Millions of older Americans leave valuable benefits unclaimed because they simply do not know to apply for state-level financial assistance. While federal programs like Social Security provide your foundational retirement security, state pension supplements act as crucial financial shock absorbers. These lesser-known programs can cover expensive Medicare premiums, drastically reduce prescription drug costs, and add direct cash supplements to your monthly income. Navigating the maze of state-specific eligibility rules takes effort, but the payoff can permanently improve your retirement budget. Whether you need relief from property taxes or want to eliminate your monthly Medicare Part B premium, state agencies offer targeted assistance programs designed to keep more money in your pocket.

The Hidden Value of State Supplementary Payments (SSP)

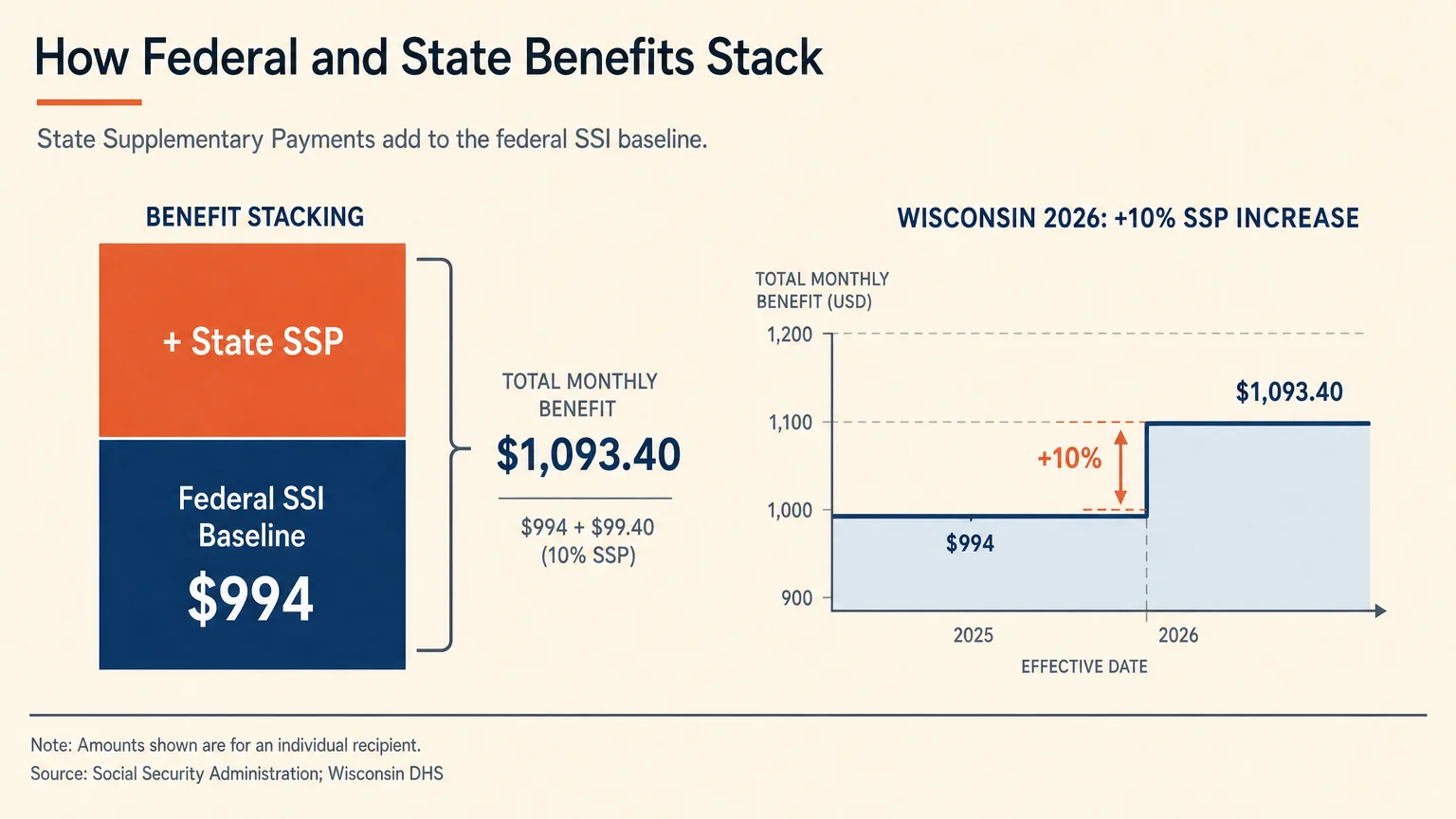

When you hear the term pension, you likely envision a traditional corporate retirement plan or your monthly Social Security check. However, the federal government and individual states coordinate to provide additional cash assistance to older adults through the Supplemental Security Income program. Federal SSI provides a basic monthly income to seniors and individuals with disabilities who have limited resources. Following the 2.8 percent cost-of-living adjustment for 2026, the maximum federal SSI payment reached $994 a month for individuals and $1,491 for married couples.

While the federal government establishes this baseline, many states recognize that $994 barely covers housing in most cities, let alone groceries and utilities. To bridge this gap, states offer a State Supplementary Payment. This is a direct cash supplement added to your federal benefit.

State programs vary significantly in their generosity and administration. Wisconsin, for example, recognized the sting of inflation and increased its SSI State Supplementary payment by 10 percent effective May 2026. California provides its own robust state supplement that adds hundreds of dollars to the federal baseline for eligible residents.

The administration of these payments also differs by location. In some states, the Social Security Administration handles the state supplement directly; you receive one combined payment each month. In other jurisdictions, the state manages its own supplement, meaning you receive two separate deposits. Applying for federal SSI typically triggers your evaluation for the state supplement, but you must actively apply for the foundational federal benefit first.

