You could be walking away from thousands of dollars in retirement income if you overlook Social Security divorced spouse benefits.

When your marriage ends, your connection to your ex-spouse’s earnings record doesn’t automatically disappear; yet many retirees mistakenly believe they forfeit these benefits once the divorce is finalized.

Understanding the exact requirements allows you to claim up to 50% of your former spouse’s full retirement age benefit without their involvement. Whether you are nearing age 62, working part-time, or adjusting your financial strategy after a separation, knowing how these specific rules apply is critical.

This article breaks down the essential 2026 Social Security regulations, eligibility criteria, and claiming strategies you need to maximize your monthly income.

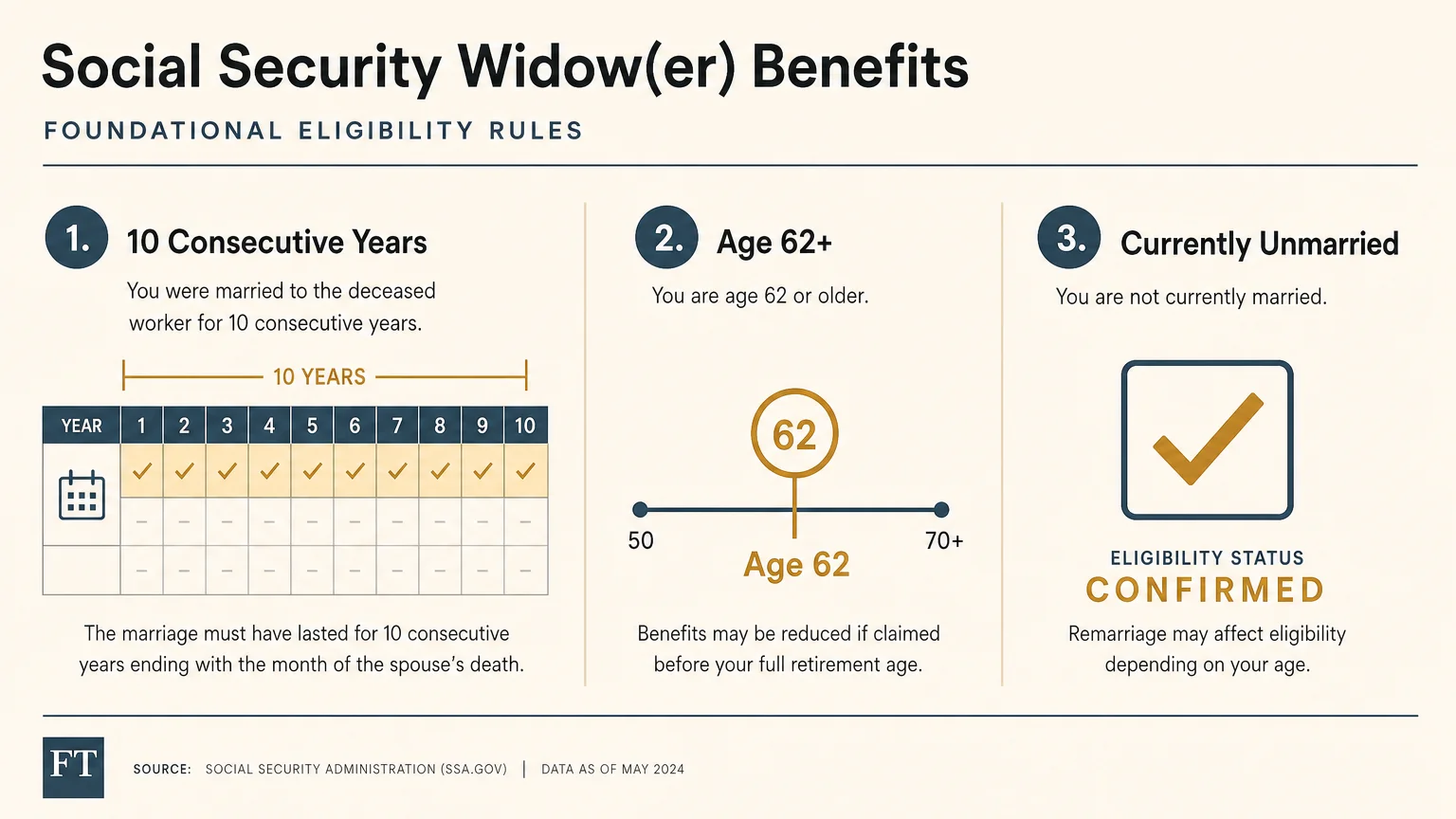

The 10-Year Rule and Foundational Eligibility

The Social Security Administration maintains strict criteria that govern whether you can legally claim benefits based on a former spouse’s earnings history. The primary hurdle most retirees face is the duration of the marriage. To qualify, you must have been married to your ex-spouse for a minimum of 10 consecutive years before the divorce became final. If your marriage lasted nine years and eleven months, you are unfortunately ineligible for this specific benefit class.

Assuming you meet the 10-year requirement, several other conditions must align for you to draw a divorced spousal benefit in 2026:

- Age requirement: You must be at least 62 years old to initiate a claim for standard spousal benefits.

- Current marital status: You must be currently unmarried. If you remarry, you forfeit your ability to collect benefits on your ex-spouse’s record unless your subsequent marriage ends through death, divorce, or annulment.

- Your ex-spouse’s entitlement: Your former spouse must be entitled to Social Security retirement or disability benefits.

- Your independent earnings record: Social Security will only pay you the divorced spouse benefit if it is higher than the benefit you would receive based on your own work history. You cannot stack the benefits; the government pays an amount equal to the higher of the two.

A common friction point for divorced retirees is the belief that their ex-spouse must actually be receiving checks for the spousal benefit to activate. This is not entirely true. If your ex-spouse qualifies for benefits but has delayed claiming them, you can still file for your divorced spouse benefits provided you have been legally divorced for at least two consecutive years.

I unfortunately was divorced on 3/1/85.

My 10 year anniversary would have been on 6/7/85. My attorney did not protect me. Did he? Is there anything I can do about this?

I was married to Rachel Clark ,for 18 yrs. Am I entitled to her ssi.

Married to Rachel Clark,Key. For 18.5 years. Can I file on her SSI?

I have been devorced for 24 years