Medicare costs are climbing, with the 2027 Part B standard premium projected to reach $209.50 per month. This expected increase from the current $202.90 baseline directly impacts your bottom line, as the federal government automatically deducts these premiums from your Social Security checks. Understanding this upcoming deduction allows you to forecast your actual net income and prevent budget shortfalls. You must also account for potential Income-Related Monthly Adjustment Amount (IRMAA) surcharges, which can multiply your healthcare costs if your retirement income exceeds specific thresholds. By proactively managing your tax brackets and adjusting your withdrawal strategies now, you can mitigate these rising expenses and protect your hard-earned retirement savings from unexpected federal deductions.

The Mechanics of the Medicare Part B Deduction

For the vast majority of retirees, paying for Medicare Part B does not involve writing a check or logging into a portal to pay a monthly bill. Instead, the Social Security Administration deducts your Part B premium automatically from your monthly retirement benefit before the money ever reaches your bank account. This seamless system ensures your healthcare coverage remains active, but it also means you have less control over your net cash flow.

To understand the projected 2027 premium, you must look at the recent historical trajectory of Medicare costs. Healthcare inflation consistently outpaces general economic inflation due to the rising costs of medical technology, prescription drugs, and increased outpatient services. For 2025, the standard premium rose to $185.00. The following year, official announcements for 2026 placed the baseline premium at $202.90. The projected climb to $209.50 for 2027 represents a continuation of this upward trend.

Because these deductions happen behind the scenes, many retirees fail to factor them into their annual household budgets. When you calculate your expected retirement income, you must look at your gross Social Security benefit and subtract the projected Medicare premiums to determine your actual spendable cash.

How the Social Security COLA Interacts with Medicare Costs

Every October, the federal government announces the Cost-of-Living Adjustment (COLA) for Social Security benefits to help retirees keep pace with inflation. Concurrently, they announce the new Medicare Part B premiums for the upcoming year. This creates a financial tug-of-war that dictates your true net income increase.

