Talking to your grown children about your retirement plans is uncomfortable, but silence is far more dangerous. If you avoid discussing cognitive decline, inheritance realities, and end-of-life care, you force your family to make agonizing decisions during a crisis instead of following a clear plan. Too many retirees quietly drain their savings to support adult children or hide the location of vital documents out of a misplaced desire for privacy. By tackling these seven specific topics now, you protect your wealth and spare your loved ones immense stress. This guide breaks down exactly what you need to discuss, the current financial facts driving these choices, and how to initiate these conversations without unnecessary drama.

1. The “Bank of Mom and Dad” Needs a Closing Date

Many retirees quietly sabotage their own financial security to fund their adult children’s lifestyles. According to 2025 data from Savings.com, half of all parents with adult children provide them with regular financial support, averaging nearly $1,500 per month. If you are subsidizing your children’s rent, car payments, or vacations, you need to have an honest conversation about setting boundaries.

You cannot afford to treat your retirement accounts like an emergency fund for your family. If your investments run dry in your eighties, you cannot take out a loan to fund your own living expenses. Tell your children exactly when the regular subsidies will stop, giving them a few months to adjust their own budgets.

“You can borrow for college, but you cannot borrow for retirement. It is your job to protect your own financial security first.” — Suze Orman, Personal Finance Expert

If you have substantial wealth and genuinely want to help your children financially, structure your generosity. Under 2026 tax laws, the Internal Revenue Service (IRS) allows an annual gift tax exclusion of $19,000 per recipient. A married couple can give $38,000 to an adult child without filing a gift tax return or tapping into their lifetime estate tax exemption. Frame these financial gifts as intentional wealth transfers rather than an open-ended ATM.

2. The True Cost of Long-Term Care (and Who Will Provide It)

Do not assume your children will move you into their spare bedroom and become your full-time caregivers. Providing round-the-clock care is physically grueling and often requires adult children to sacrifice their own peak earning years. You must discuss how you plan to handle potential physical decline and how you intend to pay for professional help.

