When affluent Americans leave the workforce, their relocation decisions revolve around preserving wealth, minimizing taxes, and upgrading their lifestyle. High-net-worth retirees are consistently migrating toward states that offer a strategic blend of zero state income tax, robust healthcare infrastructure, and premier amenities. By analyzing recent IRS migration data—which reveals Florida alone captured over $20.7 billion in net income from state-to-state moves—distinct patterns emerge showing exactly where America’s richest seniors choose to spend their golden years. Whether you are finalizing your own relocation strategy or simply looking to understand the financial mechanics behind these affluent ZIP codes, understanding how these destinations shield retirement income provides a blueprint for maximizing your portfolio’s longevity.

The Great Wealth Migration: Following the Data

Retirement relocation is no longer driven purely by the desire for warmer winters; it has evolved into a highly calculated wealth preservation strategy. According to exhaustive migration data released by the Internal Revenue Service (IRS), the United States is currently experiencing a massive, directional reallocation of income across state lines. This migration paints a clear picture of exactly where high-net-worth households are choosing to consolidate their assets and establish their permanent domiciles.

The numbers from the latest IRS reporting cycle are staggering. In a single year, approximately 6.7 million Americans packed up and moved across state borders, and among them were roughly 700,000 high-earning households generating over $200,000 annually. These affluent retirees and late-career professionals took their income, investment portfolios, and tax dollars directly to states with more favorable fiscal environments. The primary beneficiaries of this wealth transfer are lower-tax, fast-growing states located in the Sun Belt and the Mountain West. Conversely, jurisdictions with notoriously high tax burdens and cost-of-living pressures—namely California, New York, Illinois, New Jersey, and Massachusetts—continue to experience the largest net outflows of high-income tax filers.

Florida stands completely unrivaled in this domestic wealth transfer. The state netted an astonishing $20.7 billion in adjusted gross income from interstate migration. What makes Florida’s demographic shift unique is the sheer concentration of wealth; approximately 82% of that net financial gain came exclusively from households earning $200,000 or more. Texas secured the second position by capturing $5.3 billion in net new income and welcoming over 111,000 net new residents. However, the Texas migration story is broader, attracting a larger proportion of middle-class and working professionals alongside wealthy retirees, whereas Florida’s influx leans heavily toward the affluent.