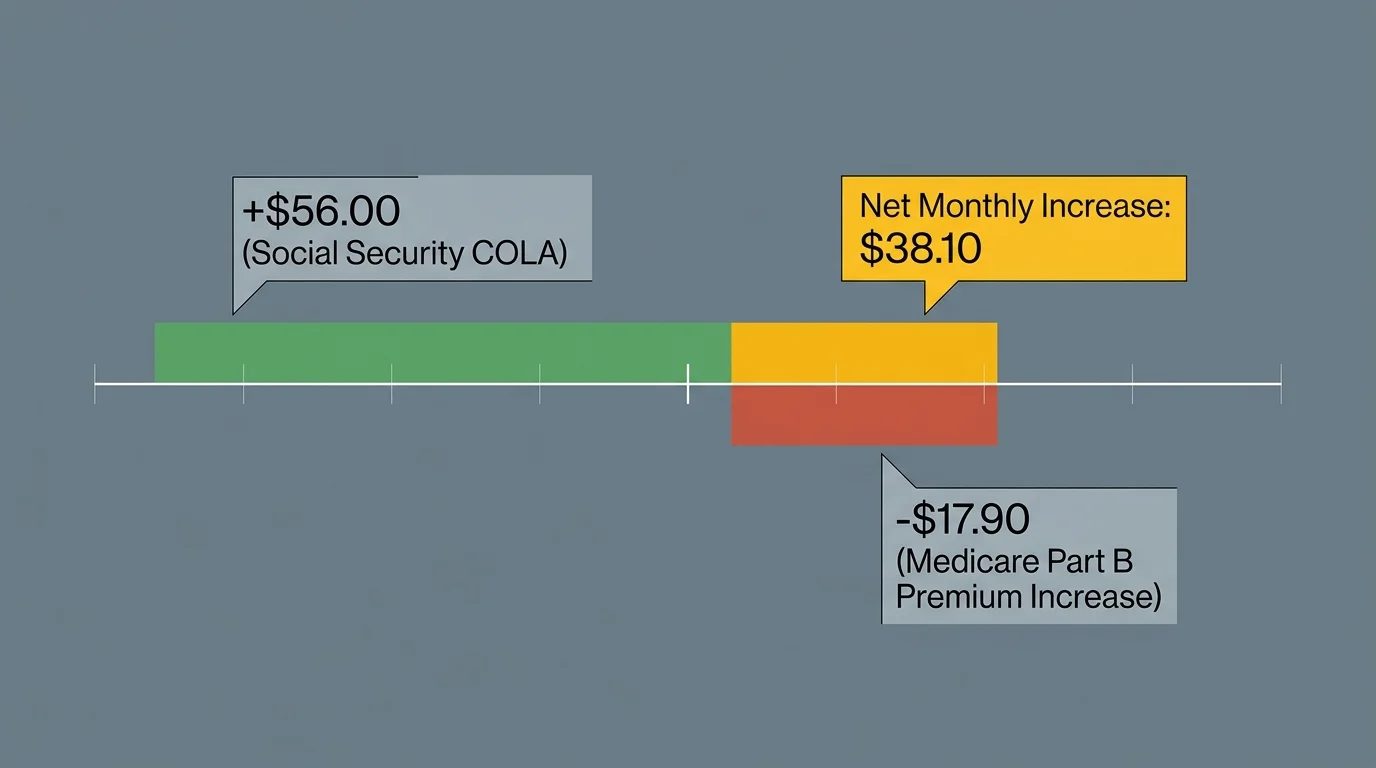

For example, in 2026, the Social Security COLA provided a 2.8% increase to retirement benefits. If your base monthly benefit was $2,000, that COLA added roughly $56 to your gross check. However, the Medicare Part B premium simultaneously increased by $17.90 per month (moving from $185.00 to $202.90). When you subtract the higher Medicare deduction from your COLA raise, your net increase drops to just $38.10. This interaction explains why many retirees feel their purchasing power declining despite receiving an annual raise.

To protect lower-income retirees from having their Social Security checks actually decrease, the government instituted the “hold harmless” provision. This rule dictates that your standard Medicare Part B premium increase cannot exceed the dollar amount of your Social Security COLA in a given year. However, you should not rely entirely on this protection. The hold harmless provision does not apply to you if:

- You are enrolling in Medicare Part B for the first time.

- You pay your Medicare premiums directly because you have delayed claiming Social Security benefits.

- You are subject to Income-Related Monthly Adjustment Amount (IRMAA) surcharges.

