Every October, the Social Security Administration announces the annual cost-of-living adjustment (COLA), directly dictating how much your monthly benefits will increase the following year. With recent projections pointing toward a 3.8% bump for 2027, tracking the inflation data now gives you a crucial head start on your retirement budget. You do not have to wait until autumn to understand the shifting financial landscape. Early indicators already reveal how persistent inflation and rising Medicare premiums will likely impact your bottom line. By monitoring the right economic markers through the summer months, you can anticipate your actual take-home pay and make proactive adjustments to your household spending long before the new rates take effect.

Current 2027 COLA Projections: What the Data Shows

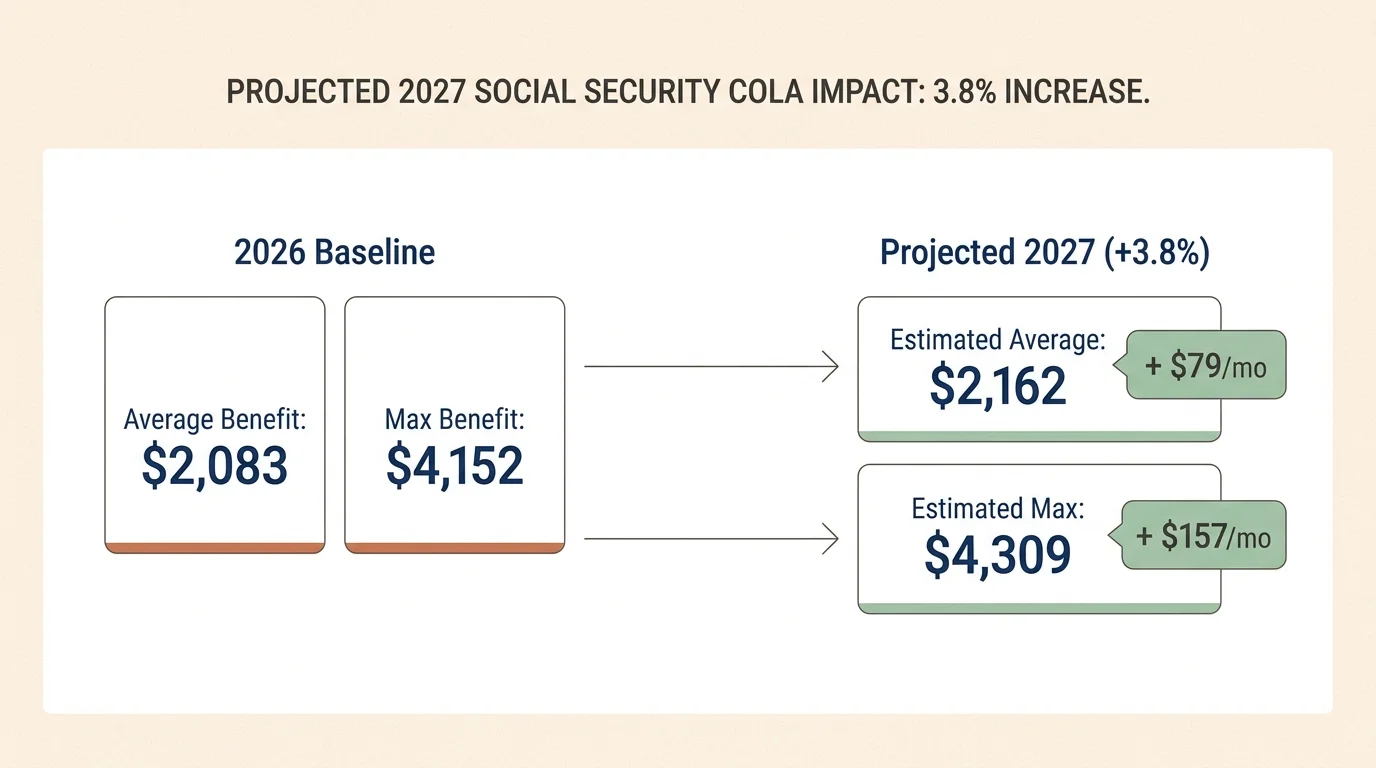

The Social Security landscape shifts continuously; early estimates help you navigate those changes. In October 2025, the Social Security Administration finalized a 2.8% increase for 2026, which pushed the average monthly retirement benefit to approximately $2,083. While that adjustment offered necessary relief, many retirees quickly found that everyday expenses outpaced the modest bump.

