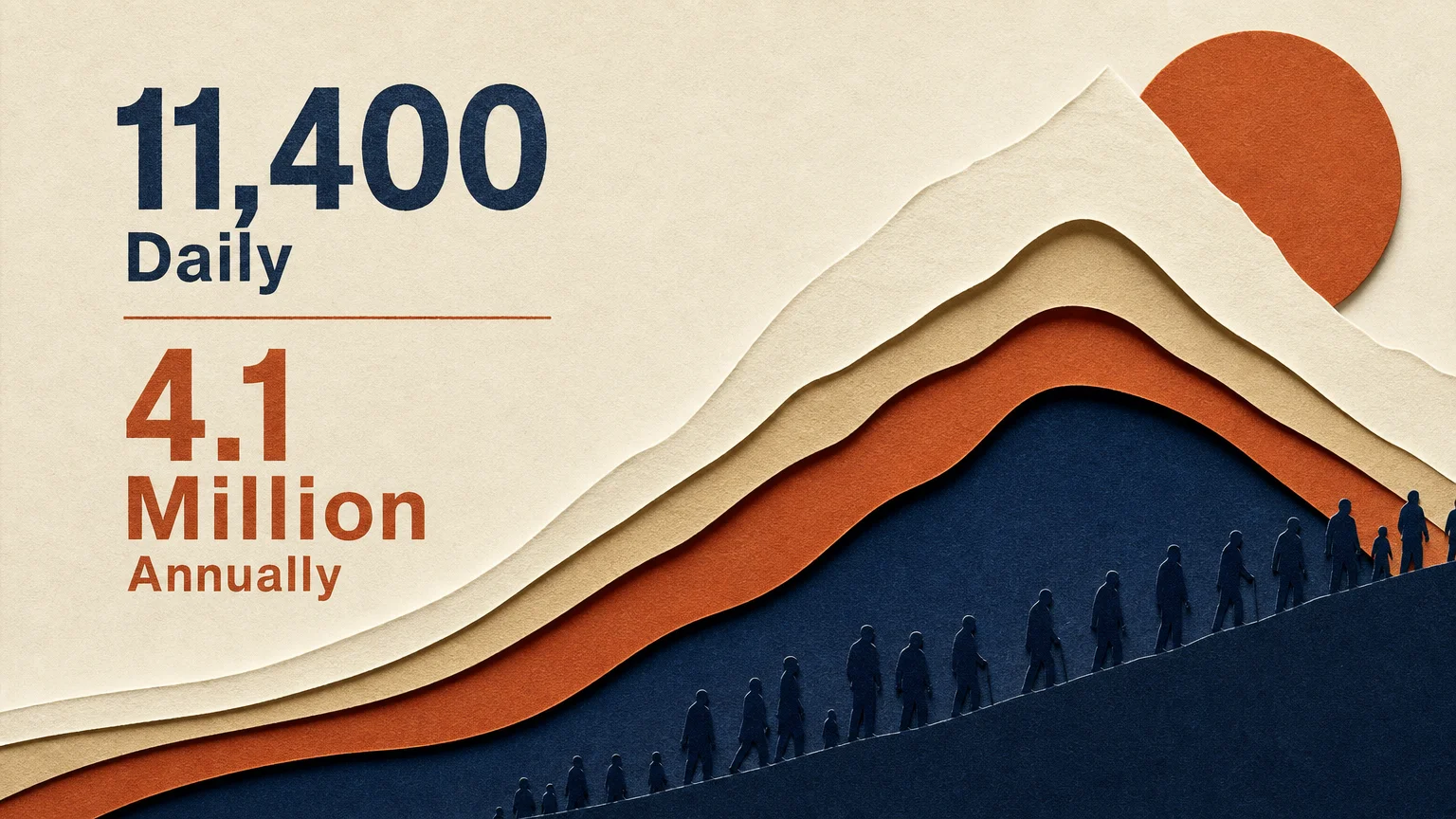

Every single day, roughly 11,400 Americans turn 65 and cross the threshold into traditional retirement age. This massive demographic shift—often called “Peak 65″—means over 4.1 million people will enter their retirement years annually between now and 2027. If you are part of this historic wave, understanding the exact number of your peers stepping away from the workforce is just the beginning. The real challenge lies in how this surge impacts the systems you rely on, from Social Security and Medicare to the healthcare industry and the broader economy. By looking at the hard data behind this retirement boom, you can make smarter, more confident decisions about your own financial timeline, health coverage, and long-term security.

