You might assume the best retirement destinations require moving to Florida or Arizona, but the latest migration data shows retirees are seeking better weather in completely unexpected places. Avoiding extreme heat, hurricanes, and high costs of living is driving a new wave of climate migration. Today’s retirees want four manageable seasons, tax advantages, and outdoor access without the premium price tags of traditional retirement hubs. From the rain shadows of the Pacific Northwest to the thermal springs of the South, these surprising locations offer plenty of sunshine and financial perks. If you are ready to trade snow shovels for comfortable living, here are seven unexpected cities where your retirement savings and the forecast both look bright.

At a Glance: The New Climate Migration

Before packing your bags, it helps to understand why the retirement map is shifting. Modern retirees are looking beyond the traditional warm-weather states for a few key reasons:

- Escaping extreme weather: Searing summer heat and severe storm seasons are pushing people toward moderate, inland climates.

- Maximizing tax benefits: A beautiful climate is less appealing if high state taxes drain your fixed income. The most popular new destinations combine pleasant weather with aggressive tax breaks for seniors.

- Seeking natural geographic advantages: Specific geographic features—like mountain rain shadows or thermal valleys—create surprisingly perfect microclimates in regions you might otherwise overlook.

1. Sequim, Washington: The Pacific Northwest’s Sunny Secret

When you think of Washington State, you likely picture endless gray skies and raincoats. However, the small city of Sequim (pronounced “skwim”) defies every Pacific Northwest stereotype. Nestled at the base of the Olympic Mountains, Sequim sits directly in a geographic “rain shadow”. As storms blow in from the Pacific Ocean, the mountains block the moisture, leaving Sequim unusually dry and bright.

Because of this phenomenon, Sequim averages over 300 days a year with at least some sunshine and receives a mere 16 inches of annual rainfall. By comparison, Seattle—just two hours away—gets notoriously soaked. Pilots even refer to the sky over Sequim as “The Blue Hole”.

Beyond the remarkably mild coastal weather, the financial forecast is highly appealing. Washington is one of the few states that levies zero state income tax. This means your Social Security benefits, pension payouts, and IRA withdrawals remain completely untouched by the state revenue department. The community is exceptionally senior-friendly, offering excellent local medical facilities with quick access to specialized care in the Greater Puget Sound area.

2. Greenville, South Carolina: Mild Winters and Tax-Friendly Living

Retirees who want to escape the harsh northern winters—but are exhausted by the oppressive humidity of deep-south summers—are finding a happy medium in Greenville, South Carolina. Located in the foothills of the Blue Ridge Mountains, Greenville offers four distinct seasons without the extremes. The city averages just three inches of snow per year, and the mountain proximity keeps the summer air slightly more breathable than the coastal regions.

Greenville’s financial climate is just as welcoming. South Carolina is incredibly tax-friendly for retirees. The state does not tax Social Security benefits. Furthermore, residents aged 65 and older can deduct up to $15,000 of other retirement income—such as distributions from 401(k) plans, IRAs, and pensions—from their state income taxes.

