Retiring without a traditional paycheck feels terrifying until you realize you can build your own monthly salary using exchange-traded funds (ETFs). A well-constructed income portfolio allows you to collect cash deposits every thirty days, instantly replacing your employer’s direct deposit. You never have to sell your principal shares to generate this cash flow. Instead, you rely on the consistent dividend distributions of specialized funds. Allocating capital into monthly dividend ETFs creates a predictable, passive income stream that covers your bills and protects your nest egg. This specific strategy provides ultimate financial freedom, giving you the steady, reliable cash required to thrive comfortably during your golden years without ever returning to the workforce.

The Mechanics of Monthly Income ETFs

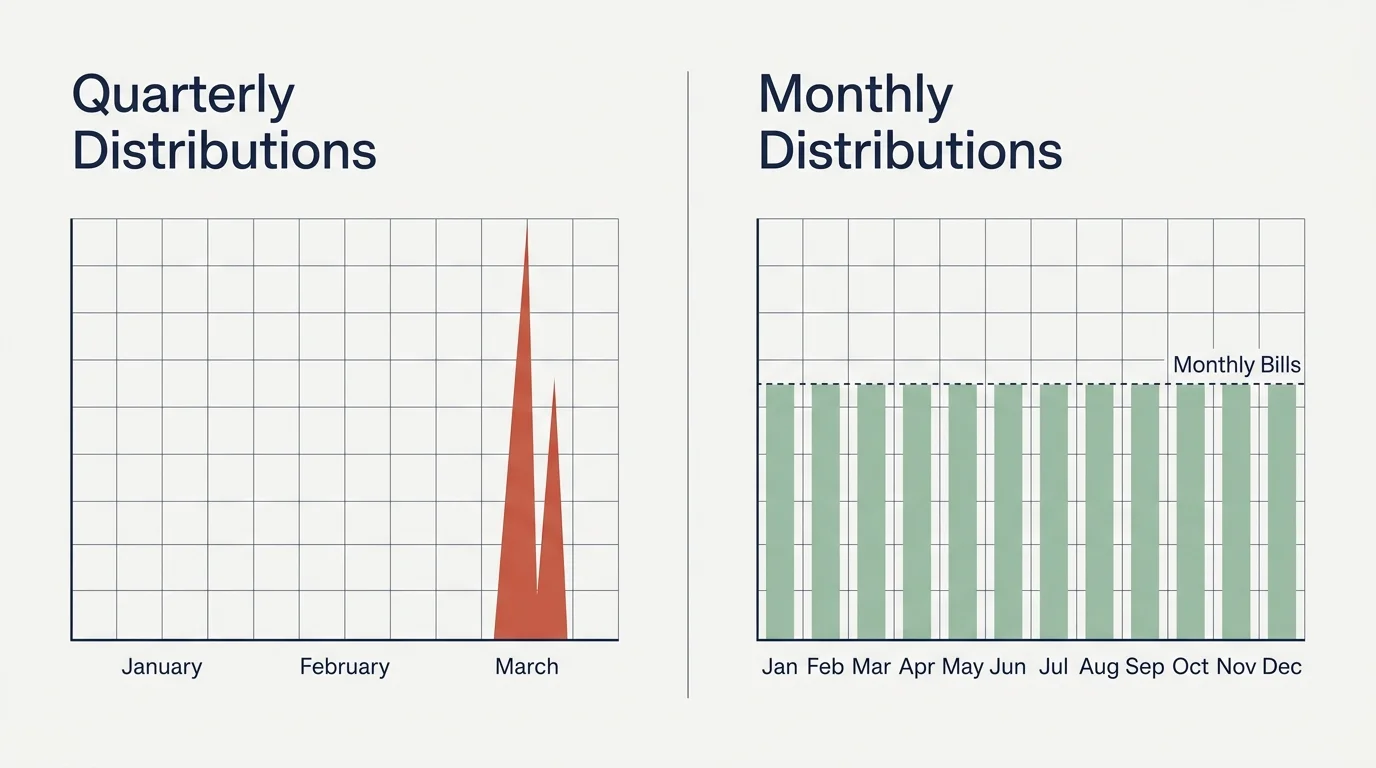

When you transition from the accumulation phase of your career to the distribution phase of retirement, your primary financial need shifts from aggressive growth to reliable cash flow. The traditional stock market setup can be frustrating for retirees because most individual stocks pay dividends on a quarterly basis. If you rely on quarterly payers, you end up with lumpy income streams—a massive cash dump in March, nothing in April or May, and another dump in June. Your utility bills, groceries, and Medicare premiums do not arrive quarterly; they arrive every single month.