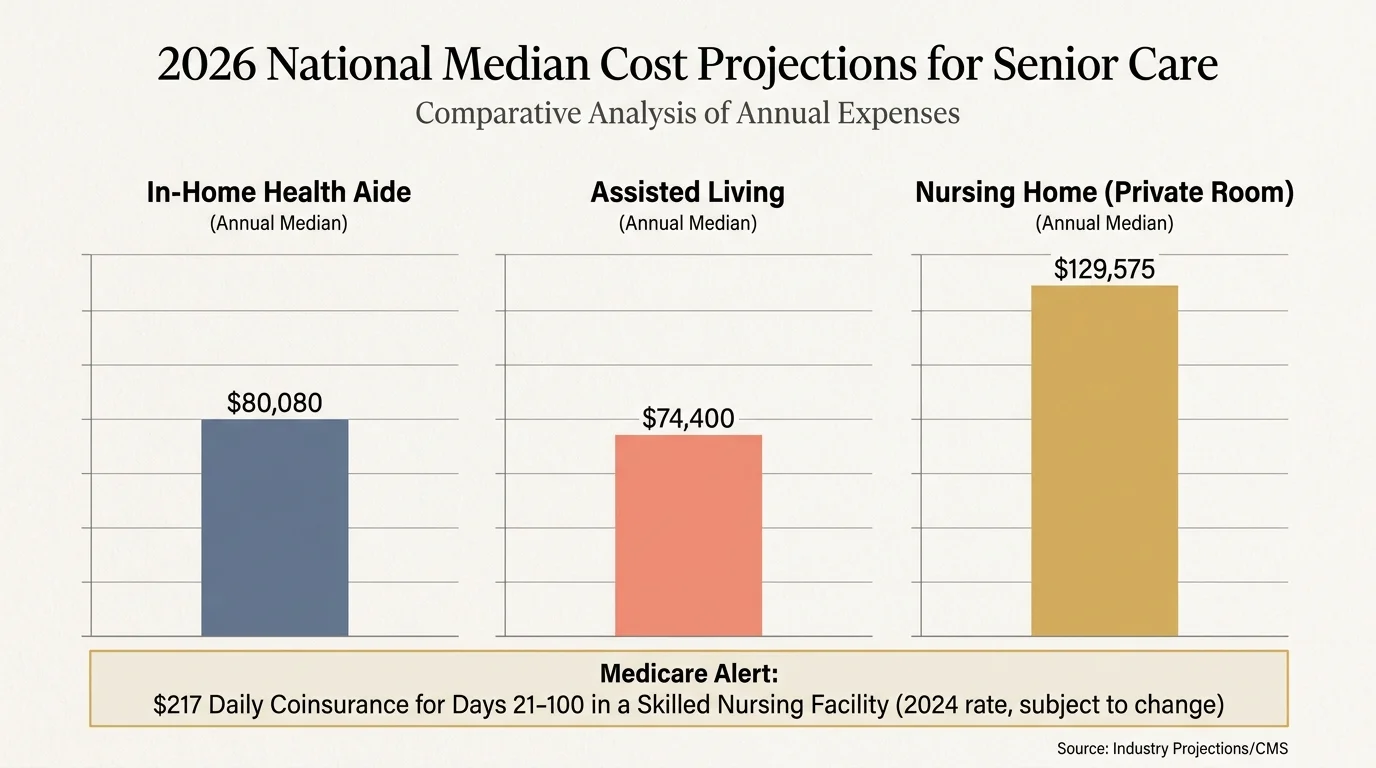

The financial reality of aging is staggering. According to the Genworth CareScout Cost of Care Survey for 2025/2026, long-term care costs continue to outpace general inflation:

| Type of Care | 2026 National Median Cost | What It Covers |

|---|---|---|

| In-Home Health Aide | ~$80,080 / year | Hands-on personal assistance (bathing, dressing) in your own home for 44 hours a week. |

| Assisted Living | ~$74,400 / year | Room, board, and daily assistance in a residential community setting. |

| Nursing Home (Private Room) | ~$129,575 / year | 24/7 skilled medical care and intense supervision. |

A massive misconception among adult children is that Medicare will cover these costs. You must correct this assumption. Medicare.gov clearly states that the program does not pay for long-term custodial care. While Medicare Part A covers up to 100 days in a skilled nursing facility after a qualifying hospital stay, it requires steep out-of-pocket costs; for 2026, beneficiaries pay a $217 daily coinsurance for days 21 through 100. Discuss whether you have long-term care insurance, plan to self-fund, or expect to eventually rely on Medicaid.

3. The Details of Diminished Capacity (Who Controls the Money)

Cognitive decline is the most terrifying topic to breach, yet it is arguably the most important. If you develop dementia or suffer a major stroke without a durable financial power of attorney in place, your adult children cannot simply access your bank accounts to pay your mortgage or medical bills. They will have to petition a court for conservatorship—a slow, public, and expensive legal process.

You need to decide who will step into your financial shoes if you lose capacity, and you must tell that person what the role entails. Naming an agent does not mean giving up control today; a “springing” power of attorney only takes effect when a physician certifies you are incapacitated. Use resources from the Consumer Financial Protection Bureau (CFPB) to guide your chosen proxy on how to legally manage someone else’s money. Make sure your children know who holds this power so they do not fight over control during a medical crisis.

4. The Reality of Their Inheritance (or Lack Thereof)

Adult children often harbor wild misconceptions about what they will inherit. Some assume they are getting millions; others assume you are broke. Both scenarios lead to poor financial planning on their part.

You do not need to show them your exact bank balances down to the penny, but you should establish expectations. If you plan to spend your last dime enjoying your retirement—as is your right—tell them not to count on a windfall. If your primary asset is your home, explain that its equity might be used to fund your late-stage medical care rather than passed down as a legacy.

If you are leaving behind a complex estate—such as a family business, real estate portfolio, or blended family trusts—transparency is even more critical. Explain the mechanics of how your assets will be distributed so siblings are not blindsided by unequal divisions or restrictive trust rules after you pass.

5. Your End-of-Life Medical Wishes

Do not leave your children guessing about your medical preferences while you lie incapacitated in an ICU. The guilt and trauma associated with guessing a parent’s end-of-life wishes can tear families apart.

You need three specific documents, and your children need to know where to find them:

- Healthcare Proxy (Medical Power of Attorney): Designates exactly who has the legal authority to make medical decisions if you cannot.

- Living Will: Outlines your specific preferences regarding life-sustaining treatments, feeding tubes, and ventilators.