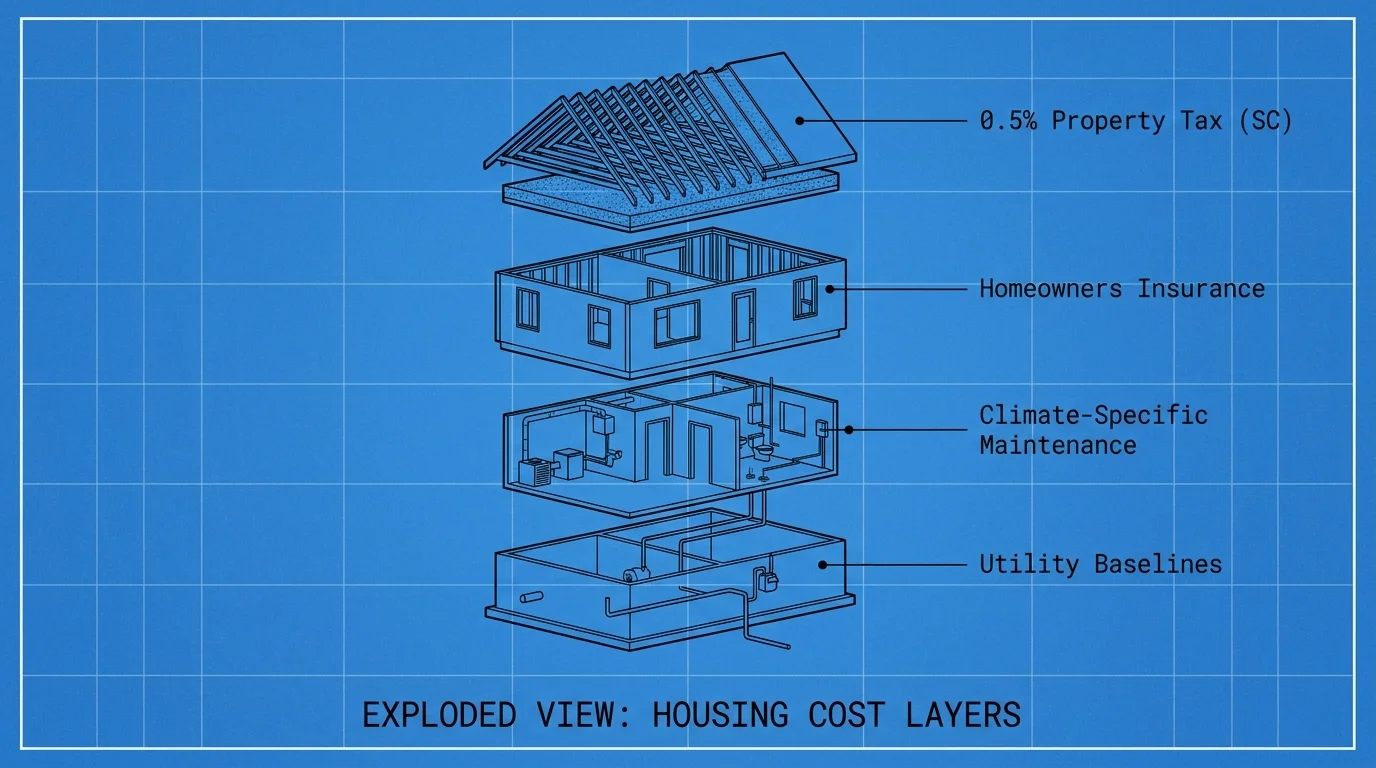

Property ownership is also highly manageable here. South Carolina features one of the lowest effective property tax rates in the country at just over 0.5%. Once you establish residency for a year, homeowners aged 65 and older can apply for a “homestead exemption,” which exempts the first $50,000 of their primary residence’s fair market value from local property taxes.

3. Chattanooga, Tennessee: The Scenic City with Zero Income Tax

Nicknamed the “Scenic City,” Chattanooga sits along the Tennessee River surrounded by the Appalachian Mountains. The location provides a magnificent buffer against extreme winter weather while offering stunning outdoor recreation. You will experience mild winters and warm, sunny summers that are perfect for hiking, boating, or simply enjoying downtown amenities.

What truly drives Chattanooga’s retirement boom is the tax environment. Tennessee does not have a state income tax. In 2021, the state fully phased out its “Hall Tax” on interest and dividends, meaning all forms of retirement income—including Social Security, 401(k) withdrawals, and pensions—are entirely tax-free at the state level.

Chattanooga balances small-town affordability with big-city perks, including some of the fastest residential internet speeds in the country and a rapidly growing healthcare sector. While Tennessee does rely on a higher state sales tax to balance its budget, the overall cost of living remains comfortably below the national average.

4. Hot Springs, Arkansas: Thermal Waters and Low Living Costs

Tucked into the Ouachita Mountains, Hot Springs is a historic resort city famous for its natural thermal baths. The surrounding mountains afford the city a mild, pleasant climate with beautiful autumn foliage and brief, gentle winters. It is an ideal setting for active retirees who enjoy fishing, boating on Lake Hamilton, or golfing year-round.