Medicare Savings Programs: Protecting Your Monthly Premium

Your Medicare coverage provides essential health security, but it comes with substantial out-of-pocket costs. Most retirees pay a standard Medicare Part B premium of $202.90 per month in 2026. Over the course of a year, that premium drains nearly $2,435 directly from your Social Security benefits. If you live on a tight budget, losing that much income to premiums forces difficult choices between healthcare and daily living expenses.

State Medicaid offices administer Medicare Savings Programs to help low-income seniors shoulder these costs. Despite the strict-sounding income requirements, these programs feature generous exemptions that make them more accessible than many retirees realize. The programs fall into three primary tiers:

- Qualified Medicare Beneficiary (QMB): This comprehensive tier pays your Part A premiums, Part B premiums, deductibles, coinsurance, and copayments. Medical providers are legally prohibited from billing QMB participants for Medicare-covered services. Federal guidelines generally limit QMB eligibility to individuals with incomes around 100 percent of the Federal Poverty Level, carrying a resource limit of $9,950 for an individual and $14,910 for a married couple in 2026. However, progressive states expand these limits. New York allows individuals with a monthly income up to $1,856 to qualify for QMB in 2026.

- Specified Low-Income Medicare Beneficiary (SLMB): This program specifically pays your Part B premium. It targets individuals with incomes slightly above the QMB limits.

- Qualifying Individual (QI): Like SLMB, the QI program pays your Part B premium, but it caters to those with slightly higher incomes. Funding for QI is limited, so states approve applications on a first-come, first-served basis.

Beyond the direct premium savings, enrolling in any Medicare Savings Program triggers a massive secondary benefit: automatic enrollment in the federal Extra Help program for prescription drugs.

State Pharmaceutical Assistance Programs (SPAPs)

Prescription drug costs consistently rank as one of the top financial stressors for older Americans. Even with Medicare Part D, copayments for specialty tier medications and the coverage gap can decimate a retirement budget. Recognizing this burden, many states fund their own State Pharmaceutical Assistance Programs to wrap around and supplement Medicare Part D.

