Finding an affordable, vibrant place to spend your golden years doesn’t mean you must settle for a sleepy, isolated town or pay a premium for a sprawling metropolis suburb. As housing costs stay elevated and the 2026 Social Security cost-of-living adjustment lands at 2.8%, many retirees are strategically relocating to dynamic small cities. These hidden gems offer world-class healthcare, walkable downtowns, and rich cultural scenes at a fraction of the cost you would find in major metropolitan areas. By trading an expensive zip code for a rising small city, you can protect your nest egg, lower your tax burden, and fund the retirement lifestyle you actually want.

Why Small Cities Are Winning Over Suburbs

For decades, the standard American retirement plan involved paying off a suburban house and aging in place. Today, soaring property taxes, aggressive homeowner association (HOA) fees, and the sheer cost of maintaining a large home are pushing retirees to reconsider. Suburbs often lack walkability, forcing you into your car for every minor errand or social outing. In contrast, revitalized small cities provide centralized infrastructure. You get the community feel of a small town alongside the dining, arts, and medical facilities of a much larger metro region—without the suburban sprawl price tag.

The Financial Reality of Relocating in 2026

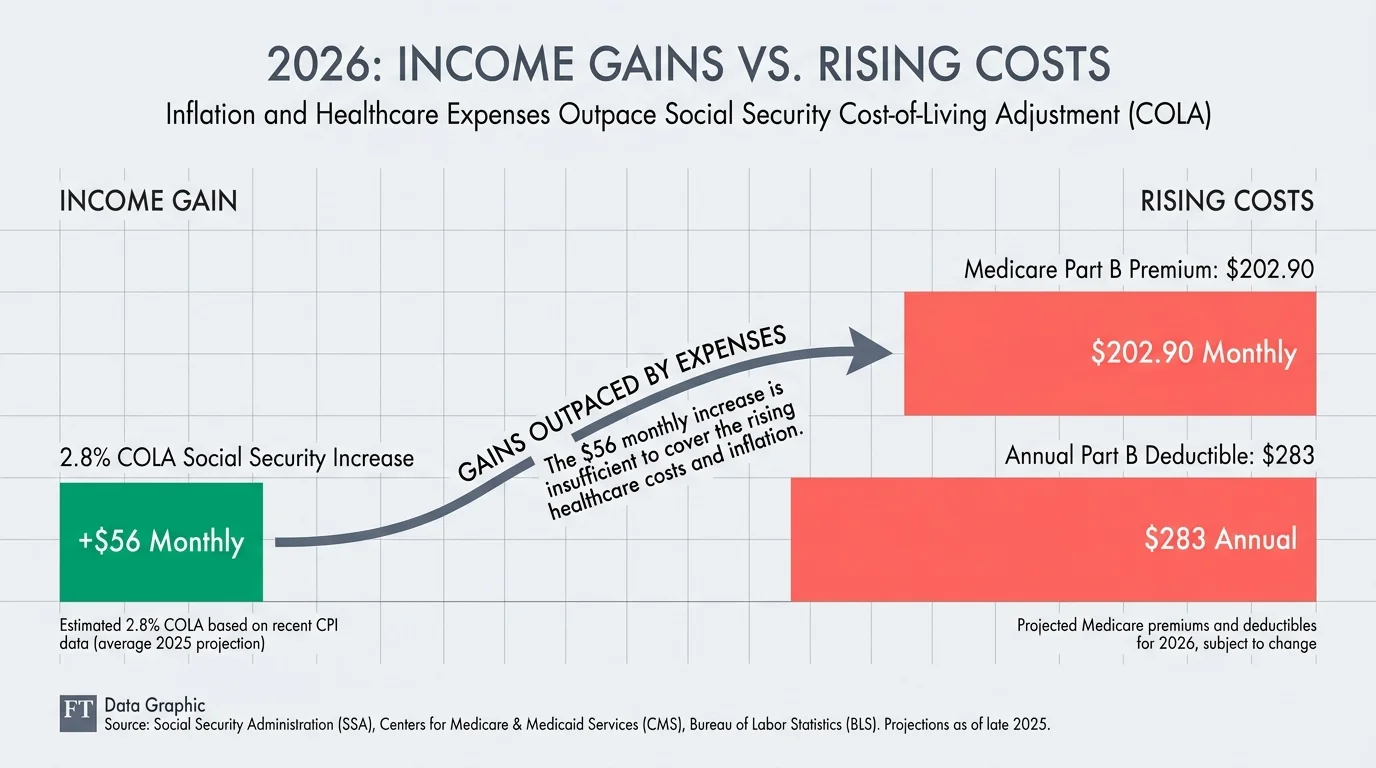

According to the Social Security Administration (2026), the cost-of-living adjustment (COLA) sits at 2.8%, bringing the average retired worker’s monthly check up by about $56 [2.2]. However, those modest gains quickly evaporate if you live in a high-cost suburb. The Centers for Medicare & Medicaid Services (2026) reports that the standard Medicare Part B premium increased to $202.90 per month, while the annual Part B deductible rose to $283. When healthcare costs and inflation chip away at your fixed income, reducing your largest expense—housing—becomes critical.

Moving to a more affordable city allows you to capture federal tax advantages while reducing state and local burdens. According to the Internal Revenue Service (2026), the standard deduction climbed to $32,200 for married couples filing jointly and $16,100 for single filers. Retirees age 65 and older receive an additional $1,650 per qualifying spouse or $2,050 for single filers. Furthermore, the recently enacted One Big Beautiful Bill Act provides a temporary $6,000 bonus deduction for qualifying older adults through 2028. You protect more of these tax-free dollars when you live in a state with low property taxes and favorable retirement income exemptions.

