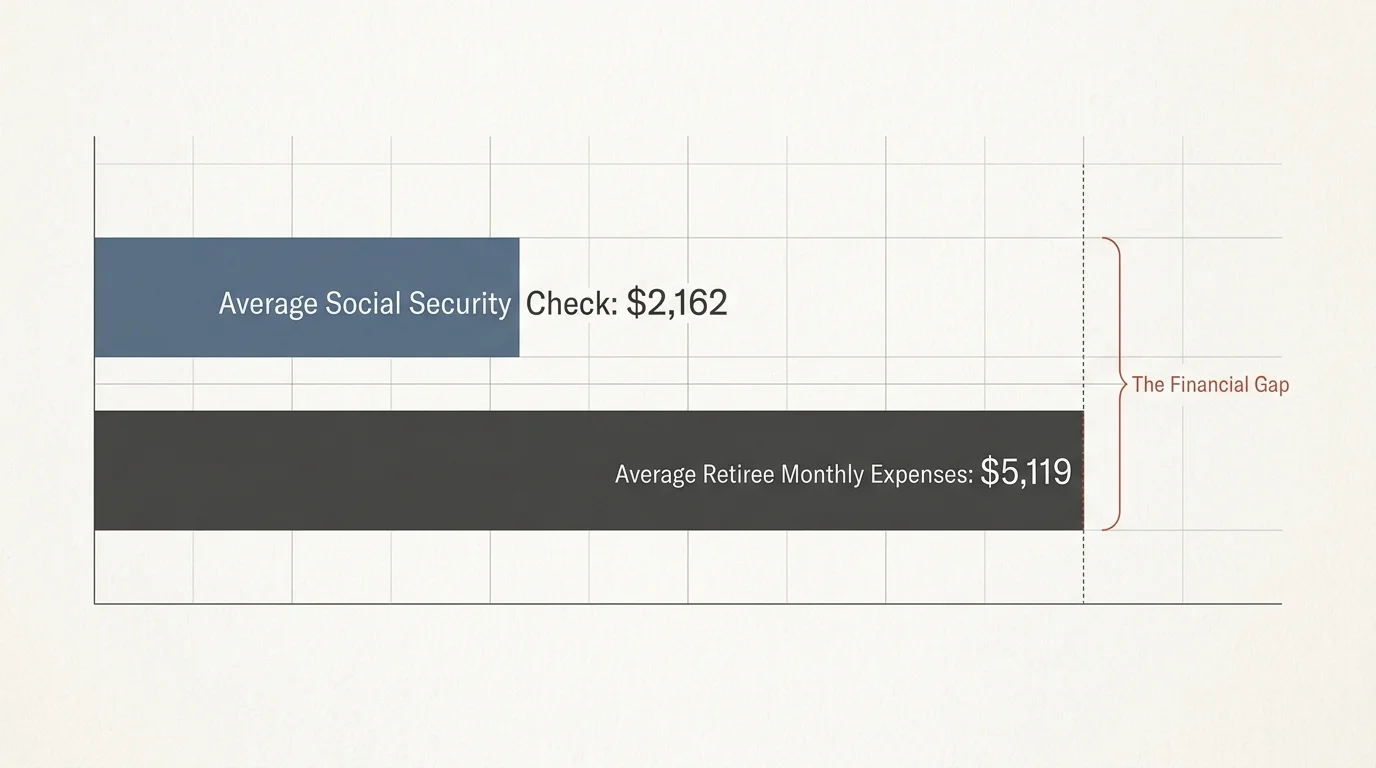

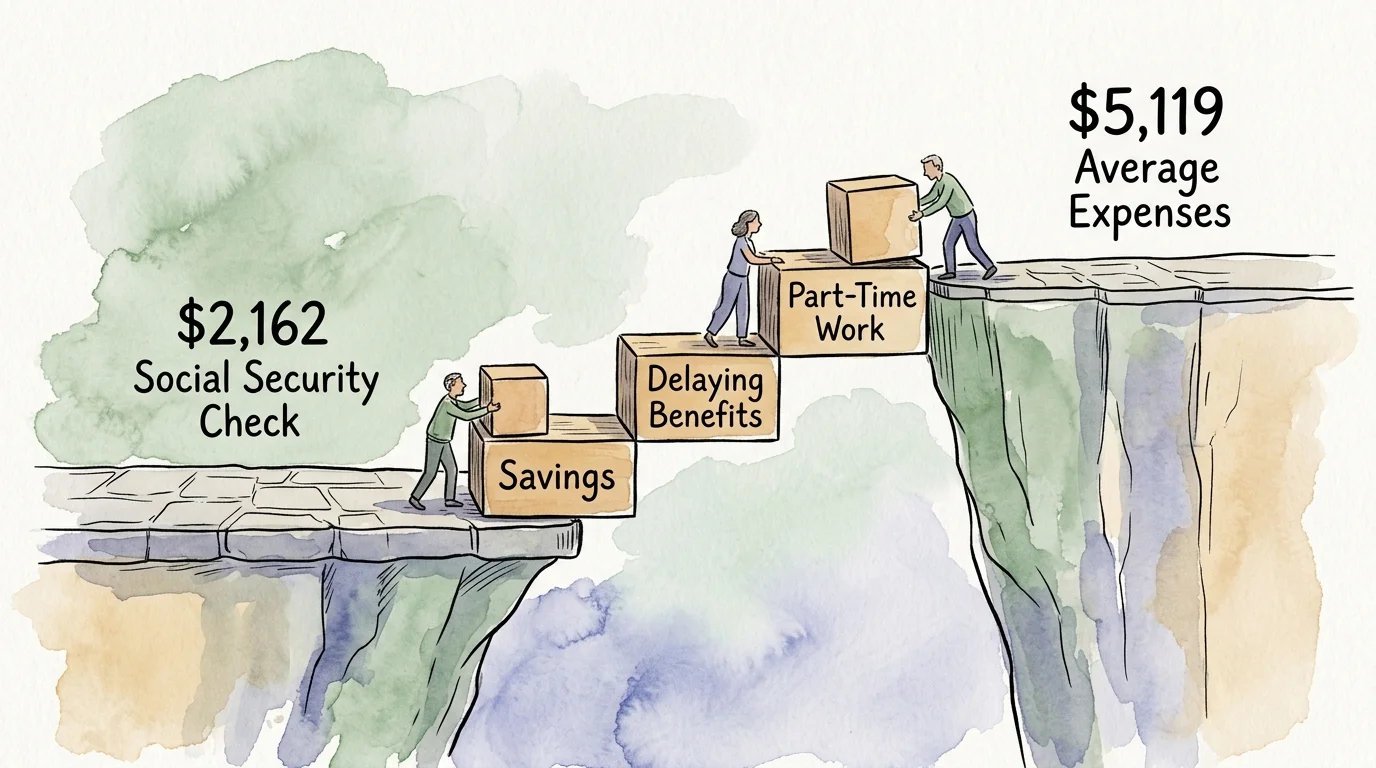

A projected $2,162 average Social Security check for 2027 might sound like a solid foundation, but you need to know exactly how far that money will stretch in the real world. For most Americans, relying entirely on this monthly payment is a fast track to financial stress, as average retiree household expenses now easily surpass $5,000 per month. This guide breaks down the math behind your future benefits and compares it directly against rising healthcare, housing, and daily living costs. By understanding the actual purchasing power of your Social Security income, you can confidently adjust your savings strategies, avoid common retirement traps, and build a concrete plan that truly supports the lifestyle you want.

The Reality of a $2,162 Monthly Benefit

The Social Security Administration calculates your retirement benefit based on your 35 highest-earning years, adjusted for historical wage growth and inflation. In 2026, the average monthly benefit for retired workers sat around $2,081. Based on recent cost-of-living adjustments and economic trends, that average payment is widely projected to climb to $2,162 by 2027.

On paper, an annual guaranteed income of roughly $25,944 from a government-backed program provides a comforting baseline. If you are married and both spouses qualify for a similar benefit amount based on individual work records, you are looking at over $51,000 in combined annual household income. However, you must evaluate this figure through the strict lens of actual living expenses rather than abstract numbers.

According to current data from the Bureau of Labor Statistics, the average household led by an individual aged 65 or older spends approximately $61,432 per year—which breaks down to about $5,119 per month. Immediately, you can see how the math becomes highly problematic. A single average Social Security check covers less than half of a typical retiree’s monthly budget.

This mathematical gap is exactly why financial educators consistently emphasize that Social Security was never intended to replace your entire working income.

“The big mistake: treating Social Security like a retirement plan. It was never designed to be one. It was designed to be a safety net.” — Dave Ramsey, Personal Finance Expert

Relying solely on this single stream of income leaves you highly vulnerable to inflation spikes, unexpected medical emergencies, and the inevitable costs of maintaining your home. You must actively confront where your money will go so you can accurately plan how to supplement your federal benefits with personal savings.