Monthly dividend ETFs solve this timing mismatch. These funds pool your money with other investors to purchase a massive, diversified basket of income-producing assets. The fund managers collect the dividends, interest payments, and option premiums generated by the underlying holdings, smooth out the math, and distribute a consolidated payment to your brokerage account every thirty days.

To generate higher-than-average yields, many modern income ETFs utilize a covered call strategy. Rather than just holding stocks and waiting for dividends, the fund managers sell call options against the stocks they own. An option is simply a financial contract that gives someone else the right to buy the stock at a specific price. By selling these contracts, the ETF collects an immediate cash premium. This premium is passed directly to you as monthly income. While this strategy intentionally caps some of the extreme upside growth during massive bull markets, it excels in flat or volatile markets by converting market movement into tangible cash in your pocket.

“If you don’t find a way to make money while you sleep, you will work until you die.” — Warren Buffett, CEO of Berkshire Hathaway

4 Monthly Dividend ETFs Built for Retirement Income

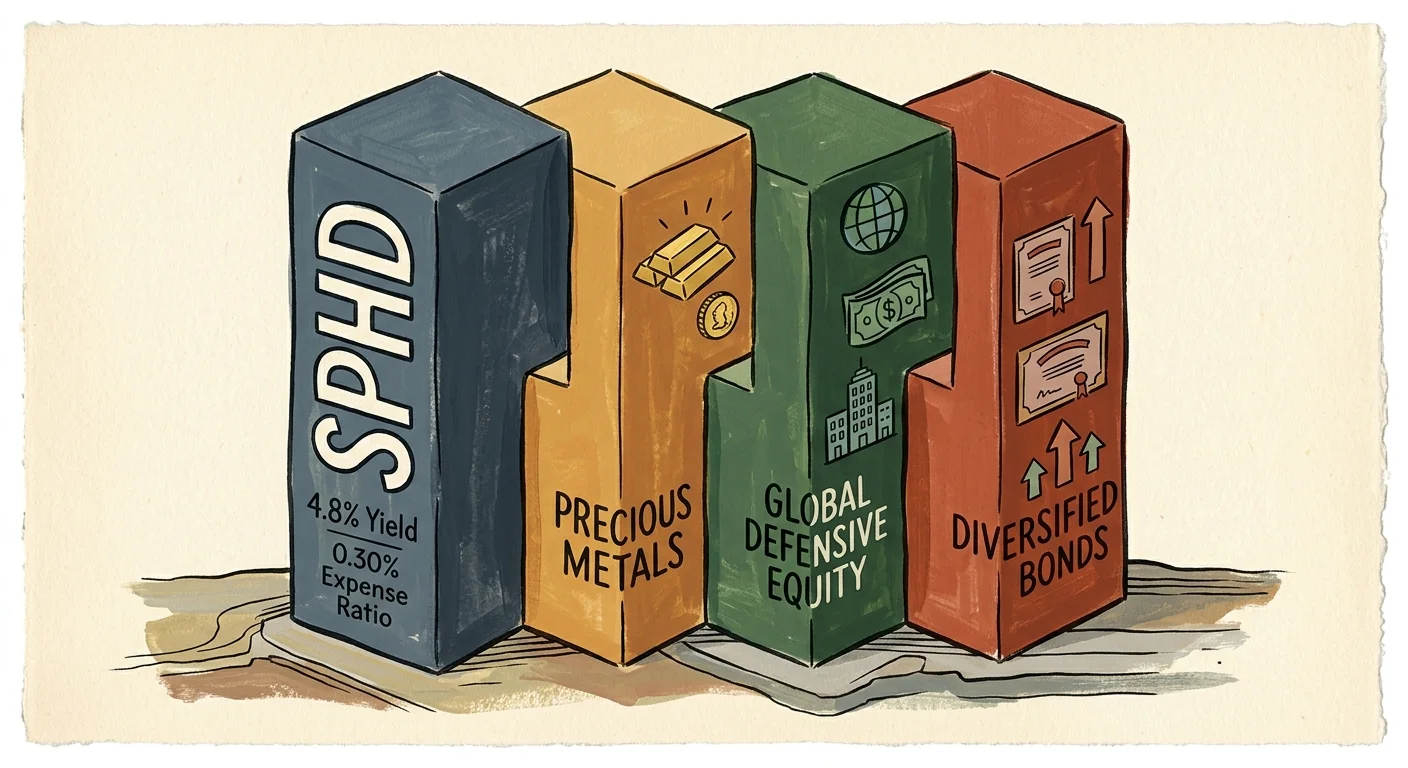

Building a resilient retirement portfolio requires diversification. You should never rely on a single fund for all your income needs. By combining different strategies—such as low-volatility value stocks, dividend growth companies, and option-enhanced tech funds—you can create a blended yield that weathers shifting economic climates. Here are four established monthly dividend ETFs to consider for your income sleeve.

1. Invesco S&P 500 High Dividend Low Volatility ETF (SPHD)

If you prefer a conservative, fundamentally sound approach to income, SPHD is a foundational choice. This fund filters the S&P 500 to find the 75 highest dividend-paying companies, then narrows the list down to the 50 stocks with the absolute lowest market volatility. The resulting portfolio is heavily weighted toward defensive sectors like utilities, consumer staples, and real estate. Because these companies sell essential products and services, they generate steady profits regardless of the economic cycle. SPHD historically delivers a stable yield of around 4.8 percent and boasts a very reasonable expense ratio of 0.30 percent.