The Premier Tax Havens for Affluent Retirees

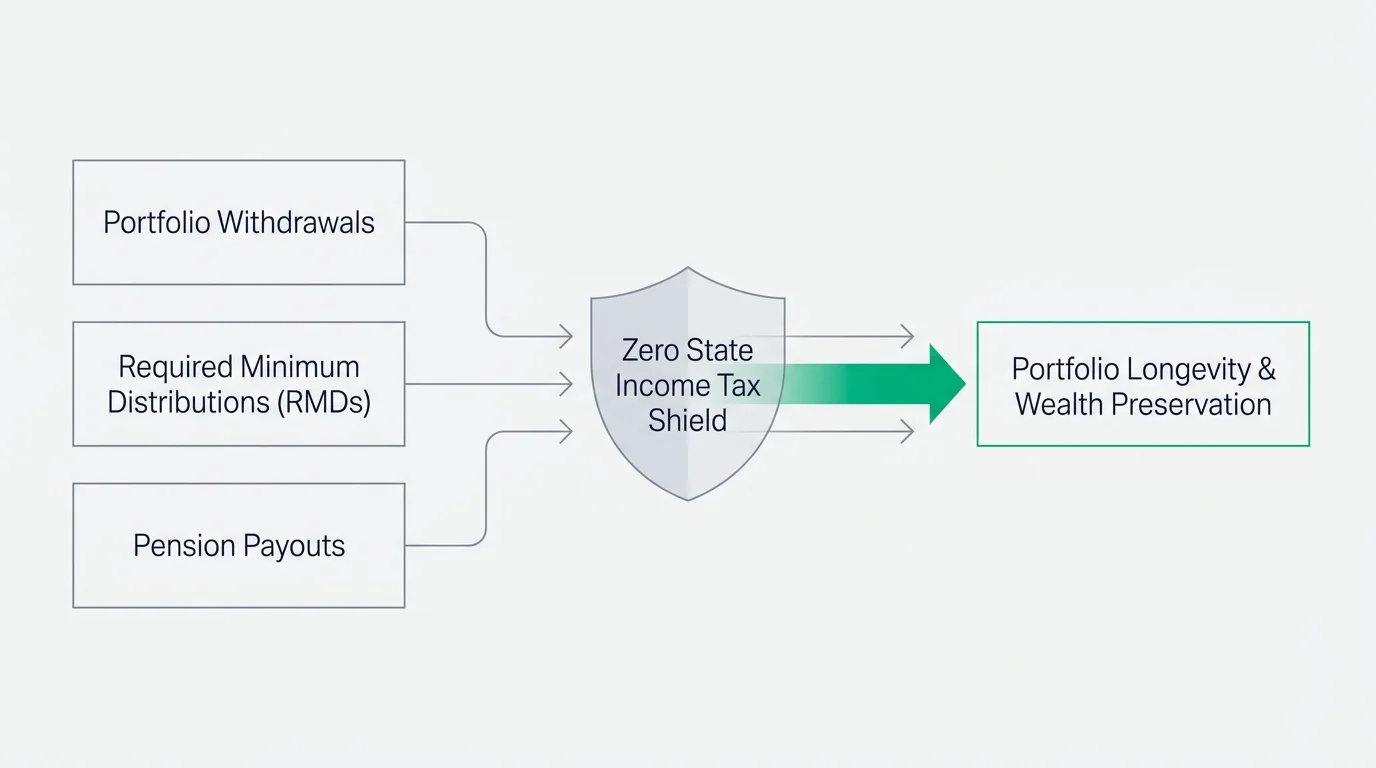

When you map the most concentrated pockets of retirement wealth in America, they overwhelmingly align with states that do not levy a personal income tax. As of 2026, nine states operate without a broad-based personal income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Wyoming, and Washington (though Washington does tax specific high-end capital gains). For an affluent retiree living on substantial portfolio withdrawals, required minimum distributions (RMDs), and large pension payouts, avoiding state income taxes can result in millions of dollars in saved capital over a two-decade retirement.

Florida’s Platinum Coast and Beyond

Florida’s tax environment—featuring no state income tax, no tax on Social Security benefits, and strong homestead protections against creditors—makes it the ultimate magnet for high-net-worth seniors. Naples, situated on the Gulf Coast, consistently ranks as a premier retirement destination due to its rare combination of pristine safety, resident satisfaction, and exceptional healthcare facilities. The concentration of wealth here is palpable, with private golf clubs, luxury marinas, and upscale shopping dominating the landscape. Further north, The Villages in central Florida has transformed into a sprawling, meticulously planned metropolis exclusively for active adults, boasting staggering growth and private amenities that rival five-star resorts.

The Nevada and Wyoming Tax Shields

For retirees who prefer dramatic mountain ranges or desert vistas over beachfront property, Nevada and Wyoming serve as elite financial sanctuaries. Nevada’s lack of state income tax has fueled massive growth in luxury 55+ communities like Sun City Anthem in Henderson, where high-end homes offer sweeping views of the Las Vegas Valley alongside world-class clubhouses and championship golf courses. Wyoming, frequently ranked as the most tax-friendly state in the country, pairs its zero income tax with an incredibly low average property tax rate of just 0.55%. Affluent retirees flock to enclaves like Jackson Hole, trading humid climates for robust privacy, vast estates, and unhindered access to nature, all while completely shielding their investment income from state revenue departments.

The Quiet Carolinas and Tennessee

While they do not often command the flashy headlines of South Florida, states like North Carolina, South Carolina, and Tennessee have quietly become massive migration powerhouses. Tennessee, which boasts zero state income tax, added over $2.8 billion in net new income recently. The Carolinas offer a slightly different proposition; while they do have state income taxes, they offer generous exemptions for retirement income and substantially lower property taxes compared to the Northeast. High-net-worth retirees are heavily concentrated in exclusive golfing communities like Pinehurst, North Carolina, where the lifestyle is elegant, the cost of living is manageable, and the tax burden remains highly competitive.

Beyond the Sun Belt: Emerging Wealthy Enclaves

It is a misconception that all wealthy retirees flee to zero-tax states. A significant demographic of affluent seniors prioritizes climate, breathtaking scenery, and proximity to family over maximum tax efficiency. In these instances, extreme wealth concentrates in highly specific, affluent ZIP codes.

