Nearly 44 percent of American seniors rely entirely on Social Security, squeezing by on an average monthly benefit of just over $2,000. If your check barely covers basic living expenses, you are likely missing out on thousands of dollars in untapped federal and state assistance. Government agencies leave billions of dollars unclaimed every year simply because eligible retirees never apply. By tapping into these specific assistance programs, you can permanently erase your Medicare premiums, drastically slash your prescription drug costs, and significantly lower your monthly grocery and utility bills. Here is how you can stretch your fixed income further and access the ten most valuable benefits available to retirees living on Social Security.

1. Medicare Savings Programs (MSPs)

If you are enrolled in Medicare, your monthly Part B premium is automatically deducted from your Social Security check. In 2026, the standard Part B premium is $202.90 per month. For someone living strictly on a modest Social Security income, losing over $2,400 a year to healthcare premiums is devastating. Medicare Savings Programs are state-administered programs that pay these premiums for you.

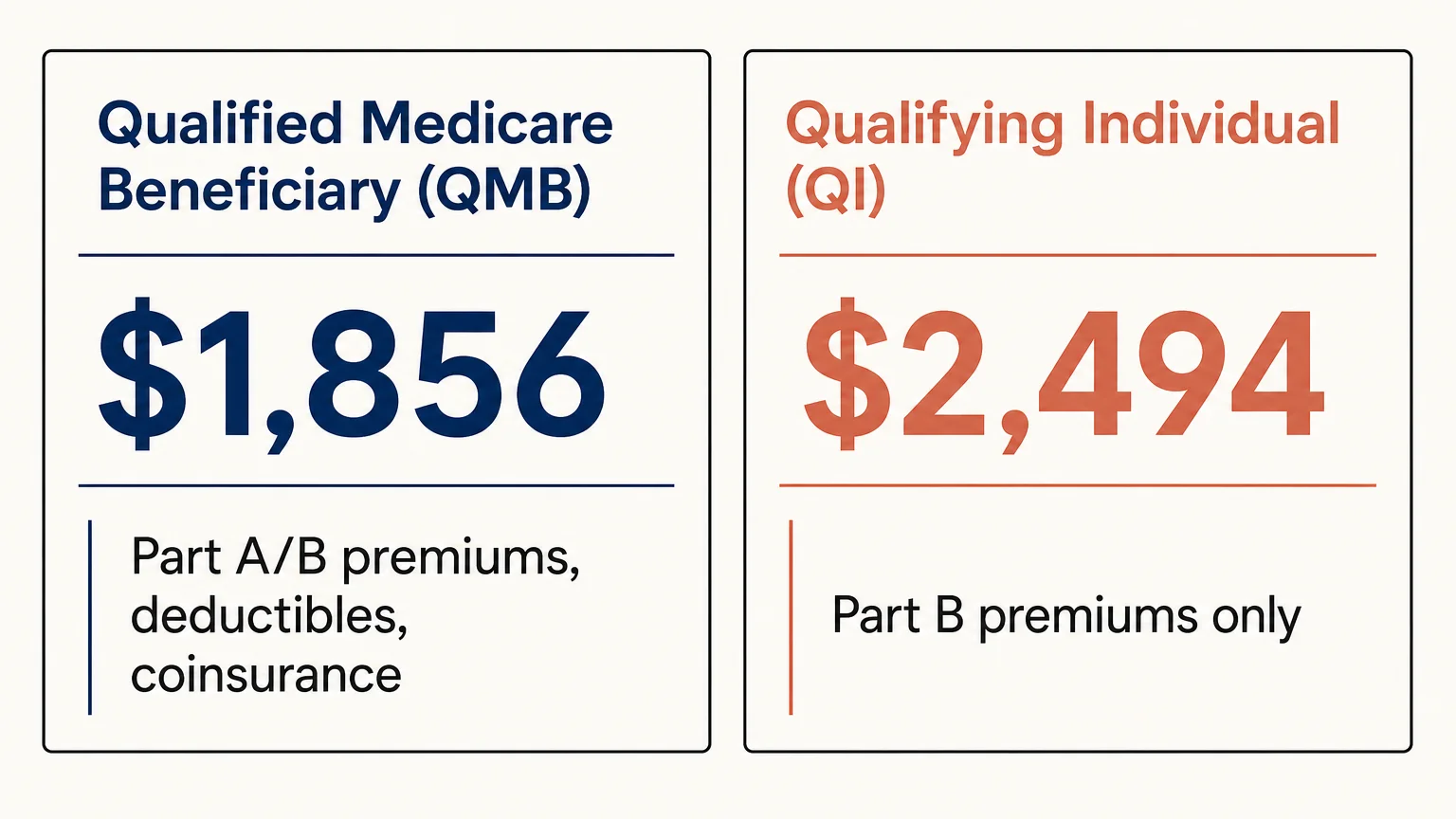

When you qualify for an MSP, your state Medicaid office covers your Part B premium, immediately returning that money to your monthly Social Security check. The most comprehensive tier, the Qualified Medicare Beneficiary (QMB) program, goes even further by paying your Part A and Part B deductibles, coinsurance, and copayments. Even if your income is slightly too high for QMB, you might still qualify for the Qualifying Individual (QI) tier, which solely covers the Part B premium.

| Medicare Savings Program | What It Covers | 2026 Monthly Income Limit (Individual) |

|---|---|---|

| Qualified Medicare Beneficiary (QMB) | Part A/B premiums, deductibles, and coinsurance | $1,856 |

| Specified Low-Income Medicare Beneficiary (SLMB) | Part B premiums only | Limits vary slightly by state |

| Qualifying Individual (QI) | Part B premiums only | $2,494 |

Limits generally include a standard $20 income disregard. Apply directly through your state’s Medicaid office or explore resources on Medicare.gov.

2. Extra Help for Prescription Drugs

Prescription medications can drain a retirement budget rapidly, but the federal Extra Help program—also known as the Part D Low-Income Subsidy—provides massive relief. Once you qualify, this program pays your Medicare Part D monthly premiums and annual deductibles. It also strictly caps your out-of-pocket pharmacy costs. In 2026, your copays are limited to $5.10 for each covered generic drug and $12.65 for each covered brand-name medication.

Thanks to recent changes under the Inflation Reduction Act, out-of-pocket prescription costs are fully capped at $2,100 per year. Once you hit that threshold, you pay absolutely nothing for covered drugs for the rest of the year. To qualify in 2026, individual income generally must fall below $2,015 per month, with total financial resources under $18,090. If you receive Medicaid, Supplemental Security Income, or an MSP, you are automatically enrolled in Extra Help.

