Your will serves as the ultimate blueprint for your legacy, but filling it with the wrong assets can trigger unnecessary probate delays, family conflict, and massive tax penalties. Leaving certain items in your will actually overrides faster, tax-efficient transfer methods that automatically bypass the probate courts. Many retirees mistakenly list every single asset they own, unknowingly creating a bureaucratic nightmare for their grieving loved ones. To protect your estate and ensure your wealth transfers exactly as you intend, you need to understand which assets belong in your will and which ones must be handled through direct beneficiary designations or trusts. Here are the ten items you need to strike from your will right now.

At a Glance: Why Certain Assets Must Stay Out

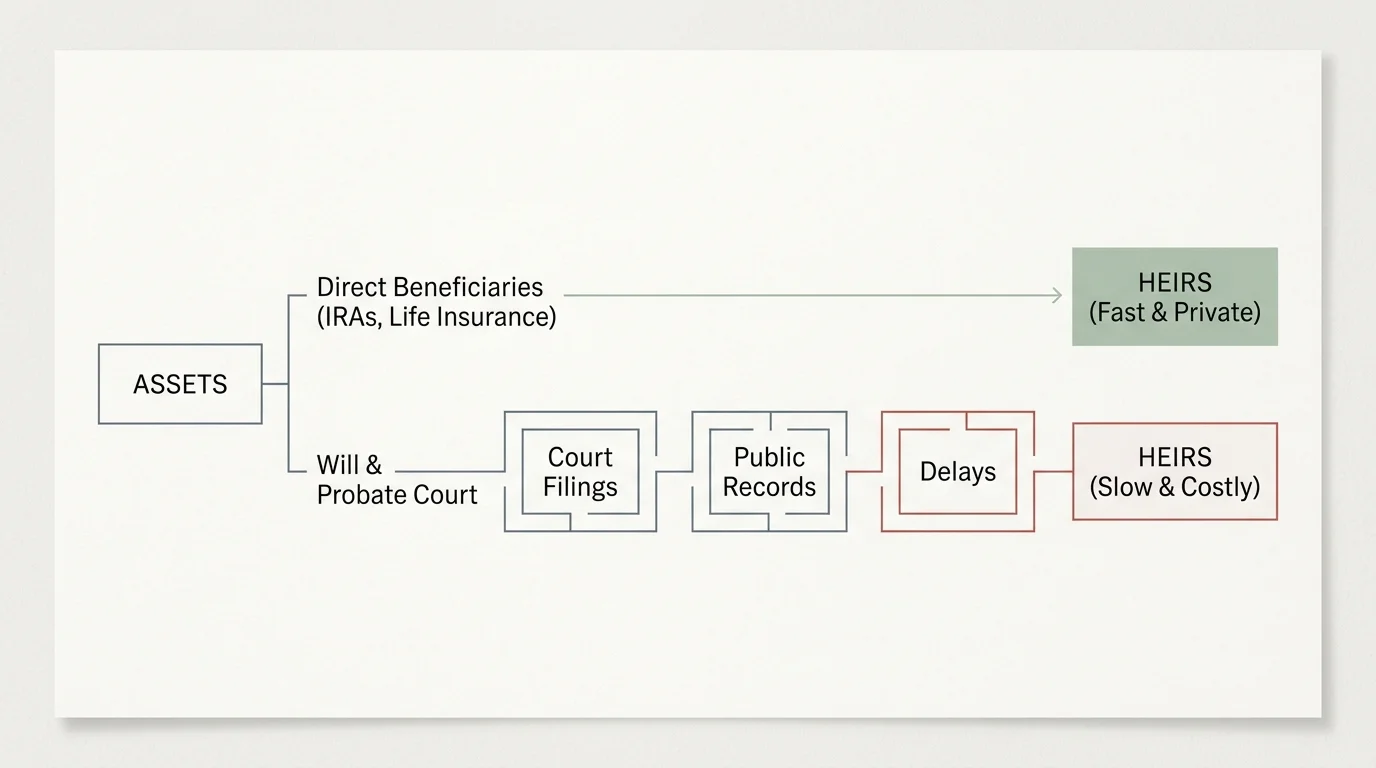

Before diving into the specific items, it helps to understand the underlying mechanics of estate planning. Putting the wrong items in your will generally causes three major problems for your heirs:

- Probate Delays: Wills must go through probate—a public, court-supervised process that can freeze assets for months or even years.

