Nearly three in ten adults aged 65 and older live alone, navigating retirement entirely on a single income. While glossy magazines promote remote beach towns and sprawling sunbelt communities as idyllic destinations, these locations are usually evaluated with couples in mind. When you rely on one Social Security check—which averages $2,071 in 2026—and face rising healthcare premiums alone, your geographic needs change dramatically. The wrong location can leave you isolated, financially strained, and miles away from essential support systems. To protect your independence and budget, you must look beyond generic retirement rankings. Here are seven popular relocation environments that frequently fail single seniors, along with the hidden risks you must evaluate.

1. Car-Dependent Sunbelt Sprawl

Retirees flock to the sunbelt for warm weather, abundant golf courses, and generally favorable tax policies. Developers respond by building massive subdivisions on the deep outskirts of cities like Houston, Phoenix, and Atlanta. For a married couple, these sprawling exurbs work reasonably well; if one partner experiences a decline in vision or mobility, the other can usually take over the driving duties. For a single senior, a car-dependent environment acts as a ticking clock on your independence.

Once you stop driving—whether due to macular degeneration, slowed reflexes, or medication side effects—you become completely reliant on others. Deep suburban exurbs rarely offer walkable grocery stores, robust public transit, or safe pedestrian infrastructure. You will bleed cash paying for ride-sharing services just to pick up prescriptions or attend doctor appointments. Relying on a fixed income leaves little room for a massive monthly transportation budget.

You must build your retirement strategy around walkability and transit access. Look for historic downtowns, inner-ring suburbs, or communities that offer dedicated senior shuttle services. If you cannot walk to a coffee shop, a pharmacy, or a community center from your front door, you risk severe isolation the moment you surrender your car keys.

2. Ultra-Expensive Coastal Enclaves

Areas like Naples, Florida, and Santa Barbara, California, offer stunning beaches, high-end dining, and world-class healthcare. They also demand premium prices that punish solo agers. Real estate professionals and financial planners often refer to this as the “singles penalty.” When a married couple buys a $600,000 beachfront condo, they utilize two lifetimes of wealth accumulation and two Social Security checks to cover the property taxes, insurance, and maintenance. You shoulder that entire financial burden alone.

Your tax situation also differs significantly from that of married peers. For the 2026 tax year, the standard deduction for a single filer sits at $16,100. If you are unmarried and 65 or older, you receive an additional $2,000 deduction, bringing your baseline standard deduction to $18,100. A married couple over 65 claims a much larger deduction, giving them a wider buffer against taxation on their combined income. This disparity leaves single seniors with less disposable income to handle the exorbitant costs of coastal living.

Coastal properties also carry the constant threat of massive homeowner association (HOA) special assessments. A $20,000 special assessment to replace a condo building’s roof might be manageable for a couple splitting the cost, but it can utterly destroy a single retiree’s emergency fund. If you desire coastal living, look for smaller, less trendy beach towns, or consider renting an apartment rather than buying property that ties up your liquidity and exposes you to unpredictable maintenance costs.

3. Remote Mountain Towns

Mountain towns in Colorado, Wyoming, and Idaho attract highly active retirees who love skiing, hiking, and pristine nature. The scenery is unmatched, but living solo at 8,000 feet introduces unique physical and logistical threats that compound as you age.

Snow removal requires intense physical labor. Shoveling heavy snow yourself invites severe cardiovascular stress and back injuries; hiring a private plow service eats away at your monthly budget. Home maintenance in extreme weather is relentless and unforgiving. Pipes freeze, roofs leak under heavy snow loads, and power outages happen frequently. Managing these crises without a partner creates immense physical and emotional stress.

“Ongoing maintenance is a must, even when you have no intention of moving. Taking care of your home today is how you avoid even higher costs later on.” — Suze Orman, Personal Finance Expert

Additionally, high altitude naturally exacerbates cardiovascular and respiratory conditions. If you need emergency care during a blizzard, an ambulance might not reach you in time. Relocate to a mountain town only if you rent a fully maintained condo, utilize a property management service, and have a rock-solid plan to migrate to lower elevations if your health suddenly declines.

