Losing a spouse is devastating, and navigating the financial aftermath should not add to your burden. Social Security survivor benefits exist to replace a portion of your partner’s income, yet many retirees lose thousands of dollars by filing at the wrong time. Whether you are currently widowed or mapping out a long-term plan with your spouse, mastering these rules is vital. You possess unique options—such as claiming a reduced survivor benefit early while letting your personal benefit grow—that can dramatically alter your lifetime income. Understanding the precise claiming timelines, 2026 earnings limits, and remarriage rules empowers you to protect your household income and secure your financial future when you need it most.

How Survivor Benefits Are Calculated

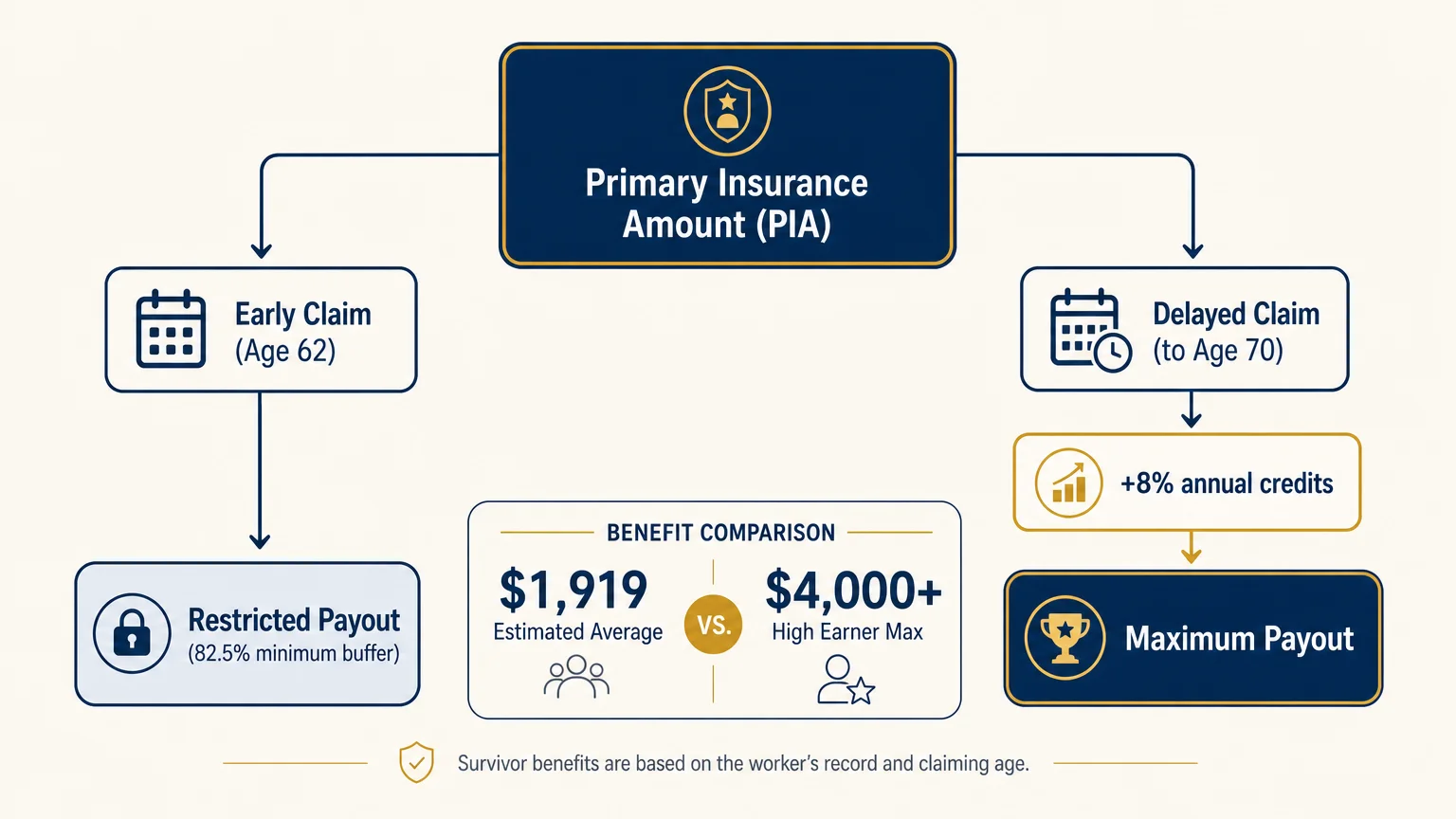

Social Security survivor benefits are designed to act as a financial safety net, but the amount you receive depends heavily on the earnings history and claiming decisions of your deceased spouse. The baseline for your payment is your spouse’s Primary Insurance Amount (PIA)—the exact monthly benefit they were entitled to receive at their full retirement age.

If your spouse waited until after their full retirement age to claim benefits, they accumulated delayed retirement credits. These credits increase their base payout by 8% for every year they delayed up to age 70. Fortunately, those delayed retirement credits fully transfer to your survivor benefit. This is a critical retirement planning strategy for married couples: when the higher-earning spouse delays claiming Social Security until age 70, they guarantee the maximum possible lifetime income for the surviving spouse.

Conversely, if your spouse filed for Social Security early—say, at age 62—their monthly benefit was permanently reduced. As a result, your survivor benefit will also be restricted. By law, your maximum survivor payout generally cannot exceed the amount your deceased spouse was receiving at the time of their death. The Social Security Administration does provide a slight buffer through a specific limitation rule, ensuring your benefit will not fall below 82.5% of your spouse’s base Primary Insurance Amount, regardless of how early they claimed.

Following the 2.8% Cost-of-Living Adjustment (COLA) implemented for 2026, the estimated average monthly benefit for an aged widow or widower living alone is $1,919. However, if your spouse was a high earner who delayed claiming until age 70, your monthly survivor check could easily exceed $4,000.

“Social Security is the foundation of your retirement house. You want to build it as strong and as big as you possibly can.” — Suze Orman, Personal Finance Expert

Eligibility Rules and Claiming Timelines

The rules governing when you can claim a survivor benefit differ significantly from standard retirement benefits. While you must wait until age 62 to draw your own retirement income, the Social Security Administration (SSA) allows you to begin collecting survivor benefits much earlier.