- Contradictory Instructions: If your will says one thing but a contract (like a beneficiary form) says another, the contract legally wins. Adding it to the will only creates confusion and potential litigation.

- Privacy Risks: Once filed in court, a will becomes a public record. Anyone can read it, making it the worst possible place to store sensitive passwords or digital credentials.

1. Retirement Accounts (IRAs and 401ks)

Your 401(k), 403(b), traditional IRA, and Roth IRA do not belong in your will. These accounts transfer wealth through direct beneficiary designations, which operate entirely outside the probate process. When you pass away, the financial institution simply requires a death certificate and identification from the named beneficiary to transfer the funds.

If you explicitly name your estate as the beneficiary to force these funds through your will, you create a massive tax headache for your heirs. The SECURE Act dramatically altered the rules for inherited retirement accounts, essentially eliminating the lifetime “stretch” provision for most non-spouse beneficiaries. Forcing an IRA through probate strips your heirs of flexibility and can accelerate mandatory taxes.

“The tax rules for inherited IRAs have always been complicated. But the SECURE Act… made beneficiary IRAs the worst possible assets for wealth transfer and estate planning.” — Ed Slott, CPA

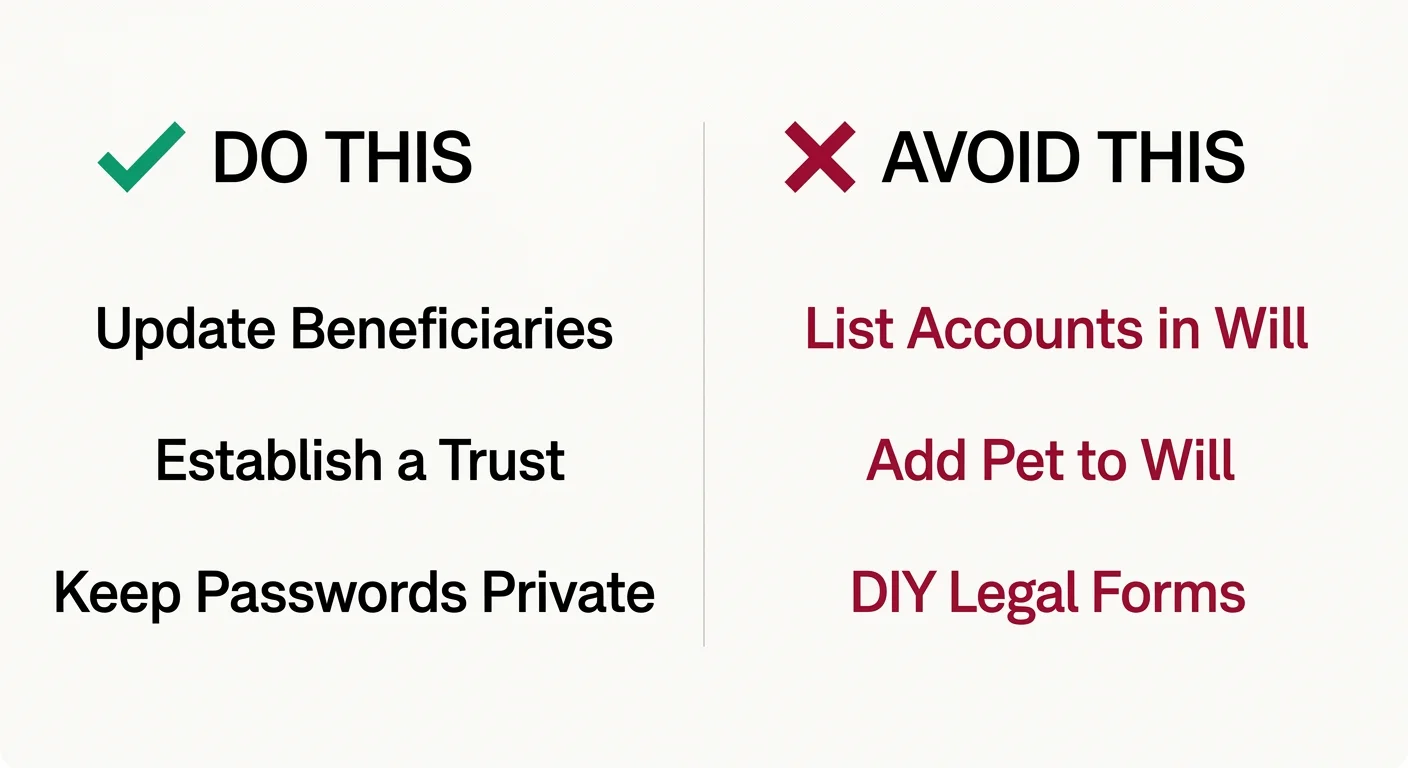

Keep retirement accounts out of your will. Instead, log into your brokerage accounts annually to review and update your primary and contingent beneficiary designations.