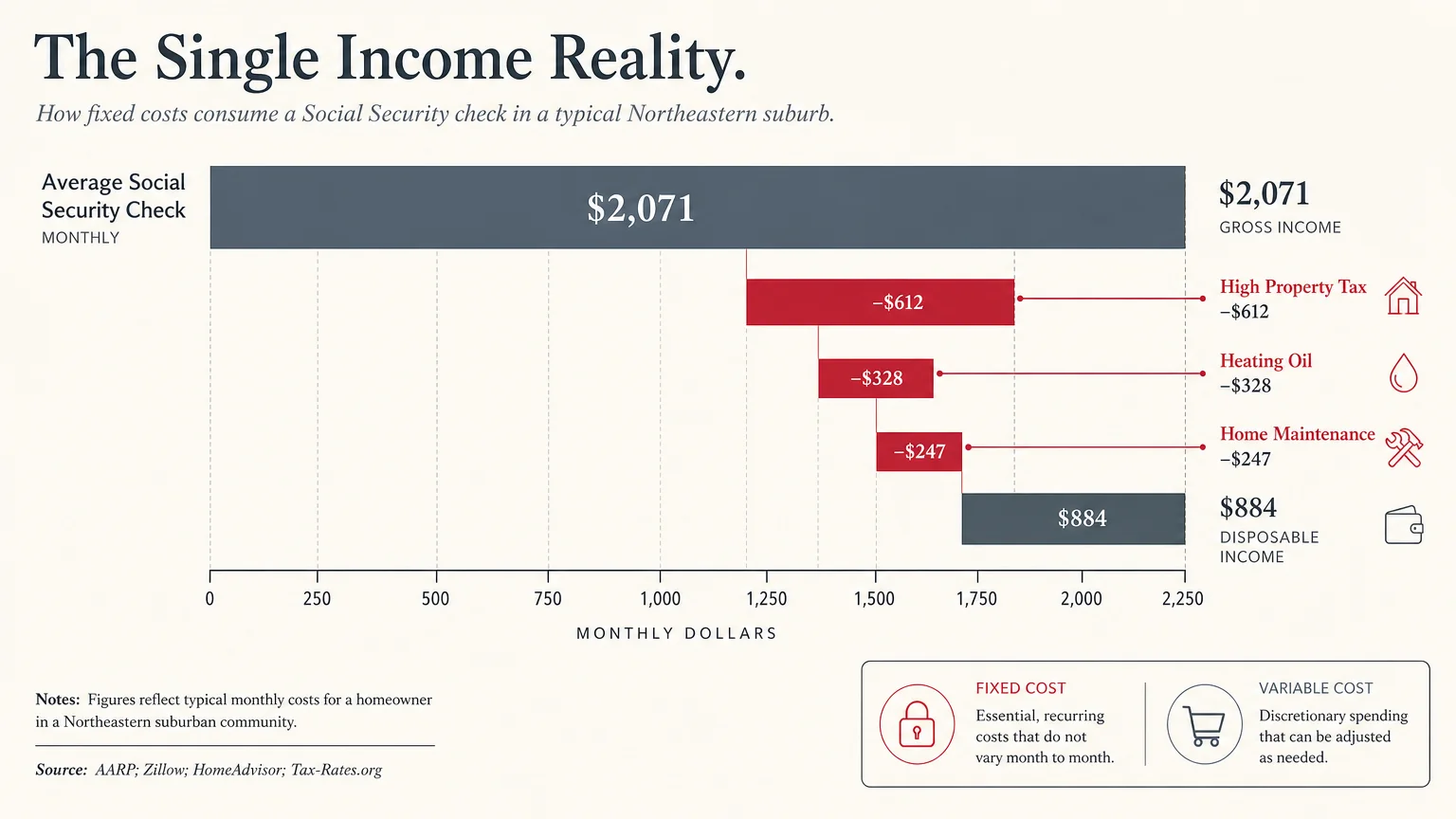

4. High-Tax Northeastern Suburbs

Counties in New York, New Jersey, and Connecticut feature excellent hospital systems, beautiful changing seasons, and proximity to major cultural hubs. Unfortunately, they also levy some of the highest property taxes in the nation. School districts, road maintenance, and local municipal services rely heavily on property tax revenue, meaning your tax bill will climb steadily year after year, regardless of what the broader economy does.