2. Amplify CWP Enhanced Dividend Income ETF (DIVO)

DIVO offers a hybrid approach designed for retirees who want both current income and protection against long-term inflation. The active managers behind DIVO select roughly two to three dozen large-cap, blue-chip companies with a history of consistently growing their dividends. To boost the yield, the managers tactically write covered calls on individual stocks within the portfolio. Unlike passive funds that blindly write calls on their entire holdings, DIVO only sells options when the premiums are highly attractive. This allows the core portfolio to participate in market growth while still delivering a yield typically ranging between 4.8 percent and 6.4 percent.

3. JPMorgan Equity Premium Income ETF (JEPI)

JEPI has exploded in popularity among retirees due to its massive yield and lower volatility profile. The fund invests in a defensive basket of U.S. large-cap stocks specifically chosen to exhibit less price movement than the broader S&P 500. To generate its outsized monthly payments, JEPI uses equity-linked notes (ELNs) to sell out-of-the-money call options on the S&P 500 index. Because the fund focuses on generating cash through option premiums, it routinely delivers yields north of 8.0 percent. The expense ratio sits at 0.35 percent, which is highly competitive for an actively managed derivative income fund.

4. JPMorgan Nasdaq Equity Premium Income ETF (JEPQ)

JEPQ is the technology-focused sibling to JEPI. Instead of tracking the S&P 500, JEPQ holds companies from the tech-heavy Nasdaq-100 index and writes call options against that specific benchmark. Because technology stocks are naturally more volatile than utility or healthcare stocks, the option premiums generated by JEPQ are significantly higher. This results in a massive target yield that frequently hovers between 10.0 percent and 11.4 percent. Adding JEPQ to your portfolio is an excellent way to juice your overall monthly cash flow, provided you balance it with more conservative holdings like SPHD to mitigate the inherent tech-sector risks.