As of mid-2026, the economic environment suggests a more substantial increase on the horizon for 2027. Recent projections from nonpartisan advocacy groups, including The Senior Citizens League, estimate the 2027 COLA will land near 3.8%. This projected rate represents a noticeable step up from 2026, driven by sticky inflation in sectors like housing, groceries, and medical care.

Applying a 3.8% increase to the current average monthly benefit of $2,083 yields an estimated gross boost of roughly $79 per month. For those receiving the maximum benefit at full retirement age—which reached $4,152 in 2026—a 3.8% bump translates to an additional $157 monthly. However, looking only at the gross increase paints an incomplete picture. You must view these early percentages as a baseline rather than a final promise; subsequent inflation reports will inevitably shift the final number.

The Mechanics of the COLA Calculation

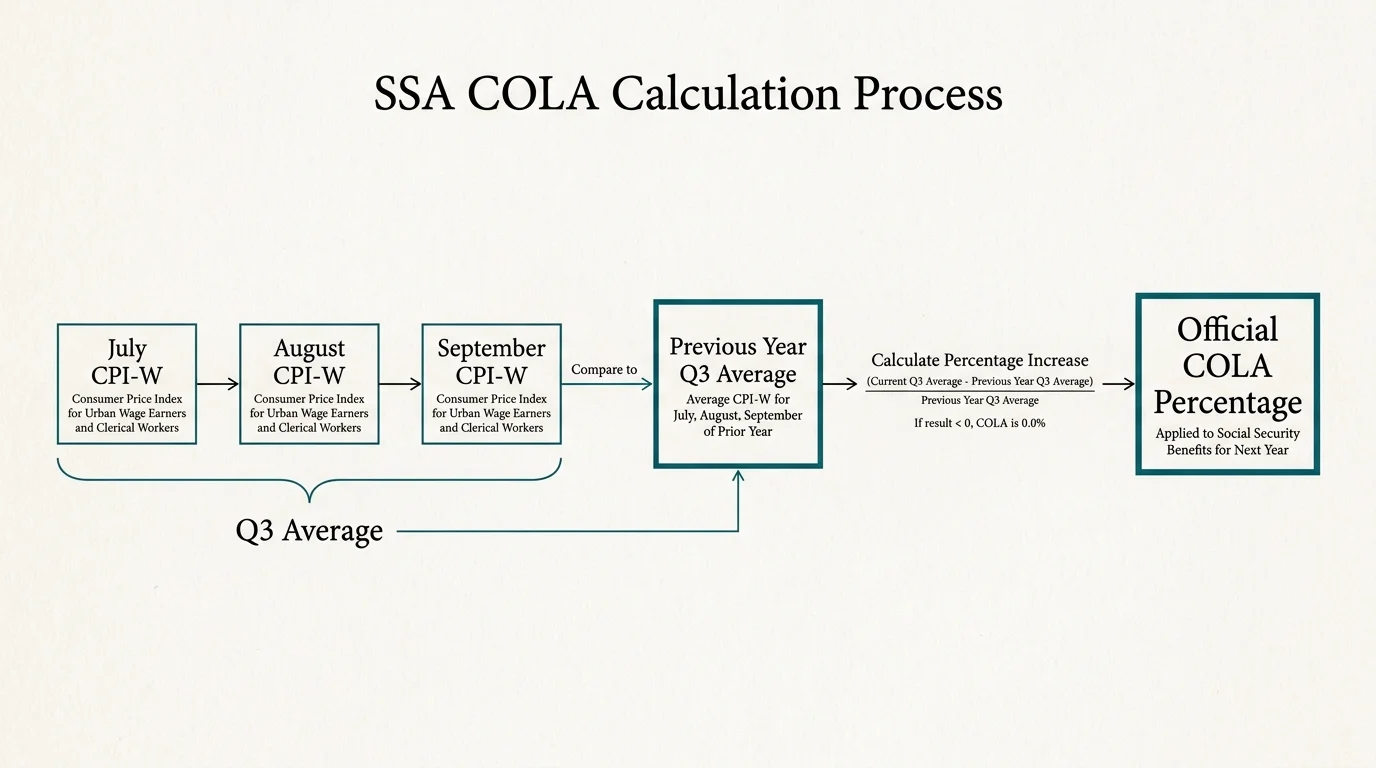

Understanding how the government calculates your annual raise allows you to track the exact metrics that matter. The Social Security Administration (SSA) does not base the COLA on a full year of inflation data. Instead, they rely strictly on a specific three-month window: July, August, and September.

The designated measurement tool is the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), published monthly by the Bureau of Labor Statistics. The formula operates through a simple comparison; the government averages the CPI-W readings from the third quarter of the current year and compares that figure to the third-quarter average from the previous year.

If the current year’s average exceeds the previous year’s, the percentage difference becomes the official COLA for the upcoming year. If prices drop and the index falls, your benefits do not decrease—the COLA simply remains at zero.

To track the 2027 prediction yourself, you must pay attention to the inflation reports released in August, September, and October of 2026. The mid-October report officially locks in the September data, prompting the Social Security Administration to formally announce the finalized percentage.