3. Supplemental Security Income (SSI)

If your Social Security work history was brief or you had historically low wages, your standard retirement benefit might fall well below the poverty line. Supplemental Security Income is a federal cash assistance program designed specifically for individuals aged 65 and older, as well as disabled adults, who have severely limited income and assets.

In 2026, the maximum federal SSI standard payment amount is $994 per month for an individual and $1,491 for a couple. If your regular Social Security benefit is lower than this threshold, SSI can step in to make up the difference, providing a crucial floor for your monthly income. Additionally, qualifying for SSI often triggers automatic eligibility for Medicaid and SNAP benefits in most states.

“Social Security was never designed to be a retirement plan. It was designed to be a safety net.” — Dave Ramsey, Personal Finance Expert

4. Supplemental Nutrition Assistance Program (SNAP)

Formerly known as food stamps, SNAP provides monthly funds on an electronic benefit transfer (EBT) card to purchase groceries. Many older adults assume they will only qualify for the minimum benefit—often just $23 a month—and decide the paperwork is not worth the effort. This is a costly misconception.

Seniors enjoy special SNAP eligibility rules that can drastically increase their monthly food allowance. The most powerful rule is the excess medical expense deduction. If you spend more than $35 a month out-of-pocket on medical care—including Medicare premiums, prescription drugs, transportation to the doctor, and over-the-counter medical supplies—you can deduct these costs from your income when your SNAP benefit is calculated. Utilizing this deduction frequently results in hundreds of dollars in food assistance each month.

5. Low Income Home Energy Assistance Program (LIHEAP)

Heating a home in the winter and cooling it during summer heatwaves forces many retirees to choose between utility bills and basic necessities. The Low Income Home Energy Assistance Program provides federally funded grants to help you cover energy costs. LIHEAP funds are distributed directly to your utility company, applying a credit to your account so your monthly bills drop significantly.

Because states administer LIHEAP locally, the exact income limits and application periods vary depending on where you live. Many programs prioritize households with residents aged 60 and older. You can locate your local LIHEAP office through the Administration on Community Living.

6. Full-Coverage Medicaid

While Medicare serves as your primary health insurance after age 65, it does not cover everything. It entirely excludes long-term nursing home care, routine dental work, hearing aids, and standard vision exams. If you are living on Social Security alone, you may meet the strict income and asset requirements for full-coverage Medicaid.