Unpacking the “Peak 65” Phenomenon

Demographers and economists have anticipated this moment for decades, yet the sheer volume of individuals exiting the workforce still feels staggering. The United States is currently in the absolute thick of the “Peak 65” zone. Driven by the youngest cohort of the Baby Boomer generation, this four-year window from 2024 through 2027 represents the largest surge of retirement-age Americans in history. With an average of 4.18 million people turning 65 in 2026 alone, the economic landscape is rapidly shifting from a period of wealth accumulation to one of decumulation and distribution.

This daily wave of 11,400 new 65-year-olds changes the equation for everyone. Employers are facing unprecedented losses of institutional knowledge, while the healthcare system braces for increased demand. For you, as an individual navigating this transition, the most pressing concern is ensuring your personal savings can withstand the pressure of longer life expectancies and evolving government policies. The reality is that reaching age 65 today looks vastly different than it did for previous generations, largely because pensions have disappeared for most workers, leaving you solely responsible for bridging the income gap.

“Longevity Risk is the risk that we will outlive our money. The thing that we aspire most for our future, longevity, is the exact thing that most threatens our future…” — Jean Chatzky, Financial Editor

How the Retirement Surge Impacts Social Security

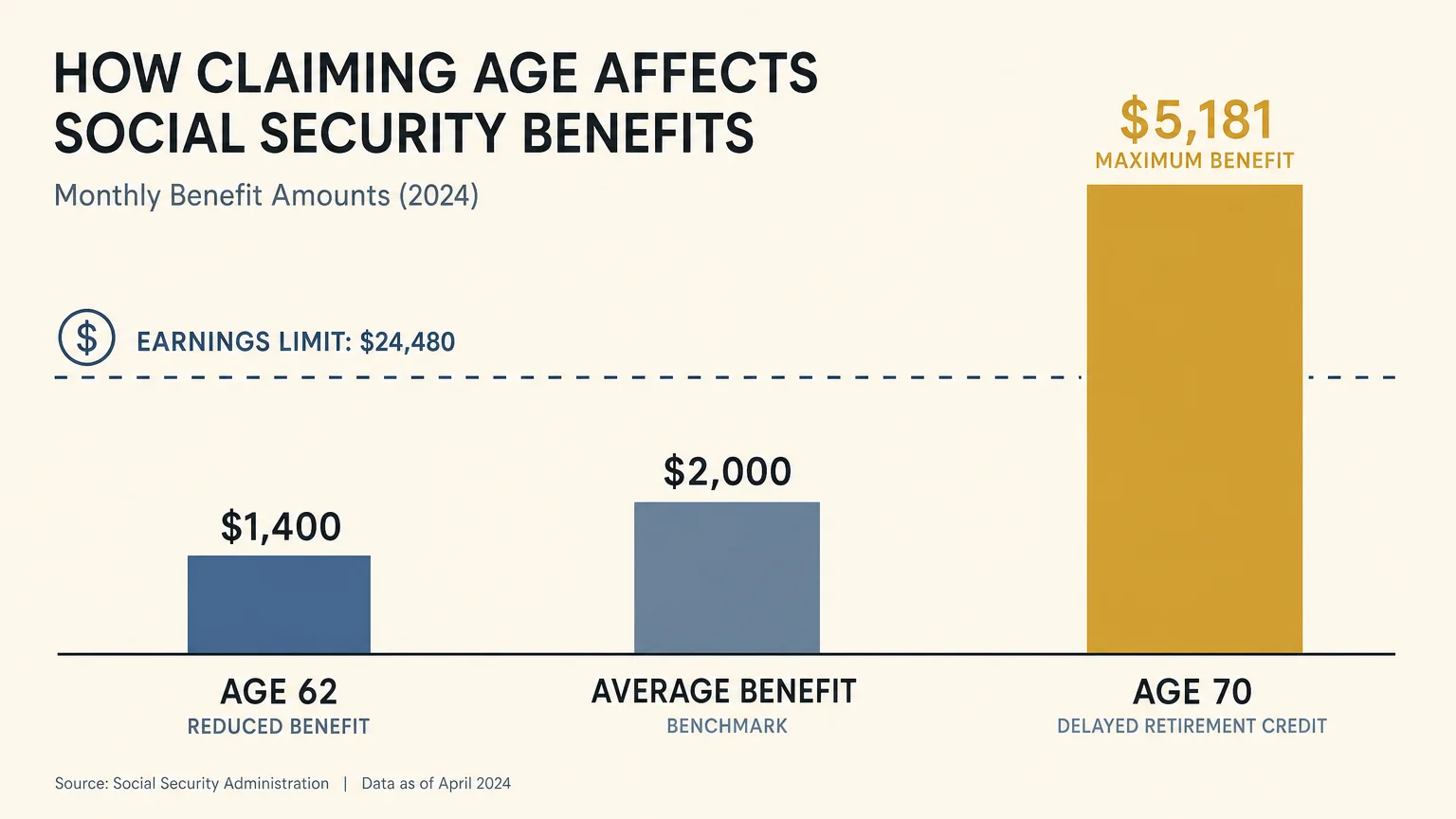

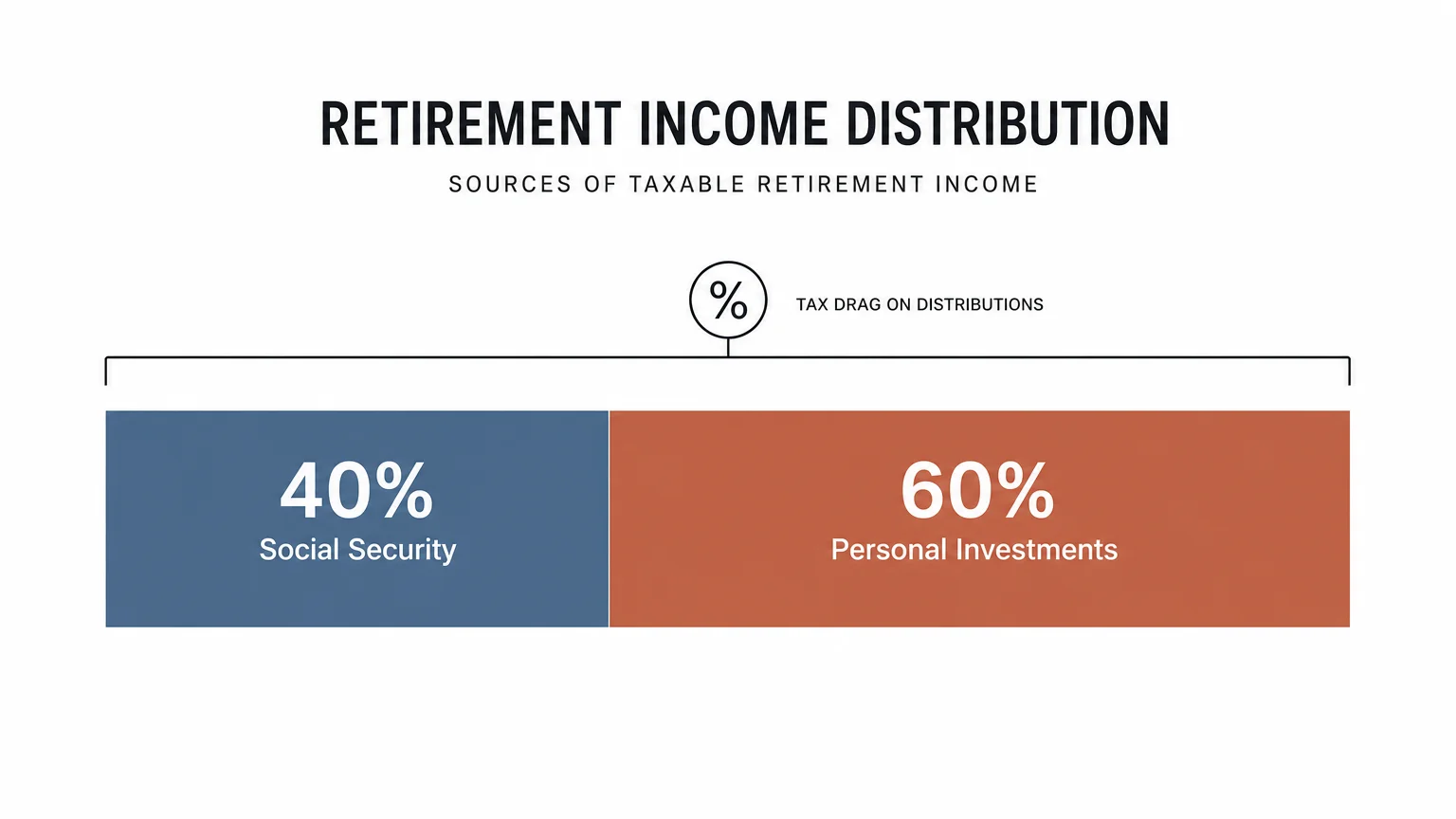

As millions of Americans transition from paying payroll taxes into the system to drawing benefits out of it, Social Security faces intense arithmetic pressure. In 2026, the average Social Security retirement benefit provides just a little over $2,000 per month. For many retirees, this amount serves as a vital foundation; however, it was never designed to replace your entire working income. Historically, Social Security replaces roughly 40 percent of pre-retirement earnings for the average worker, which means your personal investments must cover the remaining 60 percent.

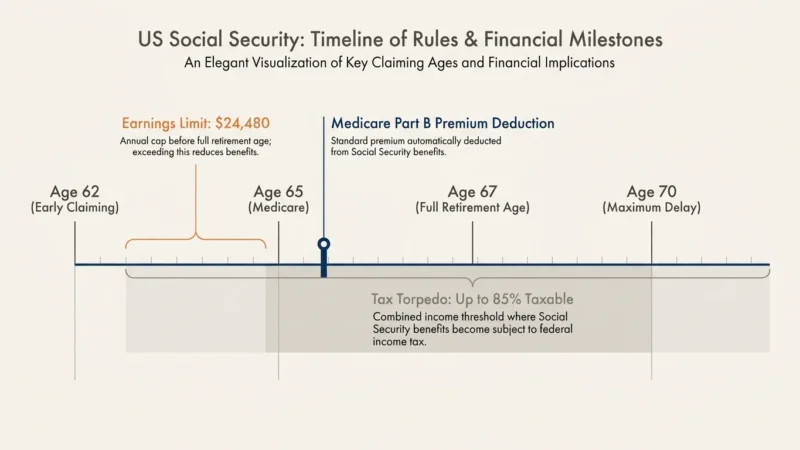

Because the system is feeling the strain of the Peak 65 wave, optimizing your claiming strategy has never been more critical. The exact age you decide to file for benefits dramatically alters your lifetime payout. While you can claim as early as age 62, doing so permanently reduces your monthly check. Conversely, if you have the financial stamina to wait until age 70, the maximum possible monthly benefit for a high earner reaches an impressive $5,181 in 2026.

If you choose to work while claiming early benefits, you must also navigate the retirement earnings test. The Social Security Administration (SSA) enforces strict caps on how much you can earn from a job before they begin withholding your benefits. For 2026, if you are under your Full Retirement Age (FRA) for the entire year, you can earn up to $24,480. Once your job income crosses that threshold, the government withholds one dollar in benefits for every two dollars you earn. During the specific calendar year you reach your FRA, the earnings limit jumps to a much more forgiving $65,160, and the penalty drops to one dollar withheld for every three dollars earned. Once you reach your FRA birthday month, the earnings limit disappears entirely, allowing you to earn as much as you want without any withholding.

