Trading a large family house for a low-maintenance condo or a vibrant 55-plus community unlocks home equity and drastically reduces your monthly utility bills. The hardest part of the transition is figuring out what to do with decades of accumulated possessions. Moving into a smaller floor plan forces you to ruthlessly evaluate every piece of furniture, heirloom, and garage tool you own. A successful downsizing strategy relies on selling high-value items to fund your move while avoiding the trap of paying to pack and transport things you no longer use. By identifying exactly which categories of household goods are best liquidated before moving day, you streamline the physical move and protect your retirement budget from unnecessary storage fees.

The Downsizing Math: Why Less Space Makes Financial Sense

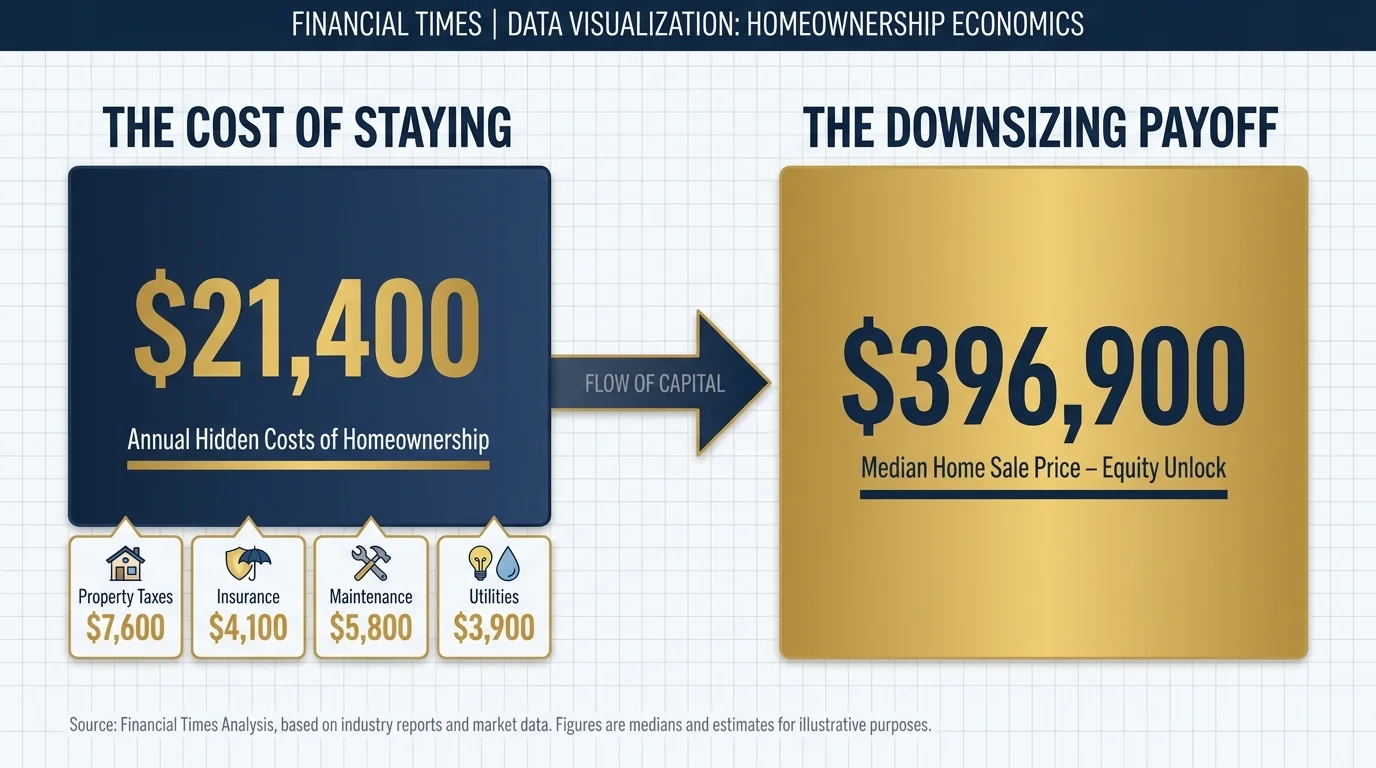

Staying in a massive, aging home slowly drains your retirement savings. Recent real estate data highlights why so many seniors are eager to transition to a smaller footprint. In early 2025, the median existing-home sale price reached $396,900. Unlocking that equity provides a powerful cash infusion for your retirement portfolio. However, the true financial drain of a large home lies in its carrying costs. A 2025 financial study revealed that the hidden costs of homeownership—encompassing property taxes, homeowners insurance, routine maintenance, and energy utilities—average $21,400 annually for a typical single-family home.

