You can protect your retirement income by learning how to navigate the persistent $438 monthly Social Security gap between men and women. Recent 2026 data reveals that female retirees receive an average of $1,760 per month, falling significantly short of the $2,198 average benefit paid to men. This $5,254 annual shortfall stems from historical wage differences, caregiving career interruptions, and longer life expectancies that stretch smaller balances over more years. With the program’s trust funds facing potential depletion around 2032, looming benefit reductions threaten to disproportionately impact women. Fortunately, by strategically timing your claim, leveraging spousal or survivor rules, and maximizing your tax-advantaged catch-up contributions, you can bridge this deficit and safeguard your financial independence.

The True Scope of the Gender Retirement Gap

The numbers surrounding retirement income reveal a stark reality for female retirees. Women currently account for 55.1 percent of Social Security recipients, yet they receive significantly less per person because benefits are permanently tied to lifetime earnings. According to a June 2026 analysis by FinanceBuzz, the national average gap sits at $438 per month. That monthly deficit cascades into a $5,254 annual shortage during years when medical costs and inflation tend to bite the hardest.

This income disparity pushes a larger percentage of women toward financial vulnerability. Between 2023 and 2024, the poverty rate for older women rose to 16.2 percent, whereas the rate for older men remained steady at 13.5 percent. When you live longer with fewer resources, every dollar matters. Understanding why this gap exists empowers you to counteract it through strategic claiming decisions and proactive financial planning.

Why Women Receive Smaller Social Security Checks

The Social Security Administration calculates your retirement benefit using your highest 35 years of indexed earnings. If you do not have 35 full years of earnings, the administration inserts zeros for the missing years. These zero-earning years drag down your overall average, creating a permanent reduction in your monthly payout. Several systemic factors disproportionately affect women in this calculation.

First, caregiving responsibilities frequently pull women out of the full-time workforce. Whether stepping away to raise young children or taking time off to care for aging parents, these career interruptions replace prime earning years with zeros on a Social Security record. Even when women remain in the workforce, they often shift to part-time roles that offer lower pay and fewer opportunities for upward mobility.

Second, the historical wage gap leaves a lasting imprint on retirement checks. On average, women earn about 80 cents for every dollar earned by men. Over a 35-year career, that 20 percent deficit compounds into hundreds of thousands of dollars in lost wages, which translates directly into a lower Primary Insurance Amount at retirement.

The 2032 Threat: Why the Gap Could Grow

A looming crisis threatens to amplify the existing gender gap. The Social Security trust funds are currently projected to face depletion around 2032. If Congress does not intervene to stabilize the program, benefits could face an automatic reduction of roughly 21 to 23 percent across the board.

An across-the-board cut would hit female retirees much harder than male retirees. Elderly women rely more heavily on Social Security as their primary source of income. Unmarried women aged 65 and older are far less likely to have significant private pension income or vast investment portfolios. Stripping 20 percent from a $1,760 monthly check cuts deeply into basic survival needs—like housing, food, and utilities—whereas a male retiree receiving $2,198 has slightly more buffer to absorb the blow.

“Claiming early does not protect you from future benefit cuts.” — Suze Orman, Personal Finance Expert

