If your grandchild was born between 2025 and 2028, the government offers a $1,000 head start on their future. The One Big Beautiful Bill Act of 2025 created Trump Accounts to help families build wealth through index investing. You want to maximize every financial advantage for your family. These custodial-style retirement accounts provide federal seed money and potential private matching funds. The program officially launches for initial deposits on July 4, 2026. Parents and grandparents must understand the strict eligibility rules, contribution limits, and long-term tax implications. Before setting aside funds, learn exactly how these 530A accounts work and whether your grandchildren qualify.

What Exactly Are Trump Accounts?

Referred to officially as 530A accounts, Trump Accounts represent a new class of tax-advantaged investment vehicles introduced under the One Big Beautiful Bill Act (OBBBA). At their core, they function as starter Individual Retirement Accounts (IRAs) for minors. While the child technically owns the assets, an authorized adult—usually a parent or legal guardian—acts as the responsible party to manage the account until the child comes of age.

The federal government designed these accounts to encourage long-term market participation from birth. Rather than allowing cash to languish in low-yield savings accounts, the legislation forces early exposure to the American stock market. The program officially opens for initial family and employer contributions on July 4, 2026, corresponding with the 250th anniversary of the United States. The U.S. Treasury has already begun processing IRS Form 4547 elections and rolling out the official Trump Accounts mobile app to help families manage the setup process.

Eligibility Rules: Securing the Federal Seed Money

The headline feature of this new program is the federal seed contribution. However, not every child qualifies for this free government deposit. To receive the $1,000 pilot program grant, your grandchild must meet a strict set of criteria.

- Birth Year Window: The child must be born between January 1, 2025, and December 31, 2028.

- Citizenship: The child must be a U.S. citizen at birth.

- Documentation: The child must possess a valid Social Security number.

Noticeably absent from these requirements are income limits. Whether a family earns $40,000 a year or $4 million a year, an eligible newborn still qualifies for the $1,000 federal grant.

If you have older grandchildren born before 2025, they miss out on the federal seed money—but they are not entirely excluded from the program. Any U.S. citizen under the age of 18 with a valid Social Security number can still have a Trump Account opened in their name. Furthermore, a private philanthropic initiative led by the Michael & Susan Dell Foundation offers a $250 charitable deposit for up to 25 million children aged 10 or younger (born in 2014 or later) who live in ZIP codes where the median family income falls below $150,000.

How Parents and Grandparents Can Contribute

The $1,000 seed money serves only as a foundation. The real growth potential relies on continuous family contributions. The tax code allows parents, grandparents, and other relatives to deposit cash into the account, up to a combined maximum of $5,000 per year per child.

Unlike standard Individual Retirement Accounts—which require the account holder to have taxable, earned income reported on a W-2 or 1099—Trump Accounts carry no earned income requirement. A newborn with zero income can receive the full $5,000 annual contribution. By contrast, if you wanted to open a traditional or Roth IRA for your grandchild in 2026, the child would need actual job earnings, and contributions would be capped at their total earnings or the $7,500 IRS limit, whichever is less.

Employers also gain a unique tax incentive under the new law. A parent’s employer may contribute up to $2,500 annually to an employee’s child’s Trump Account. Crucially, this corporate contribution does not count toward the employee’s gross taxable income, making it a highly efficient fringe benefit.

Only one 530A account can exist per child. The Internal Revenue Service dictates a strict priority hierarchy regarding who holds the legal authority to open the account. The legal guardian holds first priority, followed by a parent, an adult sibling, and finally a grandparent. Even if you plan to fund the account entirely yourself, you will likely need to coordinate with your grandchild’s parents to ensure they properly file Form 4547 to establish the account.