Single seniors on fixed incomes simply cannot absorb a $15,000 annual property tax bill without compromising other essential expenses like food, utilities, and healthcare. Furthermore, these specific suburbs frequently zone strictly for large, single-family homes. You will struggle to find a modest, single-story patio home or an affordable one-bedroom condo in the same town where you raised your family. This forces many singles to maintain a four-bedroom house they no longer need, simply because downsizing options do not exist locally.

Before you commit to a high-tax area, you must thoroughly evaluate your projected income. Visit the Internal Revenue Service website and your state’s department of revenue to fully understand how your specific retirement income—including pensions, IRA withdrawals, and Social Security—will be taxed. Often, the math simply does not work for a single individual.

5. Couples-Centric Mega-Communities

Master-planned retirement megacities offer hundreds of social clubs, pristine golf courses, and endless scheduled activities. You might logically assume these vibrant communities cure loneliness and provide the ultimate social safety net. In reality, single residents frequently report feeling alienated and marginalized.

These environments revolve heavily around couples. Dance classes, golf scrambles, dinner parties, and neighborhood events naturally default to pairs. If you are single, breaking into established couples’ cliques requires exhausting, continuous effort. When everyone else is navigating retirement alongside a spouse, your single status becomes glaringly obvious, sometimes leading to unintentional exclusion.

Recent data indicates that approximately 33% of older adults experience loneliness and isolation. Moving to a massive community where you feel like a constant third wheel will only amplify that isolation. Instead of a couples-dominated megacity, look for diverse, multi-generational neighborhoods or co-housing communities where social structures foster genuine connection regardless of marital status. Naturally Occurring Retirement Communities (NORCs)—urban or suburban neighborhoods where residents simply age in place together over decades—often provide more authentic support systems for single adults.

6. Hurricane-Prone Barrier Islands

The barrier islands of the Carolinas, the Gulf Coast, and the Florida Panhandle offer incredible oceanfront living and a laid-back lifestyle. They also sit directly in the crosshairs of severe seasonal weather. Preparing a home for a Category 3 hurricane requires intense physical labor and rapid execution.

You must move heavy patio furniture indoors, install heavy storm shutters, secure loose debris, and pack emergency survival supplies. Executing these tasks alone is dangerous and sometimes physically impossible for an older adult. Evacuation poses another massive hurdle. Driving for twelve hours in gridlocked traffic causes extreme fatigue, and paying for emergency hotel stays out of your own pocket drains your cash reserves rapidly.

Post-storm recovery involves fighting with insurance adjusters, managing contractors, and living in temporary conditions—stressful tasks that benefit immensely from a partner’s emotional and logistical support. If you lose power for a week, you have no one to help you manage food spoilage or heat exhaustion. Single seniors should prioritize inland communities that offer the charm and warmth of the South without the catastrophic, recurring weather risks.

7. Deep Rural “Off-the-Grid” Retreats

The dream of buying ten acres in the woods to enjoy absolute peace, quiet, and nature appeals to many newly minted retirees. You can garden, read, and escape the noise of the modern world. However, for a single senior, this deep isolation creates a dangerous vulnerability as the years advance.

Rural areas suffer from a severe and growing shortage of medical professionals. The standard Medicare Part B premium costs $202.90 per month in 2026, and the annual deductible is $283. You pay for this federal coverage regardless of where you live, but in a remote rural area, you extract far less value from the system. You might have to drive two hours each way just to see an in-network cardiologist or rheumatologist.