Medicare Enrollment: A Daily Avalanche of Applications

The daily figure of 11,400 Americans turning 65 directly correlates to the number of people becoming eligible for Medicare every 24 hours. This massive influx of new beneficiaries dictates how the federal government sets premiums and deductibles. Unlike Social Security, which you can delay to increase your monthly payout, Medicare operates on a strict timeline; missing your Initial Enrollment Period can trigger permanent lifetime late-enrollment penalties.

Healthcare costs are steadily climbing, and the 2026 premium data reflects this ongoing trend. The standard Medicare Part B premium—which covers outpatient services and doctor visits—has increased to $202.90 per month in 2026. Simultaneously, the annual Part B deductible rose to $283. These increases are automatically deducted from your Social Security checks. While beneficiaries received a 2.8 percent Cost-of-Living Adjustment (COLA) for 2026, the sharp rise in Part B premiums essentially erodes a significant portion of that raise before the money ever hits your bank account.

Furthermore, if you built substantial wealth during your career, you will likely face the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge is based on a two-year lookback of your tax returns. If your income crosses specific thresholds, your Part B premium for 2026 could skyrocket to as high as $689.90 per month. Managing your taxable income in the years leading up to age 65 is essential to avoid these hidden healthcare surcharges.

Navigating Taxes in the Peak 65 Era

As the “silver tsunami” crests, the Internal Revenue Service is adjusting the tax code to accommodate an aging population, but the burden of planning falls squarely on your shoulders. Retirement changes how you are taxed, not necessarily how much you are taxed. Transitioning from a steady paycheck to withdrawing funds from a 401(k) or traditional IRA shifts your income into different tax brackets.

“We put money in 401(k)s and IRAs and we made that deal with the devil, with the government, saying ‘Alright, we’ll get a little tax break upfront each year.’ But then, as with any deal with the devil, there’s a day of reckoning.” — Ed Slott, CPA and Tax Expert

To help offset the tax burden for older Americans, the Internal Revenue Service (IRS) provides specific relief measures. For the 2026 tax year, the standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. However, once you turn 65, the tax code becomes a bit more generous. Single filers aged 65 and older receive an additional standard deduction of $2,050. Furthermore, new temporary legislation introduces a “Senior Bonus Deduction” of $6,000 for qualifying taxpayers 65 and older (subject to income phase-outs), offering a unique window to lower your taxable income substantially between now and 2028.

Understanding these updated standard deductions allows you to strategize your withdrawals. For example, if you keep your traditional IRA withdrawals below your total standard deduction limit—and you manage your capital gains properly—you can effectively pull money out of a tax-deferred account while paying zero federal income tax. This is where proactive tax planning separates those who merely survive retirement from those who thrive in it.

Rethinking the “Standard” Retirement Age

Despite the historic number of Americans reaching age 65, stopping work entirely is no longer the default path. Phased retirement—where you gradually reduce your hours rather than quitting abruptly—is gaining immense traction. Employers, desperate to retain the expertise of those 11,400 daily retirees, are increasingly open to flexible arrangements. Before handing in your notice, review how different transition strategies impact your finances.

| Retirement Strategy | Primary Income Source | Healthcare Coverage Status | Social Security Impact |

|---|---|---|---|

| Traditional Full Retirement | Withdrawals from 401(k)s, IRAs, and cash savings. | Must enroll in Medicare Part A and Part B at age 65 to avoid penalties. | Can claim immediately, though delaying to Full Retirement Age or age 70 maximizes the monthly benefit. |

| Phased Retirement (Part-Time) | A blend of part-time wages and initial portfolio withdrawals. | May transition to Medicare, or remain on employer insurance if the part-time role maintains benefits. | Must monitor the 2026 earnings limit ($24,480) if claiming benefits before Full Retirement Age. |

| Working Past 65 (Full-Time) | Continued salary and employer benefits. | Can typically delay Medicare Part B if covered by a creditable employer plan (usually 20+ employees). | Benefits continue to grow by 8% annually if delayed past Full Retirement Age, maxing out at age 70. |

Your timeline should be dictated by mathematics and personal fulfillment, not a societal expectation attached to your 65th birthday. If you enjoy your career, leveraging a phased approach allows you to keep your mind sharp while giving your investment portfolio a few extra years to compound untouched.

