Comparing Quality of Life: USA vs. Russia

Compare the 2026 quality of life between the USA and Russia, including life expectancy, healthcare access, and retirement income stability.

Read more →Your golden years are your best years! Make them shine!

Compare the 2026 quality of life between the USA and Russia, including life expectancy, healthcare access, and retirement income stability.

Read more →

Discover how state-by-state senior grocery discount programs, SNAP benefits, and farmers’ market vouchers can drastically reduce your food costs in 2026.

Read more →

Discover if the projected $2,162 average Social Security check for 2027 is truly enough to live on by comparing it to the real costs of housing and healthcare.

Read more →

Explore the best seasonal retail jobs for retirees to boost income before the holidays, featuring 2026 Social Security earnings limits and tax strategies.

Read more →

Discover what the average $2,082 Social Security check actually covers in 2026, from Medicare premiums to living expenses, and learn how to bridge your gap.

Read more →

Discover the exact number of Americans retiring daily during the Peak 65 wave and learn how it impacts your Social Security, Medicare, and taxes in 2026.

Read more →

Discover exactly how to claim Social Security divorced spouse benefits in 2026 to maximize your retirement income without involving your former spouse.

Read more →

Discover lesser-known state pension supplements, Medicare Savings Programs, and property tax relief initiatives that can drastically improve your retirement budget.

Read more →

Discover the fastest-growing retirement towns in the Mountain West for 2026, including practical insights on taxes, housing, and healthcare for your relocation.

Read more →

Discover the 2026 rules for Social Security survivor benefits, from earnings limits and remarriage clauses to strategies that maximize your retirement income.

Read more →

Discover the top 50 East Coast towns attracting retirees in 2026, featuring the latest data on taxes, housing, and healthcare to help you plan your move.

Read more →

Discover 10 essential financial benefits for retirees living strictly on Social Security, including Medicare Savings Programs, SNAP, and housing assistance.

Read more →

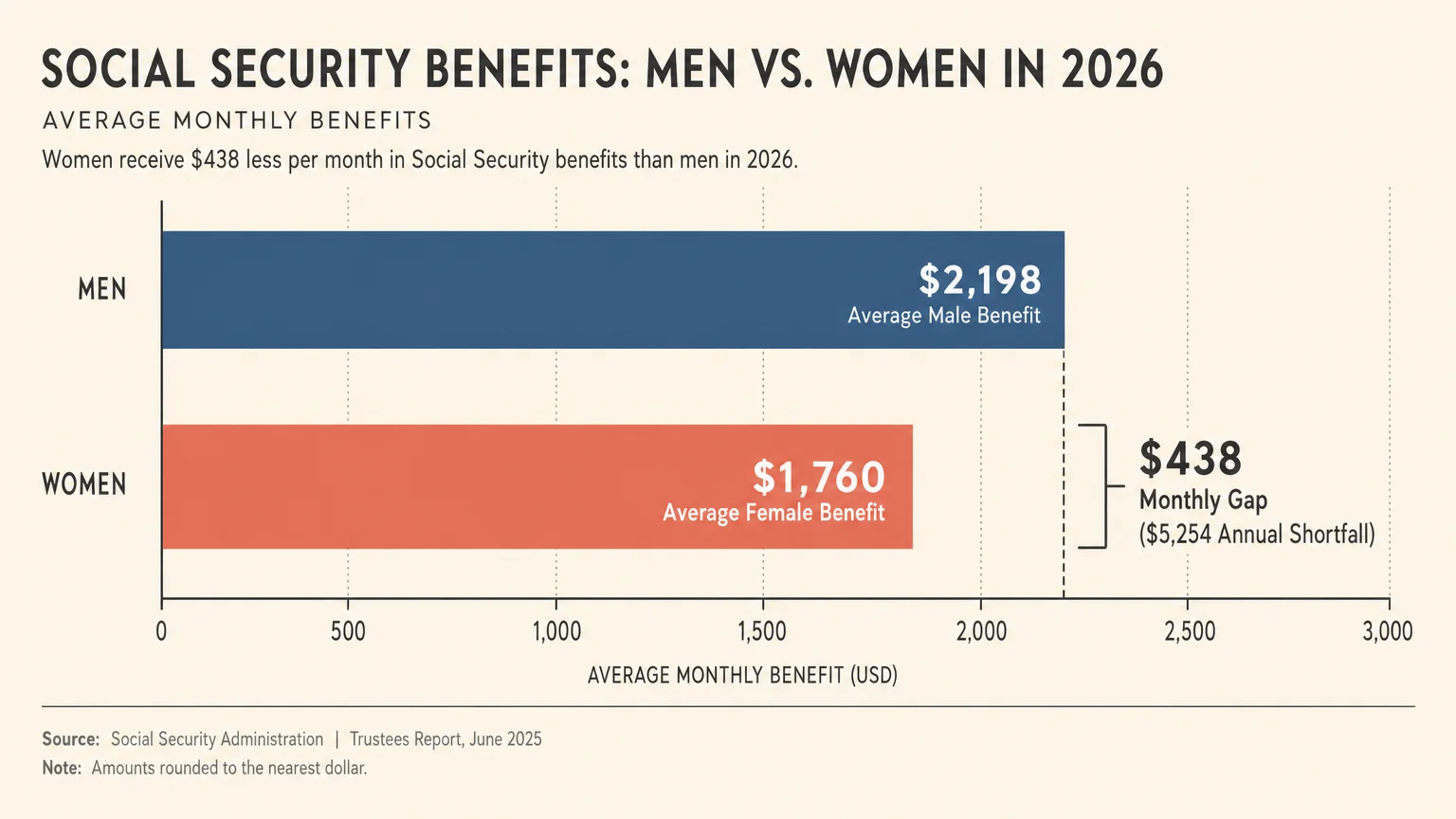

Learn why the $438 monthly Social Security gender gap exists, how 2032 cuts could impact women, and actionable strategies to maximize your retirement income.

Read more →

Discover how new 2026 retirement proposals, alternative asset rules, and the Saver’s Match impact your 401(k) strategy and long-term financial security.

Read more →

Discover eight flexible part-time jobs for retirees that offer supplemental income on your own schedule, plus 2026 tax and Social Security rules you must know.

Read more →