The Mountain West offers retirees an unbeatable combination of lower taxes, sweeping landscapes, and thriving local economies. Instead of crowding into traditional sunbelt states, savvy older adults are relocating to fast-growing mountain communities that provide a higher quality of life without coastal price tags. Towns in Idaho, Utah, Colorado, and Wyoming are expanding their healthcare infrastructure and senior amenities to welcome this influx of new residents. Moving to these booming areas allows you to stretch your retirement savings while enjoying world-class outdoor recreation right outside your front door. Whether you seek the zero-income-tax benefits of Wyoming or the mild, high-desert climate of Utah, the Mountain West delivers practical financial advantages wrapped in an active, community-focused lifestyle.

Why the Mountain West is the New Retirement Frontier

Recent demographic shifts show a clear migration away from high-cost coastal states toward the interior West. Retirees are leading this charge, seeking out locations that offer a balanced cost of living, outdoor recreation, and favorable tax policies. The Census Bureau estimates for 2025 and 2026 confirm that states like Idaho, Utah, and Nevada remain among the fastest-growing in the nation.

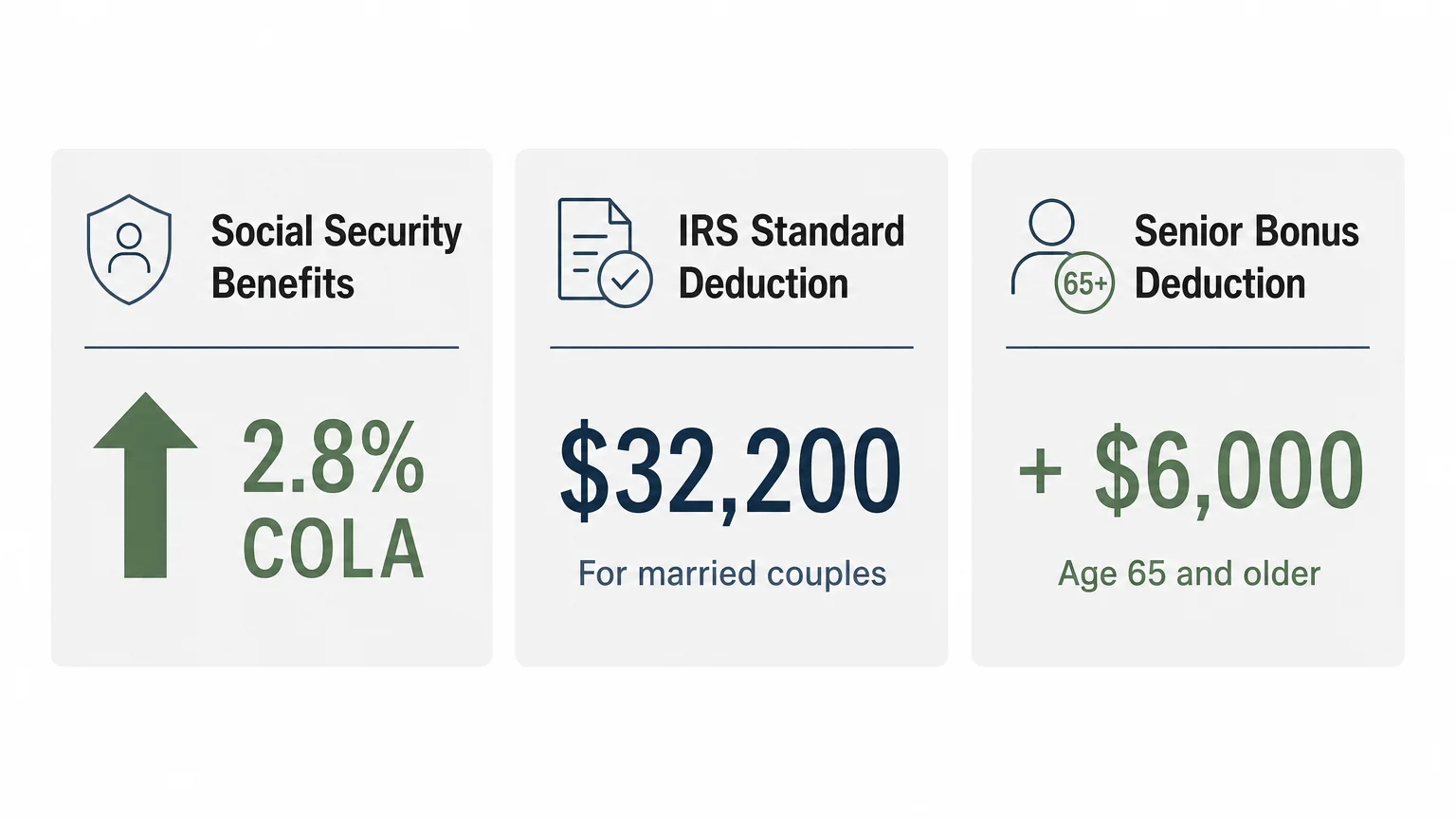

The appeal goes beyond just scenery. These states offer concrete financial advantages. For instance, the 2026 Social Security Administration Cost-of-Living Adjustment (COLA) increased benefits by 2.8%. When you live in a state with a lower overall tax burden, that COLA stretches significantly further. Additionally, many Mountain West states do not tax Social Security income, allowing you to keep more of your hard-earned benefits. Combine this with the 2026 IRS standard deduction of $32,200 for married couples filing jointly—plus the new $6,000 senior bonus deduction for those 65 and older—and you have a recipe for significant tax efficiency.