When DIY Isn’t Enough

While basic budgeting and straightforward portfolio management can be handled independently, the complexities of the Peak 65 era often require professional intervention. Consider seeking guidance from a fiduciary financial planner or tax professional in the following scenarios:

- You plan to execute large Roth conversions: Moving large sums of money from a traditional IRA to a Roth IRA triggers immediate taxes. A professional can help you navigate the 2026 tax brackets to ensure you do not inadvertently push yourself into a higher IRMAA penalty tier for Medicare.

- You own a small business: Selling a business or transitioning ownership at age 65 creates a massive liquidity event. Structuring this sale correctly is critical to minimizing capital gains taxes and protecting your wealth.

- You are coordinating spousal benefits: If you and your spouse have vastly different lifetime earnings records, calculating the optimal timeline for claiming Social Security survivor and spousal benefits requires sophisticated software and deep regulatory knowledge.

- You face a severe pension decision: Choosing between a lifetime monthly annuity payout or a lump-sum rollover from a corporate pension is an irreversible decision that dictates your sequence of returns risk for the rest of your life.

Avoiding Common Errors in the Peak 65 Era

When 4.1 million people navigate a complex transition simultaneously, bottlenecks and mistakes are inevitable. You can protect your nest egg by sidestepping the most frequent blunders made by new retirees.

- Assuming Medicare is completely free: Many retirees are shocked to discover that while Part A is generally premium-free, Part B carries a standard monthly premium of $202.90 in 2026, and Part D (prescription drugs) requires its own premium. Budget for these out-of-pocket healthcare costs immediately.

- Failing to file for Medicare on time: If you do not have qualifying health coverage through an active employer, you must sign up for Medicare during your Initial Enrollment Period. Missing this window results in a permanent 10 percent penalty on your Part B premium for every 12-month period you were eligible but did not enroll.

- Triggering the earnings test unexpectedly: If you claim Social Security at age 62 and take up a consulting gig that pays $40,000, you will blow past the $24,480 earnings limit for 2026. The SSA will aggressively withhold your benefits, causing sudden cash flow disruptions.

- Ignoring the two-year IRMAA lookback: Your 2026 Medicare premiums are based on your 2024 tax return. If you had an unusually high-income year two years prior to retiring, you must proactively file Form SSA-44 to request a reduction in your premiums based on a life-changing event (such as retirement).

Frequently Asked Questions

How many Americans retire each day?

Between 2024 and 2027, an average of 11,400 Americans turn 65 every single day. This demographic wave results in roughly 4.1 to 4.18 million people reaching traditional retirement age annually.

What is the average Social Security check in 2026?

Following the latest cost-of-living adjustments, the average Social Security retirement benefit in 2026 is slightly over $2,000 per month. However, individuals who earned a high income throughout their careers and delay claiming until age 70 can receive a maximum monthly benefit of $5,181.

How much can I earn while on Social Security in 2026?

If you have not yet reached your Full Retirement Age (FRA), you can earn up to $24,480 in 2026 without facing any withholding penalties. If you earn more than that limit, the SSA withholds $1 for every $2 earned above the threshold. During the year you reach FRA, the limit is $65,160.

What is the standard Medicare Part B premium for 2026?

The standard Medicare Part B premium for 2026 is $202.90 per month. High-income earners may pay significantly more—up to $689.90 per month—due to the Income-Related Monthly Adjustment Amount (IRMAA) surcharges.

The sheer volume of Americans entering retirement daily proves that you are part of a monumental generational shift. As the landscape of longevity, taxes, and healthcare continues to evolve, relying on outdated advice is the quickest way to jeopardize your financial security. By staying informed about the current 2026 thresholds for Social Security earnings limits, Medicare premiums, and standard tax deductions, you can construct a resilient retirement plan. Take the time to verify your earnings record at SSA.gov, review your healthcare options thoroughly at Medicare.gov, and consult with professionals through resources like the National Council on Aging when the math gets complicated. Your future self will thank you for the diligence you apply today.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.