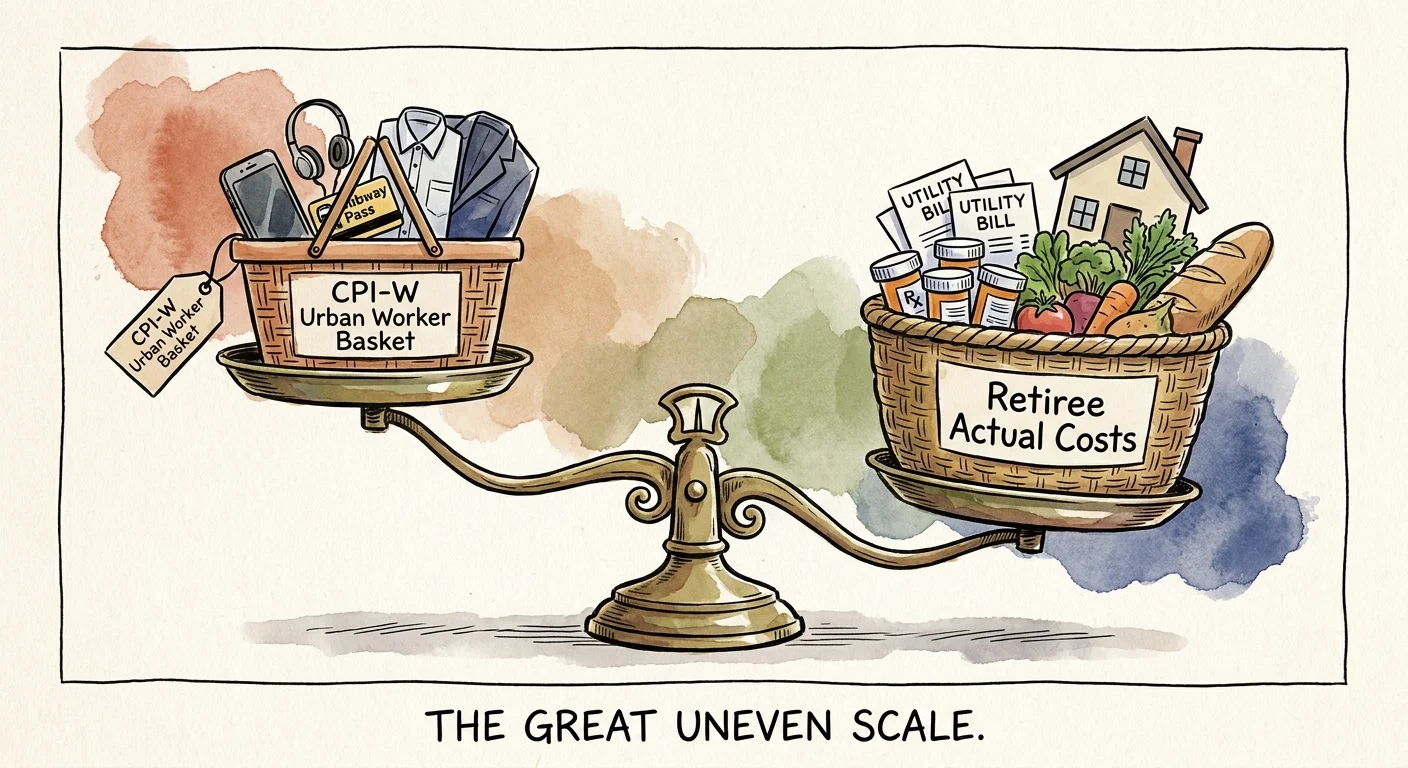

Why the CPI-W Might Not Reflect Your Actual Costs

You might notice a disconnect between the official COLA announcements and your actual checking account balance. This discrepancy stems from the fundamental design of the CPI-W. The index specifically tracks the spending habits of younger, working-age urban populations; it does not accurately weight the expenses that consume a retiree’s budget.

Seniors typically spend a significantly higher percentage of their income on healthcare, prescription drugs, and housing compared to the general workforce. Working-age individuals spend more on transportation, apparel, and education. When fuel costs drop but medical costs surge, the CPI-W might show mild overall inflation, resulting in a lower COLA—even as your personal out-of-pocket expenses skyrocket.

“The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures.” — Warren Buffett, Investor and CEO of Berkshire Hathaway

Many retirement advocates push for the adoption of the Consumer Price Index for the Elderly (CPI-E), an experimental index which heavily weights healthcare and housing. Until legislative changes occur, you must plan your finances knowing the official COLA may lag behind your true cost of living.