Medicare Premiums Take the First Bite

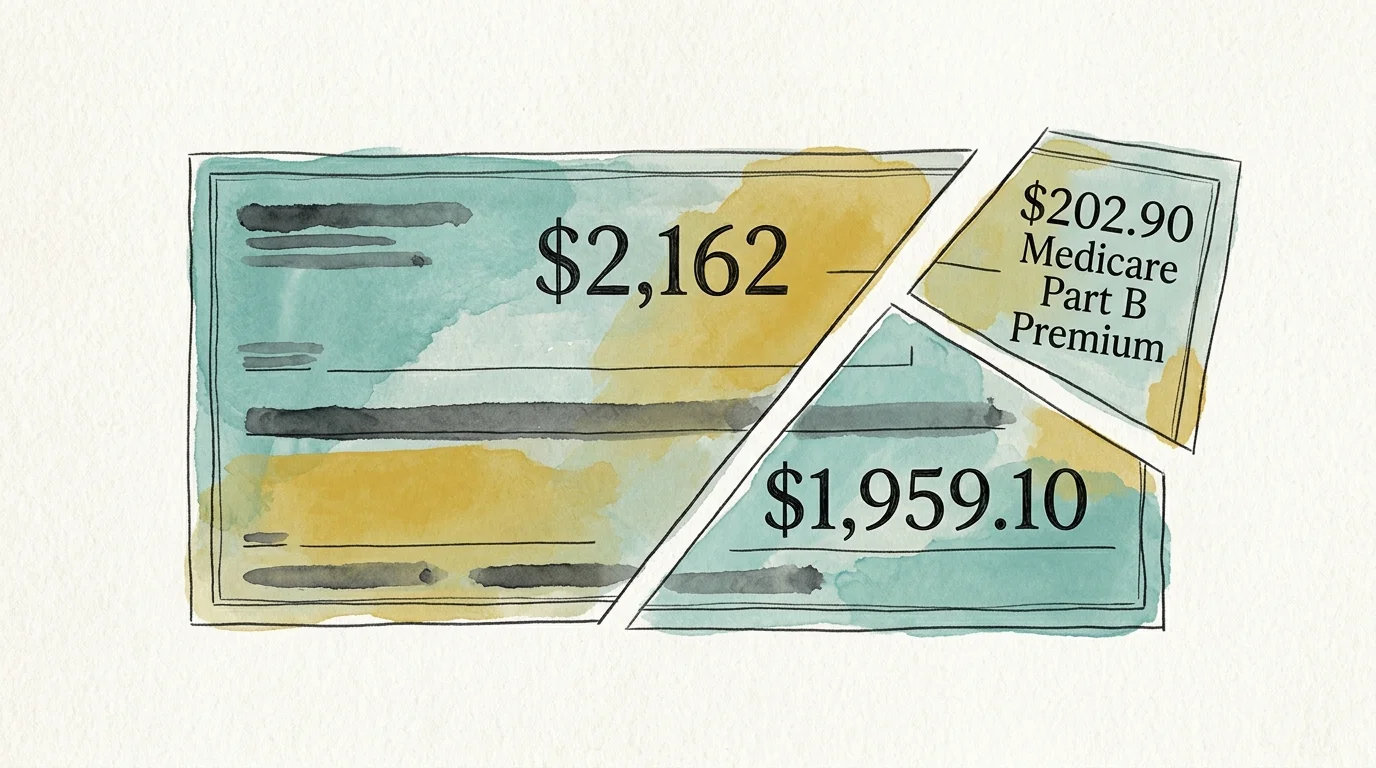

Before you even see that $2,162 hit your bank account, the federal government takes its share to cover your healthcare. Most retirees are automatically enrolled in Medicare Part B, which covers standard medical services such as doctor visits, preventative care, and outpatient procedures.

In 2026, the standard Medicare Part B premium increased to $202.90 per month. The Social Security Administration automatically deducts this premium directly from your monthly benefit before issuing your direct deposit. If you anticipate an average gross check of $2,162, your actual take-home amount immediately drops to $1,959.10.

Furthermore, if your modified adjusted gross income from two years prior exceeded specific thresholds, you will pay significantly more. Medicare imposes an Income-Related Monthly Adjustment Amount (IRMAA) on higher-earning retirees, which can push your Part B premium to more than double the standard rate. You must also factor in the costs of Medicare Part D (prescription drug coverage) premiums, along with any Medigap or Medicare Advantage plan premiums you choose to carry to limit your out-of-pocket exposure.

When you construct your retirement budget, you absolutely cannot use your gross Social Security benefit as your starting point. You must base your lifestyle choices and withdrawal strategies on the net amount that actually lands in your checking account.

The Big Three: Housing, Healthcare, and Food

Once Medicare takes its initial cut, your remaining funds must stretch to cover your day-to-day survival. For the vast majority of retirees, three distinct categories consume the lion’s share of their fixed income: housing, healthcare, and food.