IRMAA: The Hidden Surcharge for Higher-Income Retirees

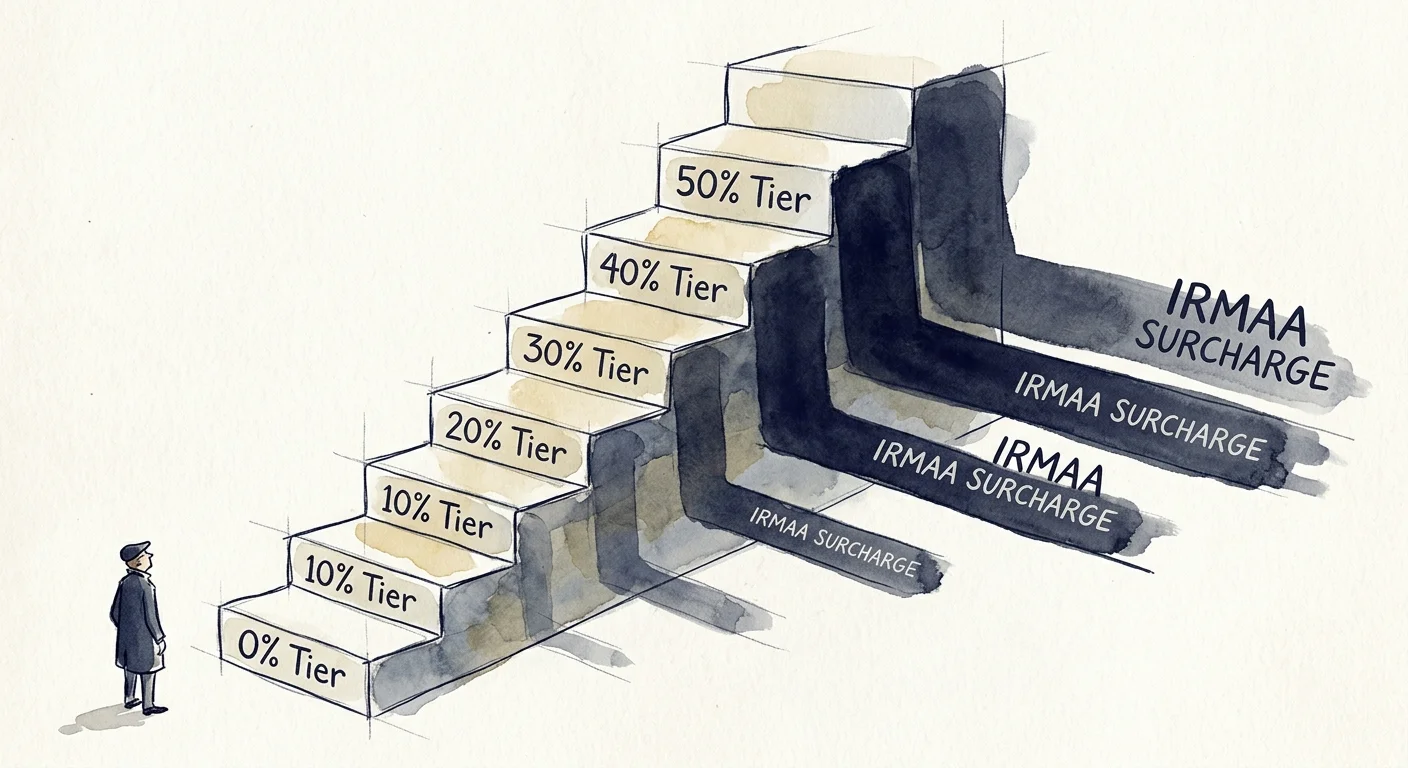

While the projected $209.50 premium represents the standard baseline for 2027, higher-income retirees face significantly steeper costs. The federal government uses a sliding scale called the Income-Related Monthly Adjustment Amount (IRMAA) to shift more of the healthcare burden onto wealthier beneficiaries.

IRMAA surcharges are based on your Modified Adjusted Gross Income (MAGI). For Medicare purposes, your MAGI is calculated by taking your Adjusted Gross Income from your federal tax return and adding back any tax-exempt interest you earned, such as income from municipal bonds. This specific calculation catches many retirees off guard.

Crucially, IRMAA operates on a two-year lookback period. Your 2027 Medicare premiums will be determined by the income you reported on your 2025 tax return. If you had an unusually high-income year in 2025, you will feel the financial sting in your 2027 Social Security checks.

To understand the financial impact, look at the baseline 2026 IRMAA brackets. In 2026, the first IRMAA threshold begins at $109,000 for single filers and $218,000 for married couples filing jointly. If your income exceeds these limits, your premiums jump significantly.

2026 Baseline IRMAA Brackets and Premiums

| Filing Status: Single (MAGI) | Filing Status: Joint (MAGI) | Total Part B Premium (2026) |

|---|---|---|

| $109,000 or less | $218,000 or less | $202.90 |

| $109,001 to $137,000 | $218,001 to $274,000 | $284.10 |

| $137,001 to $171,000 | $274,001 to $342,000 | $405.80 |

| $171,001 to $205,000 | $342,001 to $410,000 | $527.50 |

| $205,001 to $499,999 | $410,001 to $749,999 | $649.30 |

| $500,000 or more | $750,000 or more | $689.90 |

Note: IRMAA surcharges also apply to your Medicare Part D (prescription drug) coverage, adding an additional monthly fee on top of your standard plan premium.