The most common misconception about SPAPs is that they only serve those living in deep poverty. Many states explicitly design these programs to protect middle-class retirees from catastrophic drug costs.

Consider New York’s Elderly Pharmaceutical Insurance Coverage (EPIC) program. The 2026 income limits for EPIC are remarkably broad: up to $75,000 for a single person and $100,000 for a married couple. EPIC provides secondary coverage after your Medicare Part D deductible is met, drastically reducing copayments at the pharmacy counter.

Pennsylvania offers similar relief through its PACE and PACENET programs. PACENET specifically targets middle-income seniors, assisting single residents with incomes up to $33,500 and married couples with incomes up to $41,500 in 2026. Pennsylvania also recently maintained a moratorium ensuring that seniors do not lose their PACENET eligibility simply because a Social Security cost-of-living adjustment nudged them slightly over the income threshold.

If your state offers an SPAP, joining provides multiple layers of protection. These programs lower your out-of-pocket costs, help pay your Part D monthly premiums, and grant you a Special Enrollment Period. This enrollment period allows you to switch your Medicare Part D plan outside of the standard fall open enrollment window if you find a plan that better covers your specific medications.

Property Tax Relief, Freezes, and Deferrals

Paying off your mortgage represents a major retirement milestone, but homeownership comes with a perpetual expense: property taxes. As property values rise, local municipalities increase tax assessments, forcing many seniors on fixed incomes to consider selling their family homes. To combat this, states and local municipalities offer specialized property tax relief programs.

These programs typically fall into four categories:

- Circuit Breaker Programs: Named after the electrical device that stops a power surge, these programs stop your property tax bill from overloading your budget. If your property taxes exceed a certain percentage of your income, the state refunds the difference as a tax credit.

- Tax Freezes: Some jurisdictions freeze the assessed value of your home or your property tax rate on the day you turn 65. While your neighbors face annual tax hikes, your bill remains locked at your baseline rate. New Jersey offers a robust Senior Freeze program that reimburses eligible seniors for any property tax increases they experience once enrolled.

- Tax Deferrals: A deferral program allows you to delay paying some or all of your property taxes until you sell your home or pass away. The local government essentially loans you the tax money, attaching a lien to the property to recoup the funds later. Illinois recently expanded its Senior Citizens Real Estate Tax Deferral Program, raising the maximum household income limit to $75,000 for tax year 2026.

- Exemptions: An exemption directly lowers the assessed value of your home before the tax rate is applied. Most states offer a standard senior exemption that shaves a fixed dollar amount or percentage off your home’s taxable value.

Since property taxes fund local services, you usually apply for these programs through your county assessor or municipal tax office rather than a federal agency.

Navigating the Intersection of State and Federal Benefits

Understanding how federal and state benefits interlock allows you to build a comprehensive safety net. Government assistance operates in layers; federal programs form the base, while state programs fill the gaps.

| Financial Challenge | Federal Solution | State-Level Supplement |

|---|---|---|

| Basic Income Shortfall | Supplemental Security Income (SSI) | State Supplementary Payment (SSP) |

| Medicare Premiums | Standard Medicare Coverage | Medicare Savings Programs (QMB, SLMB, QI) |

| Prescription Drug Costs | Medicare Part D / Extra Help | State Pharmaceutical Assistance Programs (SPAP) |

| Housing Affordability | HUD Programs / Section 8 | Property Tax Freezes and Circuit Breakers |

“The simplest definition of retirement security is having enough income to cover your basic living expenses for the rest of your life.” — Jean Chatzky, Financial Educator

Professional vs. Self-Guided: Securing Your Benefits

Applying for state pension supplements and auxiliary benefits involves bureaucratic paperwork, strict deadlines, and complex financial disclosures. You must decide whether to tackle the application process yourself or enlist professional help. Here are four specific scenarios to guide your decision:

Scenario 1: The Straightforward Applicant (Self-Guided)

If your primary source of income is Social Security, you do not own multiple properties, and you fall clearly below the income limits for a Medicare Savings Program, you can usually apply on your own. State health insurance assistance programs offer free, unbiased counselors who can walk you through the standard forms at no cost.