Aging in place safely requires immediate community support. If you fall and break a hip in a remote cabin, you might wait hours for emergency services to arrive. If you want a slower pace of life, seek out small, rural-adjacent towns that still maintain a central hospital, a grocery store, and nearby neighbors who can check on you during emergencies.

What Can Go Wrong: The “Singles Tax” in Retirement

When you relocate as a single senior, you must account for the “singles tax”—the invisible financial penalty you pay for not splitting living costs with a partner. You buy the same refrigerator, pay the same internet bill, and heat the same living room as a married couple, but you fund it entirely yourself. This financial dynamic fundamentally changes which locations are truly affordable.

| Expense Category | Married Couple Strategy | Single Senior Challenge |

|---|---|---|

| Housing & Real Estate | Split rent or mortgage payments using two income streams. | Bears 100% of housing costs on a single fixed income. |

| Utilities & Maintenance | Shared usage reduces the per-person cost of living. | Pays the full base rates for internet, water, trash, and heating. |

| Healthcare Logistics | Spouses provide free in-home caregiving and transportation after surgery. | Must hire professional home health aides and pay for medical transport. |

| Tax Burden | Higher joint deduction thresholds and shared tax preparation costs. | Lower single standard deduction limit and fewer opportunities to shift taxable income. |

To offset these costs, single seniors must get creative. Consider relocating to a town with a strong co-housing movement, exploring house-sharing arrangements (popularly known as “Golden Girls” living), or choosing a smaller footprint in a highly walkable, amenity-rich neighborhood where you do not need to pay for a car.

When to Consult a Professional

Because you are managing your financial and physical future entirely on your own, making a relocation mistake carries a heavy penalty. You should consult a fee-only fiduciary financial advisor or a senior relocation specialist in the following scenarios:

- Evaluating Out-of-State Taxes: Moving across state lines triggers complex tax changes. A professional can help you understand how your new state taxes Social Security, pensions, and property.

- Planning for Long-Term Care: Without a spouse to act as a default caregiver, you must have a bulletproof long-term care strategy. You need to know how Medicaid rules apply in your target state if you deplete your assets.

- Executing a Downsize: Selling a family home and buying a smaller property in a new city involves significant closing costs, capital gains considerations, and logistical hurdles.

“Good financial planning can help you prepare for everything from an economic recession to an unexpected family emergency.” — Jean Chatzky, Financial Editor

Frequently Asked Questions

What is the biggest financial mistake single seniors make when relocating?

The most common mistake is failing to account for the cost of future care. Single seniors often buy a home based solely on their current health and active lifestyle. When mobility declines, they are forced to sell the home prematurely and move again to access assisted living or walkability, absorbing massive real estate transaction fees twice in one decade.

How can single seniors offset the high cost of housing in retirement?

House-sharing is becoming increasingly popular among single retirees. By splitting a larger home with another single senior, you cut your housing, utility, and maintenance costs in half while gaining a built-in emergency contact. Alternatively, prioritizing smaller condos in mid-sized, tax-friendly cities allows you to stretch your savings further.

Does Medicare cover transportation to medical appointments if I can no longer drive?

Original Medicare generally does not cover non-emergency transportation to routine doctor appointments. If you lose your ability to drive and live in a car-dependent suburb, you will have to pay out-of-pocket for taxis, ride-shares, or private medical transport. Some Medicare Advantage plans offer limited transportation benefits, but these vary wildly by zip code and provider.

Finding the right location as a single senior requires ruthless pragmatism. You must look past the scenic views and marketing brochures to evaluate a town’s walkability, tax structure, healthcare accessibility, and housing inventory. By prioritizing your independence and protecting your budget, you can find a community that truly supports your solo retirement journey.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, savings, health coverage, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: February 2026. Retirement benefits, tax laws, and healthcare costs change frequently—verify current details with official sources.