Oro Valley and the Arizona Boom

Arizona has long been a retirement haven, but specific towns are capturing the upper echelon of the market. Oro Valley, located just north of Tucson, frequently ranks as one of the safest and wealthiest retirement towns in the United States. It leads a pack of affluent Arizona communities—including Scottsdale, Prescott, and Green Valley—that offer retirees resort-style living, master-planned infrastructure, and exceptional medical care. Arizona does tax income, but its rates are historically modest, making it a comfortable middle ground for retirees seeking luxury desert living.

California’s Coastal Holdouts

Despite California leading the nation in the loss of high-income taxpayers, the state still houses some of the richest retirement towns in America. Rancho Palos Verdes, perched on coastal cliffs south of Los Angeles, is heavily populated by affluent retirees who are willing to absorb California’s aggressive tax structure in exchange for unparalleled natural beauty and convenient access to a massive metropolitan hub. Similarly, Carmel-by-the-Sea remains a legendary enclave for the incredibly wealthy. For these retirees, the premium paid in state taxes is simply the price of admission for a lifestyle they cannot replicate anywhere else.

The Mountain West Surge

An undeniable trend emerging from the latest demographic data is the rapid growth of the Mountain West. Idaho and Montana are aggressively capturing outbound wealth from the West Coast, particularly from states like California and Washington. Retirees moving to these states are often purchasing sprawling ranches or luxury lodge-style homes in private communities, prioritizing space, security, and outdoor recreation over traditional resort amenities.

The Financial Mechanics: Shielding Retirement Wealth in 2026

To truly understand why America’s richest retirees orchestrate these elaborate relocations, you must examine the current federal tax and healthcare landscape. In retirement, your gross income matters far less than your net, after-tax spending power. By relocating to a tax-friendly jurisdiction, wealthy retirees can free up substantial cash flow to cover federally mandated healthcare costs and combat inflation.

Consider the 2026 Social Security Cost of Living Adjustment (COLA), which delivered a 2.8% increase to beneficiaries. For a wealthy retiree, Social Security is likely a minor component of their overall cash flow, but preserving that income still matters. If you live in one of the states that still taxes Social Security benefits, a portion of that inflation adjustment is immediately clawed back by the state government. Moving to a state like Florida or Nevada ensures your federal benefits remain entirely yours.

“It’s not how much you make, it’s how much you keep. That is especially true in retirement when you are navigating the complex web of federal and state taxes.” — Ed Slott, CPA and Retirement Tax Expert

The most pressing financial burden for high-net-worth retirees is not necessarily base inflation, but rather the stealth taxes embedded within the Medicare system. In 2026, the standard Medicare Part B monthly premium is $202.90. However, affluent seniors are subject to the Income-Related Monthly Adjustment Amount (IRMAA). This federally mandated surcharge is based on your Modified Adjusted Gross Income (MAGI) from two years prior. For 2026, the IRMAA surcharges trigger when a single filer’s MAGI exceeds $109,000, or when a married couple’s joint MAGI exceeds $218,000. At the highest income brackets, IRMAA can push your Part B premium up to a staggering $689.90 per person, per month. Living in a zero-income-tax state does not eliminate your federal IRMAA obligations, but it completely removes the state tax burden from your portfolio withdrawals, effectively freeing up the thousands of dollars needed to pay these exorbitant healthcare surcharges.

Furthermore, the federal tax code offers specific, highly structured deductions for older Americans. Navigating these requires careful planning. For the 2026 tax year, seniors aged 65 and older who choose not to itemize can claim an extra standard deduction of $2,050 for single filers, or $1,650 per qualifying spouse for joint filers. Additionally, recent federal legislation introduced a new $6,000 enhanced deduction for seniors in 2026. However, this specific $6,000 deduction phases out entirely for taxpayers with a MAGI over $75,000 (single) or $150,000 (joint). Because America’s richest retirees routinely pull well over $200,000 annually from their accounts, they are completely phased out of this new federal deduction. This reality reinforces exactly why they must aggressively seek tax relief at the state level by moving to places like Wyoming, Texas, or Florida.

