive budgeting.

- Track Property-Related Expenses: If your mortgage is paid off, you might feel insulated from housing inflation. However, property taxes, homeowners association (HOA) fees, home insurance, and basic maintenance costs continue to rise relentlessly. Compare these specific bills to what you paid three years ago.

- Evaluate Discretionary Spending: Look at your travel, dining, and entertainment expenses. During periods of high inflation, discretionary spending is the easiest lever to pull to quickly restore cash flow balance.

- Calculate the Gap: Add up your guaranteed income—your fixed pension plus your net Social Security benefit. Subtract your baseline essential expenses. If the remaining margin is shrinking year over year, your current withdrawal strategy from your portfolio needs immediate adjustment.

Taking the time to measure your personal inflation rate prevents you from flying blind. Once you know exactly how much your cost of living has increased, you can pivot your investment strategy to ensure your portfolio yields enough to cover the shortfall.

Strategies to Protect Your Retirement Income

You cannot control the national inflation rate, nor can you rewrite the terms of your fixed pension. However, you maintain absolute control over how you deploy your remaining retirement assets. Protecting your purchasing power requires a proactive shift from wealth preservation to strategic, inflation-adjusted growth.

Maximize Tax-Advantaged Growth

If you are still working, consulting part-time, or running a small business, maximizing your tax-advantaged retirement accounts is the single best way to outpace inflation. The Internal Revenue Service regularly adjusts contribution limits to account for rising prices. For 2026, the 401(k) base contribution limit sits at $24,500. The standard IRA contribution limit for 2026 is $7,500, with an $1,100 catch-up allowance for those aged 50 and older, bringing the total to $8,600. Keeping cash on the sidelines guarantees a loss of purchasing power; routing it through tax-shielded accounts forces your money to work harder.

Incorporate Dividend Growth Investing

While bonds provide stability, they rarely provide enough yield to conquer inflation. Dividend-paying stocks—specifically companies with a decades-long history of increasing their payouts annually—serve as an excellent inflation hedge. When you invest in dividend growth funds, your principal remains invested in the market, but you receive a cash payout that historically rises faster than inflation. This creates a synthetic “COLA” for your personal portfolio, helping bridge the gap left by your fixed pension.

“The miracle of compounding returns is overwhelmed by the tyranny of compounding costs.” — John Bogle, Founder of Vanguard

As Bogle wisely noted, high fees will destroy your inflation-fighting efforts. When utilizing dividend strategies, prioritize low-cost index funds or Exchange-Traded Funds (ETFs) over expensive, actively managed mutual funds. By keeping your expense ratios near zero, you keep more of your investment yield in your own pocket.

Utilize Treasury Inflation-Protected Securities (TIPS)

For the portion of your portfolio that must remain conservative, traditional bonds expose you to significant purchasing power risk. Treasury Inflation-Protected Securities (TIPS) offer a direct solution. Backed by the U.S. government, the principal value of a TIPS bond adjusts upward with the Consumer Price Index. If inflation spikes, the underlying value of your bond increases, and your interest payments—which are calculated based on that adjusted principal—rise as well. Allocating a portion of your fixed-income portfolio to TIPS ensures that at least part of your safe money keeps pace with the cost of living.

Optimize Your Withdrawal Sequencing

Taxes are your largest lifetime expense. In retirement, every dollar you save in taxes is a dollar that can be spent combating inflation. If you pull money from traditional IRAs or 401(k)s haphazardly, you trigger ordinary income taxes, which reduces your net purchasing power and can simultaneously trigger Medicare IRMAA surcharges.

Instead, establish a tax-efficient withdrawal sequence. Draw from taxable brokerage accounts first, taking advantage of lower long-term capital gains tax rates. Allow your tax-deferred accounts (Traditional IRAs) and tax-free accounts (Roth IRAs) to continue compounding. When you do eventually tap your Roth accounts, the withdrawals are completely tax-free and do not impact the taxation of your Social Security benefits or your Medicare premiums.

Avoiding Common Errors

Protecting a fixed pension requires discipline. Many retirees inadvertently sabotage their purchasing power by falling into predictable behavioral traps. By recognizing these pitfalls early, you can keep your financial plan intact.

- Fleeing to Cash During Market Volatility: When the stock market dips, the temptation to sell investments and move everything to a cash savings account is overwhelming. However, sitting in cash during an inflationary environment guarantees that you will lose purchasing power safely. You must maintain an appropriate allocation to equities to ensure your portfolio outgrows inflation.

- Underestimating Healthcare Timelines: A common mistake is assuming Medicare covers everything. It does not cover long-term care, custodial care, or routine dental work. Failing to earmark specific funds for out-of-pocket medical expenses means you will eventually have to pull large, tax-heavy distributions from your retirement accounts, accelerating the depletion of your nest egg.

- Claiming Social Security Prematurely: Claiming your benefit at age 62 locks in a permanently reduced monthly payout. Because the annual COLA is a percentage-based calculation, applying a 2.5% increase to a reduced base yields a much smaller dollar amount than applying it to a maximized base. Delaying Social Security until age 70 guarantees an 8% annual increase in your base benefit for every year you wait past full retirement age, establishing a much larger foundation for future COLAs.

- Ignoring Required Minimum Distributions (RMDs): Once you reach RMD age, the IRS forces you to withdraw a specific percentage of your tax-deferred accounts annually. If you have a large traditional IRA alongside your fixed pension, these forced distributions can push you into a higher tax bracket and trigger IRMAA. Failing to plan for RMDs in your sixties almost guarantees tax headaches in your seventies.

When DIY Isn’t Enough

Managing a portfolio, analyzing tax brackets, and keeping up with Medicare changes can quickly become a full-time job. While many aspects of retirement budgeting can be handled independently, certain complex scenarios demand the expertise of a fiduciary financial planner or tax professional.

Pension Buyout Offers: If your former employer offers you a lump-sum buyout in exchange for surrendering your fixed monthly pension, never make the decision alone. A professional can run a discounted cash flow analysis, factoring in current interest rates, your life expectancy, and inflation projections, to determine if rolling the lump sum into an IRA provides better long-term security than keeping the fixed payments.

Executing Roth Conversions: Moving money from a Traditional IRA to a Roth IRA requires paying taxes upfront. Doing this strategically during market downturns or low-income years is brilliant; doing it recklessly can trigger massive tax bills and Medicare surcharges. A tax professional will use sophisticated software to convert exactly up to the edge of your current tax bracket without spilling over.

Sequence of Returns Risk: If you retire during a bear market while inflation is high, withdrawing funds from a declining portfolio can irreparably damage your long-term wealth. A financial advisor can establish a “bucket strategy,” securing three to five years of living expenses in cash and short-term bonds, allowing your equities time to recover without being sold at a loss.

Moving Forward With Confidence

Watching the cost of living climb while your pension remains static is undeniably stressful. However, financial anxiety thrives on a lack of planning. By acknowledging that inflation is a permanent fixture of the economy, you can take proactive steps to outmaneuver it. From maximizing your tax-advantaged accounts and tracking your personal inflation rate, to embracing dividend growth investing and optimizing your withdrawal sequence, you hold the tools to protect your wealth.

Your retirement should be defined by the experiences you enjoy, not by a constant worry over grocery bills and healthcare premiums. Take the time to review your portfolio allocation, audit your current spending, and ensure your money is working just as hard as you did to earn it.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources like the IRS and the Social Security Administration.