Financially, Arkansas is an overlooked gem. The cost of living is noticeably lower than the national average, allowing retirement nest eggs to stretch significantly further. Median home costs in Hot Springs are highly accessible, often hovering well below $200,000 depending on the neighborhood.

Arkansas does not tax Social Security benefits. For other types of retirement income, the state offers an exemption on the first $6,000 of income from IRAs or employer-sponsored plans. Additionally, homeowners aged 65 and older can freeze the assessed value of their primary residence, ensuring that their property taxes will not spike even if the local real estate market booms.

5. Athens, Georgia: A Vibrant Climate for Active Seniors

If you prefer your retirement with a side of vibrant culture, arts, and collegiate energy, Athens is an unexpected powerhouse. Located roughly 70 miles east of Atlanta, this classic college town—home to the University of Georgia—offers exceptional cultural events, continuing education opportunities, and top-tier medical facilities. The weather is comfortably warm, ensuring you will rarely have to deal with icy roads or heavy winter coats.

Georgia is routinely ranked as one of the best states for retirees from a tax perspective. Social Security income is completely exempt from state taxes. More impressively, Georgia offers a massive retirement income exclusion. Residents aged 65 and older can exclude up to $65,000 of retirement income per person. For a married couple filing jointly, that is up to $130,000 of tax-free retirement income every year. Additionally, Georgia transitioned to a flat income tax rate, dropping to 5.29% in 2026, keeping your overall tax burden light.

6. Roanoke, Virginia: Blue Ridge Beauty Without the Bitter Cold

Roanoke is a mountain sanctuary that provides the gorgeous scenery of the Blue Ridge Mountains without the punishing winters found further north. It is a hiker’s paradise, boasting over 700 miles of nearby trails, a thriving downtown arts scene, and a relaxed pace of life. The climate delivers four true seasons, but the mountain geography protects the valley from the brutal cold fronts that plague the Northeast.

Virginia offers a balanced, practical tax environment. The state does not tax Social Security benefits. For your other retirement income, Virginia provides a deduction of up to $12,000 for residents aged 65 and older, depending on their adjusted gross income. Recent tax code adjustments have also expanded standard deductions, giving seniors more flexibility when they file. Furthermore, real estate taxes in the Roanoke area are generally moderate, falling below the national average and allowing retirees to secure beautiful mountain-view properties without paying exorbitant annual fees.

7. Las Cruces, New Mexico: Desert Sunshine Without the Arizona Price Tag

For retirees who crave dry heat and brilliant desert sunshine, Arizona has traditionally been the go-to destination. But as housing prices in Phoenix and Scottsdale have skyrocketed, budget-conscious retirees are turning to Las Cruces, New Mexico. You still get over 300 days of sunshine a year and incredibly mild winters, but the cost of entry is substantially lower.

New Mexico has aggressively improved its tax laws to attract and retain seniors. The state exempts Social Security benefits for single filers with an adjusted gross income under $100,000, and for joint filers earning under $150,000. Even better, new legislation taking effect in 2026 begins phasing out the Social Security tax entirely for higher earners, starting with a 20% graduated exemption that will grow over the coming years. This forward-thinking legislation makes the “Land of Enchantment” an increasingly smart financial play for retirees.

