Keeping a close eye on the annual Cost-of-Living Adjustment is an essential habit for managing a fixed income effectively. With inflation impacting the price of groceries and healthcare, understanding how these adjustments are calculated allows you to build a more resilient budget. If you rely on Social Security, the annual increase dictates how much breathing room your finances will have in the coming year. By learning how analysts predict these numbers and how rising Medicare premiums affect your final check, you can make smarter financial decisions today. This guide breaks down the mechanics behind the estimates, explores the latest projections for upcoming adjustments, and shows you exactly how to protect your purchasing power over the long haul.

The Essentials

- Inflation Drives the Numbers: The Social Security Administration bases annual adjustments on third-quarter inflation data. Current geopolitical pressures have pushed early estimates for 2027 higher than initially expected.

- Medicare Eats Into Your Raise: Part B premiums deduct directly from your Social Security check. The standard Part B premium increased to $202.90 in 2026, effectively offsetting a portion of the latest benefit bump.

- The Hold Harmless Rule Protects You: If your Medicare premium increase exceeds your Cost-of-Living Adjustment (COLA), federal rules prevent your net Social Security check from shrinking.

- Taxes Reduce Your Net Benefit: A higher gross payment could push your combined income above IRS thresholds, triggering taxes on up to 85% of your benefits.

The Mechanics: How the Cost-of-Living Adjustment Works

Congress enacted the automatic Cost-of-Living Adjustment provision in 1973, and the first adjustment took effect in 1975. Before this legislation, retirees had to wait for Congress to pass special acts to increase benefits, leaving many seniors struggling as their purchasing power eroded.