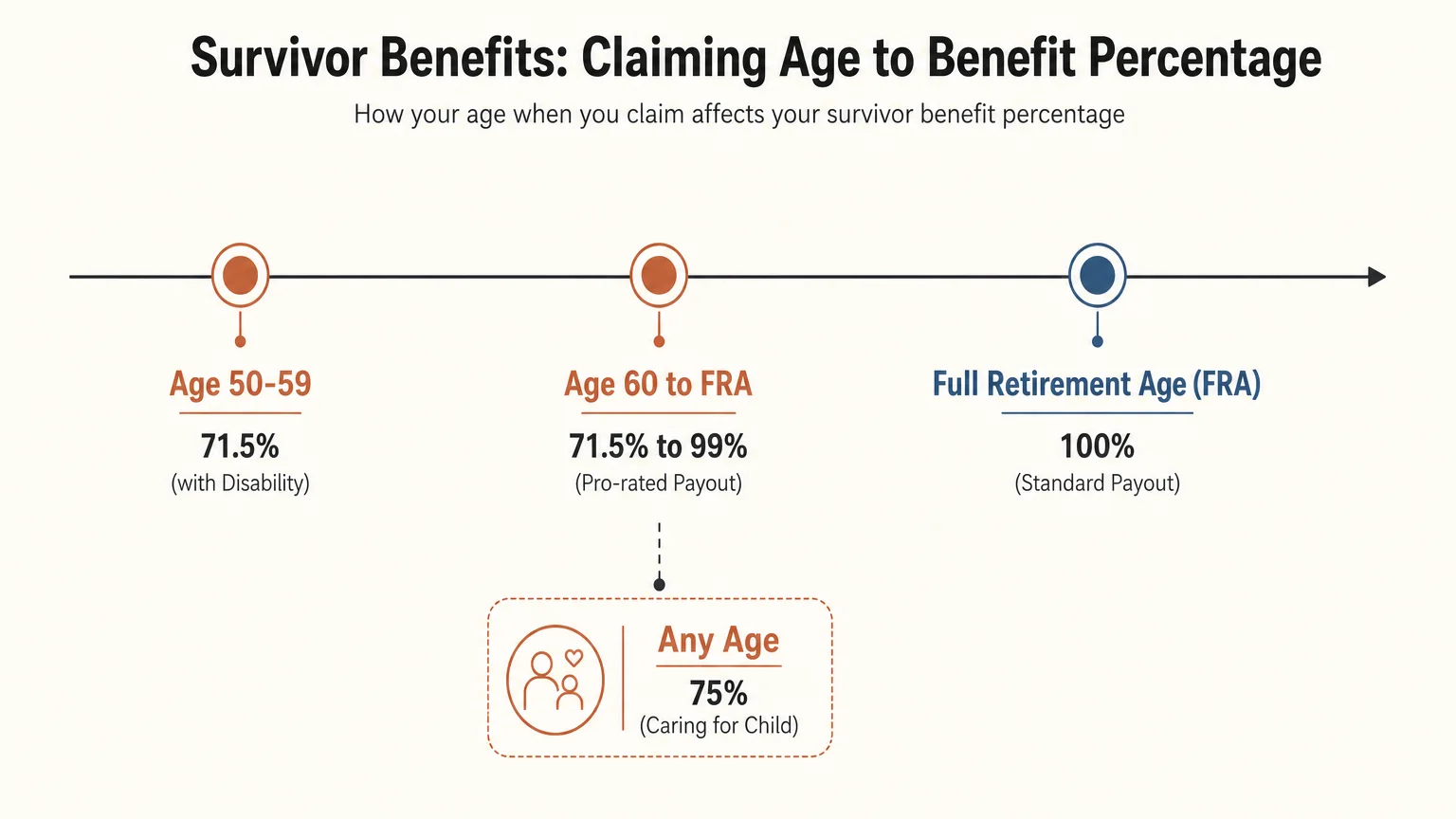

Your claiming options fall into several distinct age categories, each dictating the percentage of your spouse’s benefit you are eligible to receive. It is vital to understand that taking your survivor benefit before your designated survivor full retirement age results in a permanent reduction to your monthly check.

| Claiming Age | Percentage of Deceased Spouse’s Benefit | Eligibility Condition |

|---|---|---|

| Full Retirement Age (FRA) | 100% | Standard claiming age |

| Age 60 to FRA | 71.5% to 99% | Benefit pro-rated based on exact months filed early |

| Age 50 to 59 | 71.5% | Requires a qualifying disability that started before or within 7 years of the spouse’s death |

| Any Age | 75% | Must be actively caring for the deceased worker’s child who is under age 16 or disabled |

You must also identify your specific survivor full retirement age, which is calculated differently than your regular retirement age. For anyone born in 1962 or later, the survivor full retirement age is exactly 67. If you claim your survivor benefit the month you turn 67, you secure 100% of your deceased spouse’s allowable payout. Claiming at age 60 anchors you to the floor of 71.5% for the rest of your life.

Coordinating Your Benefits: The Switching Strategy

Perhaps the most powerful advantage built into the survivor benefits system is the ability to decouple your survivor payout from your own personal retirement payout. When both spouses are alive, a rule called “deemed filing” forces you to apply for all eligible benefits simultaneously; the SSA simply pays you the highest single amount. When you are a surviving spouse, deemed filing does not apply.

Because you are granted the flexibility to treat the two benefits independently, you can strategically sequence them to maximize your lifetime income. You can claim one benefit early while letting the other sit untouched to accumulate valuable delayed growth credits.

Consider a concrete example to illustrate this switching strategy: Jane (age 60) recently lost her husband, Mark. Jane’s own full retirement benefit at her age 67 will be $2,200 per month. Mark was a high earner receiving $2,800 per month when he passed away.