Moving to a condo, townhome, or managed retirement community drastically cuts these hidden expenses. You no longer pay to heat empty guest rooms or repair a sprawling, aging roof. Yet, realizing these savings requires a physical purge. You cannot comfortably fit a four-bedroom lifestyle into a two-bedroom floor plan. To make the transition seamless, you must adopt a minimalist mindset and systematically liquidate the items that no longer serve your daily needs.

“Simplicity is the master key to financial success. When there are multiple solutions to a problem, choose the simplest one.” — John Bogle, Founder of Vanguard

1. Formal Dining Sets and Oversized Antique Furniture

The days of formal, sequestered dining rooms are largely over. Modern condos and retirement community homes feature open-concept floor plans with multipurpose living spaces and kitchen islands. A twelve-foot mahogany dining table and its matching, leaded-glass china hutch simply will not physically fit into these modernized spaces. Furthermore, moving heavy “brown furniture” is incredibly expensive, as professional movers charge by the hour and by weight.

Retirees are aggressively selling these oversized pieces before moving day. When pricing your antiques, you must adjust your expectations to the current market. Younger generations generally prefer modular, lightweight furniture; they do not want to inherit massive, immovable heirlooms. To maximize your return, list these large items on local online marketplaces like Facebook Marketplace, OfferUp, or Nextdoor. Require the buyer to handle the transportation. If the pieces have genuine historical value or designer pedigree—such as authenticated mid-century modern credenzas—contact a reputable local consignment shop that caters to interior designers.

2. Fine China, Crystal, and Silver Collections

Decades ago, completing a fine china registry was a crucial milestone. Today, maintaining fragile, hand-wash-only plates and polishing sterling silver flatware feels like a chore. As you transition into a lighter, lower-maintenance retirement lifestyle, you will likely favor durable, microwave-safe, and dishwasher-friendly dinnerware. Storing multiple twelve-piece settings of fine china consumes precious cabinet space in a smaller kitchen.

Selling these collections requires strategy. Local buyers rarely want partial sets of china. Instead, leverage specialized online buyers. Companies like Replacements, Ltd. purchase active and discontinued china, crystal, and silver patterns directly from consumers. You can look up your specific pattern, see what items they are actively buying, and ship the pieces directly to them. Alternatively, if you own verified sterling silver flatware—not silver plate—you can sell it to precious metal dealers for its melt value, which frequently yields a higher cash return than trying to sell the set intact.

3. Multiple Vehicles and Recreational Vehicles (RVs)

When you and your spouse were both commuting to an office, maintaining two or three vehicles was a logistical necessity. In retirement, maintaining a fleet of vehicles is an unnecessary drain on your fixed income. Auto insurance premiums, registration fees, routine maintenance, and fuel costs add up quickly. If your new, downsized community is walkable or offers shuttle services, transitioning to a single-car household is an immediate financial victory.

The same logic applies to recreational vehicles, camper vans, and boats. While an RV provides a fantastic way to travel during the early “go-go” years of retirement, it becomes a financial burden when parked in a storage facility for eleven months of the year. Selling these high-ticket assets before you move instantly injects thousands of dollars into your retirement accounts and eliminates the headache of finding specialized parking in your new, smaller neighborhood.

4. Extensive Book Collections and Physical Media

Floor-to-ceiling bookshelves impart a cozy aesthetic to a large home, but books are incredibly dense, heavy, and costly to transport. Packing and moving twenty boxes of hardcover books can quickly inflate your moving bill. Retirees are embracing digital minimalism by transitioning to e-readers and tablets. A single digital device grants you instant access to millions of titles without taking up an inch of shelf space. By downloading the Libby app, you can seamlessly borrow digital books and audiobooks from your local library for free.