| ETF Name & Ticker | Primary Strategy | Estimated Yield (2026) | Expense Ratio |

|---|---|---|---|

| Invesco S&P 500 High Div Low Vol (SPHD) | Top 50 high-yield, low-volatility S&P 500 stocks | 4.85% | 0.30% |

| Amplify CWP Enhanced Dividend (DIVO) | Active blue-chip dividend growth + tactical options | 4.8% – 6.4% | 0.55% |

| JPMorgan Equity Premium Income (JEPI) | Defensive large-cap equities + S&P 500 options | 8.2% | 0.35% |

| JPMorgan Nasdaq Equity Premium (JEPQ) | Nasdaq-100 equities + Nasdaq options | 10.3% – 11.4% | 0.35% |

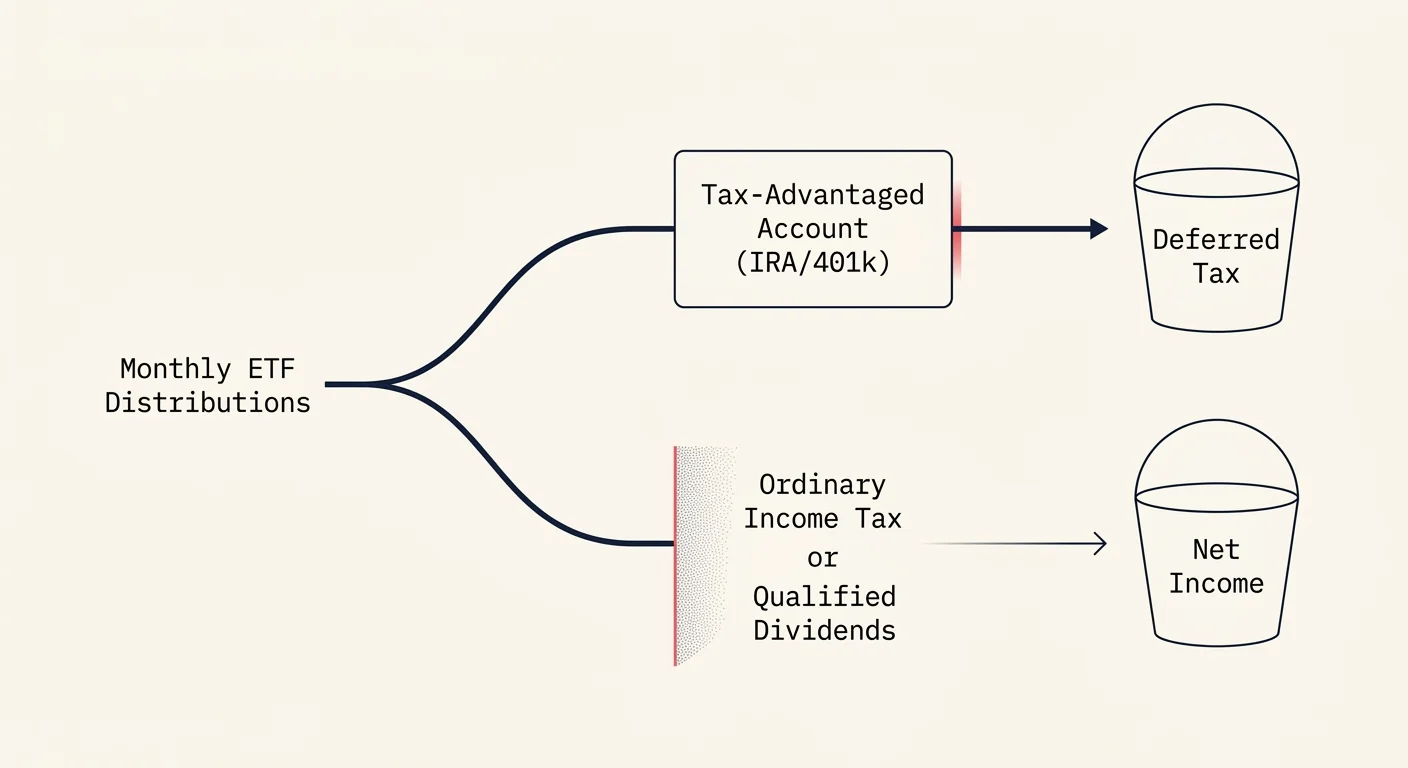

How Monthly Dividends Impact Your Taxes and Benefits

Generating massive cash flow in retirement is only half the battle; keeping that cash away from the IRS is the other half. When you invest in specialized income funds, you must understand how those distributions interact with your tax brackets, your Medicare premiums, and your Social Security benefits.