Tax Planning Strategies to Minimize Medicare Premiums

Because Medicare premiums are inextricably linked to your tax return, proactive tax planning remains your best defense against rising healthcare costs. Implementing smart withdrawal strategies can keep your MAGI below the IRMAA thresholds and save you thousands of dollars throughout your retirement.

“Taxes are the single biggest threat to your retirement savings. It is not the stock market, it is not inflation, it is taxes.” — Ed Slott, CPA and Retirement Tax Expert

Optimize Roth IRA Conversions

Distributions from a Traditional IRA or 401(k) count as ordinary income, pushing your MAGI higher and potentially triggering IRMAA surcharges. Distributions from a Roth IRA, however, are entirely tax-free and do not count toward your MAGI. By converting Traditional IRA assets to a Roth IRA before you reach age 63 (the start of the two-year Medicare lookback window), you can drastically reduce your future taxable income. If you are already on Medicare, you can still execute small, strategic Roth conversions to fill up your current tax bracket without tipping over the next IRMAA threshold.

Utilize Qualified Charitable Distributions (QCDs)

Once you reach age 73, the IRS forces you to take Required Minimum Distributions (RMDs) from your tax-deferred accounts. These mandatory withdrawals often push retirees into higher IRMAA brackets. If you are charitably inclined, you can utilize a Qualified Charitable Distribution starting at age 70½. A QCD allows you to transfer funds directly from your IRA to a qualified charity. This transfer satisfies your RMD requirement but completely bypasses your Adjusted Gross Income, effectively keeping your MAGI low and shielding you from Medicare surcharges.

Manage the Timing of Capital Gains

Selling highly appreciated stock, real estate, or mutual funds generates capital gains that flow directly into your MAGI. If you need to rebalance a large taxable portfolio, consider spreading the sales across multiple tax years to avoid a massive income spike. Additionally, utilize tax-loss harvesting by selling underperforming assets at a loss to offset the gains from your winners. This strategy neutralizes the tax impact and keeps your Medicare premiums stable.

Be Cautious with Municipal Bonds

Financial advisors frequently recommend municipal bonds to high-net-worth retirees because the interest generated is exempt from federal income taxes. While municipal bonds do provide tax-free income, the Internal Revenue Service requires you to report that interest, and Medicare explicitly adds it back into your MAGI calculation. Relying too heavily on municipal bonds can inadvertently push you into a higher IRMAA tier, negating the expected tax benefits.

What Can Go Wrong

Navigating the complex rules surrounding Medicare and taxation leaves plenty of room for error. Understanding the most common pitfalls will help you safeguard your retirement budget.

Falling Off the IRMAA Cliff

Unlike federal income tax brackets, which are progressive, IRMAA operates as a hard cliff. If the 2026 threshold for a married couple is $218,000 and your MAGI comes in at $218,001, you cross into the next tier. That single extra dollar of income will trigger an $81.20 monthly surcharge for both you and your spouse, costing your household nearly $1,950 in additional premiums for the year. Precision matters when managing retirement income.

The Widow’s Penalty

When a spouse passes away, the surviving spouse faces an emotional and financial shock. For tax purposes, the surviving spouse must eventually file as a Single taxpayer, which cuts the IRMAA thresholds exactly in half. However, the survivor often continues to receive similar levels of income, especially if they inherited a large Traditional IRA that requires mandatory distributions. This dynamic frequently forces widows and widowers into severe IRMAA surcharges just when they are most vulnerable.

Ignoring the Two-Year Lookback Period

Many retirees assume their Medicare premiums will drop the moment they retire and their salary stops. Because of the two-year lookback, your first year of retirement is often billed based on your final, highest-earning years of employment. Failing to account for this lag can result in a frustrating period where your income has dropped, but your healthcare premiums remain artificially high.

Navigating Life-Changing Events and IRMAA Appeals

You do not always have to accept an IRMAA surcharge, especially if your financial situation has genuinely changed. The Social Security Administration recognizes that the two-year lookback period can unfairly penalize retirees who have experienced a sudden drop in income. If you receive an IRMAA determination letter, you have the right to appeal the decision by filing Form SSA-44.