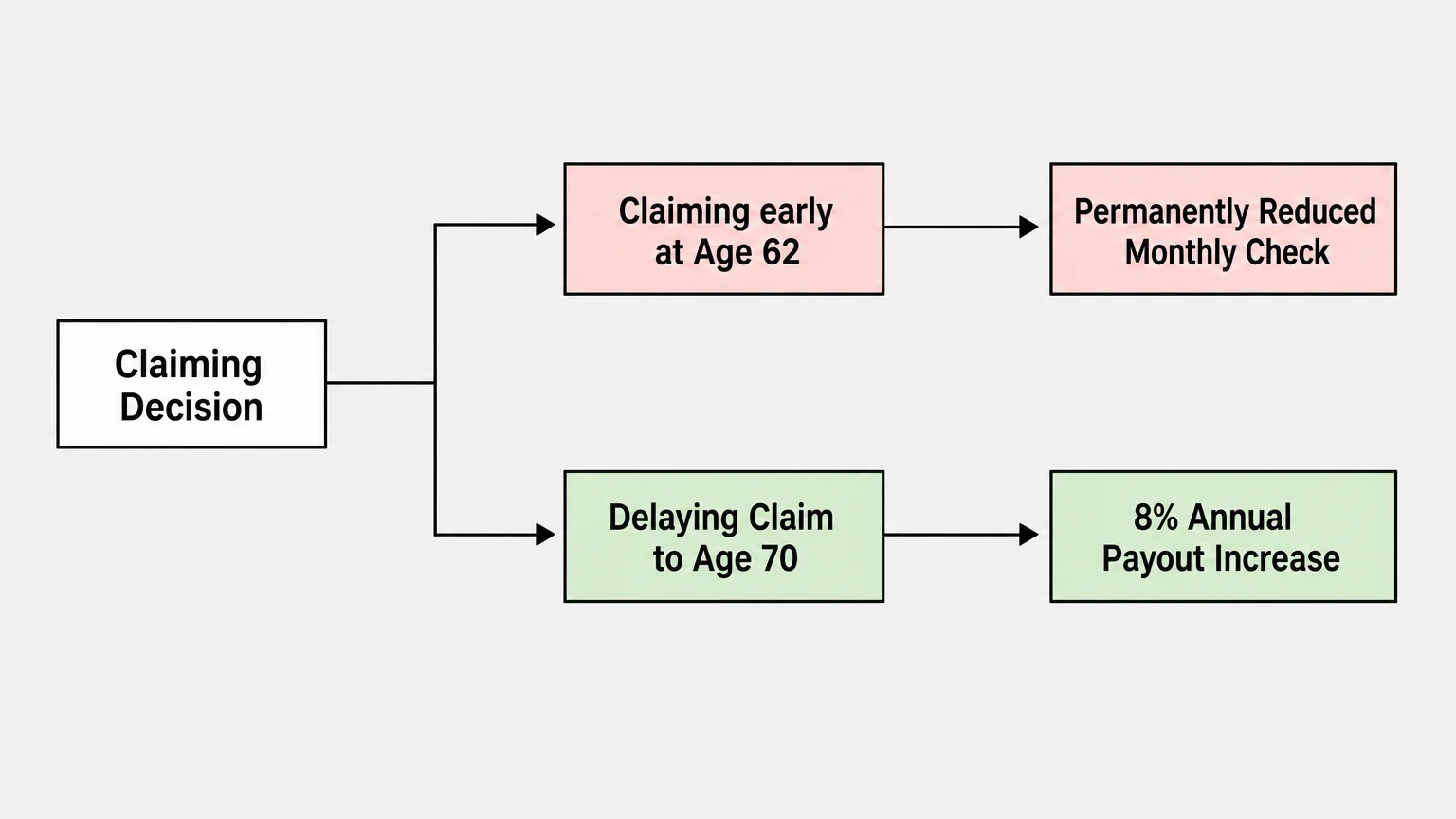

Panicking over potential 2032 cuts often drives retirees to claim their benefits as early as possible at age 62. However, locking in a permanently reduced base rate ensures that any future percentage-based cuts will hurt even more. Your best defense against future reductions is building a higher baseline benefit today.

Essential Strategies for Women to Maximize Benefits

You have more control over your Social Security payout than you might think. By utilizing the specific rules built into the system, you can legally increase your lifetime benefits and narrow the gender gap.

- Delaying Your Claim: Your Full Retirement Age (FRA) is between 66 and 67, depending on your birth year. If you can wait to claim benefits until age 70, your monthly check grows by a guaranteed 8 percent for every year you delay past your FRA. This guaranteed return is one of the most powerful tools available to increase your baseline income.

- Leveraging Spousal Benefits: If your spouse earned significantly more than you, you might be eligible for a spousal benefit. At your Full Retirement Age, you can receive up to 50 percent of your spouse’s FRA benefit amount. The Social Security Administration will automatically pay you whichever amount is higher: your own earned benefit or the spousal benefit.