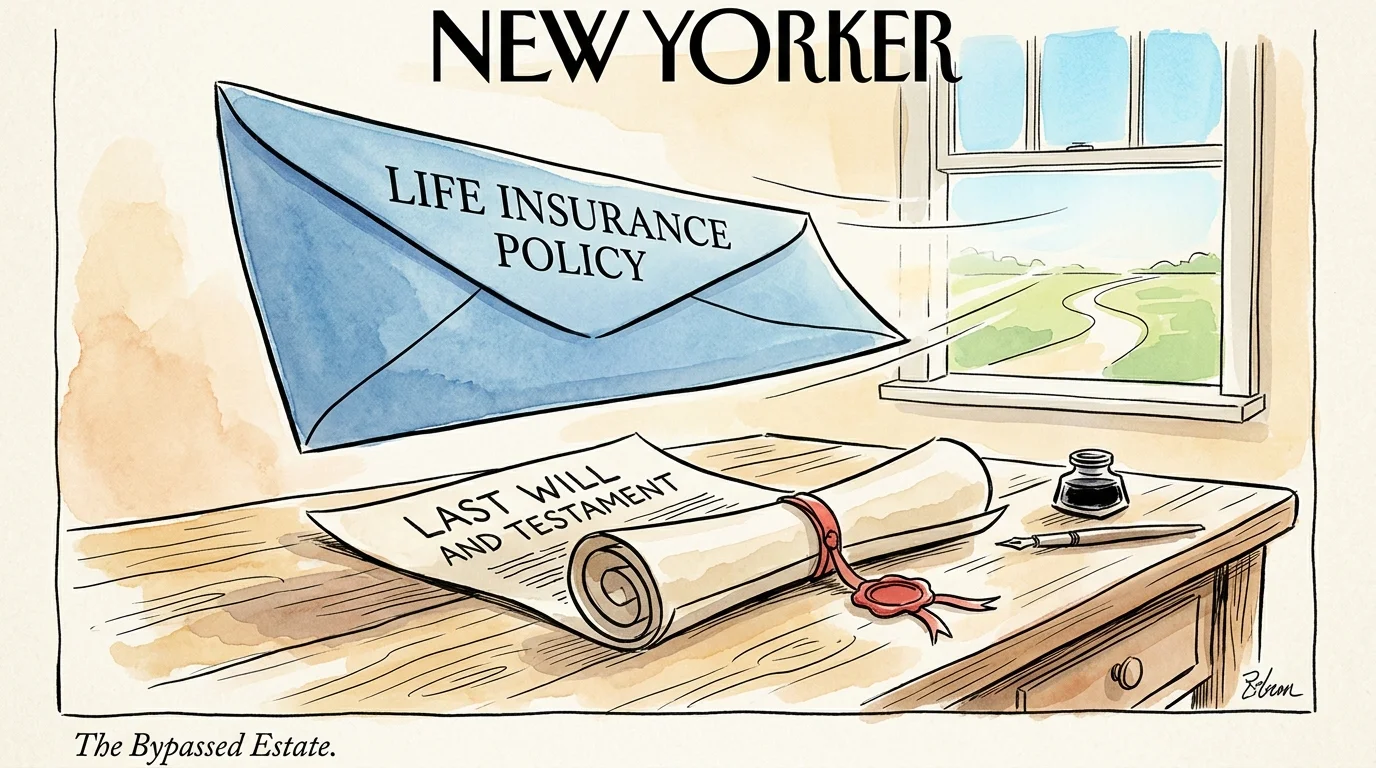

2. Life Insurance Policy Proceeds

Similar to retirement accounts, life insurance policies are legally binding contracts between you and the insurance provider. The payout goes directly to the individuals or entities you named on the policy’s beneficiary form. Naming a life insurance policy in your will accomplishes nothing legally, but it can cause severe friction if the will contradicts the policy on file.

For example, if your will leaves everything equally to your three children, but your life insurance beneficiary form only lists your oldest child, the insurance company will write the check exclusively to the oldest child. The will cannot override the contract. Ensure your policy forms reflect your current wishes and strike any mention of the policy distribution from your general will.

3. Pay-On-Death (POD) Bank Accounts

You can walk into any bank or credit union and fill out a free Pay-On-Death (POD) or Transfer-On-Death (TOD) form for your checking, savings, or brokerage accounts. This simple piece of paper ensures that the moment you pass away, ownership of the account immediately transfers to your designated beneficiary, bypassing probate entirely.

If you include a POD account in your will, you risk creating a legal conflict. If the instructions differ, the POD designation supersedes the will. To learn more about setting up proper transfer registrations for investment accounts, you can review the guidelines provided by Investor.gov.

4. Jointly Owned Property

If you own real estate, a vehicle, or a bank account jointly with someone else—specifically under “Joint Tenancy with Right of Survivorship” (JTWROS)—you cannot dictate what happens to your share in your will. By legal definition, the right of survivorship means your ownership stake automatically absorbs into the surviving owner’s stake upon your death.