Navigating the 2026 Tax Brackets

The tax treatment of your ETF income depends entirely on how the fund generates its cash. Standard dividends from domestic companies—like those heavily featured in SPHD—often qualify for the favorable qualified dividend tax rates of 0, 15, or 20 percent. However, the income generated from selling covered calls (the primary engine for JEPI and JEPQ) is taxed as ordinary income, meaning it falls under your standard tax brackets.

Fortunately, the Internal Revenue Service (IRS) provides generous standard deductions for retirees. In 2026, the standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. Additionally, if you are 65 or older, you qualify for the new senior bonus deduction of $6,000 per person. This means a married couple over 65 can shield up to $44,200 of their income from federal income taxes entirely. Strategic placement of your ETFs—such as holding ordinary-income generators like JEPQ inside a tax-sheltered IRA and holding qualified-dividend generators like SPHD in a taxable brokerage—can save you thousands of dollars annually.

Dodging the Medicare IRMAA Cliff

Your ETF income directly impacts your healthcare costs. Medicare.gov sets the standard Part B premium at $202.90 per month for 2026. However, Medicare uses a two-year lookback period based on your Modified Adjusted Gross Income (MAGI) to determine if you must pay a surcharge known as the Income-Related Monthly Adjustment Amount (IRMAA).

For 2026, the IRMAA brackets begin at $109,000 for single filers and $218,000 for married couples filing jointly. If your ETF income, combined with your pensions, Social Security, and required minimum distributions (RMDs), pushes your MAGI even one dollar over that $218,000 threshold, you trigger a surcharge that drastically increases your Part B and Part D premiums. Retirees generating high six-figure incomes from dividend portfolios must actively manage their MAGI to avoid falling off this costly cliff.

Social Security Earnings Limits and Taxation

The Social Security Administration (SSA) offers a maximum possible benefit of $5,181 per month for individuals who wait until age 70 to claim in 2026. If you choose to claim benefits early while continuing to work, the government enforces an earnings test. In 2026, the earnings limit is $65,160; if your earned income exceeds this amount, the SSA withholds $1 in benefits for every $3 you earn above the limit.

Here is the brilliant advantage of ETF investing: passive dividend income does not count as earned income. You can generate $100,000 a year in dividends from JEPI and DIVO without triggering the earnings test penalty. However, you must be aware that ETF distributions do factor into your provisional income, which is the formula the IRS uses to determine if your Social Security benefits are subject to federal income tax.

Building a Sustainable 30-Year Withdrawal Strategy

Replacing your paycheck requires a shift in mindset. When you were working, you likely adhered to traditional asset allocation models, aggressively funneling cash into broad index funds and ignoring the day-to-day volatility. In retirement, your focus must pivot to sequencing risk and distribution sustainability.

Relying exclusively on the famous 4 percent rule—where you sell off 4 percent of your principal every year adjusted for inflation—forces you to liquidate shares. If the market crashes by 20 percent and you sell shares to fund your lifestyle, those shares are permanently gone and can never recover. Monthly dividend ETFs offer an alternative: the yield-only withdrawal strategy. By spending only the cash dividends deposited into your account and leaving the principal untouched, you preserve your share count regardless of market fluctuations.

To succeed over a 30-year timeline, you must balance high current yield with long-term dividend growth. Funds like JEPI and JEPQ provide the heavy immediate cash flow needed to pay today’s bills, but their payouts can fluctuate based on market volatility. Funds like DIVO and SPHD may offer slightly lower starting yields, but they invest in underlying businesses that historically raise their dividends over time. This blend ensures that your monthly paycheck keeps pace with inflation throughout your retirement.