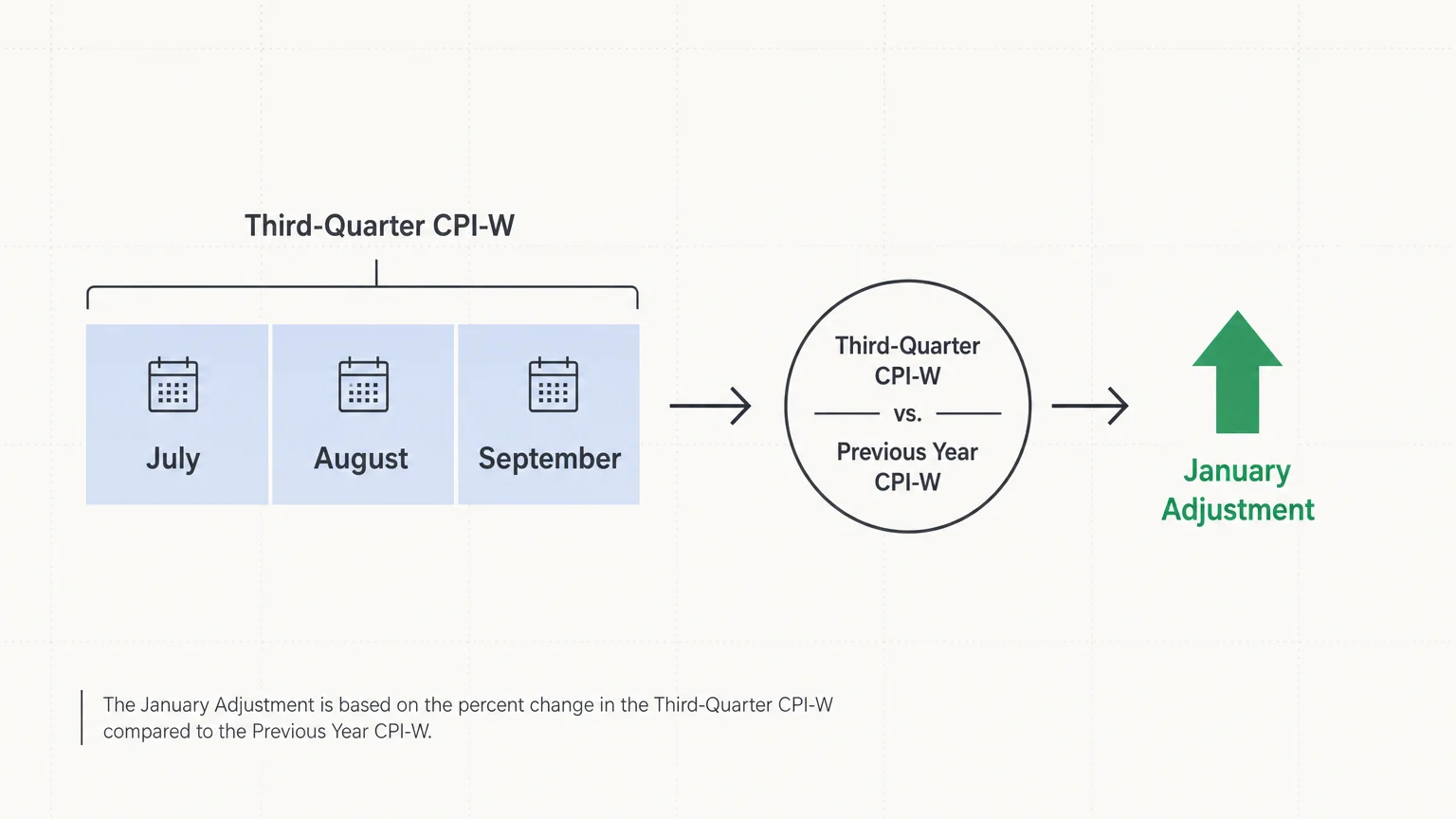

Today, the Social Security Administration relies on a specific formula to determine your annual raise. The process hinges on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which tracks the cost of a standardized basket of goods and services.

The government measures this index during the third quarter of the year—July, August, and September. Analysts take the average CPI-W from those three months and compare it to the same period from the previous year. If the index rises, you receive a corresponding percentage increase in your benefits starting in January. If prices fall and the index drops, your benefits remain flat; the government never reduces your gross check due to deflation.

“Inflation is the most destructive tax of all.” — Warren Buffett, Investor and CEO of Berkshire Hathaway

While the system offers a critical safety net, it features a notable flaw for retirees. The CPI-W measures the spending habits of younger, working-age Americans. These individuals spend a larger portion of their income on things like transportation and apparel. Seniors, however, typically allocate significantly more of their budget toward healthcare and housing. Because medical costs traditionally inflate faster than consumer goods, many advocates argue that the CPI-W fails to accurately capture the true cost-of-living increases older Americans face.