Housing Costs Remain Substantial

Many pre-retirees operate under the assumption that paying off their mortgage means they will live housing-cost-free. This is a dangerous misconception that derails many financial plans. Even without a traditional mortgage principal and interest payment, you remain financially responsible for property taxes, homeowners insurance, routine maintenance, and utilities. The Bureau of Labor Statistics notes that housing remains the single largest expense for retirees, consuming an average of $22,193 annually, or about $1,849 per month. If your net Social Security check is just $1,959, basic housing expenses can devour nearly 95% of your guaranteed monthly income.

The Escalating Burden of Healthcare

While Original Medicare provides a vital foundation, it is far from comprehensive. You are still responsible for annual deductibles, copayments, and services completely excluded by Medicare—such as routine dental care, vision exams, and hearing aids. Recent projections from Fidelity Investments estimate that a single 65-year-old retiring in 2025 will need roughly $172,500 to cover general healthcare expenses throughout their retirement. Critically, this staggering figure does not even account for potential long-term care costs, such as assisted living or skilled nursing facilities, which can exceed $6,200 per month.

Food and Daily Sustenance

Food costs have consistently risen over the past several years, putting immense pressure on fixed-income households. The average retiree household spends heavily on groceries, dining out, and basic household supplies. When you combine the essential costs of housing, out-of-pocket healthcare, and food, it becomes mathematically impossible to survive on an average Social Security check without either severe lifestyle degradation or robust supplementary income.

| Expense Category | Average Monthly Cost (Age 65+) | Percentage of a $2,162 Gross SS Check |

|---|---|---|

| Housing (Taxes, Insurance, Maintenance, Utilities) | $1,849 | 85.5% |

| Transportation (Gas, Auto Insurance, Repairs) | $794 | 36.7% |

| Healthcare (Out-of-Pocket, Medigap, Dental) | $648 | 30.0% |

| Food & Groceries | $661 | 30.5% |

| Total Basic Expenses | $3,952 | 182.7% |

Note: Averages are drawn from the most recent Bureau of Labor Statistics data for households aged 65 and older. These figures demonstrate that an average Social Security check cannot cover even basic living expenses independently.

Common Mistakes to Avoid

Managing your retirement income requires precision and foresight. A single miscalculation regarding your benefits can permanently impair your financial security. You must actively avoid these common traps as you approach your target filing date.

Claiming Too Early Out of Fear

The earliest age you can claim Social Security retirement benefits is 62, but choosing this route results in a permanently reduced payout. If your full retirement age is 67 and you claim at 62, your monthly check is slashed by up to 30%. Many pre-retirees file early simply because they fear the program will run completely out of money. While the Social Security trust funds do face well-documented funding challenges in the 2030s, claiming early locks you into a heavily reduced payment for the rest of your life. This permanently damages your purchasing power and severely limits the raw dollar amount of your future cost-of-living adjustments.

Forgetting the Tax Man

Social Security benefits are not automatically tax-free. Depending on your combined income—calculated as your adjusted gross income plus any nontaxable interest and half of your Social Security benefits—up to 85% of your benefits may be subject to federal income tax. Furthermore, several states continue to tax Social Security benefits at the state level. Failing to account for taxes can lead to shocking tax bills in April and force you to deplete your personal investment accounts far faster than anticipated.

Underestimating the True Impact of Inflation

While Social Security does include an annual Cost of Living Adjustment (COLA), these percentage increases historically lag behind the actual, localized inflation rates experienced by older Americans. Healthcare premiums, prescription drugs, and property taxes typically rise much faster than the general Consumer Price Index used to calculate the COLA. If you simply assume your $2,162 check will possess the same functional buying power ten or fifteen years into your retirement, you will likely find yourself struggling to maintain your standard of living as you age.

Professional vs. Self-Guided: Planning Your Income

Effectively bridging the massive gap between your Social Security benefit and your actual living expenses requires a disciplined strategy. Depending entirely on the complexity of your financial life, you must decide whether to manage your portfolio withdrawals yourself or hire a professional fiduciary advisor.

- Scenario 1: You have substantial, easily accessible savings (Self-Guided). If you have built a large, uncomplicated nest egg primarily in low-cost index funds and require only a simple 3% to 4% withdrawal rate to supplement your $2,162 check, you may comfortably manage this process yourself. Utilizing free educational resources and automated withdrawal tools from major brokerages can help you set up a tax-efficient, recurring monthly “paycheck.”