- Filing as an Ex-Spouse: If you are divorced, you can still claim benefits based on your ex-spouse’s earnings record. You must have been married for at least 10 consecutive years, and you must currently be unmarried. Claiming on an ex-spouse’s record does not reduce their benefit, nor does it impact their current spouse.

- Maximizing Survivor Benefits: Widows face unique financial challenges, but the survivor rules provide a crucial safety net. As a widow, you can step into your late spouse’s exact monthly benefit amount if it is larger than your own. Strategic planners often have the higher-earning spouse delay claiming until age 70 specifically to leave behind the maximum possible survivor benefit for the remaining spouse.

Filling the Void: Building Your Independent Safety Net

Because Social Security was never designed to replace 100 percent of your working income, you must build an independent safety net to cover the shortfall. With the 2026 Cost-of-Living Adjustment (COLA) sitting at a modest 2.8 percent, relying on government adjustments alone will not maintain your purchasing power against rising living expenses.

Take full advantage of current tax-advantaged retirement accounts while you are still working. The Internal Revenue Service (IRS) increased the standard 401(k) contribution limit to $24,500 for 2026. If you are age 50 or older, you can utilize an additional $8,000 catch-up contribution. Furthermore, the SECURE 2.0 Act introduced a new “super catch-up” provision for 2026, allowing workers aged 60 to 63 to contribute an extra $11,250 to their workplace plans.

If you do not have a workplace plan, Individual Retirement Accounts (IRAs) offer another powerful savings vehicle. For 2026, the standard IRA contribution limit is $7,500, with an expanded total limit of $8,600 available for individuals age 50 and older.

You must also budget aggressively for rising healthcare costs. Medicare.gov outlines that the standard Medicare Part B premium for 2026 is $202.90 per month. Because Medicare premiums are deducted directly from your Social Security check before the money ever hits your bank account, your actual net income will be lower than your gross award amount. A smaller gross benefit means Medicare premiums consume a larger percentage of your overall fixed income.

Avoiding Common Errors

Retirement planning requires precision. Avoid these common missteps that permanently reduce women’s wealth in retirement.

First, do not ignore the earnings test if you plan to work while claiming early benefits. If you claim Social Security before your Full Retirement Age and continue to work, the administration will withhold $1 for every $2 you earn above the annual limit. For 2026, that earnings limit is set at $24,480. While those withheld benefits are eventually credited back to your record after you reach FRA, the temporary reduction can disrupt your monthly cash flow.

Second, failing to coordinate a claiming strategy with your spouse leaves money on the table. Married couples should look at their combined life expectancy rather than individual break-even points. The higher earner should almost always delay their claim as long as possible to protect the surviving spouse, who will inherit the single highest benefit check when the first spouse passes away.

When DIY Isn’t Enough

While basic retirement planning can often be managed independently, certain scenarios require professional intervention. Consider hiring a fee-only fiduciary financial planner if you encounter any of the following complexities.

If you have been widowed or divorced multiple times, the rules surrounding which record to claim—and when—become highly intricate. A professional can run specialized software to determine the exact month you should claim to maximize your lifetime payout.

Tax planning is another area where professional guidance pays for itself. Required Minimum Distributions (RMDs) from traditional IRAs can easily push a single widow into a higher tax bracket, a phenomenon often called the “Widow’s Penalty.”

“Taxes are the single biggest factor that separates people from their retirement dreams.” — Ed Slott, CPA and Retirement Tax Expert

A professional can help you execute Roth conversions during your lower-income years, effectively defusing the tax bomb waiting inside your traditional 401(k) or IRA. Transitioning funds into a tax-free Roth account ensures that your future withdrawals will not trigger higher taxes or increased Medicare Part B IRMAA surcharges.

The gender retirement gap is a formidable challenge, but it is not insurmountable. By understanding how the Social Security formula works, anticipating the potential program changes in 2032, and taking aggressive steps to fund your own retirement accounts, you can build a resilient financial foundation. Focus on maximizing your high-earning years, delaying your benefits when possible, and staying informed about changing tax and contribution laws. Your future self will thank you for the security and independence you build today.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.