“The miracle of compounding returns is overwhelmed by the tyranny of compounding costs.” — John Bogle, Founder of Vanguard

Bogle’s wisdom is critical when selecting specialized ETFs. Always verify the expense ratio before buying. The funds highlighted in this guide feature reasonable fees under 0.60 percent. Avoid complex derivative products that charge upwards of 1.5 percent, as those fees will ruthlessly erode your passive income over a multi-decade retirement.

Common Mistakes to Avoid

Transitioning to an income-focused portfolio comes with a learning curve. Avoid these common traps to protect your monthly cash flow.

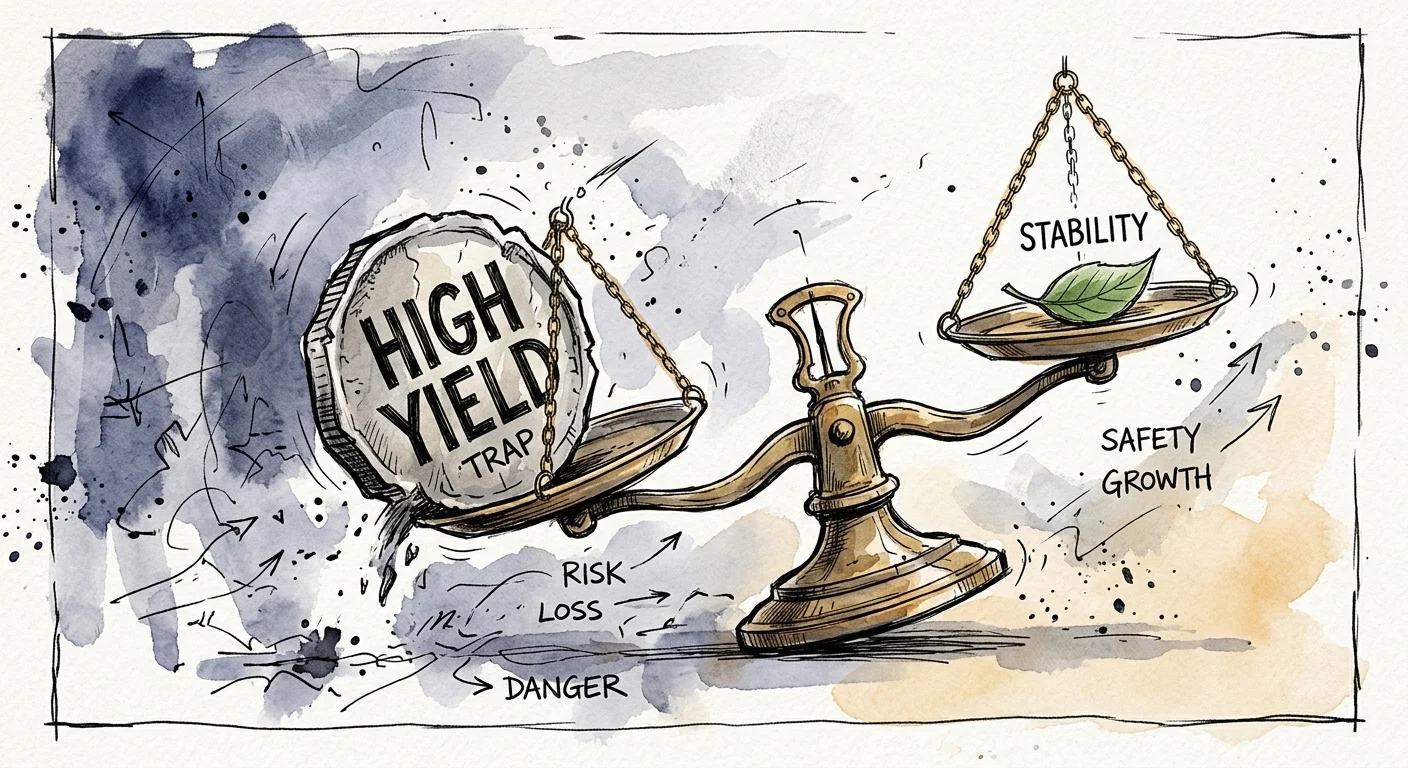

- Chasing Unsustainable Yields: A fund advertising a 20 percent yield is a massive red flag. Extremely high yields often indicate a deteriorating principal asset or a return of capital, meaning the fund is simply handing your own money back to you while charging a management fee. Stick to established funds with yields in the 4 to 12 percent range.