Before boxing up your library, separate the valuable items from the paperbacks. Signed copies, true first editions, and out-of-print historical volumes should be evaluated by a local antiquarian bookseller or sold individually online to collectors. For the bulk of your reading material, scan the barcodes using an app like BookScouter, which instantly tells you if online buyback companies will pay cash for specific titles. Donate the remaining inventory to a local library fundraiser or charity thrift shop.

5. Specialty Kitchen Gadgets and Appliances

Downsizing often involves trading a massive chef’s kitchen for a highly efficient, streamlined cooking space. You will no longer have the luxury of dedicating a cabinet exclusively to rarely used appliances. Bread makers, massive stand mixers, dedicated roasting ovens, canning equipment, and elaborate juicers take up prime real estate on your new, limited countertops.

Evaluate your cooking habits honestly. If you only use the stand mixer once a year to bake holiday cookies, it is time to sell it. High-quality kitchen appliances—particularly brands like KitchenAid, Vitamix, and Le Creuset—retain their resale value remarkably well. Clean them thoroughly, take brightly lit photos, and sell them on local community boards. Keep only the versatile, daily-use tools that support your immediate nutritional needs.

6. Holiday Decorations and Seasonal Gear

In a four-bedroom house, dedicating a portion of the basement or an entire walk-up attic to holiday storage is easy. A downsized condo will not accommodate fifteen plastic bins of seasonal decorations. You must ruthless curate your collection before paying movers to transport items that will ultimately sit in a rented, off-site storage unit.

Keep a small, manageable collection of highly sentimental ornaments and essential decorations. Sell the bulky items—such as ten-foot artificial trees, massive outdoor inflatables, and heavy yard displays. Timing is crucial when liquidating seasonal goods; sell winter decor in November and patio sets in April. Pay special attention to vintage ornaments from the 1950s and 1960s; mid-century holiday decor has a massive collector base online, and certain glass ornaments can command premium prices.

7. High-Maintenance Landscaping Equipment

One of the primary benefits of downsizing to a townhouse, condominium, or a 55-plus community is relinquishing exterior maintenance. A homeowners association (HOA) typically handles lawn care, tree trimming, and snow removal. Consequently, your heavy-duty landscaping arsenal becomes instantly obsolete.

Riding lawnmowers, heavy gas-powered snowblowers, chainsaws, and commercial-grade power washers are expensive machines that hold solid resale value. Clean the equipment, perform basic maintenance to ensure they start smoothly, and list them for sale locally. Selling these items not only pads your moving budget but also eliminates the danger of storing and transporting volatile gasoline and oil cans.

8. Bulky Fitness Equipment

Treadmills, elliptical machines, and universal weight benches consume massive amounts of square footage. When transitioning to a smaller home, dedicating an entire bedroom to a personal gym is rarely a viable option. Disassembling, transporting, and reassembling complex fitness machinery is a frustrating task that movers often charge a premium to handle.

Instead of moving heavy equipment, savvy retirees sell these items and leverage their health insurance benefits. If you are enrolled in a Medicare Advantage (Part C) plan, you likely have access to the SilverSneakers program. In 2026, the estimated average monthly premium for a Medicare Advantage plan sits around $14, and these plans frequently include free or heavily discounted memberships to thousands of participating gyms and fitness centers nationwide. Sell the bulky treadmill, reclaim your living space, and utilize the state-of-the-art equipment at a local community center instead.

Strategic Ways to Sell Your Items

Once you identify what needs to go, you must execute the sales efficiently. Mixing and matching different sales channels based on the value and size of the items will yield the best financial return. Use this breakdown to plan your liquidation strategy:

| Selling Method | Best For | Expected Fees | Time & Effort Required |

|---|---|---|---|

| Estate Sale Companies | Liquidating an entire household quickly; handling massive volumes of goods. | Typically 30% to 50% commission on the total gross sales. | Low. The company handles pricing, staging, advertising, and crowd control. |

| Online Marketplaces (eBay, Poshmark) | High-value, easy-to-ship items like designer clothing, jewelry, and rare collectibles. | 10% to 15% platform fees, plus shipping and transaction costs. | High. You must photograph, describe, package, and ship every individual item. |

| Local Apps (Facebook Marketplace, Nextdoor) | Large, heavy items like furniture, appliances, and lawn equipment. | Usually zero fees for local, cash-in-hand transactions. | Medium. Requires communicating with buyers, negotiating, and scheduling pickups. |

| Consignment Shops | High-end designer accessories, mint-condition vintage decor, and boutique furniture. | 40% to 60% of the final sale price goes to the shop. | Low. You drop the items off, and the shop handles the merchandising and sales. |

Avoiding Common Errors: The 1099-K Tax Trap

As you begin selling decades worth of accumulated possessions, you must stay vigilant regarding current tax reporting regulations. The Internal Revenue Service recently updated the reporting thresholds for digital sales, catching many casual sellers off guard.