To win an appeal, you must prove that your income reduction is the direct result of a specific, qualifying “Life-Changing Event.” The approved events include:

- Marriage, divorce, or annulment.

- The death of a spouse.

- Work stoppage or a significant reduction in work hours.

- Loss of an income-producing property due to a disaster or event beyond your control.

- Loss of a defined benefit pension plan.

- An employer settlement payment related to a company closure or bankruptcy.

When filing Form SSA-44, you must provide documentation of the event, such as a letter of resignation, a death certificate, or a divorce decree. You will also need to provide a realistic estimate of your newly reduced MAGI for the current year. If approved, the government will remove the surcharge and adjust your Part B premium down to the standard level immediately, saving you from paying inflated costs during the two-year lag period.

When to Consult a Professional

While standard Medicare enrollment is straightforward for many, certain financial scenarios require the expertise of a Certified Financial Planner (CFP) or a specialized tax advisor. You should seek professional guidance if you encounter any of the following situations:

- Selling a Business or Real Estate: Liquidating a major asset will create a massive, one-time spike in your capital gains. A professional can help you structure the sale using installment agreements or charitable trusts to spread out the tax burden and avoid maximum IRMAA penalties.

- Executing a Roth Conversion Ladder: Shifting large sums of money from tax-deferred accounts to tax-free accounts requires precise calculations. An advisor can map out a multi-year conversion strategy that fills your current tax bracket exactly to the brim without triggering the IRMAA cliff.

- Inheriting Significant Wealth: Inheriting a Traditional IRA subjects you to the IRS 10-Year Rule, forcing you to empty the account and claim the income within a decade. A tax expert can help you sequence these mandatory withdrawals to minimize the impact on your Medicare premiums.

Frequently Asked Questions

Will my Medicare Part B premium go down if my income drops?

Yes, your premium will eventually adjust downward. Because of the two-year lookback period, a drop in income in 2025 will automatically reflect in lower premiums in 2027. If the income drop was caused by a qualifying life-changing event (like retirement), you can file an appeal to have your premium lowered immediately rather than waiting two years.

Do Medicare Advantage plans cover the Part B premium?

No. If you choose to enroll in a Medicare Advantage (Part C) plan instead of Original Medicare, you are still required to pay the standard Part B premium to the federal government. While some Medicare Advantage plans offer a “Part B Giveback” benefit that covers a small portion of the cost, you remain responsible for the underlying premium and any applicable IRMAA surcharges.

How do I pay my Part B premium if I delay claiming Social Security?

If you enroll in Medicare at age 65 but delay your Social Security benefits to maximize your future monthly payouts, there is no automatic check for the government to deduct from. In this scenario, the Centers for Medicare and Medicaid Services (CMS) will mail you a quarterly bill called a “Medicare Premium Bill” (CMS-500). You can pay this bill directly via mail, phone, or through your secure Medicare.gov account.

Can I use my Health Savings Account (HSA) to pay Medicare premiums?

Yes. If you funded a Health Savings Account during your working years, you can withdraw funds tax-free to pay for your Medicare Part B, Part D, and Medicare Advantage premiums. However, you cannot use HSA funds to pay premiums for Medicare Supplement (Medigap) policies. Furthermore, you must stop contributing new money to your HSA at least six months before applying for Medicare to avoid IRS penalties.

Take Control of Your Healthcare Costs

The projected 2027 Medicare Part B premium of $209.50 serves as a crucial reminder that healthcare costs in retirement are neither static nor cheap. As baseline premiums continue to rise alongside inflation, your net Social Security income faces constant pressure. By understanding how the Part B deduction works, monitoring your MAGI to avoid the unforgiving IRMAA cliffs, and deploying intelligent tax strategies like Roth conversions and QCDs, you can keep more of your money in your own pocket.

Retirement planning is about seeing the road ahead and steering accordingly. Review your current tax brackets, project your future Required Minimum Distributions, and begin making strategic adjustments today. A proactive approach will ensure that rising Medicare costs never derail the retirement lifestyle you worked so hard to build.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.