“Price is what you pay. Value is what you get.” — Warren Buffett, CEO of Berkshire Hathaway

7 Affordable Small Cities for Retirement

Finding value in your retirement destination requires balancing housing costs with quality of life. Resources like AARP provide excellent livability indexes, but we evaluated specific locations offering robust healthcare access, cultural amenities, and housing markets that fall well below expensive suburban averages.

| City, State | Estimated Median Home Price (2026) | Retiree Tax Climate |

|---|---|---|

| Greenville, SC | $327,000 – $410,000 | Highly Favorable (No SS Tax) |

| Winchester, VA | $396,000 – $420,000 | Moderate |

| Fayetteville, AR | $385,000 – $469,000 | Highly Favorable (No SS Tax) |

| Midland, MI | Below National Avg. | Favorable (Pension Exemptions) |

| Weirton, WV | Highly Affordable | Favorable (Phasing out SS Tax) |

| Appleton, WI | $291,000 | Highly Favorable (No SS Tax) |

| Green Valley, AZ | Under $300,000 | Highly Favorable (No SS Tax) |

1. Greenville, South Carolina

Nestled in the foothills of the Blue Ridge Mountains, Greenville has transformed from a quiet textile town into a major destination for retirees. A vibrant, walkable downtown centers around Falls Park on the Reedy, giving you instant access to nature, public art, and culinary hotspots without suburban gridlock. Housing costs remain highly attractive; recent data suggests the median home price in Greenville ranges from $327,000 to $410,000, noticeably below the national average. South Carolina also refuses to tax Social Security benefits, keeping more money in your pocket each month.

2. Winchester, Virginia

If you want to stay close to the East Coast metropolitan hubs without paying Washington, D.C., prices, Winchester offers an ideal compromise. Known for its historic walking mall and apple orchards, this Shenandoah Valley city boasts a median home price hovering around $396,000 to $420,000. You secure the charm of historic architecture and modern healthcare facilities while dodging the crippling property taxes of Northern Virginia’s primary suburbs.

3. Fayetteville, Arkansas

Tucked into the Ozark Mountains, Fayetteville provides a dynamic college-town atmosphere thanks to the University of Arkansas. Retirees flock here for the mild climate, expansive trail systems, and excellent healthcare infrastructure. The median home price sits between $385,000 and $469,000, delivering exceptional value for a rapidly growing region. With Arkansas exempting Social Security benefits from state income tax, Fayetteville serves as a powerful financial haven for retirees.