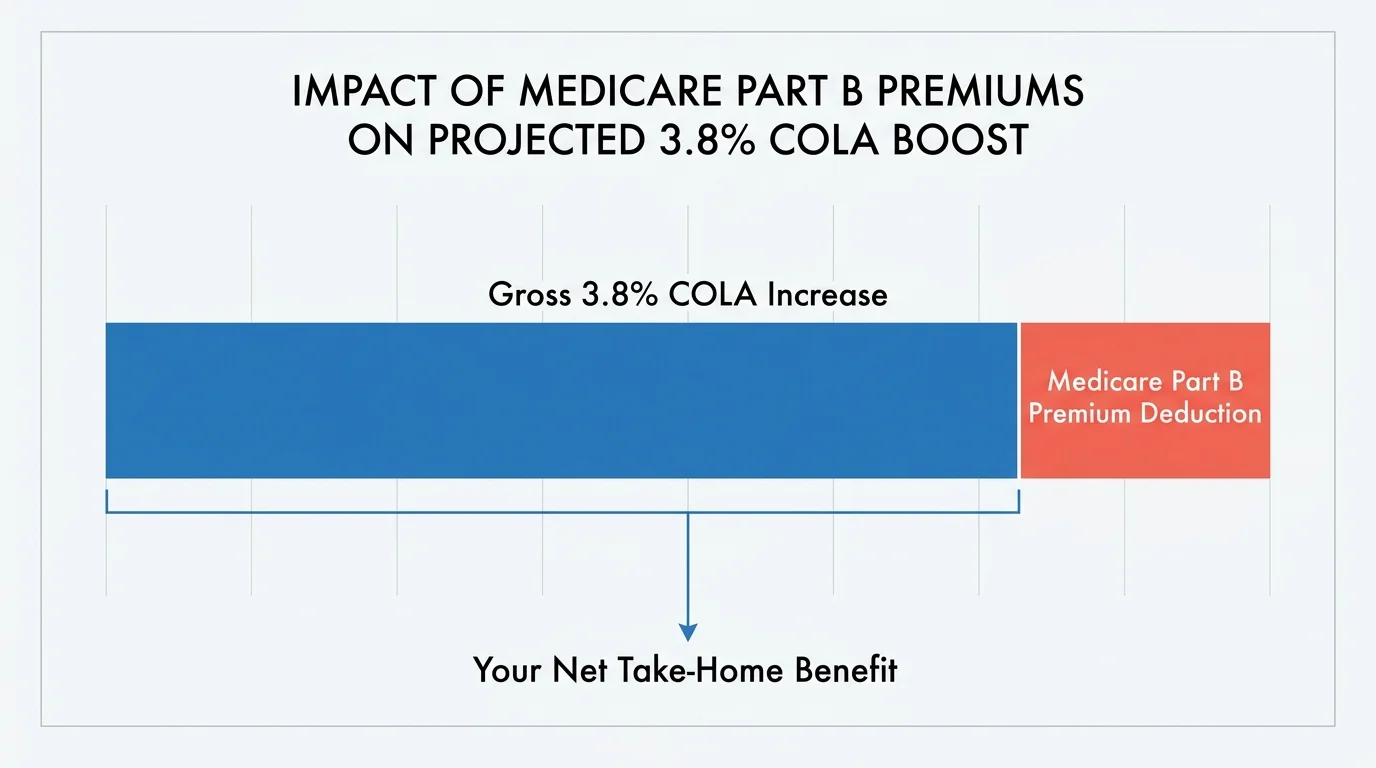

The Medicare Part B Factor: Calculating Your True Net Income

Your Social Security check and your Medicare coverage operate in tandem. For the vast majority of retirees, the Centers for Medicare & Medicaid Services deducts Medicare Part B premiums directly from Social Security payments before the funds ever hit a bank account.

In 2026, the standard Medicare Part B premium rose sharply to $202.90 per month. Additionally, the Medicare Part A inpatient hospital deductible climbed to $1,736 per benefit period. When the Social Security Administration announces the gross COLA, you must subtract any forthcoming Medicare premium increases to find your actual net raise.

Consider a practical scenario based on current 2026 data and a hypothetical 2027 adjustment:

| Financial Metric | 2026 Actual Amounts | 2027 Projected Amounts (3.8% COLA) |

|---|---|---|

| Gross Monthly Benefit | $2,083.00 | $2,162.15 |

| Gross Monthly Increase | — | +$79.15 |

| Medicare Part B Premium | $202.90 | $215.00 (Hypothetical Increase) |

| Net Monthly Benefit | $1,880.10 | $1,947.15 |

| True Net Monthly Increase | — | +$67.05 |

A crucial safety net exists for many retirees called the “hold harmless” provision. By law, standard Medicare Part B premium increases cannot reduce your net Social Security benefit below what it was the previous year. If the Part B premium hikes exceed your dollar-amount COLA increase, your premium adjustment is capped so your net check remains flat. However, this protection has significant blind spots; it does not protect high-income earners, nor does it apply to those who have their premiums billed directly rather than deducted from their benefits.