For the 2025 and 2026 tax years, third-party payment networks—such as PayPal, Venmo, eBay, and Facebook Marketplace checkouts—are required to issue a Form 1099-K to any seller who receives $600 or more in payments for goods and services. If you sell a single piece of furniture online, you will likely trigger this reporting threshold.

Do you owe taxes just because you received a 1099-K? Usually, no. If you sell a used leather sofa for $400 that you originally purchased years ago for $1,500, you are selling personal property at a loss. The IRS views this as a non-deductible personal loss, meaning it does not generate taxable income. You simply report the transaction on your tax return to offset the 1099-K data, showing zero taxable gain.

However, the rules change drastically if you sell items that have appreciated in value. If you sell fine art, rare coins, or vintage comic books for more than you originally paid, the resulting profit is subject to capital gains tax. For specific collectibles, the long-term capital gains tax rate can soar as high as 28 percent, depending on your overall income bracket. To protect yourself during an audit, maintain meticulous records detailing the original purchase price (your cost basis) and the final sale price of your high-value items.

When DIY Isn’t Enough

While managing your own garage sale or online listings maximizes your profit margins, there are specific scenarios where hiring a professional liquidator is the smartest financial move. Do not hesitate to call in the experts under the following conditions:

- You Own Specialized Collections: If you possess original artwork, rare stamps, extensive coin collections, or high-end mechanical watches, you risk severely underpricing them on your own. Hire a certified appraiser to establish a documented fair market value before attempting to sell.

- You Face a Strict Timeline: If your home sold faster than anticipated and you have to vacate the property in thirty days, you do not have time to haggle over individual lamps on the internet. An auction house or a turn-key estate liquidation firm can clear the property entirely within a strict deadline.

- You Have Physical Limitations: Downsizing is a physically grueling process. If lifting heavy boxes, moving furniture, or managing a weekend-long garage sale threatens your health, the 40 percent commission paid to an estate sale company is a worthwhile investment in your physical safety.

Frequently Asked Questions About Downsizing

Are proceeds from a moving sale or estate sale considered taxable income?

In most scenarios, no. If you sell used personal items—like clothing, basic furniture, and kitchenware—for less than their original purchase price, the IRS considers this a personal loss, which is not taxable. However, if you sell appreciating assets, such as fine art or rare antiques, for a profit, that specific gain is subject to capital gains tax. Always consult a certified public accountant regarding your specific tax liabilities.

Will I receive a tax form for selling items online?

Yes. Starting with the 2024 tax year (affecting 2025 and 2026 filings), third-party payment platforms like PayPal, Venmo, and eBay must issue a Form 1099-K if you receive $600 or more in gross payments for goods. Receiving this form ensures the IRS tracks the transaction, but it does not automatically mean you owe taxes if the items were sold at a personal loss.

How early should I start decluttering before a retirement move?

To avoid physical exhaustion and emotional burnout, financial planners and professional organizers recommend beginning the decluttering process at least six to twelve months before your planned move. Starting early allows you to take your time selling high-value items, ensuring you get the best possible price rather than accepting lowball offers in a last-minute panic.

Next Steps for Your Lighter Retirement

Shedding the physical weight of a large home is a liberating experience. By systematically selling oversized furniture, unused appliances, and high-maintenance equipment, you fund your moving expenses and protect your retirement nest egg from unnecessary storage fees. Start small to build momentum—tackle a single linen closet or a single bookcase this weekend. As you see the open space emerge, the task of downsizing an entire house will feel far less intimidating.

This article provides general retirement education and information only. Tax laws, real estate markets, and Medicare benefits change frequently. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice regarding estate sales, capital gains taxes, or retirement housing strategies, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources such as the IRS and Medicare.gov.