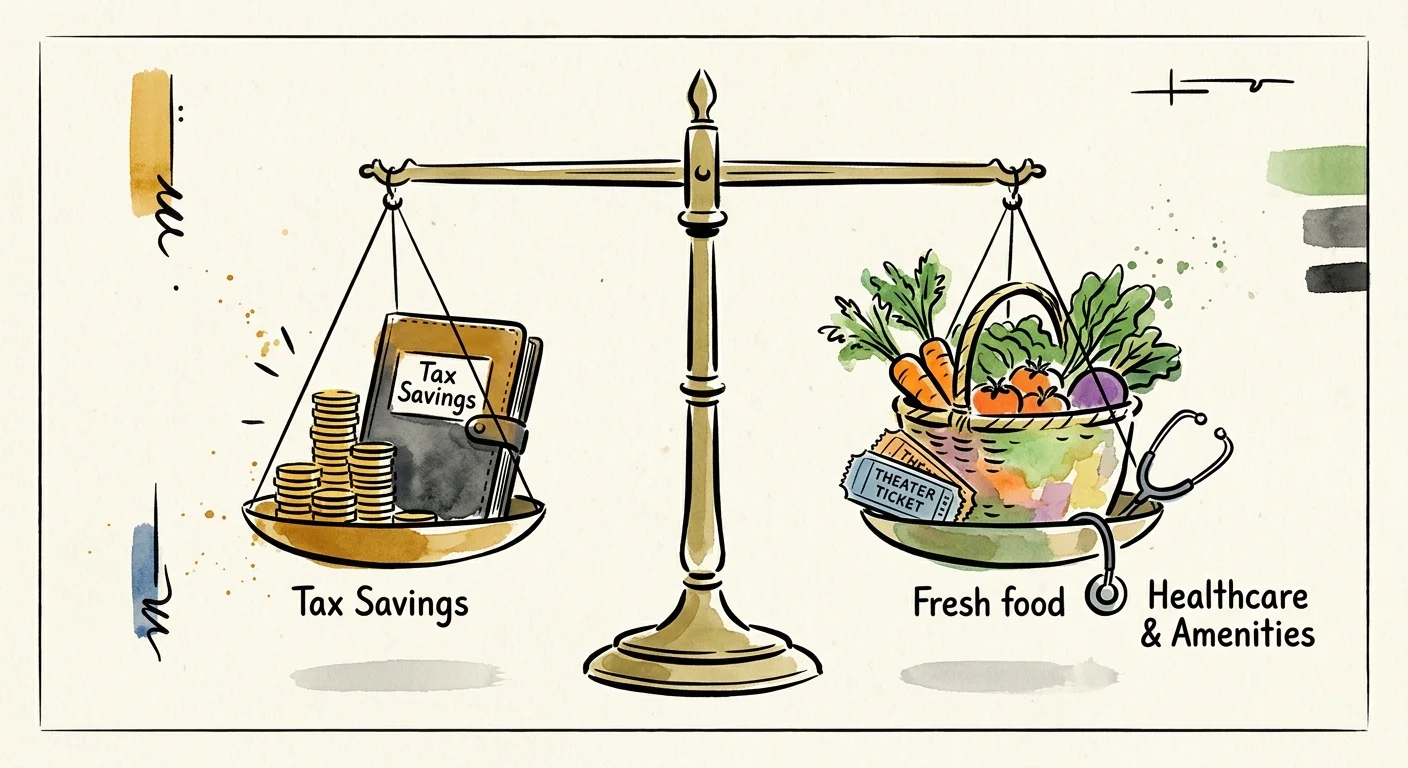

Evaluating the Trade-Offs

Relocating for retirement requires balancing tax savings against lifestyle preferences and hidden costs. Before contacting a real estate agent, consider how different regions stack up.

| Destination Type | State Income Tax | Property Tax & Insurance Trends | Primary Appeal for High-Net-Worth Retirees |

|---|---|---|---|

| Sun Belt Havens (FL, TX, NV) | 0% | Rising sharply; property insurance in coastal/hurricane zones is highly volatile. | Massive income tax savings, master-planned luxury communities, year-round warm weather, and excellent estate preservation. |

| Mountain West Sanctuaries (WY, ID, MT) | 0% to Moderate | Generally stable; Wyoming offers exceptionally low property tax rates. | Unmatched privacy, vast acreage, robust tax protections, and elite outdoor recreation. |

| High-Tax Coastal Enclaves (CA, NY, MA) | High (up to 13.3%+) | High baseline property taxes, though some states cap annual assessment increases. | Deep familial roots, historic properties, unrivaled cultural amenities, and sweeping oceanfront vistas. |

| The “Middle Ground” (NC, SC, AZ) | Moderate (Flat or Graduated) | Manageable; often lower than national averages with specific senior exemptions. | Balanced cost of living, pronounced seasonal changes without harsh winters, and premier golf infrastructure. |

Avoiding Common Errors

Executing a cross-country move to protect your wealth involves significant legal and financial execution. High-net-worth retirees routinely stumble into avoidable traps.