4. Midland, Michigan

Securing the top spot on U.S. News & World Report’s 2025–2026 Best Places to Retire ranking, Midland represents the pinnacle of Midwestern affordability. As the home of Dow Chemical’s world headquarters, the city supports impressive amenities for its size, including a 110-acre botanical garden and an 80-park system. Housing runs significantly below the national median, allowing you to downsize your mortgage while upgrading your access to outdoor recreation.

5. Weirton, West Virginia

Securing the number two spot on the U.S. News & World Report rankings, Weirton offers a tight-knit river community feel just a short drive from Pittsburgh. By choosing this friendly panhandle town, you secure some of the lowest housing costs in the nation. West Virginia also offers generous tax breaks for retirees, making it an exceptional choice for those managing a strict fixed income.

6. Appleton, Wisconsin

If you tolerate snowy winters, Appleton rewards you with phenomenal affordability and low crime rates. Situated along the Fox River, this outdoorsy college town boasts a median home price near $291,000. Wisconsin exempts Social Security benefits and government retirement plans from state income tax, allowing you to build a comfortable lifestyle around the city’s vibrant arts scene and seasonal festivals.

7. Green Valley, Arizona

For retirees seeking year-round warmth outside of heavily congested Phoenix or Scottsdale, Green Valley provides an oasis. Located south of Tucson in the Santa Cruz River Valley, this community caters explicitly to active adults. Forbes recently highlighted Green Valley for maintaining median home prices under $300,000. The 3,000-foot elevation ensures cooler summer nights than the rest of the desert, and Arizona does not tax Social Security benefits.

What Can Go Wrong

Relocating for retirement introduces unique risks. Avoid these common pitfalls to ensure your move is a success:

- The Boomerang Effect: Moving strictly for a lower cost of living often leads to regret if you deeply miss your family and friends. Moving back a few years later wipes out any financial savings you initially gained.

- Overlooking Healthcare Access: A rural town might look idyllic, but an hour-long drive to the nearest cardiovascular specialist can quickly become dangerous. Prioritize small cities with established, high-quality hospital systems.

- Ignoring Climate Realities: Visiting a city in October feels vastly different from enduring its extreme summer heat or harsh winter snow. Test the location during its most challenging season before signing a mortgage.

When to Consult a Professional

Before packing your boxes and putting your current home on the market, seek guidance in these specific scenarios:

- You plan to sell a highly appreciated home. An accountant can help you navigate capital gains tax exclusions and prevent unexpected federal or state tax bills.

- You rely heavily on a Medicare Advantage plan. Healthcare networks change dramatically by zip code. Verify that your preferred doctors and hospitals accept your coverage in the new state by checking Medicare.gov.

- You receive out-of-state pension income. A financial advisor can clarify how your new home state taxes your specific pension, 401(k), or IRA withdrawals.

Frequently Asked Questions

Is it better to rent first when relocating for retirement?

Yes. Renting for six to twelve months in your new city allows you to experience the traffic patterns, healthcare access, and neighborhood dynamics without locking your equity into a permanent decision. It acts as an affordable insurance policy against buyer’s remorse.

Will moving to a new state lower my Social Security benefits?

No. Your federal Social Security benefit amount remains exactly the same regardless of where you live in the United States. However, moving to one of the many states that do not tax Social Security at the state level can increase your net take-home pay.

Do I need to update my estate plan if I cross state lines?

Absolutely. Every state enforces different laws regarding probate, medical directives, and power of attorney. Have a local estate planning attorney review your current documents immediately after you establish residency in your new small city.

Making Your Next Move

Relocating is a significant decision that reshapes your daily routine, your financial trajectory, and your social circle. The suburbs served their purpose while you were working and raising a family, but retirement opens the door to a more tailored, affordable lifestyle. Visit a few of these small cities during different seasons, rent a short-term property in a residential neighborhood, and test the waters before committing to a purchase.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.