Current Trends: A Look at the 2026 Landscape

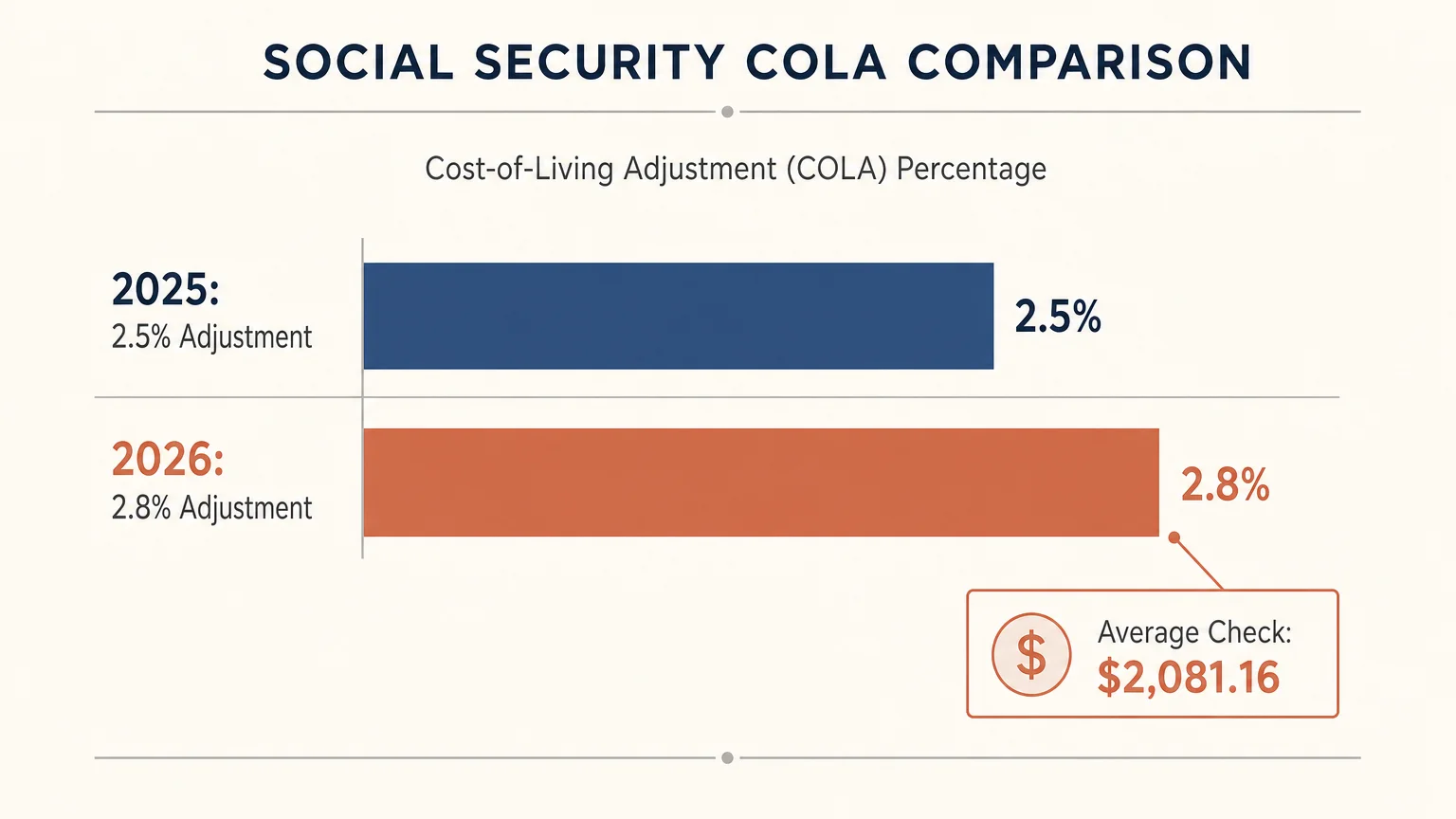

To understand why analysts are watching future estimates so closely, you must examine the current baseline. Following a 2.5% increase in 2025, the Social Security Administration finalized a 2.8% adjustment for 2026.

This 2.8% boost lifted the average monthly check for retired workers to $2,081.16 by April 2026. While any raise provides relief, a sub-three-percent adjustment feels restrictive for retirees who remember the massive 8.7% bump delivered in 2023. Furthermore, economists quickly noted that a 2.8% raise might not provide enough of a buffer against the subsequent waves of inflation that hit the economy.

As everyday expenses escalated throughout the early months of 2026, retirees found themselves stretching those dollars further. A $56 average monthly increase barely covers the rising costs of utilities, property taxes, and a trip to the grocery store. This squeeze forces retirees to pay close attention to the early forecasts for the following year.

Looking Ahead: Why 2027 Projections Are Climbing

Estimating the next adjustment requires tracking monthly inflation data long before the official third-quarter measurement period begins. Advocacy groups and independent policy analysts run sophisticated models to project where the numbers will land.

In the spring of 2026, those estimates began to paint a picture of a larger upcoming raise. The Senior Citizens League (TSCL), a prominent advocacy group, initially projected a steady 2.8% adjustment for 2027. However, as geopolitical tensions and supply chain disruptions drove gasoline and housing prices higher, forecasts began to shift dramatically.

By June 2026, updated estimates suggested the 2027 adjustment could reach 3.8%. Meanwhile, independent Medicare and Social Security policy analyst Mary Johnson revised her forecast upward to 4.7%. She noted that the surge in inflation represented the highest cost pressures seen in three years, deeply impacting seniors on fixed incomes.

If the official number lands near 4.7%, it would mark the largest increase since 2023. A 4.7% boost would add roughly $95 to an average $2,026 monthly benefit, pushing it well over the $2,100 mark. While a higher check sounds appealing, it signals a harsh economic reality: the cost of surviving is getting more expensive. You are not getting richer; your benefits are simply trying to catch a moving train.