- Ignoring Tax Placement: Placing tax-inefficient covered call ETFs in a standard brokerage account will result in a hefty tax bill at ordinary income rates. Whenever possible, house your highest-yielding, ordinary-income assets inside a tax-sheltered account like a Roth IRA, where the monthly distributions remain completely tax-free.

- Forgetting About Inflation: High-yield option funds do not always grow their dividend payouts over time. If your entire portfolio consists of fixed-income instruments, your purchasing power will decline as the cost of groceries and healthcare rises. Always dedicate a portion of your portfolio to dividend growth strategies.

- Over-Concentrating in One Asset Manager: Do not put all your retirement capital into a single fund family. Diversify across different issuers (such as Invesco, JPMorgan, and Amplify) to protect yourself against institutional risk and strategy drift.

Professional vs. Self-Guided

Determining how to manage your monthly income portfolio depends on your financial literacy, your tax complexity, and how you want to spend your time.

Scenario 1: The Do-It-Yourself Investor

If you understand the difference between qualified and ordinary dividends, feel comfortable calculating your MAGI to avoid IRMAA penalties, and enjoy researching expense ratios on platforms like Morningstar, you can easily manage this strategy yourself. You simply purchase the ETFs through a discount broker, opt out of automatic reinvestment (DRIP), and transfer the monthly cash to your checking account.

Scenario 2: The Tax-Conscious Retiree

If you and your spouse have multiple income streams—including pensions, Social Security, and substantial traditional 401(k) balances that will trigger massive Required Minimum Distributions (RMDs)—the tax calculations become complex. A sudden spike in ETF income could push you over the $218,000 joint IRMAA threshold or subject 85 percent of your Social Security to taxes. In this scenario, hiring a fiduciary Certified Financial Planner to map out Roth conversions and asset location is highly recommended.

Scenario 3: The Delegation Seeker

Perhaps you understand the math perfectly, but you simply do not want to spend your retirement logging into brokerage accounts or monitoring ex-dividend dates. Using a Vanguard Retirement advisory service or a fee-only planner allows you to hand over the execution of the strategy. You pay a small management fee in exchange for total peace of mind, allowing you to spend your time traveling and enjoying your family.

Frequently Asked Questions

Do monthly dividend ETFs guarantee a fixed payment?

No. Unlike traditional fixed annuities or bonds, ETF dividends fluctuate. The amount you receive depends on the actual dividends paid by the underlying stocks and the premiums generated by the fund’s option strategy. Payments will vary slightly from month to month.

Are covered call ETFs safe for a conservative retirement portfolio?

They are generally considered less volatile than pure growth stocks because the option premiums provide a cash buffer during market downturns. However, they are still equity investments and carry market risk. They will lose value during a severe stock market crash, though typically less than the broader index.

Should I hold monthly income ETFs in an IRA or a brokerage account?

It depends on the fund’s tax profile. Funds that generate ordinary income (like JEPI and JEPQ) are best held inside tax-advantaged accounts like a Traditional or Roth IRA. Funds that generate qualified dividends (like SPHD) are more tax-efficient and can be comfortably held in a taxable brokerage account.

Can dividend income cause my Social Security benefits to be taxed?

Yes. While ETF dividends do not count toward the earned income limit (meaning they will not cause the SSA to withhold your checks), they are included in your provisional income calculation. If your provisional income exceeds certain thresholds, up to 85 percent of your Social Security benefit becomes taxable at the federal level.

Building a self-sustaining paycheck requires patience, discipline, and a willingness to step away from traditional accumulation strategies. By harnessing the power of monthly dividend ETFs, you can create a resilient financial engine that funds the lifestyle you deserve. Take the time to evaluate your income needs, consult with a tax professional regarding your brackets and IRMAA limits, and begin constructing your ultimate retirement portfolio today.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.