Jane opts to claim her survivor benefits immediately at age 60. Because she is claiming early, she receives the reduced rate of 71.5%, providing her with a reliable $2,002 per month to cover living expenses. Meanwhile, she entirely defers her personal retirement benefit. Jane lets her own record grow past her full retirement age, earning the 8% annual delayed retirement credits. By the time Jane turns 70, her personal benefit has grown roughly 24% to about $2,728 per month. She simply contacts the SSA, switches from her survivor benefit to her own optimized retirement benefit, and enjoys the higher payout for the rest of her life.

You can also execute this strategy in reverse. If your own earning history is relatively modest, you might claim your own reduced retirement benefit at age 62, creating immediate cash flow. Then, upon reaching your survivor full retirement age, you switch to the unreduced 100% survivor benefit.

The 2026 Earnings Limit: Working While Collecting

Many widows and widowers continue to work either out of necessity or a desire to stay engaged. If you are still working and decide to claim survivor benefits before reaching your full retirement age, your payouts are subject to the Social Security earnings limit. Earning too much money can temporarily wipe out your monthly check.

For 2026, the strict annual earnings limit is $24,480. If your wages from a job or net earnings from self-employment exceed this ceiling, the SSA will withhold $1 in benefits for every $2 you earn above the threshold. This reduction can drastically diminish the value of claiming early if you maintain a high salary.

During the specific calendar year you reach your full retirement age, the rules become far more lenient. The earnings limit jumps to $65,160 for 2026, and the penalty drops; the SSA only withholds $1 for every $3 earned above the limit, counting only the earnings accumulated in the months before your birth month. Once you officially reach your full retirement age, the earnings limit vanishes completely. From that point forward, you can earn an unlimited income without facing any reductions to your Social Security payments.

It is important to note that the money withheld due to the earnings test is not lost forever. When you reach your full retirement age, the SSA recalculates your benefit amount, removing the early-claiming reduction for the specific months your checks were withheld. This recalculation will permanently increase your monthly payout going forward.

Navigating Remarriage and Divorce Rules

Your marital status plays a pivotal role in your eligibility for survivor income. If you are a divorced spouse, you still possess strong rights to claim survivor benefits on your ex-spouse’s record, provided your marriage lasted for a minimum of 10 consecutive years. Drawing a survivor benefit as an ex-spouse has absolutely no impact on the benefits available to the deceased worker’s current widow or widower.

Remarriage, however, requires careful navigation. The SSA enforces a very strict “Age 60 Remarriage Rule” that determines whether you retain or forfeit your survivor benefits.

- Remarrying Before Age 60: If you remarry before you turn 60 (or before age 50 if you are disabled), you completely forfeit your right to collect survivor benefits on your deceased spouse’s record. You cannot collect these payments for as long as your new marriage remains intact.

- Remarrying After Age 60: If you wait to remarry until after you have reached age 60 (or age 50 if disabled), your new marriage will not affect your survivor benefits in any way. You will continue to receive the exact same monthly payout as if you had remained single.

If you remarry and your new spouse is also collecting Social Security, you have the option to apply for spousal benefits on their record if that amount would be higher than your current survivor benefit. The system ensures you receive the highest single payout available to you, but navigating the exact timing requires a clear understanding of your unique timeline.

Pitfalls to Watch For

Retirement planning is riddled with complexities, and the survivor benefit system is no exception. Avoid these common missteps to ensure you protect your household income.

Assuming You Get to Keep Both Checks: A widespread misconception is that surviving spouses inherit their partner’s monthly check in addition to their own. You do not keep both. The SSA simply pays you an amount equal to the higher of the two benefits. If your personal benefit is $1,800 and your spouse’s was $2,500, your total monthly income drops from $4,300 as a couple to a single check of $2,500 as a widow.

Triggering the Government Pension Offset (GPO): If you spent the majority of your career working in a job where you did not pay Social Security taxes—such as a public school teacher in certain states, a police officer, or a municipal employee—your survivor benefit will likely be impacted by the GPO. This provision reduces your Social Security survivor benefit by two-thirds of the amount of your government pension. For many public servants, this offset completely wipes out their survivor benefit. You must calculate this offset before making long-term financial plans.