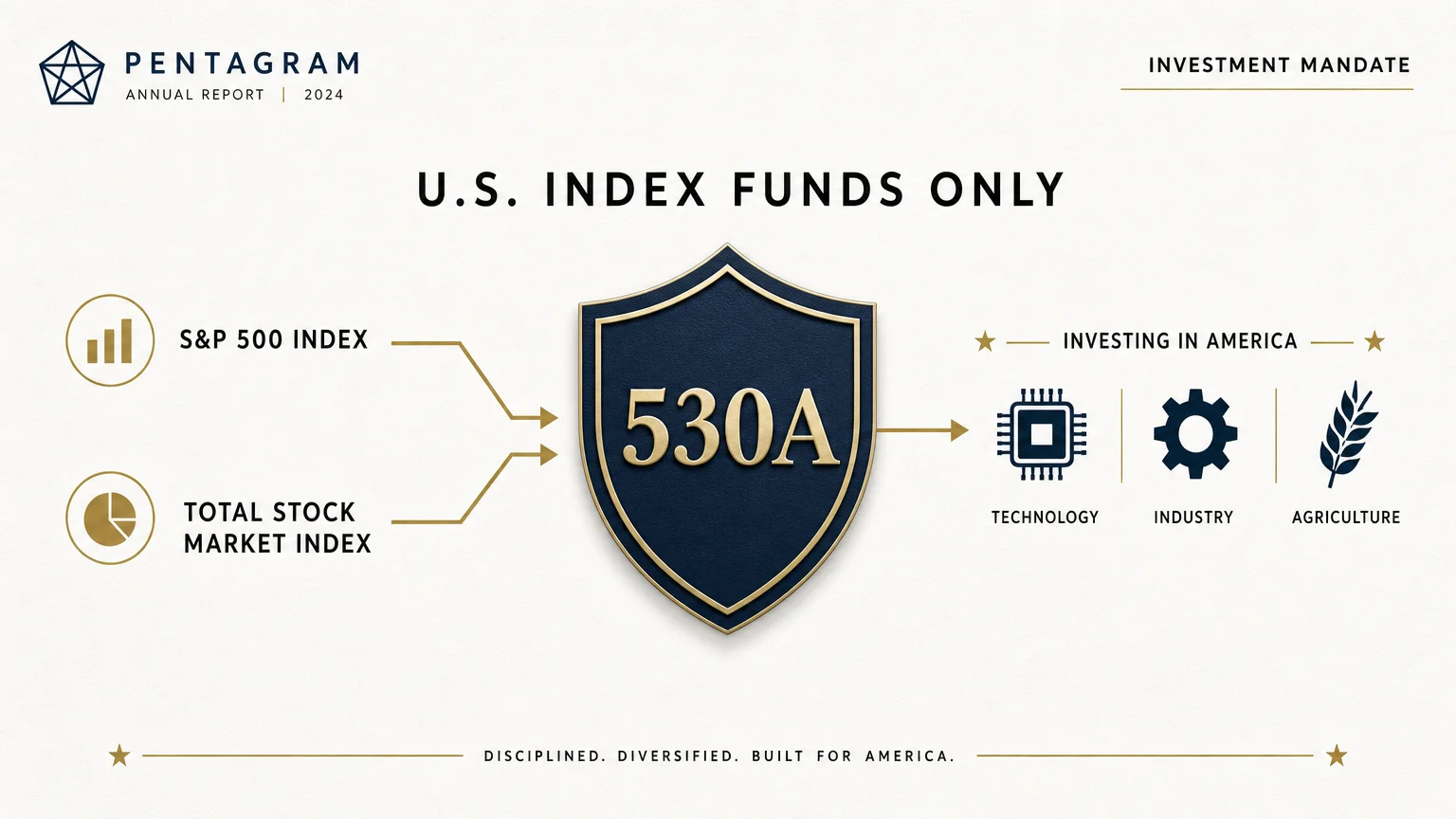

* 1. This

* 2. diagram

* 3. shows

* 4. U.S.

* 5. index

* 6. funds

* 7.

The Mandatory Investment Strategy: U.S. Index Funds Only

You cannot use a Trump Account to day-trade individual tech stocks, dabble in cryptocurrency, or purchase international bonds. The legislation imposes strict guardrails on how the money must be invested.

All deposits must be directed into low-cost mutual funds or exchange-traded funds (ETFs) that track a broad American stock market index, such as the S&P 500. To protect families from predatory Wall Street practices, the law legally caps the management fees (expense ratios) on these funds at just 0.10%, or 10 basis points. This restriction guarantees the child’s wealth compounds efficiently over time without being eroded by high administrative costs.

“By periodically investing in an index fund, for example, the know-nothing investor can actually out-perform most investment professionals.” — Warren Buffett, Chairman and CEO of Berkshire Hathaway

For a grandchild with an 18-year time horizon, an all-equity portfolio tracking the largest U.S. companies offers substantial growth potential. However, it also removes your ability to reallocate the assets into safer bonds as the child approaches college age. The Securities and Exchange Commission (SEC) regularly reminds investors that while index funds provide excellent diversification, 100% equity portfolios remain highly susceptible to short-term market volatility.

Comparing Savings Options for Grandchildren

A Trump Account adds a new tool to your wealth-transfer arsenal, but it does not replace the existing options. Depending on your financial goals, a 529 Education Plan or a Custodial Roth IRA might still serve your grandchild better. Evaluate the differences carefully.

| Account Feature | Trump Account (530A) | 529 Education Plan | Custodial Roth IRA |

|---|---|---|---|

| Primary Purpose | General wealth building and retirement | Qualified education expenses | Retirement or first-home purchase |

| 2026 Contribution Limit | $5,000 family + $2,500 employer | Varies by state (often $300,000+ lifetime) | $7,500 (or up to total earned income) |

| Earned Income Required? | No | No | Yes (child must have W-2 or 1099 income) |

| Federal Seed Money | $1,000 for 2025-2028 babies | None | None |

| Tax Treatment on Growth | Tax-deferred; taxed as ordinary income at withdrawal | Tax-free if used for qualified education | Tax-free withdrawals in retirement |

| Control Transfer | Child assumes full control at age 18 | Account owner (you) retains control indefinitely | Child assumes control at age 18 or 21 (varies by state) |

If your primary goal is paying for your grandchild’s university tuition or trade school, a 529 plan remains superior due to its completely tax-free withdrawals for education. If your teenage grandchild has a summer job, a Custodial Roth IRA provides unparalleled tax-free growth for their retirement. Trump Accounts fill the gap for young children without earned income whose families want to build general, non-education-specific wealth.