If you own a beachfront property jointly with your sister and try to leave “your half” to your daughter in your will, the probate court will invalidate that clause. Your sister will take full ownership of the property. If you genuinely want your daughter to inherit your share, you must change the deed structure to “Tenancy in Common” while you are still alive, which allows you to pass your specific portion through a will.

5. Assets Placed in a Living Trust

A living revocable trust acts as a separate legal entity that holds your assets. Because the trust—not you—technically owns the house or the brokerage account, those items avoid your personal probate proceeding altogether. Listing trust-owned assets in your will defeats the entire purpose of establishing the trust.

“Living revocable trusts ensure efficient estate planning, and are an important protection in case you become disabled while you are alive.” — Suze Orman, Personal Finance Expert

Recent legislative changes have made trusts incredibly appealing for probate avoidance rather than just tax dodging. The “One Big Beautiful Bill Act” permanently increased the federal estate tax exemption to $15 million per individual starting in 2026. Because most middle-class retirees no longer have to worry about federal estate taxes, the primary function of a trust today is keeping your family out of a public, expensive probate court.

6. Digital Account Passwords

When you die, your will is filed with the local probate court and becomes a matter of public record. Anyone—including scammers and identity thieves—can pull a copy. Writing your Apple ID, online banking credentials, email passwords, or cryptocurrency wallet keys directly into your will is a catastrophic security risk.