Top Fast-Growing Retirement Towns to Consider

If you plan to relocate, you want a town that balances small-town charm with necessary amenities like high-quality healthcare and shopping. Here are the standout retirement destinations in the Mountain West experiencing rapid growth:

- Colorado Springs, Colorado: Located at the base of Pikes Peak, Colorado Springs offers world-class outdoor access and a cost of living that is 20% to 30% lower than nearby Denver. The city boasts excellent healthcare facilities and a robust economy.

- Boise and Coeur d’Alene, Idaho: Idaho consistently ranks as a top retirement destination due to its low crime rates and affordable housing. Boise offers a vibrant cultural scene with roughly 210 sunny days a year, while Coeur d’Alene provides stunning lakeside living.

- Eagle Mountain, Utah: As one of the fastest-growing cities in Utah, Eagle Mountain offers modern housing developments and wide-open spaces, all within a short drive of Salt Lake City’s premier medical centers.

- Rock Springs, Wyoming: For the ultimate tax break, Wyoming imposes no state income tax. Rock Springs offers an active downtown, access to the Flaming Gorge National Recreation Area, and housing values averaging around $300,000.

- Montrose, Colorado: Known for negligible traffic and unbeatable access to outdoor recreation, Montrose is developing active adult communities designed specifically for retirees looking to age in place.

Comparing Taxes and Living Costs by State

When evaluating the fastest-growing retirement towns, you must look at the state-level tax landscape. Relocating across state lines impacts everything from your property taxes to how your pension is treated.

| State | State Income Tax | Social Security Taxed? | Notable Retirement Benefit |

|---|---|---|---|

| Wyoming | None (0%) | No | No state income, estate, or inheritance tax. |

| Nevada | None (0%) | No | Zero income tax and highly favorable business environment. |

| Colorado | Flat rate (4.40%) | Exempt for ages 65+ | Very low property taxes compared to the national average. |

| Idaho | Flat rate (5.69%) | No | Low overall cost of living and affordable housing. |

| Utah | Flat rate (4.65%) | Partially taxed | High-quality healthcare networks and active senior communities. |

Keep in mind that while state taxes are important, federal costs also impact your budget. For 2026, the standard Medicare Part B monthly premium increased to $202.90, with an annual deductible of $283. Budgeting for these fixed national healthcare costs is crucial, regardless of where you decide to live.

“When considering a relocation in retirement, you must balance the emotional pull of a new adventure with the hard math of taxes, healthcare, and cost of living.” — Jean Chatzky, Financial Editor and Author

Common Mistakes to Avoid

Relocating to a mountain town sounds idyllic, but retirees often make avoidable errors during the transition. Keep these pitfalls in mind:

- Underestimating the Altitude and Weather: Many Mountain West towns sit at elevations above 5,000 feet. This can exacerbate cardiovascular or respiratory conditions. Always consult your physician and spend an extended period in the town before buying property.

- Ignoring Healthcare Logistics: A small mountain town might look perfect on a postcard, but if it lacks specialists, you will face long drives for routine care. Verify that the local hospital system can manage your specific health needs. Veterans should specifically check wait times and proximity to VA clinics, which vary widely between states.

- Triggering Medicare IRMAA Surcharges: If you sell a highly appreciated home in an expensive state to pay cash for a home in Idaho or Wyoming, that large capital gain will spike your adjusted gross income. This can trigger an Income-Related Monthly Adjustment Amount (IRMAA), significantly increasing your Medicare Part B and Part D premiums two years later.

Professional vs. Self-Guided Relocation

Moving across the country during retirement involves complex financial and logistical moving parts. Here is how to decide if you need professional help:

- Self-Guided: If you are renting a home first, have straightforward finances (e.g., standard IRA withdrawals and Social Security), and are moving to a town you already know well, you can likely manage the transition yourself.

- Professional Real Estate Agent: If you are buying a home in a competitive, fast-growing market like Boise or Colorado Springs, a local agent who specializes in senior relocations can help you navigate competitive bidding and find age-in-place features.

- Tax Professional or Financial Planner: If you are selling a business, liquidating a large primary residence, or moving between states with vastly different tax codes, consult a fiduciary. They can help you time your income to avoid Medicare surcharges and maximize your 2026 tax brackets.

Frequently Asked Questions

What is the most tax-friendly state in the Mountain West?

Wyoming and Nevada are the most tax-friendly states in the region, as neither levies a state income tax. They also do not tax Social Security benefits, pensions, or retirement account withdrawals.

Are housing prices affordable in the Mountain West?

Affordability varies. While major hubs like Denver and Salt Lake City have seen significant price increases, smaller, fast-growing towns remain accessible. For example, Rock Springs, Wyoming, and Price, Utah, feature median home values around $300,000, which sits comfortably below the national average.

How does the 2026 standard deduction impact my retirement relocation?

The 2026 IRS standard deduction is $32,200 for married couples, plus a new $6,000 senior bonus deduction per eligible person age 65 and older. This means a married couple over 65 can shield up to $44,200 of income from federal taxes. Moving to a state with no income tax maximizes this federal benefit, leaving more cash in your pocket to fund your lifestyle.

Planning your move carefully ensures your new mountain home provides the perfect backdrop for your golden years. Take time to visit these growing communities, assess your healthcare needs, and run the tax numbers with a professional. The mountains are calling, and with the right strategy, your retirement can be as expansive as the western sky. The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.