The Medicare Factor: Your True Net Income

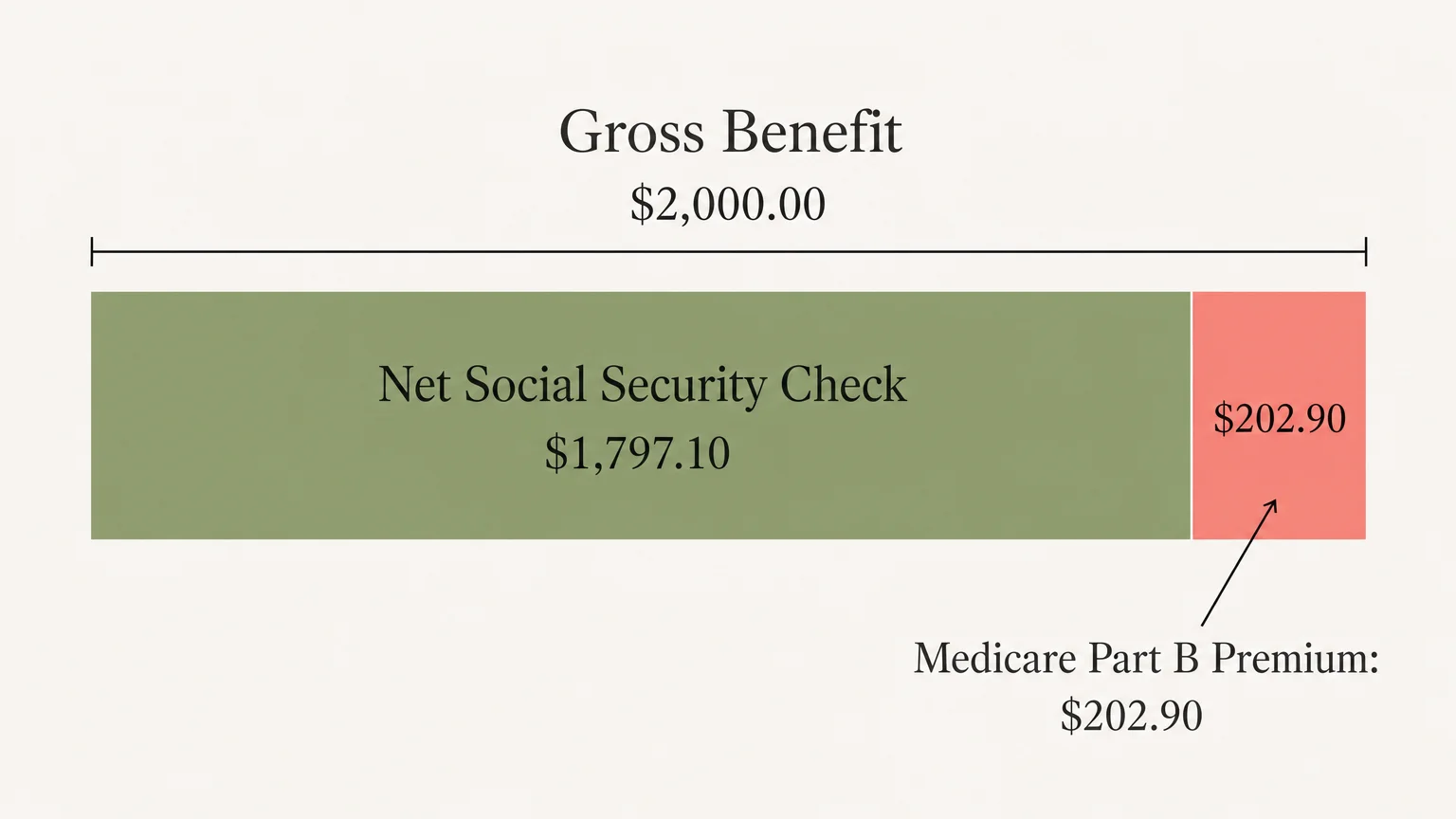

Watching gross benefit estimates provides only half the picture. To calculate your actual take-home pay, you must factor in Medicare Part B premiums. The government automatically deducts this premium from your Social Security benefit before the funds ever reach your bank account.

In 2026, the standard Medicare Part B premium rose to $202.90 per month, an increase of $17.90 from the 2025 rate of $185.00. The annual Part B deductible also jumped to $283 in 2026, up from $257 the previous year.

Consider how this dynamic impacts a typical retiree. If your gross Social Security benefit was $1,800 in 2025, your net check after the $185.00 Medicare deduction was $1,615.00. With the 2.8% adjustment for 2026, your gross benefit increased by roughly $50 to $1,850. However, because your Medicare premium increased to $202.90, your net check became $1,647.10. You only realized about $32 of that $50 raise.

Medicare Part B Costs: 2025 vs. 2026

| Benefit Feature | 2025 Amount | 2026 Amount |

|---|---|---|

| Standard Monthly Premium | $185.00 | $202.90 |

| Annual Deductible | $257.00 | $283.00 |

Fortunately, federal law provides a safety mechanism known as the “hold harmless” provision. This rule dictates that a Medicare Part B premium increase cannot reduce your net Social Security benefit below what you received the previous year. If your COLA adds $15 to your monthly check, but the Medicare premium increases by $17.90, the government caps your Medicare premium increase at $15. Your actual bank deposit remains exactly the same; it just fails to grow.