Instead, use a secure password manager and designate a legacy contact. Most states have adopted the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), which allows you to name a digital executor. You should reference this digital executor in your will, but keep the actual passwords in a separate, secure document stored with your attorney or in a home safe.

7. Funeral and Burial Instructions

While it seems logical to put your final wishes in your final testament, practical timing makes this a bad idea. Wills are often locked in safe deposit boxes or kept at a law office; they are frequently not located and read until weeks after the person has passed away.

If your family doesn’t see the will until after the funeral, your specific requests regarding burial versus cremation, religious services, or charitable donations in lieu of flowers will be missed. Put these time-sensitive details in a separate “Letter of Instruction” and hand copies directly to your executor, your spouse, and your adult children while you are healthy.

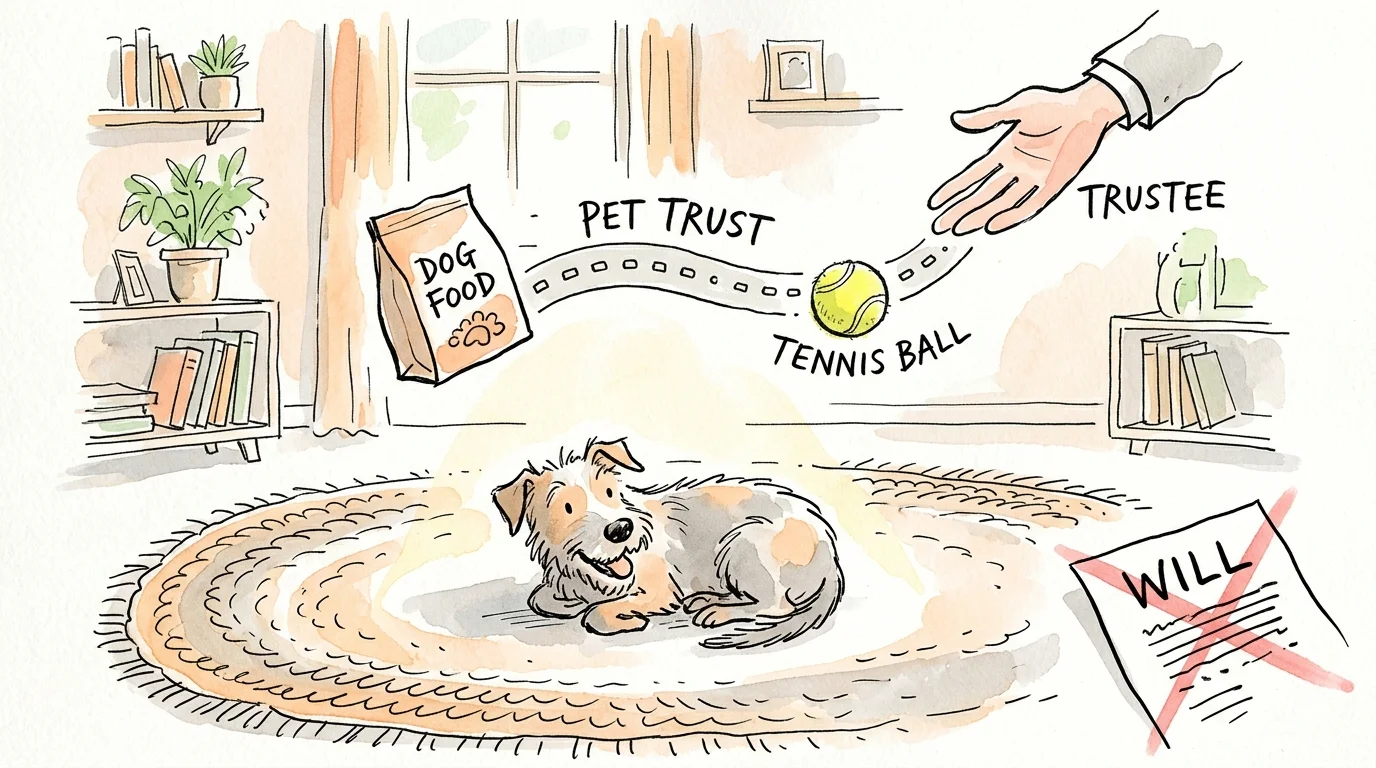

8. Direct Financial Gifts to Pets

In the eyes of the law, pets are considered property. You cannot legally leave a $10,000 inheritance to a golden retriever. If you explicitly name your pet as a financial beneficiary in your will, the probate judge will invalidate the gift, and the money will fall into your residuary estate.

To ensure your furry companion is cared for, you have two options. You can leave the animal to a trusted friend or family member along with a separate cash gift intended to cover their expenses. Alternatively, you can establish a formal Pet Trust, which legally mandates that the designated funds be used exclusively for the animal’s veterinary care and upkeep.

9. Direct Inheritances to Special Needs Dependents

Leaving a direct lump sum to a dependent with special needs can be a devastating financial mistake. Government assistance programs like Supplemental Security Income (SSI) and Medicaid have strict asset limits. An unexpected inheritance of even a few thousand dollars can instantly disqualify your loved one from receiving housing assistance, income support, and vital medical care.

Replacing that care out of pocket is profoundly expensive; for context, even the standard Medicare Part B premium sits at $202.90 per month in 2026, and full-time specialized care costs exponentially more. To provide for a disabled dependent without jeopardizing their benefits, work with an attorney to establish a Special Needs Trust (SNT). You can find more information about SSI limits directly through the Social Security Administration.