What Can Go Wrong

Navigating retirement income requires vigilance; seemingly beneficial increases can trigger unintended financial consequences if you fail to look ahead.

Falling Victim to the Tax Torpedo

The Internal Revenue Service (IRS) taxes Social Security benefits based on a formula called “provisional income.” You calculate provisional income by taking your adjusted gross income, adding any tax-exempt interest, and adding 50% of your Social Security benefits. If you file as a single individual and your provisional income exceeds $25,000, up to 50% of your benefits become taxable. If it exceeds $34,000, up to 85% of your benefits are subject to federal income tax. For married couples filing jointly, those thresholds sit at $32,000 and $44,000. Because Congress has never indexed these thresholds for inflation, each annual COLA inadvertently pushes more retirees over the limits.

Triggering IRMAA Surcharges

Higher-income retirees face an additional hurdle known as the Income-Related Monthly Adjustment Amount (IRMAA). In 2026, individuals with tax-reported incomes over $109,000—and married couples filing jointly over $218,000—pay surcharges on top of the standard Part B and Part D premiums. A significant COLA increases your overall income and can push you into a higher IRMAA bracket. Because IRMAA calculations look at your Modified Adjusted Gross Income (MAGI) from two years prior, a spike in your income in 2025 will dictate your Medicare premiums in 2027.