Forgetting the Lump-Sum Death Payment: In addition to monthly income, the SSA provides a one-time lump-sum death payment of $255 to the surviving spouse who was living with the deceased. While the amount is modest, it helps defray immediate final expenses. You must explicitly apply for this payment within two years of your spouse’s death; it is not issued automatically.

Ignoring Medicare Premium Increases: Because the death of a spouse forces you to file your taxes as a single individual rather than married filing jointly, your tax brackets shrink significantly. Even if your overall income decreases, your modified adjusted gross income might push you into a higher bracket for Medicare Part B and Part D premiums. This surcharge, known as IRMAA (Income-Related Monthly Adjustment Amount), can quietly eat into your monthly survivor check.

How to Apply for Survivor Benefits

Unlike standard personal retirement benefits, you cannot simply log onto the Social Security website and apply for survivor benefits online. The SSA requires a more secure verification process to activate survivor payments.

You must apply either over the phone by calling the national toll-free number at 1-800-772-1213, or by scheduling an in-person appointment at your local Social Security office. When you prepare for your appointment, gather your essential documents. You will need your spouse’s original death certificate, your own birth certificate, your marriage certificate, and the Social Security numbers for both you and your deceased spouse. Have your bank account routing and account numbers ready to establish your direct deposit.

If you are already receiving standard spousal benefits on your partner’s record when they pass away, the transition is usually automatic. The SSA will convert your spousal benefit into a survivor benefit once they receive the official report of death from the funeral home or state vital records office. However, you should still contact the SSA to confirm the transition and apply for the $255 lump-sum payment.

Getting Expert Help

While the rules are clear, applying them to your unique financial footprint can be daunting. You should strongly consider consulting a fiduciary advisor, such as a professional from the Certified Financial Planner Board, or a dedicated Social Security optimization expert if you encounter the following scenarios:

- You and Your Spouse Were Both High Earners: Identifying the mathematically optimal month to switch between your survivor benefit and your personal benefit requires complex breakeven analysis, factoring in life expectancy and tax brackets.

- You Have Minor Children: If you are caring for young children who also qualify for survivor benefits, you must navigate the Family Maximum Limit. This cap restricts the total amount of money a single family can draw from one deceased worker’s record, usually landing between 150% and 180% of the base benefit.

- You Own a Business or Have Complex Income: Managing the 2026 earnings test of $24,480 while pulling business income or capital gains requires precise tax coordination to avoid sudden benefit suspensions.

Frequently Asked Questions

Can I claim survivor benefits if I am already receiving my own Social Security?

Yes. If your eligible survivor benefit is higher than the personal retirement benefit you are currently receiving, you can apply for survivor benefits. The SSA will pay your personal benefit first, and then add a supplemental amount to bring your total monthly payment up to the higher survivor amount.

Do Social Security survivor benefits increase with inflation?

Yes. Survivor payments are subject to the same annual Cost-of-Living Adjustment (COLA) as standard retirement and disability benefits. For example, survivor benefits increased by 2.8% in 2026, helping widows and widowers maintain their purchasing power against rising living costs.

Do I have to pay taxes on my survivor benefits?

Potentially, yes. Survivor benefits are taxed exactly like regular Social Security benefits. If your provisional income (half of your Social Security benefit plus all other taxable and non-taxable income) exceeds $25,000 for a single filer, up to 50% of your benefit may be subject to federal income tax. If your provisional income exceeds $34,000, up to 85% of your benefit may be taxed.

How long do survivor benefits last?

Once you begin receiving aged widow or widower benefits, the payments continue for the rest of your life. The only events that will stop these payments are if you remarry before age 60, or if you proactively choose to switch to your own higher personal retirement benefit at a later date.

Planning for or reacting to the loss of a spouse requires immense resilience. By taking control of your Social Security claiming strategy, you can ensure that your partner’s legacy of hard work continues to protect and sustain you throughout your retirement years. Gather your earnings statements, review the current earnings limits, and carefully evaluate your switching strategy before committing to a filing date. You have earned these benefits, and structuring them correctly will provide the financial peace of mind you deserve.

This article provides general retirement education and information only. Everyone’s financial situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.