The Domicile Trap

You cannot simply purchase a beachfront condominium in Naples, spend your winters there, and claim you no longer owe taxes to New York or California. High-tax states employ aggressive residency auditors who will ruthlessly examine your life to prove you never actually left. To legally change your domicile, you must typically spend more than 183 days in your new state. More importantly, you must sever primary ties to your old state. Auditors will check your voter registration, where your vehicles are registered, where your primary doctors are located, the location of your family heirlooms, and even your cellular tower data. If you are moving to save millions in taxes, you must commit to the relocation entirely.

Underestimating the Insurance Crisis

A zero-percent income tax rate is incredibly attractive, but it does not make you immune to rising costs. In states like Florida and Texas, the property insurance markets have experienced massive volatility due to extreme weather events and litigation costs. Affluent retirees purchasing multimillion-dollar coastal estates are often shocked by six-figure annual insurance premiums—if they can secure comprehensive coverage at all. You must factor carrying costs, specialized flood insurance, and rising property assessments into your long-term cash flow projections.

Ignoring Healthcare Access

Wealth can buy many things, but it cannot buy proximity to a stroke center in an emergency. Retirees who move to remote, ultra-private mountain ranches in Wyoming or Idaho often underestimate the logistical challenges of aging in a rural setting. America’s richest retirees mitigate this by clustering near premier medical institutions—such as the Mayo Clinic in Arizona or the Cleveland Clinic branches in Florida—ensuring their wealth is supported by world-class, accessible healthcare.

When DIY Isn’t Enough

For affluent households, a retirement relocation is a complex financial transaction that should not be attempted without professional guidance. You should engage a Certified Financial Planner (CFP) and a specialized estate planning attorney if you encounter any of the following scenarios:

- Multi-State Asset Holdings: If you plan to retain a secondary residence or rental properties in a high-tax state while domiciling in a low-tax state, you will likely trigger complex multi-state tax filing requirements. You need an expert to ensure your income is sourced and taxed correctly.

- Business Liquidations: If you are selling a business, the timing of your move relative to the finalization of the sale is critical. Selling a heavily appreciated asset while still legally domiciled in California or New York will subject the windfall to severe taxation, whereas executing the sale after establishing residency in Nevada or Florida can save millions.

- Advanced Estate Planning: Estate taxes vary wildly by state. Moving across borders may require completely redrafting your trusts, updating your power of attorney documents to comply with local statutes, and establishing new strategies to mitigate generation-skipping transfer (GST) taxes.

Frequently Asked Questions

What state has the highest concentration of wealthy retirees?

Based on recent IRS migration and income data, Florida attracts the highest absolute number of high-net-worth retirees, securing over $20.7 billion in net new adjusted gross income in a single reporting year. Cities like Naples and Palm Beach are globally recognized hubs for affluent seniors.

Do zero-income-tax states have hidden costs?

Yes. States must generate revenue to fund public infrastructure. Jurisdictions without an income tax often compensate by levying higher sales taxes, imposing higher property tax rates (as seen in Texas), or heavily taxing specific corporate entities. Additionally, property insurance in popular tax-free states like Florida has risen dramatically in recent years.

How does relocating to a new state affect my Medicare coverage?

Your foundational Medicare Parts A and B travel with you seamlessly anywhere in the United States. However, Medicare Advantage (Part C) and Part D prescription drug plans are region-specific. If you permanently relocate, you are granted a Special Enrollment Period (SEP) to select new plans that are in-network for your new primary ZIP code. You must update your address with the Social Security Administration immediately to trigger this window.

Can I still claim standard deductions if I move to a state with no income tax?

Absolutely. The federal standard deduction, including the $2,050 additional deduction for singles aged 65 and older in 2026, applies to your federal tax return regardless of where you live in the United States. State residency only affects your state-level tax obligations.

Taking control of your retirement destination is one of the most powerful financial decisions you will ever make. By aligning your physical location with your portfolio strategy, you can insulate your wealth from aggressive taxation while enjoying the lifestyle you spent decades working to achieve. Take the time to visit these enclaves, consult with a multi-state tax professional, and build a relocation strategy that serves both your financial legacy and your daily happiness.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.