When you have both Medicare and Medicaid—known as being “dual-eligible”—Medicaid acts as your secondary insurance. It sweeps up the deductibles and coinsurance that Medicare leaves behind. More importantly, Medicaid pays for in-home caregiving services and long-term facility care, completely shielding you from the devastating costs of aging.

7. Section 202 Supportive Housing for the Elderly

Housing represents the single largest expense for most retirees. The Department of Housing and Urban Development (HUD) oversees the Section 202 program, which creates affordable housing exclusively for very low-income seniors. These independent living communities are designed specifically for older adults, often featuring grab bars, ramps, and on-site care coordinators.

Under this program, your rent is legally capped at exactly 30 percent of your adjusted gross income. If your Social Security check is $2,000 a month, your rent will not exceed $600. Waitlists for Section 202 properties and standard Housing Choice Vouchers can span years, so it is imperative to apply through your local Public Housing Authority as soon as possible.

8. The Lifeline Program

Staying connected with family and healthcare providers is non-negotiable. The Federal Communications Commission manages the Lifeline program, which provides a standard $9.25 monthly discount on broadband internet or telephone service for eligible low-income subscribers. If you live on qualifying Tribal lands, the discount increases to $34.25 per month.

You automatically qualify for Lifeline if you currently receive Medicaid, SNAP, SSI, or Veterans Pension and Survivors Benefits. The application process is straightforward and handled directly through participating telecommunications providers.

9. Weatherization Assistance Program (WAP)

While LIHEAP helps pay your utility bills, the Weatherization Assistance Program actively upgrades your home to permanently reduce your energy consumption. If you own your home but cannot afford major repairs, WAP dispatches professional contractors to inspect and improve your property free of charge.

Services typically include installing heavy-duty insulation, sealing drafts around windows and doors, repairing or replacing highly inefficient heating systems, and upgrading thermostats. These permanent structural improvements save the average participating household hundreds of dollars every single year in avoided energy costs.