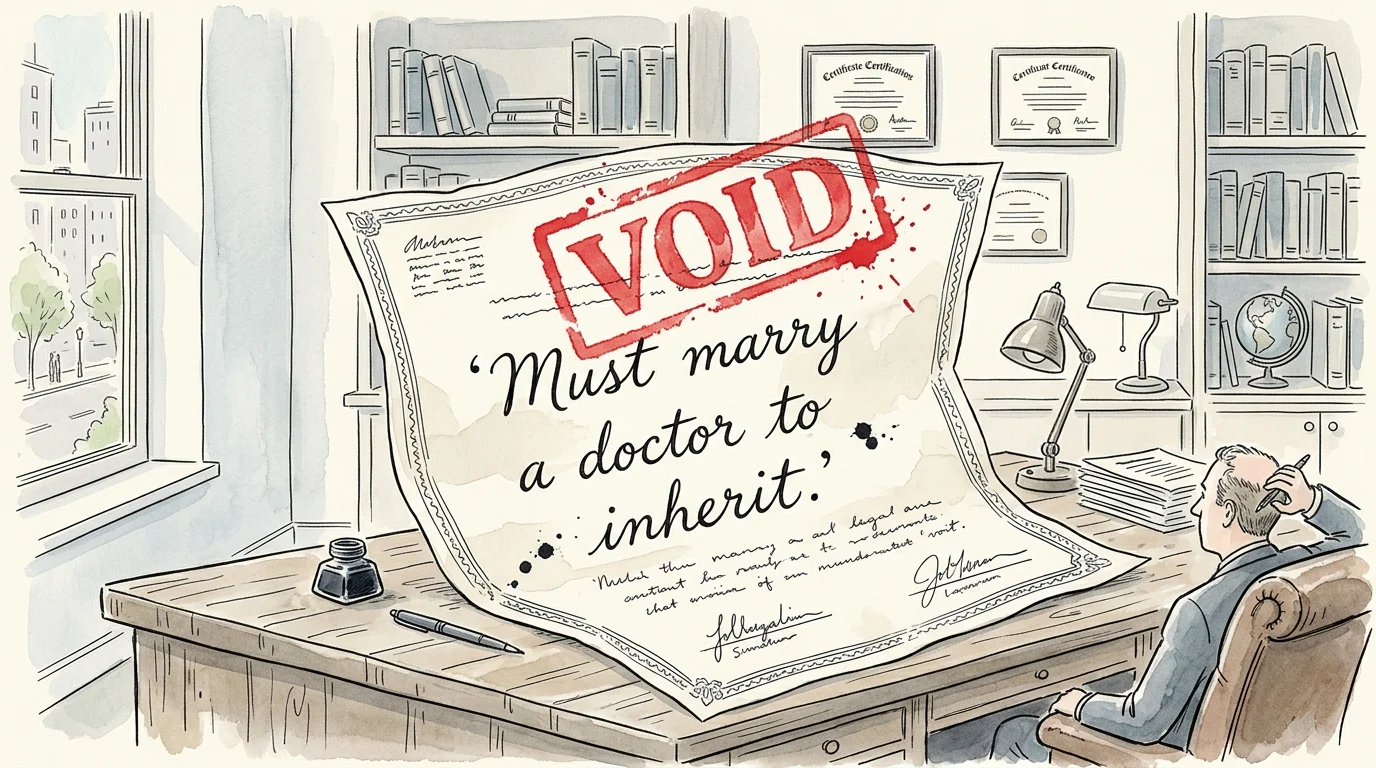

10. Unenforceable or Illegal Contingencies

You cannot use your will to force beneficiaries to perform illegal acts or comply with demands that violate public policy. For example, clauses stating “My son only inherits if he divorces his current wife” or “My daughter must change her religion to access her trust fund” will almost certainly be struck down by a probate judge.

Adding highly controlling, emotional, or spiteful contingencies to your will rarely works out the way you envision. Instead, it invites the excluded heirs to contest the will in court, draining the estate’s resources in legal fees and leaving a legacy of bitter family resentment.

When DIY Isn’t Enough

While simple estates can sometimes rely on basic online will templates, certain complexities require the skilled eye of an estate planning attorney. You should strongly consider professional legal guidance if you fall into any of these categories:

- Blended Families: If you are in a second marriage and have children from a previous relationship, DIY wills frequently fail to protect both the current spouse and the biological children.

- Business Owners: Passing a business down requires specialized succession planning to prevent sudden tax burdens or operational gridlock.

- High Net Worth: While the 2026 federal exemption is $15 million per individual, many states have much lower thresholds for state-level estate and inheritance taxes.

Avoiding Common Estate Planning Errors

Removing the wrong items from your will is only half the battle; maintaining your broader estate plan is just as critical. The most common error retirees make is treating estate planning as a “set it and forget it” task.