- Scenario 2: You face complex tax considerations (Professional). If your lifetime assets are heavily fragmented across traditional 401(k)s, Roth IRAs, physical real estate, and standard taxable brokerage accounts, deciding precisely which account to draw from first is incredibly complicated. A certified financial planner or CPA can develop a strategic withdrawal sequence that minimizes your lifetime tax burden and carefully keeps your Medicare IRMAA surcharges in check.

- Scenario 3: You are coordinating spousal benefits (Professional). Married couples have highly intricate options for claiming Social Security, especially if there is a significant age gap or a major disparity in lifetime earnings. A professional advisor can utilize advanced software to determine the mathematically optimal month each spouse should claim in order to maximize lifetime household benefits and fiercely protect the surviving spouse’s future income.

Practical Strategies to Bridge the Gap

If the math clearly dictates that your expected Social Security check will fall significantly short of your lifestyle needs, you have actionable levers you can pull right now to drastically improve your retirement outlook. Do not wait until you have already submitted your claim to make these adjustments.

Delay Your Claim to Maximize Your Monthly Check

If you can manage to live on your personal savings or continue working part-time, delaying your Social Security claim is one of the most powerful financial moves available to you. For every single year you wait past your full retirement age—up to age 70—your base benefit increases by a guaranteed 8%. Therefore, a $2,162 check at age 67 could systematically grow to over $2,680 at age 70, and that figure does not even factor in the compounding effect of annual cost-of-living adjustments along the way. This higher baseline payment provides a significantly stronger hedge against longevity risk.

Aggressively Lower Your Fixed Costs

You cannot always control stock market returns or government tax policy, but you do retain ultimate control over your baseline spending. Consider strategically downsizing to a smaller, more energy-efficient home in a state with highly favorable retiree tax laws. Completely eliminating a mortgage, reducing unneeded square footage, and cutting your annual property taxes dramatically lowers your required monthly cash flow. When your fixed expenses drop, your Social Security check immediately stretches much further.

Optimize Tax-Efficient Withdrawals (The Roth Conversion)

If you retire at 62 but wait until 70 to claim Social Security, you enter a “gap” period where your taxable income might be artificially low. This presents a prime opportunity to convert funds from your traditional pre-tax IRA into a Roth IRA. While you will pay taxes on the conversion now, you do so at a much lower marginal rate. Later in retirement, when you are receiving your maximized Social Security check and forced to take Required Minimum Distributions (RMDs), you can pull from that Roth account completely tax-free. This keeps your taxable income low, protecting your Social Security benefits from heavier taxation.

Build Reliable, Supplemental Income Streams

Your investment portfolio must generate reliable, predictable cash flow to cover the massive expenses that Social Security misses. Dividend-paying index funds, municipal bond ladders, and high-yield cash equivalents can provide steady, passive distributions. If you desire absolute certainty and want to eliminate market anxiety, you might explore fixed annuities. An annuity effectively converts a portion of your accumulated savings into a guaranteed monthly paycheck, acting as a personal, private pension to seamlessly supplement your federal benefits.

Frequently Asked Questions

What is the maximum Social Security benefit you can receive?

The maximum benefit depends entirely on the age you choose to file. If you wait until age 70 to claim in 2026, the maximum possible benefit can exceed $4,800 per month. However, to actually achieve this absolute maximum, you must have earned the maximum taxable wage limit for at least 35 full working years.

Can I continue to work while receiving Social Security?

Yes, but if you claim benefits before reaching your full retirement age, your work earnings are strictly subject to an income limit. If you earn over a specific annual threshold (which the SSA updates yearly), the government temporarily withholds $1 in benefits for every $2 you earn above that limit. Fortunately, once you reach your full retirement age, you can earn an unlimited amount of money with zero penalty to your benefits.

Does my spouse automatically get half of my benefit amount?

A spouse can claim a spousal benefit worth up to 50% of your primary insurance amount, provided they wait until their own full retirement age to claim it. However, if your spouse claims this spousal benefit before reaching their full retirement age, the 50% percentage is permanently reduced. The SSA always pays out your spouse’s own earned benefit first; if the calculated spousal benefit is higher, they will add a supplemental amount to reach that higher number.

How do I find out exactly what my future check will be?

You should immediately create a free, secure “my Social Security” account on the official SSA.gov website. This portal allows you to review your lifetime earnings history for accuracy and provides highly personalized estimates of your future monthly benefits based on various claiming ages.

Reaching retirement is a massive life milestone, and your Social Security check will remain a critical, foundational component of your financial security. However, as the localized math clearly demonstrates, a projected $2,162 average check is simply not designed to fully fund a modern retirement on its own. Take active control of your future today by rigorously analyzing your expected expenses, maximizing your specific claiming strategy, and building a diversified, tax-efficient income plan.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.