What to Consider Before Relocating for Weather

When you move across state lines, you are not just trading snowstorms for sunshine; you are adopting an entirely new financial ecosystem. Before committing to a move, weigh these critical factors:

| Factor | What to Research | Why It Matters |

|---|---|---|

| Income Taxes | State taxation of Social Security, pensions, and IRAs. | A state with no income tax can save you thousands annually, preserving your nest egg. |

| Property & Sales Taxes | Local assessment rates, senior freezes, and combined sales tax rates. | States with zero income tax often compensate by levying higher property or sales taxes. Look at the total burden. |

| Healthcare Access | Distance to specialists and major hospital networks. | Rural mountain or desert towns might offer peace and quiet, but a 90-minute drive to a cardiologist becomes burdensome as you age. |

| Climate Realities | Humidity, wildfire risk, and allergy seasons. | A mild winter might come with high summer humidity or heavy spring pollen. Visit your target city during its worst weather month, not just its best. |

“The true measure of wealth in retirement is the richness of your life: the experiences you’re having, the relationships you’re developing, and the things you’re learning about the world and yourself.” — Warren Buffett, Investor and CEO

What Can Go Wrong: Avoiding Relocation Regrets

A poorly planned move can quickly erode your savings and your peace of mind. Here are the most common pitfalls retirees face when chasing better weather.

Misunderstanding Medicare Networks

If you are enrolled in Original Medicare (Parts A and B), you can generally see any doctor in the country who accepts Medicare. However, if you use a Medicare Advantage plan, your coverage is localized. Moving to a new state—or even a new county—will almost certainly require you to enroll in a new plan. If your new sunny hometown has a limited network of specialists, you could face steep out-of-pocket costs. Always verify your healthcare options before buying a home.

Remember to budget for healthcare inflation, too. For example, the standard Medicare Part B premium rose to $202.90 per month in 2026. Relocating to an area with a lower cost of living can help you absorb these unavoidable federal healthcare costs.

Underestimating the Hidden Costs of Homeownership

Moving to a region with mild weather might save you money on heating oil, but it could introduce new utility or insurance expenses. If you move near the coast or into a forested mountain region, your homeowners insurance premiums might skyrocket due to flood or wildfire risks. Additionally, moving away from a strong support network of friends and family means you may have to pay out-of-pocket for home maintenance, yard work, or caregiving tasks that loved ones previously helped with.

When to Consult a Professional

A cross-country retirement move is a major life transition. You should strongly consider consulting a fee-only fiduciary financial advisor and a tax professional in the following scenarios:

- You are selling a highly appreciated primary residence. You need a strategy to manage capital gains taxes, especially if your profits exceed the federal exclusion limits ($250,000 for single filers; $500,000 for married couples filing jointly).

- You are establishing a new legal domicile. If you plan to split your time between two states, you must clearly establish residency in your new, tax-friendly state to avoid being taxed by your former state.

- You have complex retirement income streams. Managing Required Minimum Distributions (RMDs) while navigating a new state’s tax brackets requires precision.

“You never have to worry about the uncertainty of what future higher taxes could do to your standard of living and spending ability in retirement… You can lose more money if you don’t do good tax planning.” — Ed Slott, CPA and Retirement Tax Expert

Frequently Asked Questions

Do I need to change my Medicare plan if I move to a new state?

If you have Original Medicare (along with a Medigap policy), your coverage generally travels with you anywhere in the U.S. However, if you have a Medicare Advantage plan or a standalone Part D prescription drug plan, you will trigger a Special Enrollment Period when you move. You will need to select a new plan that services your specific new ZIP code.

How long do I need to live in a new state to establish residency for tax purposes?

Most states require you to live there for at least 183 days of the year to be considered a resident for tax purposes. However, establishing a legal “domicile” also involves changing your driver’s license, registering your vehicles, registering to vote, and updating your estate planning documents to reflect your new state’s laws.

Do all states tax Social Security benefits?

No. The vast majority of U.S. states do not tax Social Security benefits. As of 2026, only a shrinking handful of states still tax these benefits, and even those states often provide generous exemptions based on age and income level. For comprehensive federal tax rules on benefits, you can consult the Social Security Administration.

Final Thoughts

Finding the perfect retirement destination requires balancing your desire for sunshine with the realities of your budget. By looking outside the traditional retirement hotspots, you can find vibrant, welcoming communities that protect your wealth while keeping you comfortable year-round. Whether you prefer the dry mountain air of the Pacific Northwest or the historic charm of a Southern college town, your ideal climate is out there waiting for you.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: May 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.