Major life events—births, deaths, marriages, and divorces—demand an immediate review of your documents. A surprisingly common disaster occurs when a retiree passes away, only for the family to discover that a multi-million dollar 401(k) was left to an ex-spouse from thirty years ago because the beneficiary form was never updated after the divorce. Furthermore, ensure your chosen executor actually knows where your original documents are located; storing a will in a bank safe deposit box often traps the document, as the bank may require probate court approval for the executor to open the box.

| Asset Type | Does It Belong In a Will? | Proper Transfer Method |

|---|---|---|

| Real Estate (Sole Ownership) | Yes | Will or Living Trust |

| 401(k)s and IRAs | No | Direct Beneficiary Designation Form |

| Life Insurance Payouts | No | Policy Beneficiary Form |

| Jointly Owned Property (JTWROS) | No | Automatically passes to surviving owner |

| Digital Passwords | No | Digital Legacy Contact / Secure Password Manager |

Estate planning gives you the power to protect your loved ones from unnecessary stress during their hardest moments. By cleaning up your will and relying on direct beneficiary designations, trusts, and transfer-on-death registrations, you streamline the transfer of your wealth. Take time this month to review your documents, update your beneficiaries, and ensure your legacy plan reflects your actual wishes.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA. Last updated: July 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.

Great information, essential in planning for Final Arrangements. Thank you !