- HIPAA Authorization: Allows medical professionals to discuss your condition freely with your named family members.

Sit your designated healthcare proxy down and have a blunt conversation about your views on quality of life versus length of life. Make sure the person you choose is emotionally capable of pulling the plug if that aligns with your written wishes.

6. Downsizing and the Family Home

Your four-bedroom, two-story house was perfect for raising a family, but it might be a hazard for aging in place. Steep stairs, high-maintenance yards, and isolating suburban layouts often force retirees to reconsider their living arrangements.

Adult children frequently attach deep emotional sentiment to the family home. They might assume you will keep it forever so they can bring their kids back for the holidays. If you plan to sell the house and move to a 55+ community, downsize to a condo, or relocate to a warmer climate, tell them early. Give them a timeline so they can retrieve their childhood belongings from the attic before the dumpster arrives.

7. Where Your Important Documents Are Actually Stored

A brilliant estate plan is completely useless if your family cannot find it. Too many retirees lock their wills in a safe deposit box without telling anyone which bank holds the key, or they store crucial passwords in their heads.

“The best estate plan is one where your family knows exactly what to do, who to call, and where the money is located long before they actually need to know.” — Ed Slott, Retirement Tax Specialist

Create a physical “In Case of Emergency” binder or a secure digital vault, and give the location to your executor. This checklist must include:

- Original copies of your Will and Trust documents

- Contact information for your estate attorney, CPA, and financial advisor

- A list of all bank accounts, brokerage accounts, and safe deposit boxes

- Details on life insurance policies and where to find the physical contracts

- Instructions for accessing your digital life (email passwords, social media, phone passcodes)

- Your Social Security Administration (SSA) and Medicare numbers

- Pre-planned funeral arrangements or burial plot deeds

Common Mistakes to Avoid When Initiating These Talks

Having the conversation is important, but how you handle it determines whether your family embraces the plan or recoils from the tension. Avoid these common blunders:

- Ambushing the Holidays: Do not drop heavy financial or end-of-life topics in the middle of Thanksgiving dinner. Schedule a dedicated time to talk when everyone is sober, rested, and prepared.

- Using Vague Language: Saying “you’ll be taken care of” means entirely different things to different people. Be concrete. Use real scenarios and explain your legal documents clearly.

- Waiting for a Health Crisis: If you wait until you receive a scary diagnosis to have these talks, emotion will cloud everyone’s judgment. The best time to discuss aging is when you are healthy and independent.

Professional vs. Self-Guided: When to Bring in a Mediator or Advisor

Not every family can handle a raw conversation about money and death without outside help. Determine your family dynamic before deciding how to approach the discussion.

- Self-Guided Discussions: Best for families with open communication, simple estates, and siblings who generally get along. You can facilitate the meeting yourself using an agenda.

- Using a Financial Planner: Ideal when explaining complex investments, business successions, or significant wealth transfers. An advisor acts as a neutral third party who can explain the tax logic behind your decisions.

- Using an Elder Law Attorney: Necessary when navigating Medicaid planning, setting up special needs trusts, or dealing with highly fractured family dynamics where litigation is a real risk.

Frequently Asked Questions

Does Medicare pay for assisted living if I run out of money?

No. Medicare does not cover the cost of room, board, or personal care in an assisted living facility. If you deplete your assets, you will have to rely on Medicaid, which has strict income and asset limits and typically only covers care in approved nursing homes, not standard assisted living communities.

When is the best time to have the estate planning conversation?

The ideal time is in your early sixties, shortly after you retire. This establishes your financial boundaries early, gives your children clarity on their inheritance, and ensures your medical directives are in place well before any cognitive decline begins.

How do I stop financially supporting my adult children without ruining our relationship?

Communicate the change as a reality of your own retirement math, not as a punishment. Give them a firm timeline—such as three to six months—to take over their own cell phone bills, car insurance, or rent. Offer them budgeting advice, but stand firm on the cutoff date to protect your own longevity risk.

Your retirement years should be defined by peace of mind, not by the anxiety of unspoken expectations. By stepping up and initiating these seven conversations, you give your adult children the ultimate gift: a clear roadmap for the future. You eliminate the guesswork, prevent sibling rivalries over money, and ensure your final decades unfold exactly as you intended. Schedule a family meeting, gather your documents, and start talking.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.