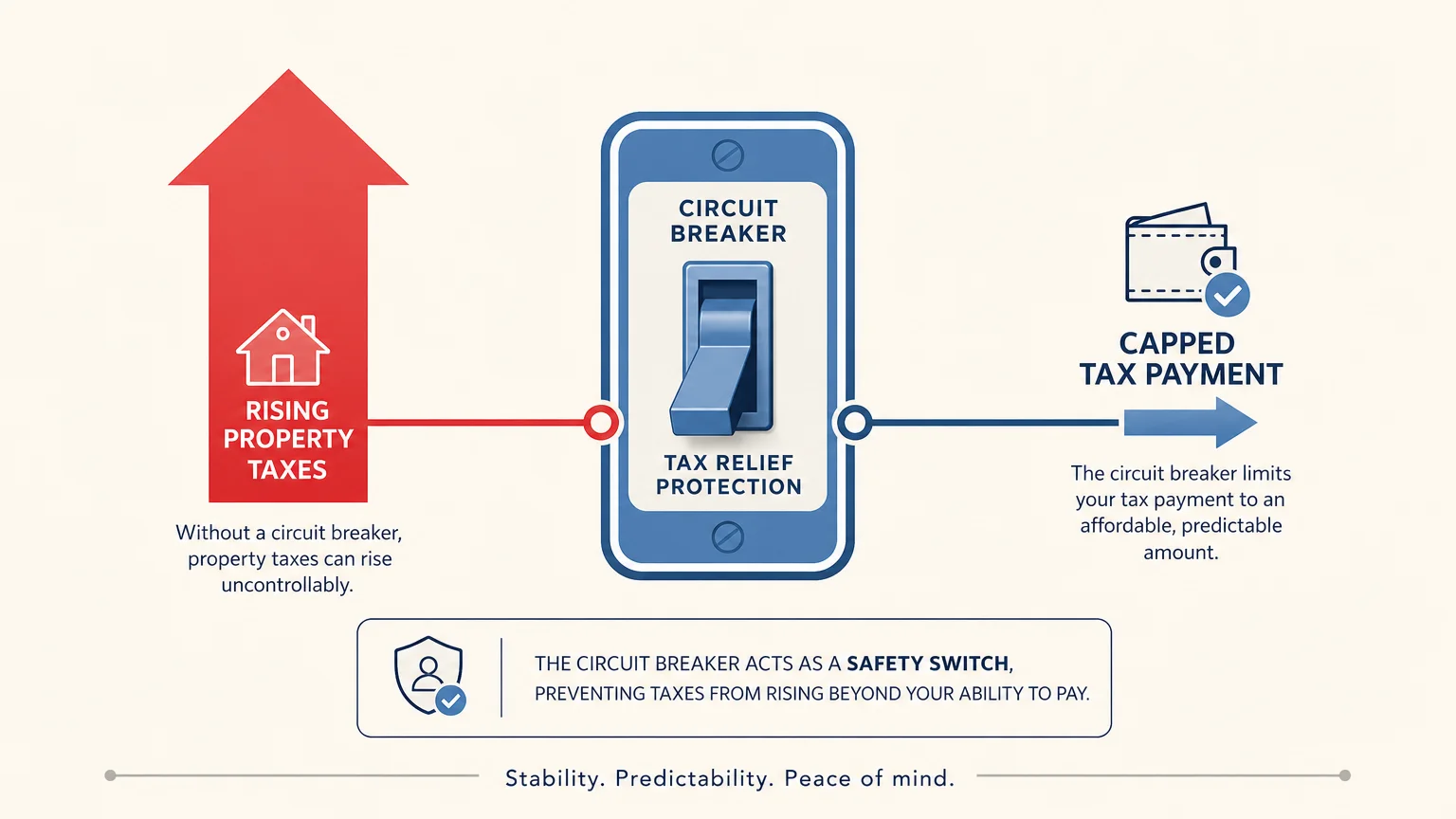

10. Property Tax Circuit Breakers

Rising property taxes threaten to price older homeowners out of houses they paid off decades ago. To prevent this, nearly every state offers some form of property tax relief exclusively for seniors. These programs are frequently referred to as “circuit breakers” because they trigger a tax freeze, deferral, or total exemption when your property tax burden exceeds a certain percentage of your fixed income.

Because property taxes are assessed at the county or municipal level, you must apply through your local tax assessor’s office. Never assume your local government automatically applies these discounts to your tax bill; you must proactively request the application and submit proof of your age and income.

Getting Expert Help

Navigating the maze of government bureaucracy is exhausting. You do not have to tackle these applications alone. Take advantage of free, unbiased assistance through these organizations:

- State Health Insurance Assistance Programs (SHIP): Reach out to a SHIP counselor for free, one-on-one guidance regarding Medicare Savings Programs and Extra Help. They can pinpoint exactly which health benefits you qualify for.

- Area Agencies on Aging (AAA): Your local AAA serves as a central hub for senior assistance. Case managers there can screen you for SNAP, LIHEAP, and local transportation benefits all at once.

- BenefitsCheckUp: Managed by the National Council on Aging, this free online tool allows you to input your zip code and basic financial details to generate a comprehensive list of programs you qualify for locally.

Pitfalls to Watch For

As you apply for these valuable safety nets, remain vigilant about a few common stumbling blocks that cause retirees to lose their benefits:

- Ignoring Asset Limits: Programs like SSI and full Medicaid strictly monitor your bank accounts. Typically, individual asset limits hover around $2,000, excluding your primary residence and one vehicle. Keep precise track of your checking and savings balances.

- Failing to Recertify: Government assistance is rarely permanent without periodic reviews. You must fill out recertification paperwork annually or bi-annually. Ignoring mail from your local social services office will result in automatic termination of your benefits.

- Overlooking Local Add-Ons: Federal programs grab the headlines, but state and county governments offer unique benefits like discounted public transit passes, utility life-support discounts, and free local community college courses. Always ask your local AAA what hyper-local programs exist in your specific county.

Frequently Asked Questions

Are these assistance benefits taxed as income?

No. Need-based government assistance—including SSI, SNAP, LIHEAP, and housing vouchers—is generally exempt from federal and state income taxes. These benefits exist to support your basic living standards, not to trigger a tax liability.

Can I apply for multiple assistance programs at once?

Yes, and you absolutely should. Qualifying for one program often streamlines your application for others. For instance, being approved for SSI typically grants you automatic eligibility for Medicaid and the Extra Help prescription drug program.

How do I know if my life insurance policy counts against my asset limits?

Term life insurance generally does not count as a financial asset because it holds no cash value. However, whole life insurance policies that accumulate cash value are scrutinized by Medicaid and SSI. If the cash surrender value exceeds the program’s asset thresholds, it could disqualify you. Consult a financial counselor or elder law attorney to review your specific policies.

Your Next Steps

Securing these benefits requires patience and persistence. Gather your current financial documents, bank statements, and Social Security award letters so you have everything ready for applications. Start by contacting your local Area Agency on Aging or SHIP counselor to screen your eligibility across multiple programs simultaneously. This is educational content based on general retirement planning principles. Individual results vary based on your situation. Always verify current benefit amounts, tax laws, and eligibility with official sources.

Last updated: June 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.