Prematurely Upgrading Your Lifestyle

Basing major purchases on summer COLA projections sets a dangerous trap. A 3.8% projection in July can easily dwindle to a 3.0% reality by October if fuel prices plummet late in the summer. Wait until you receive your personalized COLA notice before committing to higher fixed expenses or financing new purchases.

Strategic Moves to Make Before the October Announcement

Preparation outperforms reaction. Use the months leading up to the official announcement to optimize your financial position and safeguard your income.

- Audit your current spending: Track exactly where your money goes for three consecutive months. Categorize expenses into fixed obligations and discretionary spending. This baseline ensures you know exactly how much income you require to maintain your lifestyle.

- Review your withholding strategy: If your COLA pushes your provisional income higher, you may owe more taxes in April. Consider submitting a Form W-4V to the Social Security Administration to voluntarily withhold a percentage of your benefits for federal taxes. You can choose to withhold 7%, 10%, 12%, or 22%.

- Maximize tax-advantaged withdrawals: If you pull funds from a traditional IRA or 401(k), those distributions increase your taxable income. Consider strategically shifting some withdrawals to a Roth IRA, as qualified Roth distributions do not impact the provisional income formula that triggers Social Security taxation.

- Establish a secure online account: The quickest way to access your finalized benefit amount is through the official government portal. Create or log in to your “my Social Security” account. The agency typically posts personalized COLA notices in the Message Center by early December.

When to Consult a Professional

While you can manage basic budgeting independently, certain scenarios warrant expert intervention. To help manage your overall financial wellness, the Consumer Financial Protection Bureau (CFPB) offers resources for older adults, but consider engaging a fiduciary financial planner (credentials verifiable through the Certified Financial Planner Board) or a Certified Public Accountant (CPA) if you encounter the following situations:

You Approach the IRMAA Thresholds: A professional can help you utilize Roth conversions, charitable distributions, or strategic asset location to keep your modified adjusted gross income below the IRMAA surcharge brackets.

You Manage Complex Income Streams: If you draw income from pensions, rental properties, taxable brokerage accounts, and Social Security simultaneously, a CPA can optimize your withdrawal sequence to minimize your lifetime tax burden.

You Plan to Relocate: Moving across state lines fundamentally alters your tax landscape. A financial planner can run detailed projections comparing the true cost of living and tax impacts of your desired destination versus your current residence, especially since certain states tax Social Security benefits while others do not.

Frequently Asked Questions

When exactly does the Social Security Administration announce the new COLA?

The agency traditionally announces the finalized COLA in mid-October. This announcement aligns directly with the release of the September Consumer Price Index data by the Bureau of Labor Statistics.

When will I see the increased amount in my checks?

For the vast majority of retirees, the new COLA takes effect with the January payment. However, if you receive Supplemental Security Income (SSI), your increased payments typically begin slightly earlier, often on December 31 of the preceding year.

Does a higher COLA mean the Social Security trust funds will deplete faster?

Yes; larger payouts accelerate the depletion of the program’s reserve funds. Cost-of-living adjustments permanently increase the benefit baseline for millions of recipients, which puts additional strain on the system’s long-term solvency unless Congress enacts structural reforms.

Can my Social Security check ever decrease because of deflation?

No. By law, if the CPI-W shows a negative inflation rate (deflation) for the third quarter, your Social Security benefits will not decrease. The COLA for that year will simply be zero, and your gross benefit amount will remain flat.

Securing your retirement requires active participation in your financial life; you cannot afford to leave your budget to chance. By keeping an eye on the monthly inflation reports and understanding the strict interplay between Social Security adjustments and Medicare premiums, you position yourself to absorb economic shifts smoothly. Review your tax strategies now, utilize authoritative resources like Medicare.gov to verify your coverage costs, and prepare your household budget for the reality of 2027.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.