IRMAA: When Success Costs You More

While most retirees pay the standard Part B premium, higher-income earners face a different reality. The Income-Related Monthly Adjustment Amount (IRMAA) is a surcharge added to both Medicare Part B and Part D premiums for individuals who report a modified adjusted gross income above certain thresholds.

The government bases your IRMAA surcharge on your tax return from two years prior. Therefore, your 2026 Medicare premiums rely on the income you reported on your 2024 tax return. If you sold a business, converted a traditional IRA to a Roth IRA, or simply withdrew a large sum from your retirement accounts, you could trigger this surcharge.

When high inflation drives up your Social Security benefits, it subtly increases your gross income. Over time, combined with required distributions from retirement accounts, you might accidentally cross an IRMAA threshold. Once crossed, the government significantly increases your Medicare premiums, rapidly devouring your Social Security raise. Managing your taxable income brackets carefully throughout retirement helps you avoid these steep penalty tiers.

“A good financial plan is a road map that shows us exactly how the choices we make today will affect our future.” — Jean Chatzky, Financial Editor and Author

What Can Go Wrong

Relying solely on government estimates and automatic adjustments to fund your retirement lifestyle introduces significant risk. Avoid these common pitfalls to keep your financial plan on track:

- Forgetting About the Tax Man: Many retirees assume their Social Security benefits are tax-free. In reality, the Internal Revenue Service taxes up to 85% of your benefits if your combined income exceeds specific thresholds. Because these tax thresholds are not adjusted for inflation, each annual COLA pushes more retirees into higher tax brackets. A bigger gross check often results in a larger tax bill the following April.

- Treating the COLA as a True Raise: You must remember that this adjustment looks backward, not forward. The increase you receive in January compensates you for the inflation that already occurred in the previous year. If inflation continues to surge in the new year, your new check is already losing ground. Spending the extra money on luxury items rather than allocating it to basic living expenses can drain your cash reserves.

- Ignoring Healthcare Inflation: While your standard living costs might rise by 3% or 4%, out-of-pocket medical expenses often grow at double that rate. Failing to budget for supplemental insurance premiums, dental care, and prescription copays leaves a massive hole in your retirement strategy.

When to Consult a Professional

Retirement planning rarely remains static. Navigating the intersection of taxes, healthcare, and fixed income often requires a trained eye. Consider consulting a fiduciary financial advisor or tax professional in the following scenarios:

- You are approaching age 73: Required Minimum Distributions (RMDs) from traditional retirement accounts become mandatory. A professional can help you structure these withdrawals to minimize the impact on your Social Security taxation and avoid IRMAA surcharges.

- You plan to sell a major asset: Liquidating real estate, selling a business, or cashing out heavy stock positions creates massive capital gains. An advisor can help you time these sales across different tax years to protect your Medicare premiums.

- You are deciding when to claim benefits: Because your annual adjustments multiply against your base benefit, waiting to claim Social Security until age 70 results in permanently higher monthly checks. A planner can run a break-even analysis tailored to your specific health history and portfolio size.

Frequently Asked Questions

When is the official Social Security COLA announced?

The Social Security Administration officially announces the next year’s Cost-of-Living Adjustment in mid-October. They release the exact percentage shortly after the Bureau of Labor Statistics publishes the September inflation data, finalizing the third-quarter calculation.

Does a higher adjustment mean my purchasing power is increasing?

No. The adjustment is designed strictly to maintain your purchasing power, not increase it. Because the formula relies on historical data, a high adjustment simply means you are being reimbursed for the higher prices you already paid at the grocery store and gas pump over the last twelve months.

What happens to my benefits if the inflation rate drops to zero?

If the CPI-W shows no inflation—or even deflation—the adjustment formula yields a zero. Your benefits will not decrease; they will remain exactly the same as the previous year. You will never receive a negative adjustment.

Can a Medicare premium increase reduce my Social Security check below last year’s amount?

No. Thanks to the “hold harmless” provision, your net Social Security benefit cannot drop due to standard Medicare Part B premium increases. If the premium hike is larger than your benefit increase, the government simply caps your premium deduction so your net check remains flat.

As you map out your budget for the coming year, keep a steady eye on both inflation data and upcoming policy shifts. Understanding how these moving parts interact empowers you to protect your nest egg and enjoy a more secure retirement.

Last updated: June 2026. The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.