Scenario 2: Borderline Income with High Medical Costs (Professional)

If your income slightly exceeds the threshold for a State Pharmaceutical Assistance Program, do not give up. Certain states allow you to deduct specific medical expenses or health insurance premiums from your gross income to qualify. A financial planner or elder law attorney knows exactly which deductions the state permits, potentially bringing your countable income below the eligibility line.

Scenario 3: Real Estate Rich but Cash Poor (Professional)

Many retirees find themselves living in a home that has skyrocketed in value, yet they struggle to afford groceries. Applying for state assistance when you hold substantial illiquid assets requires careful navigation. An elder law professional can help you structure your assets, explore property tax deferrals, and ensure your home equity does not disqualify you from vital cash supplements.

Scenario 4: Married Couple Requiring Long-Term Care (Professional)

When one spouse needs nursing home care and the other remains in the community, the financial stakes are enormous. State Medicaid programs offer spousal impoverishment rules designed to prevent the healthy spouse from going bankrupt. Because these rules are notoriously complex and vary by state, hiring an elder law attorney is virtually mandatory to protect your life savings while securing state benefits.

Common Mistakes to Avoid

Navigating government benefit programs requires precision. Avoid these frequent missteps to ensure you receive all the assistance you deserve.

Assuming You Earn Too Much Money

The most damaging mistake retirees make is self-disqualifying. They look at federal poverty guidelines and assume state programs use the same austere metrics. As demonstrated by New York’s EPIC program, which accepts married couples earning up to $100,000, many state supplements target the middle class. Always verify your specific state’s income limits before walking away.

Overlooking Asset Disregards

When a state program imposes an asset or resource limit, applicants often panic, assuming they must count everything they own. In reality, most state programs disregard your primary residence, one vehicle, personal belongings, and burial plots. When the state asks for your resources, only declare the countable assets required by the application.

Missing Annual Recertification Deadlines

State benefits are rarely a permanent guarantee. Most programs require annual recertification to prove you still meet the income and asset guidelines. If you miss the mail notice and fail to submit your renewal forms, the state will abruptly terminate your premium assistance or prescription drug coverage. Create a calendar system to track your recertification dates.

Failing to Report Life Changes

If your spouse passes away, your living arrangement changes, or you receive an unexpected financial windfall, you must report these changes to the administering state agency. Failing to do so can result in overpayments, and the state will aggressively claw back those funds from your future Social Security checks.

Frequently Asked Questions

Do state supplement programs affect my Social Security retirement benefits?

No. State supplementary payments, Medicare Savings Programs, and property tax relief programs do not reduce your earned Social Security retirement benefits. These programs act as separate additions to your financial foundation. However, receiving a state cash supplement might alter your eligibility for other strict need-based programs like the Supplemental Nutrition Assistance Program.

How do I apply for a Medicare Savings Program?

You must apply through your state’s Medicaid office, not through the federal Medicare agency. You can initiate the process by calling your state Medicaid agency or working with a local counselor from the National Council on Aging network. They will provide the specific application forms required for your jurisdiction.

Can I receive both Extra Help and a State Pharmaceutical Assistance Program?

Yes; in fact, the programs are designed to work together. If you qualify for the federal Extra Help program, your state pharmaceutical program will act as a secondary payer. Extra Help will cover the bulk of your drug costs, and your state program will step in to cover remaining copayments or premiums, driving your out-of-pocket costs down to nearly zero.

Protecting your retirement nest egg requires more than just smart investing; it requires diligent management of your expenses. State pension supplements, Medicare Savings Programs, and property tax relief initiatives exist specifically to ease the financial pressure of aging. Take a proactive approach this week by visiting your state’s department of aging website or scheduling a call with a local health insurance counselor. A few hours of paperwork could secure thousands of dollars in annual savings.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.