Avoiding Common Errors with 530A Accounts

New government programs always carry growing pains and hidden complexities. Grandparents eager to fund these accounts must navigate several potential pitfalls.

The Ordinary Income Tax Trap

The most significant drawback of a Trump Account lies in its tax structure. When you contribute up to $5,000 a year, you use after-tax money—meaning you cannot deduct the contribution from your own taxes. The money then grows tax-deferred for decades.

However, once the grandchild turns 18, the account functions almost identically to a traditional IRA. When they eventually withdraw the funds, the IRS taxes the entire distribution (both your original contributions and the market gains) at their ordinary income tax rate. Financial analysts at the Cato Institute point out that this structure can actually leave a family worse off than simply using a standard taxable brokerage account. In a standard brokerage account, long-term capital gains are taxed at much lower rates. Locking up after-tax money only to pay higher ordinary income rates upon withdrawal represents a hidden tax trap you must carefully consider before aggressively maxing out the $5,000 limit.

Triggering Your Own Medicare IRMAA Surcharges

Many retirees fund their grandchildren’s accounts by taking distributions from their own retirement portfolios. If you pull $5,000 out of your pre-tax traditional IRA to fund your grandchild’s Trump Account, that withdrawal adds directly to your Adjusted Gross Income (AGI). Spiking your AGI can inadvertently push you over the income thresholds for the Medicare Income-Related Monthly Adjustment Amount (IRMAA), causing your Part B and Part D premiums to skyrocket two years later. Always review current Medicare brackets at Medicare.gov before taking large taxable distributions to fund family gifts.

Assuming the Account Opens Automatically

The U.S. Treasury will not proactively hunt down your grandchild to hand them $1,000. An authorized adult must actively file IRS Form 4547 to establish the election. Treasury data indicates that families missing the filing windows will simply forfeit the federal seed money. Ensure the child’s parents have downloaded the official Trump Accounts app and submitted the necessary paperwork well ahead of the July 2026 deposit launch.

Ignoring the Early Withdrawal Penalties

These accounts are designed for the long haul. While the child gains legal control of the assets at age 18, they cannot simply cash out the account to buy a sports car without facing severe consequences. Because the account converts to traditional IRA rules, any withdrawals made before age 59½ that do not qualify for a short list of specific exemptions (such as higher education or a first-time home purchase) will trigger a 10% early withdrawal penalty on top of the ordinary income tax.

When DIY Isn’t Enough

While taking advantage of the free $1,000 federal grant is a simple, straightforward decision, deciding whether to contribute your own thousands of dollars annually requires a broader strategic view.

- Estate Planning: If you intend to pass down substantial wealth to your grandchildren, funneling it through a 530A account limits your control once they turn 18. An estate attorney can help you construct trusts that offer more robust asset protection.

- Tax Optimization: A Certified Public Accountant (CPA) can run projections comparing the future tax burden of a Trump Account against a 529 plan or an irrevocable trust.

- Coordinating Family Limits: Because the $5,000 annual limit applies per child—not per contributor—you must communicate with the child’s parents and the other set of grandparents. Accidentally overcontributing will trigger IRS excise taxes.

If you feel overwhelmed by these interconnected moving parts, consider locating a fiduciary advisor through the Certified Financial Planner Board to help integrate this new account into your family’s generational wealth strategy.

Frequently Asked Questions

When does my grandchild gain control of their Trump Account?

The child gains legal control of the account when they turn 18. At that point, the account operates under the standard rules of a traditional IRA, meaning they can choose different investments but will face taxes and penalties for early, non-exempt withdrawals.

Can an employer match contributions to a child’s 530A account?

Yes. An employer can contribute up to $2,500 annually to an employee’s child’s Trump Account. This corporate contribution does not count toward the parent’s taxable gross income, serving as a highly effective employment benefit.

Can I open multiple Trump Accounts for the same grandchild?

No. The law restricts each eligible child to one single Trump Account. If multiple family members wish to contribute, they must all coordinate to deposit funds into that single designated account, ensuring the total combined deposits do not exceed the $5,000 annual limit.

Does a 5-year-old qualify for the $1,000 government seed money?

No. The $1,000 federal pilot contribution is strictly reserved for children born between January 1, 2025, and December 31, 2028. However, a 5-year-old in 2026 (born in 2021) may qualify for the $250 Dell Foundation charitable grant if they reside in a qualifying ZIP code.

Practical Next Steps

The introduction of Trump Accounts gives American families a compelling new mechanism to foster financial literacy and long-term investment habits from birth. Your immediate priority as a grandparent should be ensuring the child’s parents properly file IRS Form 4547 to secure the $1,000 federal seed money for eligible newborns. Beyond that initial step, evaluate your own financial bandwidth. Compare the ordinary income tax structure of the 530A account against the tax-free benefits of a 529 plan before you commit to annual deposits. Educating yourself now ensures you can provide your grandchildren with the strongest possible financial foundation.

This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources. Last updated: June 2026.